Is Zosano Pharma (NASDAQ:ZSAN) Using Debt In A Risky Way?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Zosano Pharma Corporation (NASDAQ:ZSAN) does carry debt. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Zosano Pharma

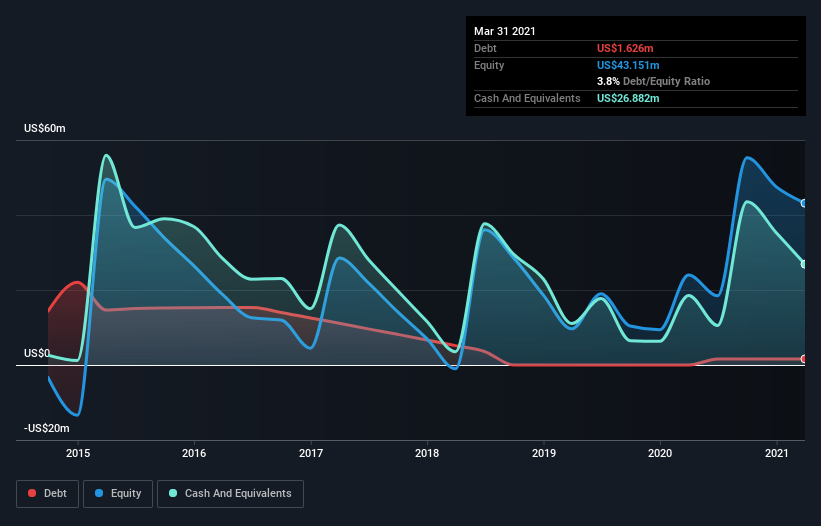

What Is Zosano Pharma's Debt?

You can click the graphic below for the historical numbers, but it shows that as of March 2021 Zosano Pharma had US$1.63m of debt, an increase on none, over one year. However, it does have US$26.9m in cash offsetting this, leading to net cash of US$25.3m.

How Strong Is Zosano Pharma's Balance Sheet?

We can see from the most recent balance sheet that Zosano Pharma had liabilities of US$14.4m falling due within a year, and liabilities of US$8.15m due beyond that. On the other hand, it had cash of US$26.9m and US$243.0k worth of receivables due within a year. So it can boast US$4.57m more liquid assets than total liabilities.

This surplus suggests that Zosano Pharma has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Simply put, the fact that Zosano Pharma has more cash than debt is arguably a good indication that it can manage its debt safely. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Zosano Pharma's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Since Zosano Pharma doesn't have significant operating revenue, shareholders must hope it'll ramp sales of its new medical tech as soon as possible.