Art Wager

Art Wager

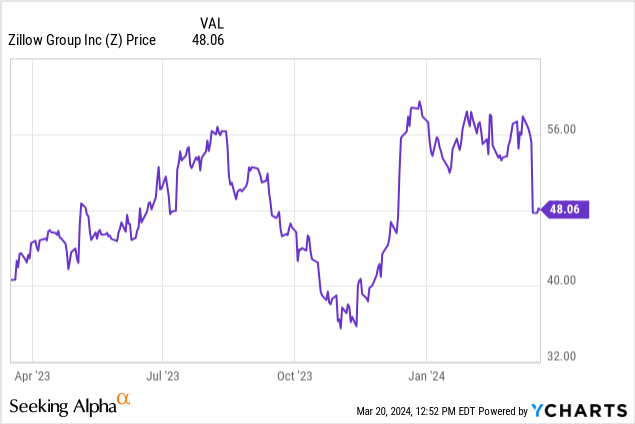

The news is out now: after months in litigation, the NAR (National Association of Realtors) agreed in mid-March to pay a $418 million settlement in response to accusations of the powerful trade group colluding to inflate brokerage commissions. Real estate stocks, which had been on an upward trajectory this year as investors looked forward to interest rate cuts and an increase in housing supply, got battered on the news.

But amid pessimism and uncertainty surrounding the new ruling, I think there's one amazing buying opportunity to be had, and that's Zillow (NASDAQ:Z), the popular home search platform. Shares of Zillow have shed more than 15% year to date after the impacts of the NAR decision, but I think there's plenty of room to rebound ahead as the company reports better results.

I last wrote a bullish note on Zillow in November, when the stock was trading closer to the mid/high-$30s. Since then, Zillow has rebounded alongside the rest of the market, and I believe there's further upside ahead as I think Zillow can recoup some of the NAR-related losses.

Let's be abundantly clear here: the impacts of the ruling, which at face value only removes the commission-split arrangement between buyers' and sellers' agents, will take time to play out. But what most industry prognosticators are predicting is that A) real estate commissions will come down over time, and B) if forced to pay for their own buyers' agent, many more home shoppers will turn to a DIY approach. Why, after all, would a buyer pay a commission to an agent to help them search for homes when looking online (as well as touring online!) via Zillow is now easier than ever?

It's the latter element here that I think will actually be a tailwind for Zillow. The company can benefit from more consistent traffic as more people forego their agents and find homes online themselves. The buy-side agency will likely shift to focusing on paperwork and closing, which buyers may not have the expertise to do on their own.

Of course, the sea change in the real estate industry is not without its risks for Zillow. Zillow, after all, relies on advertising dollars from real estate agents for the vast majority of its revenue, and if fees are coming down overall, agents will have less gunpowder to spend on Zillow. Still, I think the prospect of higher traffic from DIY buyers helps to offset this risk.

Here is a refresher on what I believe to be the other elements of the long-term bull case for Zillow:

Stay long here: especially with strong results exiting Q4, Zillow is poised for a recovery.

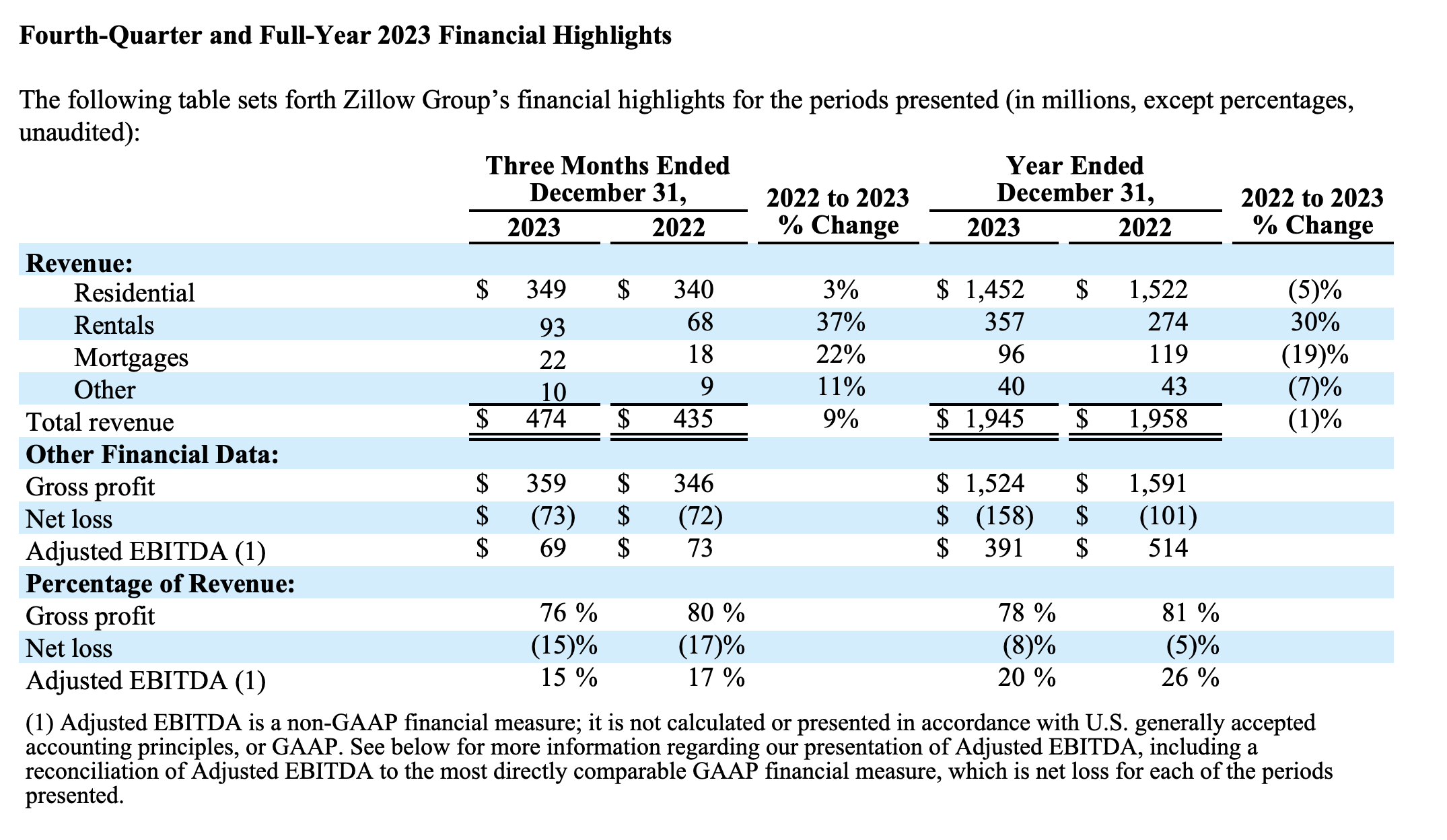

Let's now go through Zillow's most recent quarterly results in greater detail. The Q4 earnings summary is shown below:

Zillow Q4 highlights (Zillow Q4 shareholder letter)

Zillow's total revenue grew 9% y/y to $474 million, well ahead of Wall Street's expectations of $451 million (+4% y/y) and the company's own internal guidance range of $430-$455 million -1% y/y to +5% y/y. Growth also accelerated sharply versus 3% y/y in Q3.

The big driver here was a resurgence in residential revenue (the vast majority of which is the Premier Agent business), which returned to 3% y/y growth after declining 3% y/y in Q3. Zillow notes as well that during the same quarter, the overall real estate industry declined -4% y/y in total transaction value, meaning that Zillow outperformed the industry by 7 points. In 2023 as a whole, the company's -5% decline in residential revenue actually outpaced the broader industry's -17% decline by 12 points.

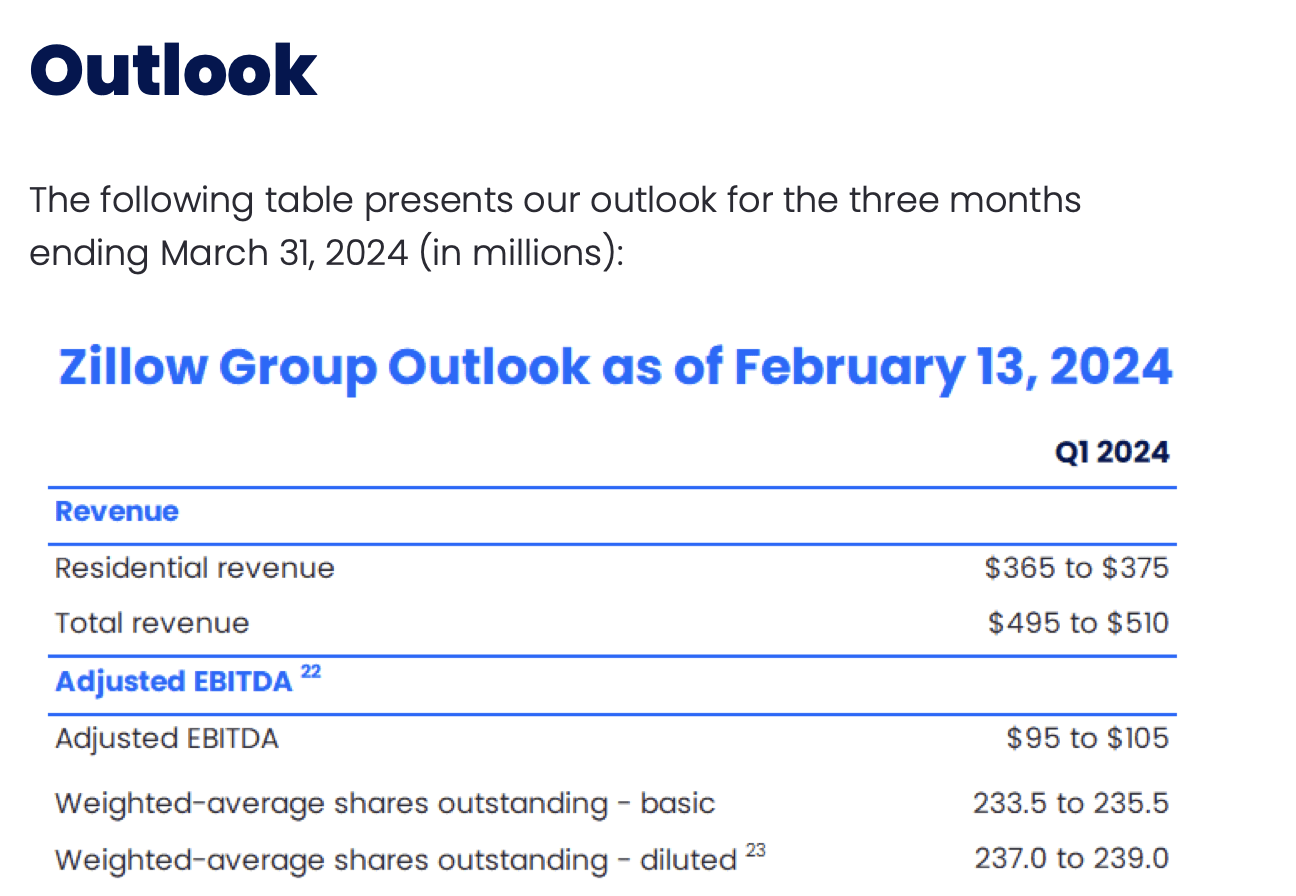

The company believes its outperformance will continue into the first quarter of 2024, where it's expecting residential revenue of $365-$375 million, representing 1-4% y/y growth.

Zillow outlook (Zillow Q4 shareholder letter)

Speaking to the outlook on the Q4 earnings call, Zillow CFO Jeremy Hofmann noted as follows:

Despite the tough macro existing home sales environment, we expect our residential revenue to outperform the industry in Q1 as our growth pillars begin to contribute to revenue and the investments we have made in our overall funnel continue to deliver benefits. We expect rentals revenue to continue to grow more than 30% year-over-year in Q1 as we benefit from the strength of our execution and favorable industry backdrop, driving landlord demand for advertisers.

We expect positive growth in mortgages revenue year-over-year in Q1. We plan to expand integration with our premier agent partners in enhanced markets, send more of our mortgage leads to ZHL directly and drive engagement with more consumers on our apps and sites to grow our origination volumes."

Also of note: Zillow's results in the rentals segment have also skyrocketed. Growth of 37% y/y accelerated versus a 34% y/y pace in Q3, which the company noted is due to incredible strength in the multifamily apartment space.

The company also expects adjusted EBITDA to return to ~flat y/y in Q1, similar to results in Q4.

In my view, Zillow will adapt well to the post-NAR real estate world. In the meantime, the company is posting solid results that show both a return to growth and a vast outperformance versus the broader real estate industry. Use this dip as an opportunity to add more.