Michael Vi

Michael Vi

If you're in my camp, you're probably looking at the S&P 500 sitting at 5,100 and thinking: is there anything left I can buy without paying an egregious valuation multiple for? The answer is certainly yes, but we have to focus on relatively unpopular corners of the tech sector for these plays. I continue to maintain the position that "growth at a reasonable price" will be a winning strategy for 2024. We've already seen a number of beaten-down names advance sharply this earnings season (Pure Storage (PSTG), C3.ai (AI), and Okta (OKTA) come to mind) - investors just have to be patient for these rebounds.

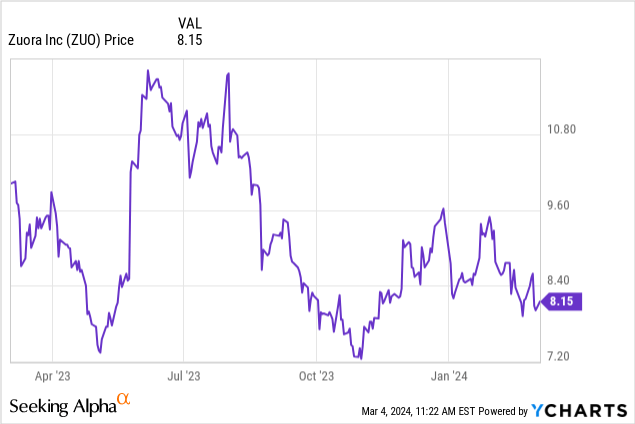

Zuora (NYSE:ZUO), in my view, is bound for a similar rebound, though admittedly this stock has required a bit of patience. A software company dedicated to revenue management tools for fellow subscription companies, Zuora has seen its share price drop nearly 10% year to date (though many of its peer software companies have seen double-digit gains), with losses picking up after the company's recent Q4 earnings release.

I last wrote a bullish note on Zuora in December, when the stock was trading at $9 per share. Since then, Zuora has only seen further declines while the rest of the market has soared, even while the company has reported relatively strong results that featured sizable boosts to operating margins. It's this focus on profitability amid consistent, if unexciting growth, that leads me to believe Zuora remains a high-quality M&A target. But even with or without the prospect of a takeover deal, I remain very bullish on Zuora for the remainder of this year.

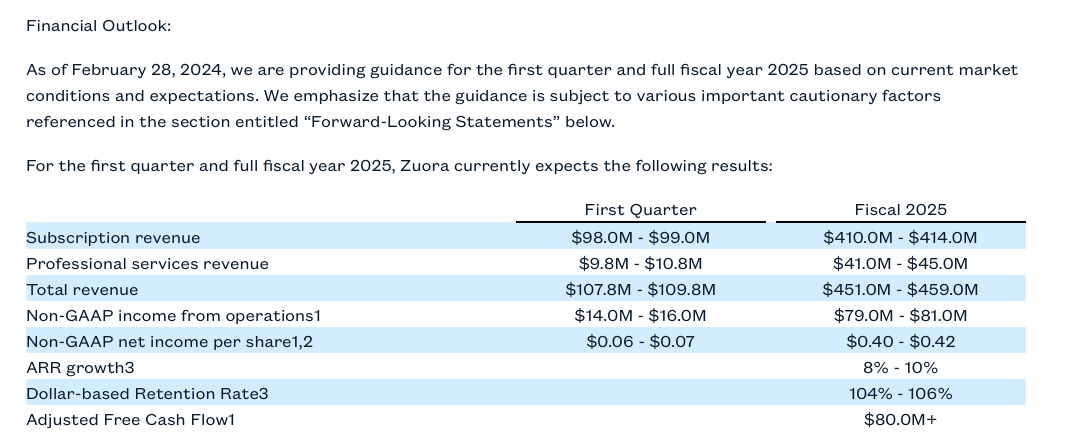

When considering Zuora's outlook for the current year, we have to remember that even though the company is facing macro pressure like most of its software peers, where Zuora really excels is in bolstering its bottom line. It scored more than ten points of y/y pro forma operating margin expansion and is set to continue expanding profits in FY25. Take a look at its guidance below:

Zuora guidance (Zuora FY24 outlook)

Pro forma operating margins are set to expand to 18% (and on a nominal basis, nearly double from FY23's ~$47 million), up from 11% in FY24 and just 1% in FY23. The company is still expected to grow ARR at an 8-10% clip, and I also think there's room in the company's dollar-based net retention rate. Retention rates saw pressure this year as companies shrunk headcount and monitored spending on IT, but with lower expansion trends this year, Zuora has easier comps in FY25 - and so the prospect of dollar-based net retention rates falling to 104-106% from Q4's 108% rate is probably too conservative.

At current share prices near $8, Zuora trades at a market cap of just $1.15 billion. Its enterprise value, after netting off $514.2 million in cash and $359.5 million in debt, is even lower at just $995 million. Taking guidance midpoints at face value, this puts Zuora's valuation multiples at:

Here are all the long-term reasons to be bullish on Zuora:

Stay long here and use the post-earnings dip and very low valuations as an opportunity to buy Zuora. In my view, any whiff of positive news (accelerating growth or expansion rates; or any signs of acquirer interest) will send Zuora soaring.

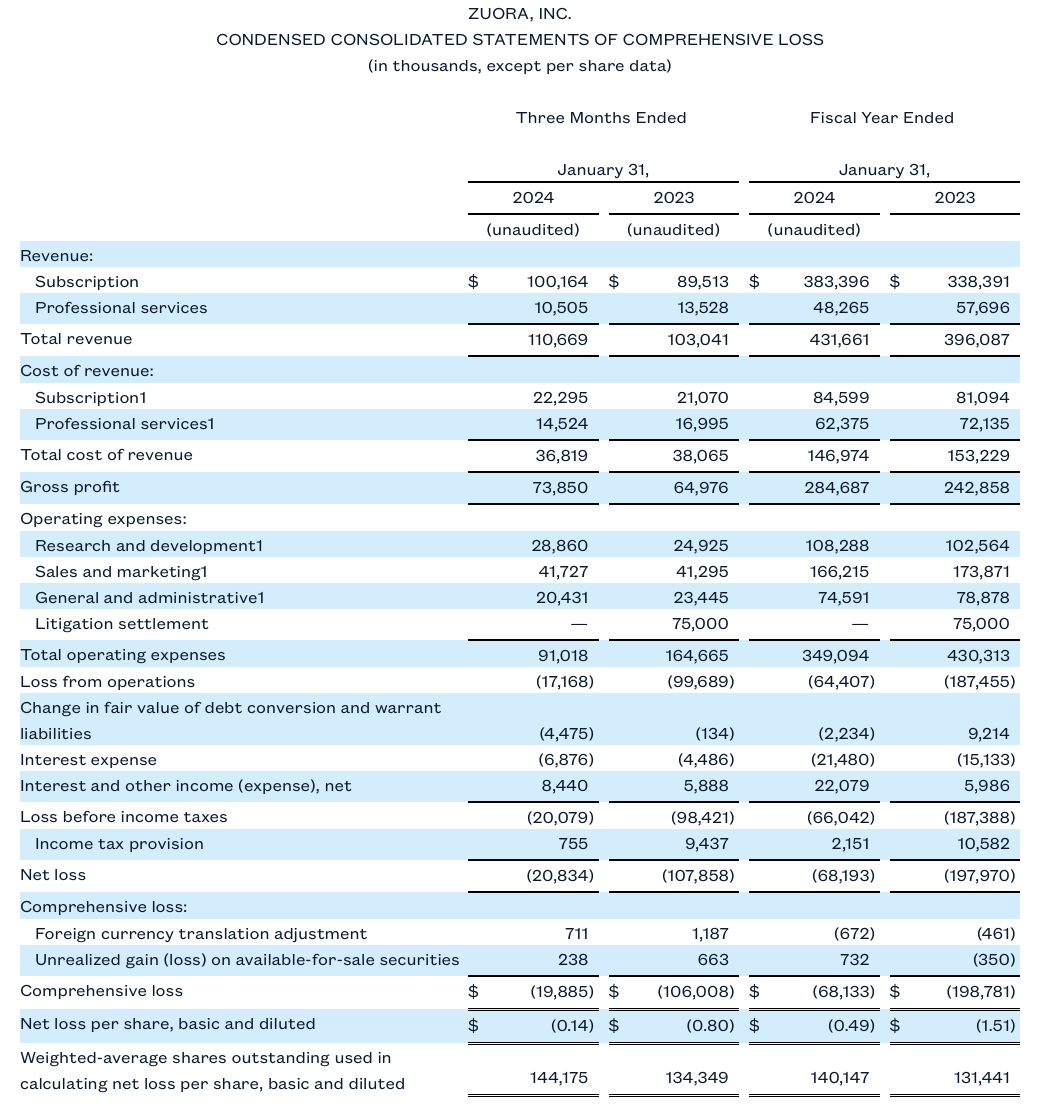

Though nothing to write home about, Zuora's Q4 results showed a business that is continuing to execute consistently well and improving on profitability. Take a look at the Q4 results below:

Zuora Q4 results (Zuora Q4 earnings release)

Revenue grew 7% y/y to $110.7 million, in-line with Wall Street's expectations but unfortunately decelerating two points from Q3's 9% y/y growth pace. In spite of the weaker top-line metrics, we note that dollar-based net expansion rates still remained healthy at 108% (indicating a net 8% upsell and that existing customers are still spending more than enough to offset churn). The company also had a number of notable go-lives in the quarter, including with restaurant point-of-sale vendor Toast (TOST); and in addition, the company deepened its cross-selling relationship with fellow mid-market software company Avalara, which focuses on automating sales tax compliance.

In light of the tougher macro environment and the greater scrutiny on enterprise deals, Zuora smartly shifted its go-to-market focus on smaller wins with the hope of "landing and expanding" over time. Per CEO Tien Tzuo's remarks on the Q4 earnings call describing this strategy (key points bolded for emphasis):

To put all this in context, let's go back to the start of the fiscal year. Like many other companies, one year ago, we were seeing signs of a general slowdown in IT spending. Many expressed that the office of the CFO was an area that could be affected. And there's a general consensus that there was going to be a slowdown in the digital transformation projects that have driven technology spending over the previous few years.

And so we adjusted. Specifically, we said we would do two things. First, as we've been highlighting in the last few earnings calls, we shifted to doing faster lands at a lower ACV. So of course, still focused on what we believe is the sweet spot of the market, large enterprises and fast-growing disruptors, in other words, the leaders of today and of tomorrow.

Second, we said we would strike a good balance between growth and profitability, and we committed to making progress towards the Rule of 40 framework. As it turns out, this was the right approach. As the year progressed, we did indeed see a pause in digital transformation projects. In FY '24, we saw fewer 7-digit ACV new logo deals. And in Q4, we did see these deals continue to push.

However, our strategy of pursuing smaller, faster lands allowed us to sign almost 30% more new logos in fiscal '24 as compared to the previous year. In fact, if you just look at Q4, we signed on over 40% new logos compared to Q4 of last year [...] We also saw sales cycles shorten. In fact, when I look at new logo deals between 100k and 500k ACV, these deals closed 25% faster as compared to FY '23."

Now, we can look at this shift downmarket in two ways. On the more conservative angle, we could say that smaller companies and smaller trials may lead to more churn down the line, as smaller companies are more likely to either run out of business or switch software providers without too much bureaucratic slowdown.

But the same also holds true in reverse: smaller companies have much more room to expand their usage of Zuora over time. The company's larger pipeline of expansion-ready customers may help net revenue retention rates to increase over time.

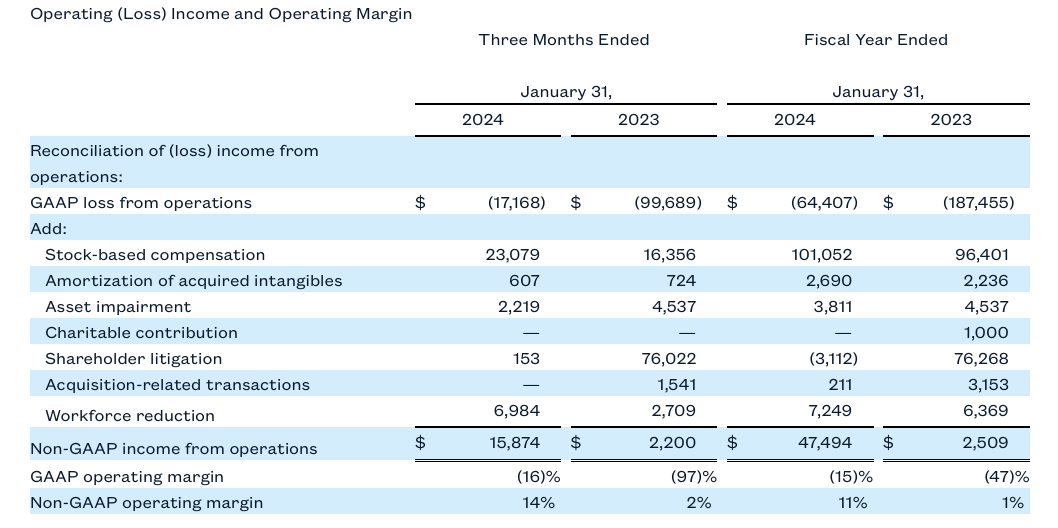

Meanwhile, Zuora continues to make solid progress on profitability, the result of continued headcount trimming (with the latest announcement to cut 8% of its global workforce).

Zuora margins (Zuora Q4 earnings release)

As shown above, pro forma operating margins zoomed to 14% in Q4, up 12 points y/y. The company is continuing to expect pro forma operating profit dollars to nearly double in FY25, sending the market a signal that even though the company is only clocking in single-digit revenue growth, it is still capable of delivering outsized profitability gains.

No, Zuora isn't perfect. Its growth rates compare poorly against most growth software stocks - and yet, the company has charted out its own path to success, focusing on smaller and lower-effort deal closings with the hope of expanding these clients' business over time. Trading at cheap multiples of both revenue and FCF, I'd say this stock is more than worth the benefit of the doubt.