LeoPatrizi

LeoPatrizi

Welcome to another installment of our CEF Market Weekly Review, where we discuss closed-end fund ("CEF") market activity from both the bottom-up - highlighting individual fund news and events - as well as the top-down - providing an overview of the broader market. We also try to provide some historical context as well as the relevant themes that look to be driving markets or that investors ought to be mindful of.

This update covers the period through the third week of March. Be sure to check out our other weekly updates covering the business development company ("BDC") as well as the preferreds/baby bond markets for perspectives across the broader income space.

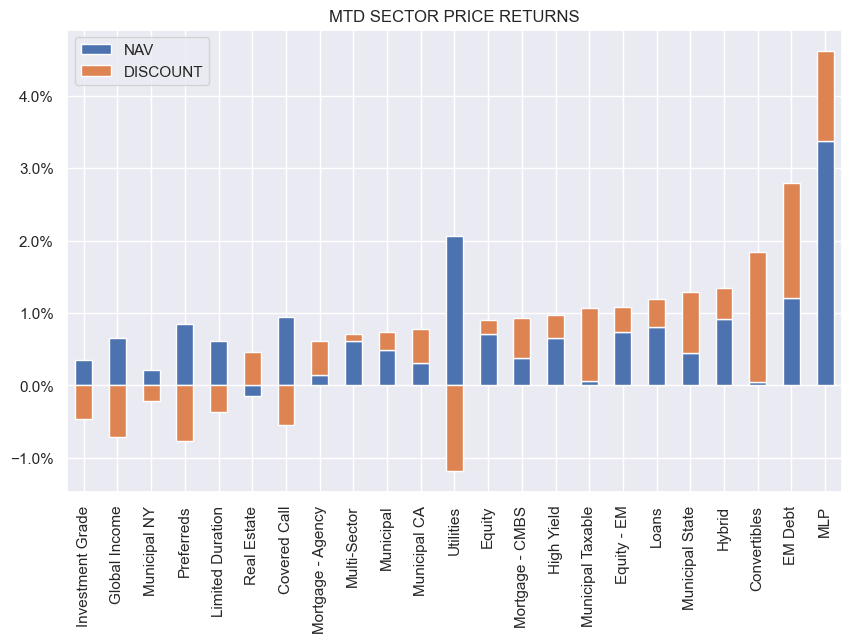

Nearly all CEF sectors saw lower NAVs over the week due to the drop in stocks and Treasuries. MLP and loan CEFs eked out gains, however. Despite this weakness, discounts managed to tighten across all but 3 sectors. Month-to-date, most sectors remain in the green.

Systematic Income

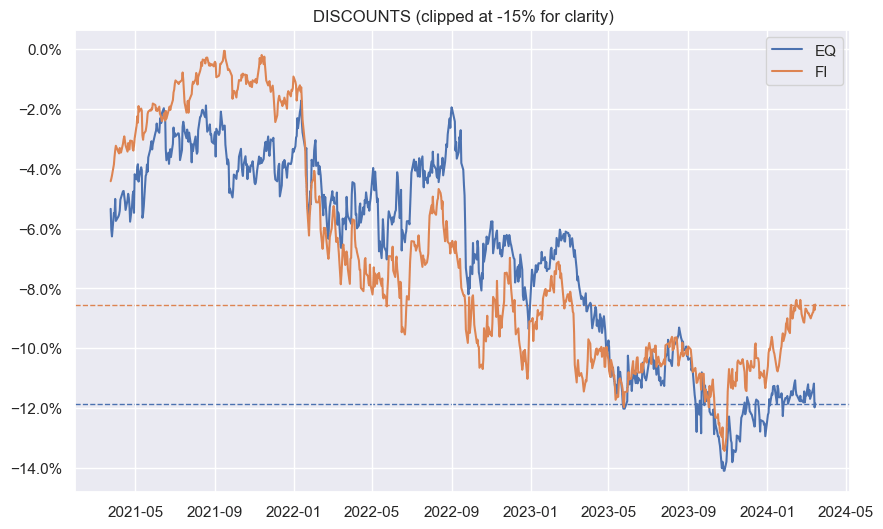

The divergence between fixed-income and equity CEF sectors remains a theme of the CEF market. While equity CEF sector discounts have remained flat this year, fixed-income CEF sector discounts have tightened considerably, to an extent that they are fairly-valued on a longer-term basis.

Systematic Income

Saba is getting into a fight with the ASA Gold & Precious Metals CEF (ASA). It owns 16.9% of the fund’s shares and is presumably looking to do what it does best which is to control the board of the fund and, potentially, terminate it to close the discount and push the price higher. In order to prevent Saba from getting more shares, ASA has adopted a rights-offering plan which will trigger if any entity with a 15% or more ownership (i.e. Saba) buys 0.25% more shares in the fund.

In a rights offering a fund issues rights that allow existing shareholders to buy more shares at a certain subscription price. Typically, the subscription price is below the NAV which leads to NAV dilution (i.e. a drop in the NAV). The way to mitigate this is to either sell the rights (at the right price) or to exercise the rights and acquire new shares.

Shareholders who are granted rights but do not use them simply lose money because they experience NAV dilution without monetizing the rights. Because of the way the rights offering is structured, Saba would lose a ton of money because they would be prevented from exercising rights (which involves acquiring more shares which ASA has forbidden for someone like Saba) and would lose a ton of money - a kind of poison pill.

Recall that Nuveen lost an appeal of a previous lawsuit brought and won by Saba in 2021 referencing 5 Nuveen CEFs (JFR, JRO, JSD, JGH, NSL). Nuveen earlier adopted an amendment to its bylaws which restricted shareholders in these funds from voting shares above a certain level of ownership. The Court ruled that Nuveen violated the Investment Company Act of 1940 (key legislation that regulates investment funds) by, in effect, stripping certain shareholders (i.e. those like Saba with a holding above a fixed level) of voting rights.

Overall, it seems more likely than not that ASA will lose the lawsuit. On the face of it, what ASA has done is allow some shareholders of the fund to have superior rights to others specifically, when it comes to exercising the rights under the offering. This seems unlikely to succeed but we should know more at a later stage. It’s possible ASA knows full well they could lose in court but are just hoping Saba will deem it too expensive to litigate it, causing it to move on to another target.

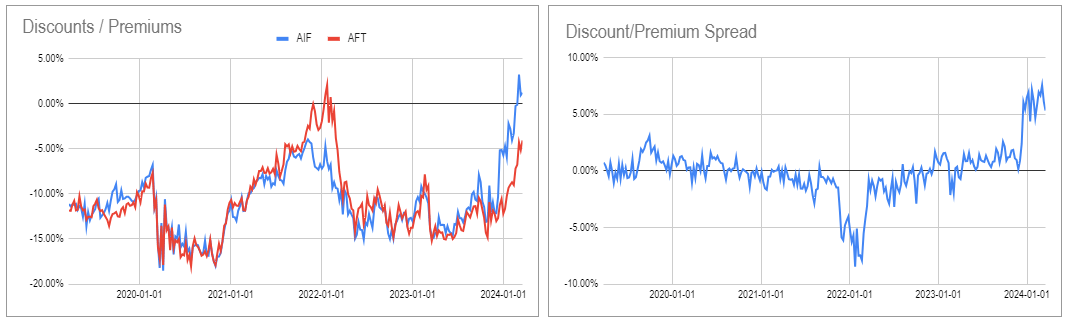

Apollo credit CEF Tactical Income Fund (AIF) hiked the distribution by around 4%. Interestingly, its sister fund Senior Floating Rate Fund (AFT) which has a larger floating-rate profile did not. The funds are the strongest performers in the loan CEF sector this year with an average total price return of around 10% - well above the median 6.3%. AFT is in our High Income Portfolio after a rotation from AIF.

AIF is very expensive, trading at a small premium while AFT is a tad rich as well. Its 5-year discount percentile is 91%, meaning the discount has been tighter only 9% of the time in the last 5 years. Its DSSP or discount spread percentile is 85%, meaning the discount differential to the sector average has been tighter only 15% in the last 5 years.

Systematic Income CEF Tool

The CEF Virtus Total Return Fund (ZTR) is holding a tender offer at the start of April (expiring on 1-May) for up to 10% of shares at 98% of NAV. It's generally a good idea to participate in these as the sale price is typically well above where the fund is trading otherwise. Investors who want to maintain the same number of shares can just turn around and buy back the shares that were accepted into the tender offer which should trade at lower than the buyback price.

The price of the fund jumped 3% on the news however it has come off since then. Typically, it’s unusual for the discount to tighten a whole lot into the tender offer given the relatively small percentage of the buyback so it should remain north of 10%. ZTR has two other tender offers planned, conditional on the discount remaining wider than 10%. That’s a very shareholder friendly feature - more funds should have this in place.