VioletaStoimenova/E+ via Getty Images

VioletaStoimenova/E+ via Getty Images

My recommendation for Zeta Global Holdings (NYSE:ZETA) is a buy rating. ZETA has shown very strong momentum in expanding its customer base, especially in the super-scaled customer cohort, and also in its ARPU. I am expecting this momentum to continue as ZETA rolls out more products that it can sell to its existing clients, which should drive up ARPU and NRR. The good progress made with its agency partners and system integrators will also bode well for stronger logos in the future as ZETA increases its distribution capacity.

You can think of ZETA as a platform that digests large amounts of customer-related data via multiple channels, analyses them, and generates a "report" to its clients (corporates that are selling something to consumers). ZETA's clients benefit from this offering because they are able to better refine their strategies to target the right set of consumers. This is done through various AI and ML solutions, and the "report" is basically a single view of a consumer profile (buying intent, purchasing behaviors, etc.). While ZETA operates globally, 96% of its revenue still originates from the US.

ZETA

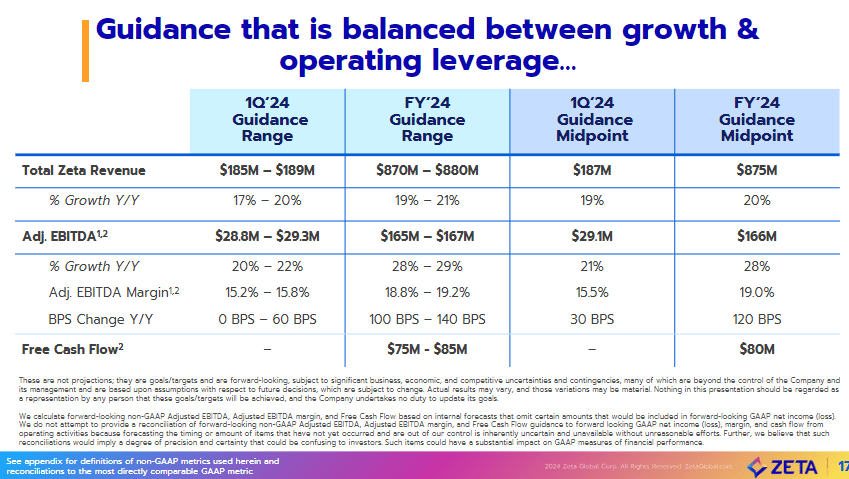

ZETA reported strong revenue growth of ~20% in 4Q23 to $210.3 million, ending FY23 with $728.7 million in revenue. The strong growth was driven by strong sales productivity, which led to healthy new customer adoption and ARPU expansion. While a gross margin of 60% came in below the 4Q22 level by 360 bps, mainly due to a mix shift away from direct platform revenue, adj. EBITDA margins actually improved by 280 bps from 18.5% to 21.3%. The better EBITDA performance was driven by strong revenue growth, which suggests ZETA is enjoying healthy operating leverage. On a GAAP basis, EPS came in at -$0.22, an improvement vs. 4Q22 of -$0.36. Although GAAP earnings were negative, ZETA still continued to generate positive FCF. 4Q23 saw ~$21 million in FCF generated, vs. $18.4 million in 4Q22. ZETA ended the year with a healthy balance sheet and net debt of ~$50 million.

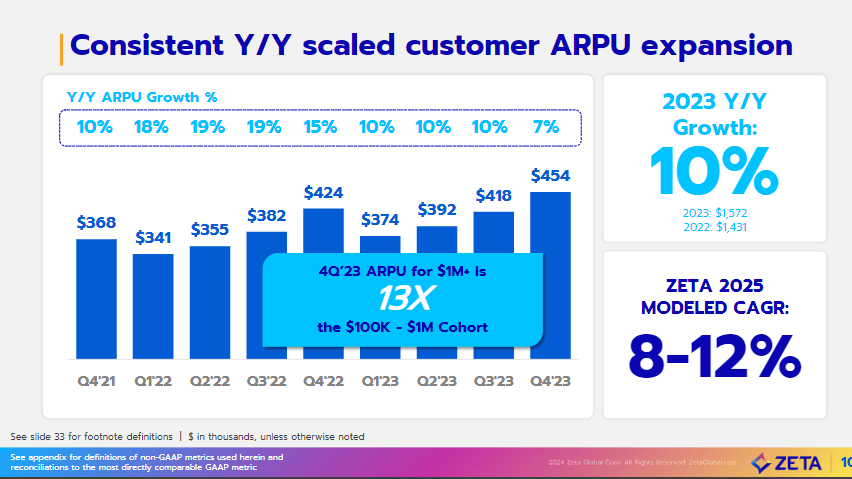

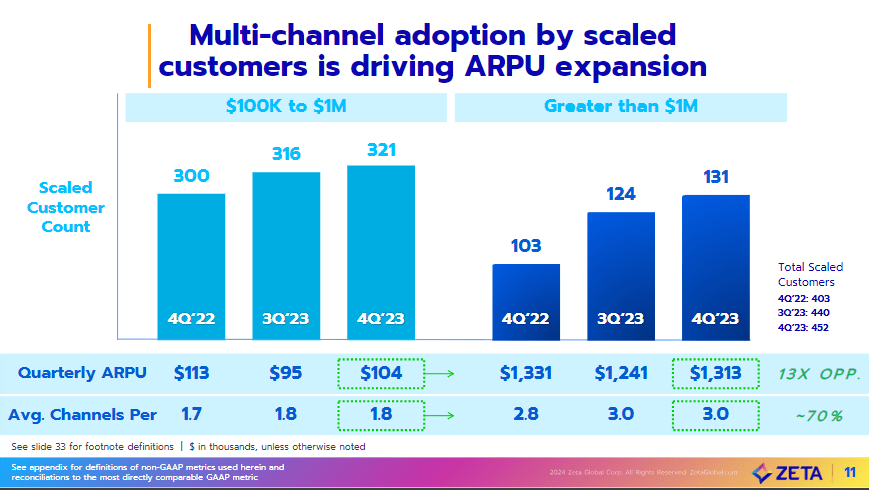

In 4Q23, ZETA added 12 new scaled customers, bringing the total to 452. This growth was driven by strong new logo growth. This set of performances is a lot better considering the underlying mix of customers that were added. When breaking down yearly growth in total customers, ZETA was most successful in the revenue range of over $1 million, where it added 7 customers sequentially and ended the quarter with 131. Zeta also added five new scaled $100k-$1 million revenue customers, ending 4Q23 with 321 scaled customers. This significantly pushes up the overall ARPU profile of ZETA's underlying customer base and also indicates that ZETA has a strategy for penetrating the upmarket. For reference, ZETA saw scaled customer ARPU improve 9% sequentially from $418k in 3Q23 to $454k in 4Q24, which is a 7.1% annual increase.

ZETA

I expect ZETA to continue this ARPU expansion momentum as it is increasingly being driven by channel additions, as channel growth was faster in >$1 million revenue customers, up ~7% Y/Y to 3 channels, whereas the scaled customers were up ~6% Y/Y to 1.8 channels. One thing to highlight regarding ARPU is that the headwinds from the auto and insurance verticals continued to pressure the super-scaled ARPU (fell by 1.4% to $1.313 million), which resulted in net revenue retention [NRR] declining by 100 basis points to 111% vs. FY22. While I do acknowledge this, we should not discount all the other parts of ZETA that are doing very well. Adjusting for these 2 weak verticals, which I believe are going to show strength as we move through FY24 given that management has been seeing positive traction since late 4Q23, NRR would have come in at 118% in FY23, as 6 of Zeta's 10 largest verticals grew by more than 25%.

On the first question around the two challenged verticals, the automotive vertical and the insurance vertical, the short answer is very good visibility into the sales pipeline. Much of that, frankly, already starting late 4Q, so it will already start to feather in beginning in the first quarter. So feeling really good about the return of those industries back to growth in 2024, probably even starting to see some in the latter part of the first half of this year. 4FQ23 earnings

ZETA

I am also looking forward to more product releases (or monetization of products) that should drive ARPU and NRR upwards. In particular, I think AI could be a game-changer. For instance, ZETA Intelligent Agent Composer enhances customer efficiency and effectiveness through the creation of AI agents that offer a wide range of intelligent and automated tools. The new product and extra GenAI features will be monetized in various ways, according to management. As per management in the FY23 earnings call, one of these ways is by developing new billable modules, which will lead to increased consumption and less demand on marketing resources in businesses. Additionally, management recognizes a chance to integrate the ZMP with all subsystems through a conversational interface on mobile devices, which would allow for the consolidation of point solutions into a comprehensive platform. Management believes this could be the next $100 million business, and mobile accounts for less than 2% of revenue, so the revenue growth opportunity is huge (source: FY23 earnings call). Suppose this scales up to $100 million over 3 years; that easily translates to a mid-single-digit growth tailwind. And if we include the upside from the AI products, we could easily see an acceleration in growth back to mid- or high-20 percentage rates.

As I mentioned above, channels are likely going to lead ARPU expansion ahead, and hence, I was pleased to hear that management sees agency partnerships as a way to increase penetration, especially because they can serve multiple brands efficiently through one relationship. I think this is an excellent strategy because establishing a master relationship with an agency will allow ZETA to reach out to other potential clients much more rapidly than approaching each of them directly (it takes a lot more manhours to do this). On penetrating the upmarket, we could see an acceleration in gains as well (likely in 2025 and beyond given the multi-year roll-out process), as ZETA is in advanced discussions with system integrators, which can further adoption by large enterprises.

Our unique position in the market and continued investment in AI-powered marketing technology is also creating interest across the ecosystem as we expand our relationships with Systems Integrators. But to have gone from talking about this too we're knee-deep in two integrations with them now, which will launch two separate systems integrators with two separate enterprises. We're very excited about those prospects. 4FQ23 earnings

Redfox Capital Ideas

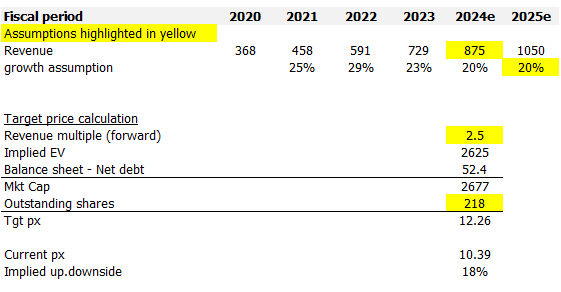

I believe ZETA is worth $12.26, which is an 18% upside vs. the current share price of $10.39. My growth assumptions are based on management FY24 guidance and my belief that growth can continue at the 20% rate through FY25, which implies ZETA generating $1.05 billion in revenue in FY25. However, I must note that my estimates are conservative, as there is potential for growth acceleration if:

Both of these catalysts are hard to underwrite today with confidence, given the lack of information. I would continue to monitor management's comments during each earnings call to see if there is any meaningful progress on these fronts.

Relative to its own trading history, ZETA is now trading slightly below its average of 2.85x, and I think it is fair that it trades at a discount given the slowing growth rates reported (from high 20s to just 20% in FY24e). That said, ZETA has also turned more profitable (adj. EBITDA basis), so that should net off any major discounts. I would expect ZETA to continue trading somewhere at this level until it shows that growth can accelerate (likely from the catalyst I noted above), at which point that market should revalue the stock to at least its historical average of 2.85x.

ZETA

ZETA's ability to grow is directly impacted by the marketing budget of its underlying clients, which is heavily exposed to macrocycles. In good years, companies flush their marketing departments with a lot of budget as consumer demand is high. However, in bad times, like what we saw last year, marketing budgets get cut easily (typically because these are variable costs anyway), and we have seen how this has impacted ZETA (revenue growth went from 29% in FY22 to 23 in FY23). If the macroeconomic situation continues to get worse, it might be hard for ZETA to accelerate growth.

My view for ZETA is a buy rating. ZETA has shown strong momentum in customer acquisition, particularly among high-value super-scaled clients, and is successfully expanding its ARPU. I believe this trend is likely to continue as ZETA rolls out new products and strengthens its distribution channels through agency partnerships and system integrators. ZETA's improving profitability and the potential for growth acceleration through its AI and mobile initiatives are also catalysts that could drive valuation upwards.