FatCamera

FatCamera

In my last article, I mentioned my desire to reduce (and potentially, eliminate) my exposure to bio-pharma companies. So, the fact that I’m writing a bullish piece on Zoetis Inc. (NYSE:ZTS) here might come as a surprise. But, in today’s report I’m going to discuss why I view Zoetis in a more positive light than other, better known, healthcare stocks such as Amgen (AMGN), Johnson and Johnson (JNJ), and Pfizer (PFE).

Simply put, since spinning off from Pfizer, Zoetis has produced very unique compounding results which have set the company apart from other human-centric bio-tech/bio-pharma companies.

Zoetis has posted positive annual EPS growth every year since its 2013 spin-off.

ZTS’s average annual EPS Growth rate since becoming a public company is 15.9%.

This has allowed the company to produce dividend growth CAGR of nearly 25% since 2013.

That fundamental growth/dividend growth performance makes ZTS one of the highest dividend growth stocks in the entire market over the last decade or so.

What’s more, this isn’t just an income play. ZTS has outperformed the S&P 500 (SP500) by a wide margin during the last decade, posting price returns of 492% versus the S&P 500’s 176% gains.

Simply put, this stock checks all of the boxes that I’m looking for in a dividend growth stock and, therefore, ZTS is a company that I’m happy to continue to accumulate, despite wanting to trim/sell several of its peers.

The fact is, people are extremely lonely these days.

Loneliness is becoming a big problem for society, and the lack of meaningful human connection is driving demand for companion animals.

Last year, the US Surgeon General, Dr. Vivek Murthy, called loneliness an epidemic, noting that it is very detrimental to both physical and mental health, contributing to increased risk of heart disease, stroke, dementia, and premature death.

A paper by Ian Marcus Corbin and Joe Waters written in response to Murthy’s claims states, “Lack of social connection, according to one dramatic formulation, has been found to be as dangerous as smoking up to 15 cigarettes a day.”

And while data shows that younger generations are suffering the most from this issue, this is a growing issue across all age groups right now.

A 2020 Harvard study noted that 61% of young adult felt “serious loneliness.”

51% of mothers with young children also reported loneliness as a major problem.

Overall, the Harvard study reported that 36% of Americans suffer from loneliness and since the pandemic, this problem has only gotten worse.

This isn’t just a societal issue…there’s an argument to be made that this is a leading issue for the long-term survival of our species.

A study by Scientific American notes that this loneliness problem isn’t just about the lack of social interaction, but ultimately, reproduction.

According to the study, during the last 15 years or so there has been a significant decrease in sexual activity, both partnered and solo, amongst both men and women, ages 19-49.

I’ll be honest, when I began writing this report on an animal healthcare company, I had no idea that I’d end up reading abstracts about sexual trends and how this could potentially lead to extinction…but that’s due diligence for you.

I won’t break down the data here, but If you’re interested in learning more about these trends, here’s a scientific report which breaks down the recent trends spotted in sexual behavior in great detail.

In short, things like video games and social media are transforming (and meaningfully reducing) sexual desire.

Technology is distorting the way that humans interact.

Digital escapism is an easy avenue for young people to take when it comes to boredom…but this quick fix leads towards longer-term issues with regard to a lack of in-personal interaction and relationship building.

This is sad, disturbing, and morbid, I know. And I don’t have the slightest idea how to solve this issue. But as an investment analyst, I do know how to profit from it…

That’s one silver lining (especially if you’re someone who believes that money can buy happiness).

The answer is simple: pets.

Companion animals, whether we’re talking about dogs, cats, birds, fish, reptiles, and a number of other small creatures, are where lonely people are turning for love and affection.

As our collective love for these animals grows, so does our pet-related spending.

This was a trend that was building pre-pandemic and in recent years its prevalence has increased.

I know that people love to hate Jim Cramer…and I know that his stock picks aren’t always great. But, one thing that Jim nailed was the “humanization of pets” trend.

He was banging the table about this investment trend prior to the pandemic.

Back in 2017, he called it one of the greatest investment themes in the market.

He was talking about people bringing animals out of dog houses and into their beds.

He was talking about the growing health foods trend…and how this heightened awareness was trickling down to companion animals as well.

Well, Cramer was spot on.

Since then Zoetis is up roughly 220%.

And the demand trends that served as the fuel for this growth remain in place.

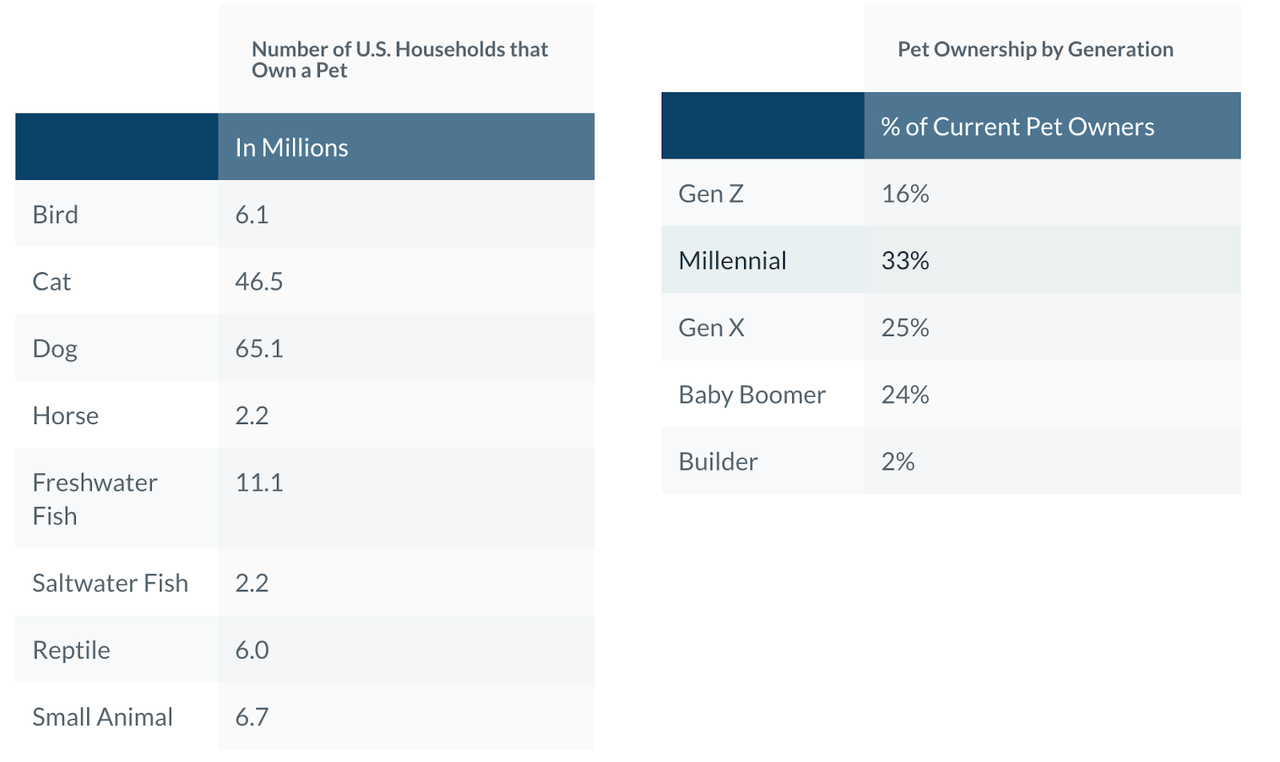

The American Pet Products Association’s (APPA) 2023-2024 Pet Owners Survey noted that 66% of U.S. households (nearly 87 million) own pets.

APPA: Industry Trends and Stats

As you can see, pet ownership amongst the younger generations is very high, which coincides with that loneliness epidemic theory.

But, it’s not just young people who’re finding meaningful connections with pets.

The silver tsunami is one of the largest demographic trends that America is facing right now.

A recent Forbes article noted that since 2010, there have been roughly 10,0000 people turning 65 years old a day. Well, many of these elderly individuals are finding comfort in pampering their pets.

And as you can see, Baby Boomers make up 24% of U.S. pet ownership.

Gen X is the second largest cohort of pet owners, which makes sense, since these people are typically empty nesters now (unless, of course, they have a lonely millennial living in their basement).

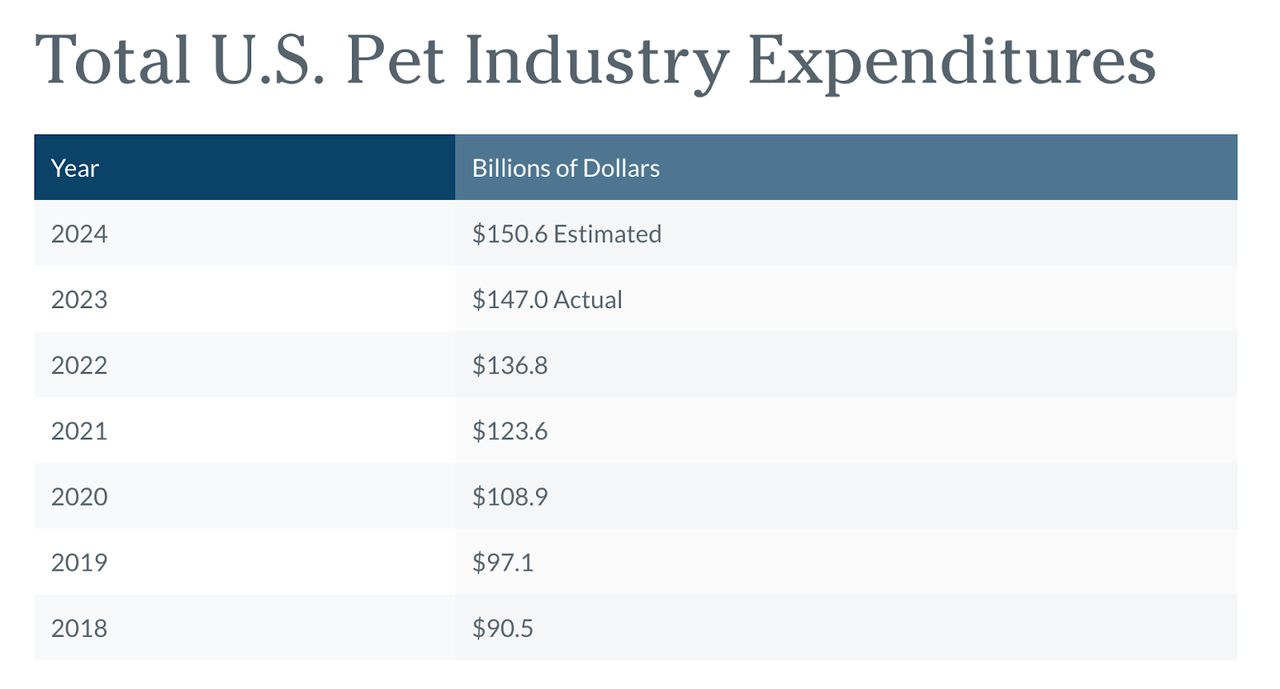

This widespread ownership and increasing welfare of companion animals is leading to big spending in the pet industry.

APPA: Industry Trends and Stats

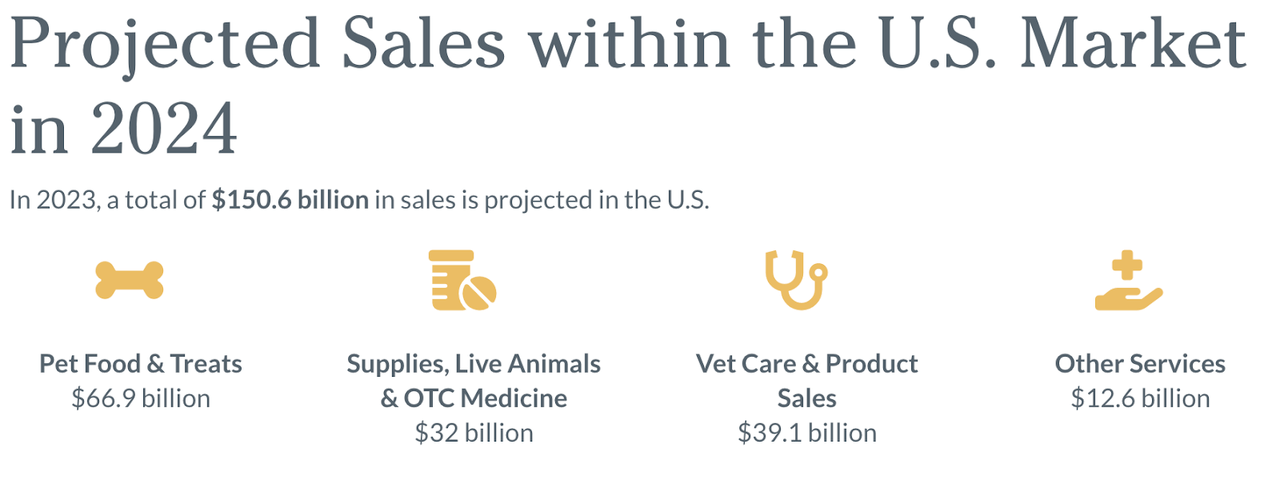

As you can see, this is expected to be a $150b+ industry in 2024…and the vast majority of this spending isn’t going to be directed towards chew toys, but instead, healthcare.

According to the APPA, roughly 56% of that $150b in sales will be directed towards healthcare and wellness.

APPA: Industry Trends and Stats

And as the undisputed king of animal health, Zoetis is set up nicely to be a major beneficiary of these trends.

One of the benefits of the animal health market, as opposed to the human health market, is the increased pricing power by drug makers because drug prices aren’t determined by regulation, government buyers, PBM’s, or other large-scale managed care firms that buy in bulk.

The buyer situation is much more fragmented in the animal care space.

There are large protein producers who buy at scale due to the industrial nature of their agriculture infrastructure, but historically they’ve still been willing to pay premiums for trusted, name brand drugs because when maintaining a healthy herd is your livelihood, it’s simply not worth taking the chance with an unknown drug/antibiotic.

And in the pet space, there aren’t really PBM’s in place for the owners of companion animals or veterinarians to use.

Because the animal health space is less competitive than the bio-tech/pharma space for humans, many of the leading animal health products lack generic competition.

CFRA’s Business Summary of ZTS states:

“At present, we do not believe there is a well-capitalized generic animal pharmaceutical producer operating on a global scale to compete with ZTS. Nor do we expect one to emerge due to unique barriers to generic entry in the animal pharmaceutical business.”

This leads to higher margins for companies like ZTS (compared to human bio-pharma peers). It also provides longer growth runways for established drugs than we see in the human health market because successful animal drugs don’t often face stringent competition from generics/biosimilars.

Furthermore, not only does Zoetis have unique pricing power, it also benefits from secular growth trends due to the ongoing rise in popularity of pets.

No, you’re not going to find the explosive growth that big-pharma stocks like Eli Lilly (LLY) or Novo Nordisk (NVO) are offering right now on the backs of their GLP-1 success in the animal health market.

The total addressable market ("TAM") for big oncology, diabetes, obesity, Alzheimer’s, etc., drugs is going to dwarf the pet health market.

But, these massive TAMs breed intense competition…which Zoetis doesn’t face.

Zoetis generated $8.5 billion in sales in 2023.

These sales grew by 5.7% on a y/y basis.

Merck (MRK) has an animal health business that is probably ZTS’s most formidable competitor. MRK’s Animal Health segment posted $5.6b in sales in 2023, up by 1% on a y/y basis.

Elanco (ELAN) is ZTS’s closet peers in terms of being a pure-play in the animal health space, but it’s 2023 sales were only $4.4b.

And, from a profitability standpoint, ZTS’s gross margin figures put ELAN’s to shame.

During their most recent quarters, ELAN generated a gross margin of 50.1%. Zoetis’s U.S. segment posted Q4 gross margins of 78.9% and its International segment posted gross margins of 67.2%.

Zoetis’s pole position when it comes to relationships with farmers and vets makes it easier to launch new products. This factors into its moat. Its large cash flows also allow it to maintain a marketing budget larger than its peers. Once again, this is an example of ZTS’s size/scale creating barriers to entry that are tough for startup competition to clear.

Looking at recent trends, I believe that ZTS is clearly the best-in-breed (pun intended) play in the animal health space. And, as the company continues to pivot its focus away from livestock and towards the companion animal market (taking advantage of the societal trends which have led to the “humanization of pets” thesis), I think there is plenty of growth ahead.

Morningstar estimates that by 2027, roughly 70% of Zoetis’ revenues will come from their compassion animal products.

I should also note that this focus on companion animals is likely to lead to higher rates of growth moving forward because it’s essentially a play on the rise of the middle class from emerging markets.

ZTS markets products in nearly 50 countries. But, the U.S. made up roughly 53% of its sales in 2023.

The CFRA note estimates that pet ownership in emerging markets is roughly 80% below the pet/household rate that we see in the U.S. Yet, as discretionary income rises in those countries (especially China and India, with massive populations) that represents a major TAM expansion opportunity for a company like ZTS.

Zoetis shares are not cheap. But, I don’t think they should be.

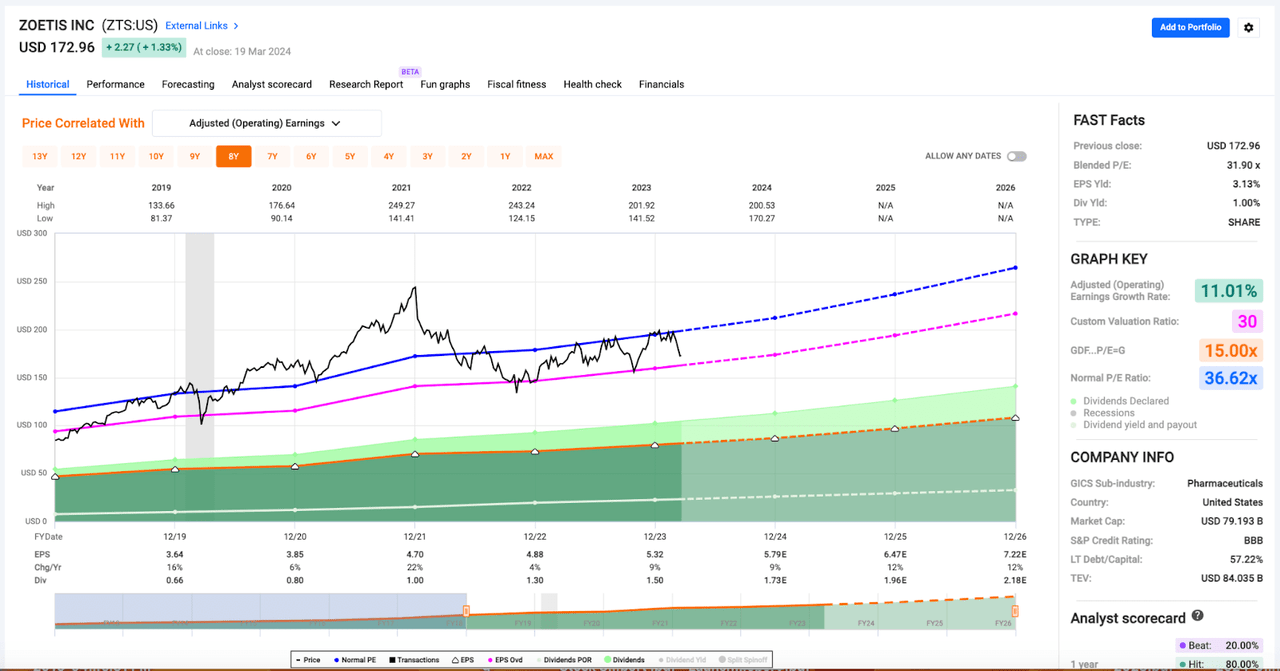

ZTS stock has fallen by roughly 14% on a year-to-date basis and currently trades with a blended P/E ratio of approximately 31.5x.

That’s still well below most bio-pharma stocks (outside of the GLP-1 names like LLY and NVO); however, I think the discussion above, regarding the lack of regulation and competition, shows why ZTS warrants a premium valuation.

Because the consensus analyst estimate for ZTS’s EPS growth in 2024 is currently 9%, shares are a bit cheaper on a forward basis.

ZTS’s forward P/E ratio is roughly 29.3x.

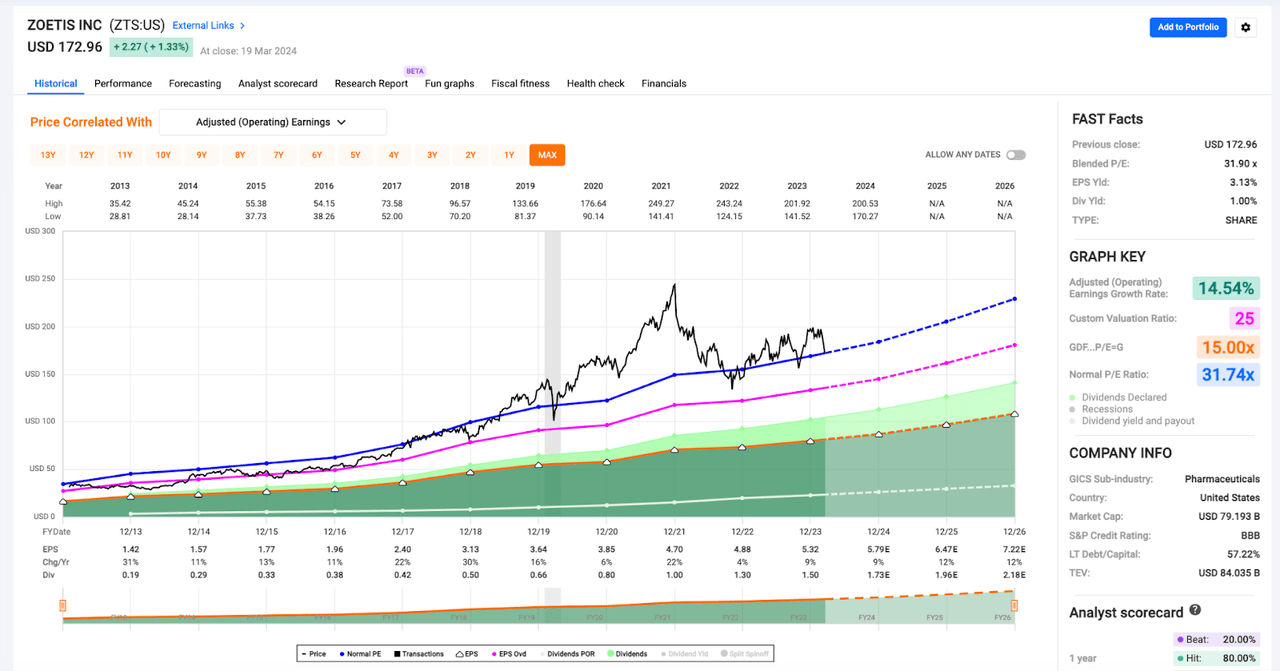

FAST Graphs

That’s well below the stock’s 3, 5, and 10-year average P/E ratios of 39.7x, 36.6x, and 31.7x, respectively.

On the chart above, you’ll notice the pink line, representing the 25x earnings threshold. That is the level where ZTS sat for a few years after its spin-off; however, it launched higher during early 2017 and hasn’t traded for 25x earnings since.

Obviously, I’d love to buy ZTS with that sort of multiple attached, but it seems unlikely. And I don’t want to wait around on the sidelines forever as the fundamentals here continue to compound, driving my fair value estimate higher and higher over time.

I don’t believe that the margin of safety here in the $170 area is very wide. But, I don’t need to see a wide margin of safety to buy a blue chip compounder. Buying at fair value is a great way to build wealth with companies like this since their fundamentals and dividends consistently rise over time.

My current fair value estimate for ZTS is $174 (basically 30x forward).

29x forward is $168.00.

28x forward is $162.00.

These are all levels that I have in mind when it comes to building out my ZTS position.

And looking at the graphic below, you’ll see that shares have only been this cheap a couple of times during the past 5 years, meaning that this is a relatively rare opportunity to buy ZTS at ~30x level.

FAST Graphs

The high cash flow multiple that ZTS trades with has resulted in a relatively low dividend yield.

Today, shares yield roughly 1.00%.

That might seem extraordinarily low to some people; however, this one is about the compounding potential, not the yield in the present.

As I already said, ZTS has been compounding its dividend at a ~25% CAGR since inception.

Someone who bought ZTS when it began trading in 2013 would be sitting on a yield on cost north of 5%.

Now, I don’t expect to see the dividend grow at that pace moving forward, but I still think a 10%+ CAGR is possible here over the next 5-10 years.

With that in mind, this 1% could quadruple over the next 15 years or so.

ZTS’s forward EPS payout ratio is 29.8%.

This means that Zoetis shares offer a safe, reliably growing dividend that pares really nicely with the expected share price appreciation that its fundamental growth should support.

I use the growing dividend here as a mental anchor which allows me to hold shares throughout volatility.

Buying and holding blue chips like this is the best way that I know of to generate significant wealth.

Well, ZTS’s reliably growing dividend is what allows me to own shares, through thick and thin, in a relatively stress free way.

I believe this pullback has pushed shares back down to fair value and therefore, has provided investors with an intriguing opportunity to buy a wonderful company at a fair valuation.

That’s been Buffett’s mantra for success for years now and it has served me well in the past as well.

Yes, there are risks here. To me, the biggest risk with ZTS is likely multiple compression. If this stock gets re-rated down to the 15-17x range where many of the human-centric bio-pharma stocks trade, then we’d be looking at significant downside here.

I don’t think the fundamentals justify such a move though…and relative to the best human bio-pharma names, ZTS trades at a massive discount (for instance, LLY shares sport a forward P/E ratio of approximately 62x right now).

There’s also some ESG risk at play here, especially in the livestock area, with health food concerns about drugs/antibiotics in animals entering into the human food chain.

Lastly, it's important to note that changing protein consumption trends (less animal protein and more plant-based protein) could negatively impact the demand for ZTS’s livestock-related portfolio.

But, as I’ve already said, it looks like ZTS is pivoting its focus towards the companion animal space and that helps to reduce these concerns.

Overall, I believe that ZTS offers a safe and reliably growing dividend and therefore, as this sell-off persists, this company continues to rise up my personal watch list.

As new cash becomes available to invest, Zoetis Inc. stock will be a top target of mine moving forward. And, at the very least, I plan to add to my position in early April when I selectively invest my March dividends.