Analysts Have Been Trimming Their Zuora, Inc. (NYSE:ZUO) Price Target After Its Latest Report

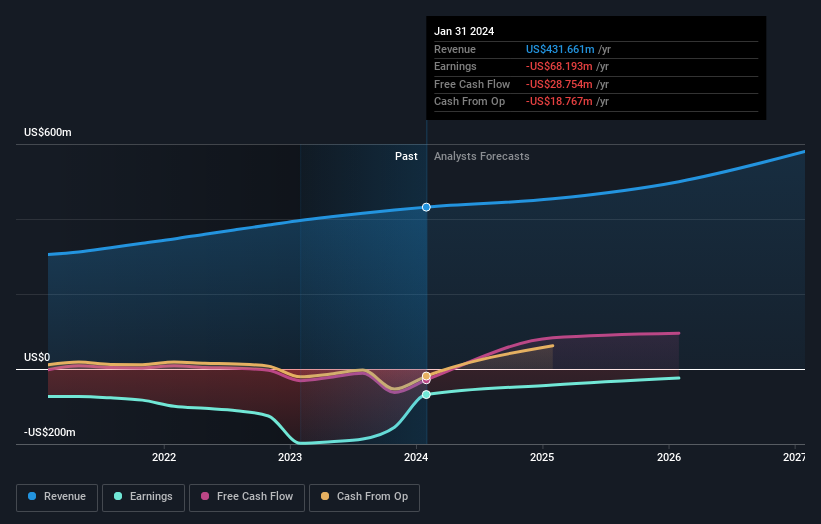

Shareholders might have noticed that Zuora, Inc. (NYSE:ZUO) filed its annual result this time last week. The early response was not positive, with shares down 2.2% to US$8.01 in the past week. The statutory results were mixed overall, with revenues of US$432m in line with analyst forecasts, but losses of US$0.49 per share, some 2.1% larger than the analysts were predicting. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

See our latest analysis for Zuora

Taking into account the latest results, the current consensus from Zuora's six analysts is for revenues of US$453.7m in 2025. This would reflect an okay 5.1% increase on its revenue over the past 12 months. Losses are predicted to fall substantially, shrinking 42% to US$0.28. Before this earnings announcement, the analysts had been modelling revenues of US$471.7m and losses of US$0.36 per share in 2025. Although the revenue estimates have fallen somewhat, Zuora'sfuture looks a little different to the past, with a very favorable reduction to the loss per share forecasts in particular.

The consensus price target fell 7.4% to US$11.57, with the dip in revenue estimates clearly souring sentiment, despite the forecast reduction in losses. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. There are some variant perceptions on Zuora, with the most bullish analyst valuing it at US$15.00 and the most bearish at US$8.00 per share. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. We would highlight that Zuora's revenue growth is expected to slow, with the forecast 5.1% annualised growth rate until the end of 2025 being well below the historical 12% p.a. growth over the last five years. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 12% per year. So it's pretty clear that, while revenue growth is expected to slow down, the wider industry is also expected to grow faster than Zuora.