MicroStockHub

MicroStockHub

A year ago, I wrote a review of the Amplify High Income ETF (NYSEARCA:YYY). Although I liked the YYY ETF's attractive 11% forward distribution yield, I urged caution, as the fund had not historically 'earned' its distribution.

With a year gone by, I wanted to revisit my thesis on the YYY ETF to see if my initial conclusion was correct.

The Amplify High Income ETF aims to pay high current income through a passive portfolio of closed-end fund ("CEF") investments. YYY's portfolio contains 45 CEFs that are selected based on their distribution yields, discount to net asset value ("NAV"), and liquidity.

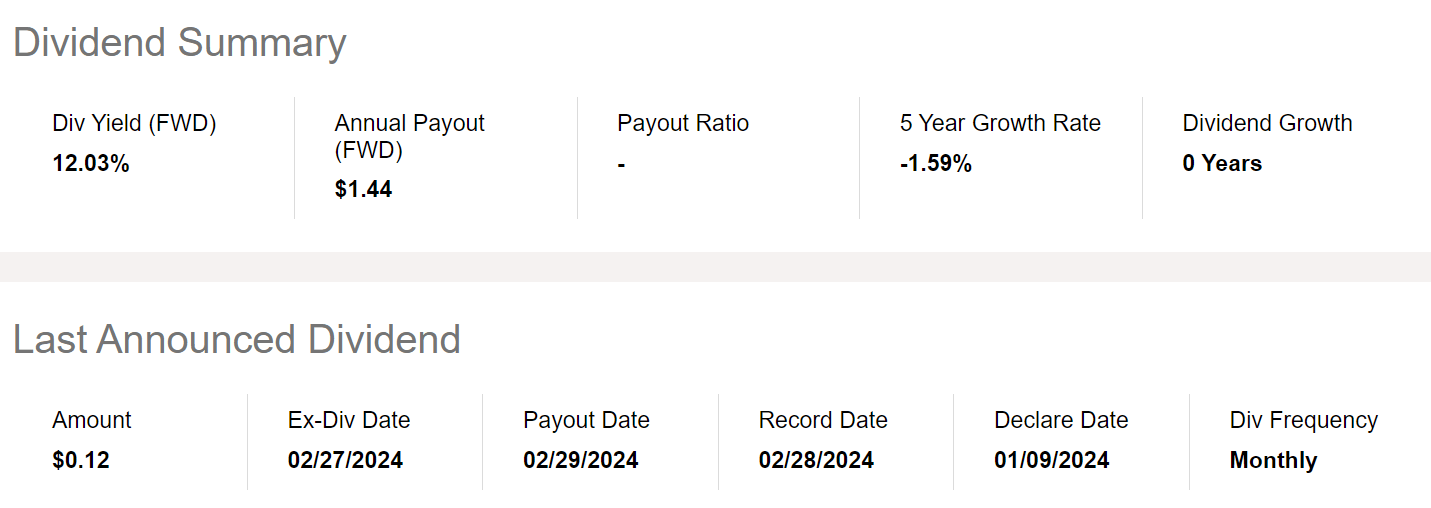

Based on its portfolio of high yielding CEFs, the YYY ETF itself pays an attractive distribution yield, currently set at $0.12 / month or a forward yield of 12% (Figure 1).

Figure 1 - YYY distribution yield (Seeking Alpha)

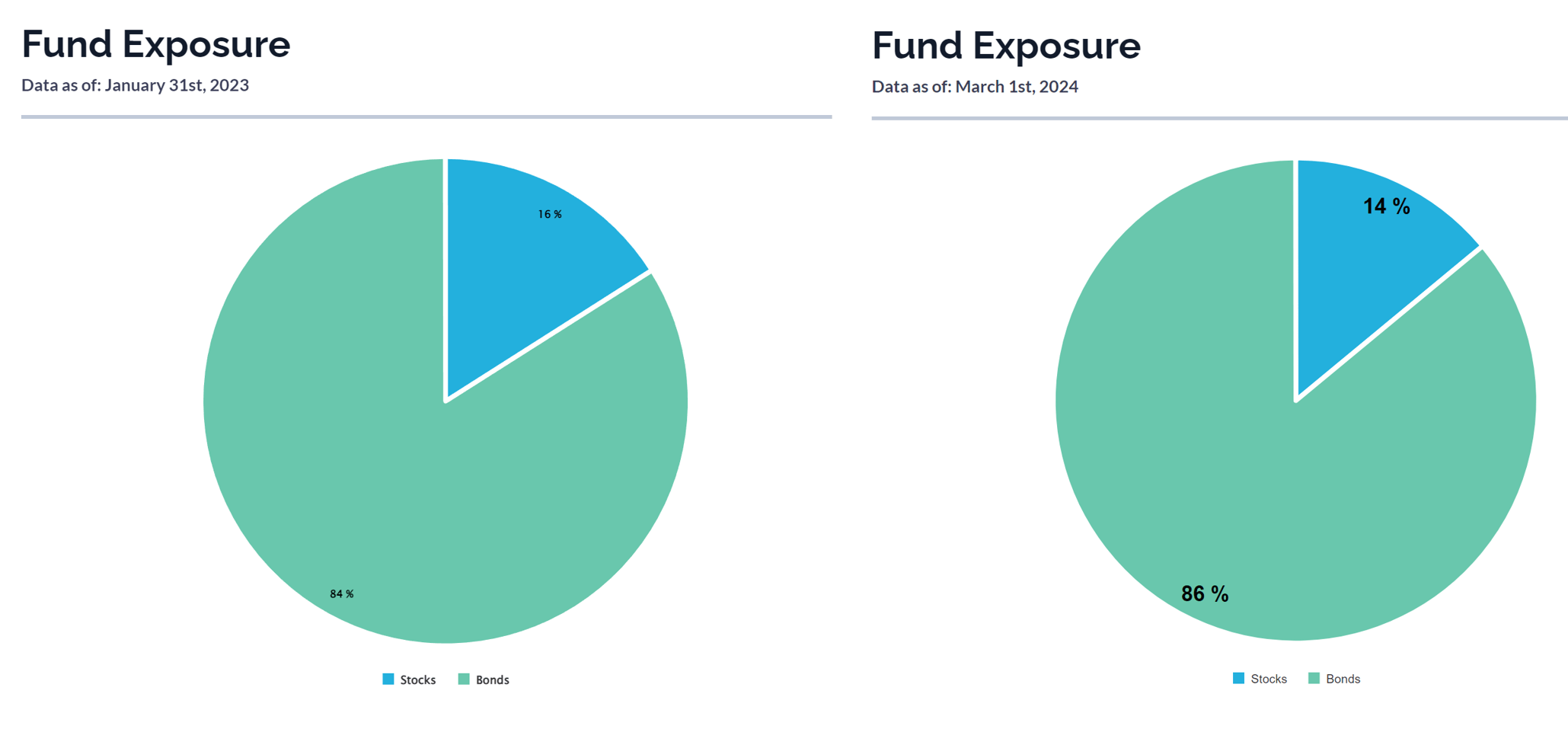

Compared to a year ago, YYY's overall portfolio allocation has been fairly constant, with 86% of the portfolio invested in Bond funds as of March 1, 2024, compared to 84% in January 31, 2023 (Figure 2).

Figure 2 - Fund exposure, March 1st 2024 vs. January 31st 2023 (amplifyetfs.com)

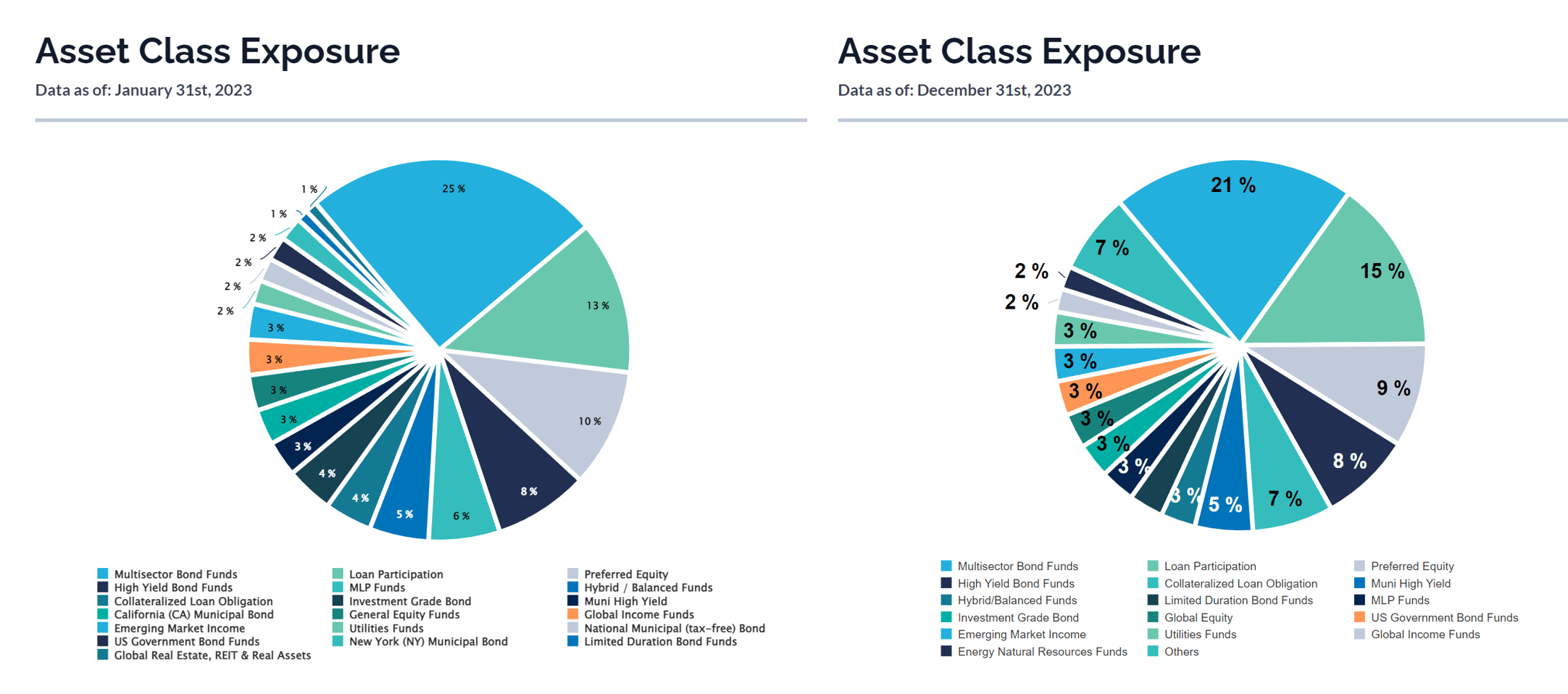

Asset class allocations have also been fairly consistent, with only small changes in individual asset class weights such as a decrease in Multi-sector Bond funds from 25% to 21% and an increase in CLO funds from 4% to 7% (Figure 3).

Figure 3 - Fund asset class weights, December 31st, 2023 vs. January 31st, 2023 (amplifyetfs.com)

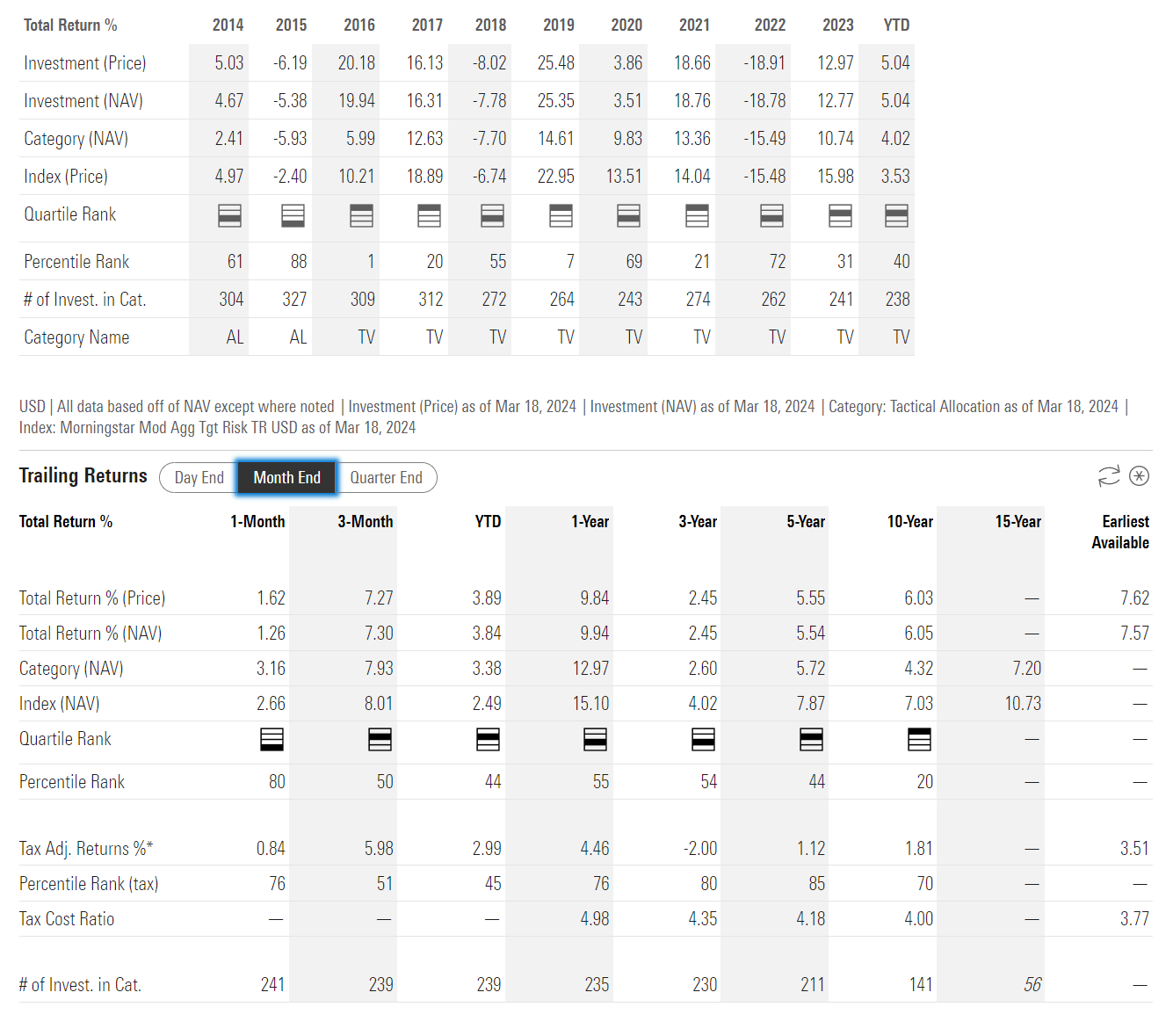

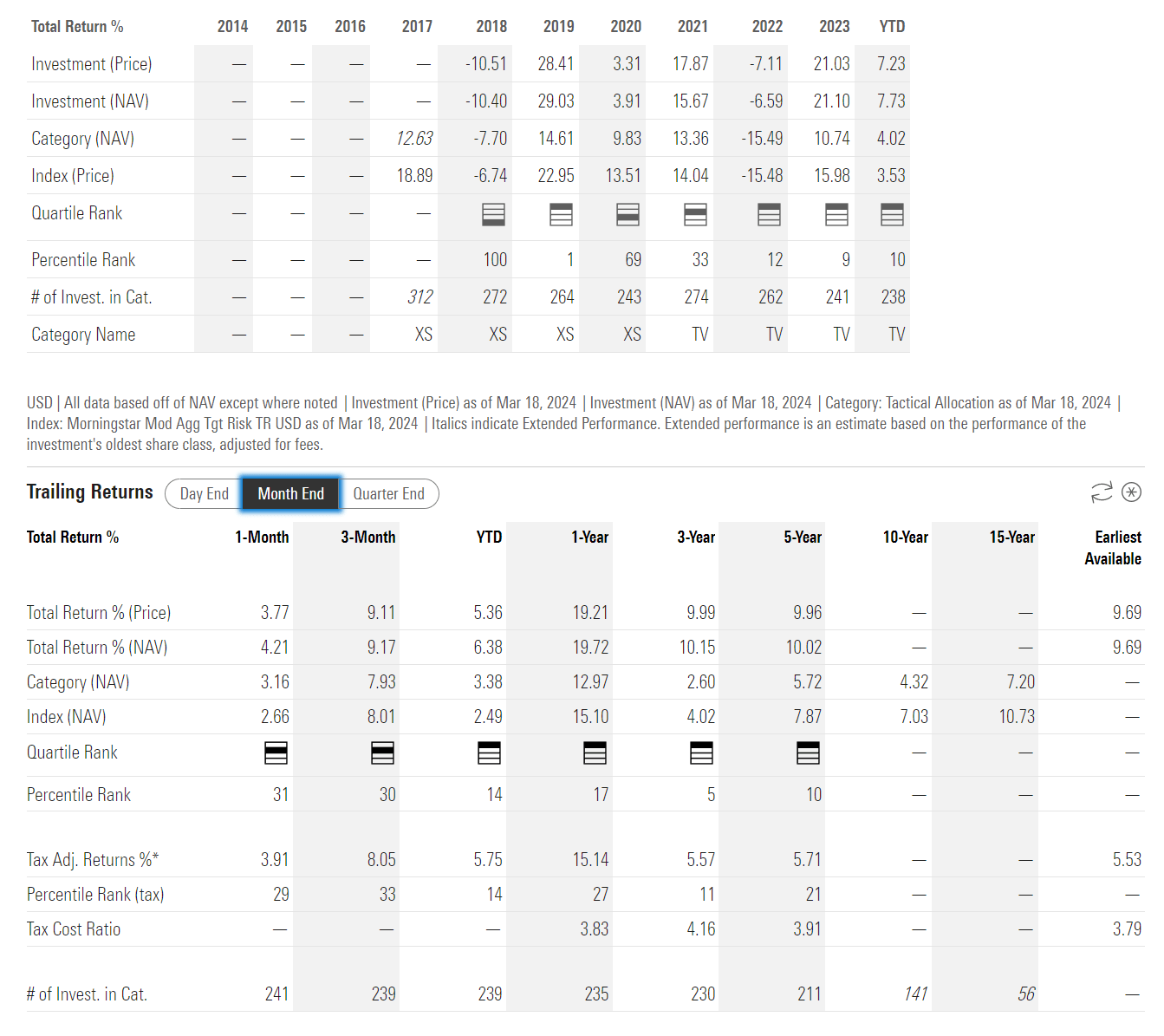

With buoyant equity markets and tightening credit spreads, it is no surprise that the YYY ETF delivered a solid performance in the past year, returning 12.8% in 2023 and 5.0% YTD 2024 (Figure 4).

Figure 4 - YYY historical returns (morningstar.com)

However, even after a decent 2023 performance, the YYY ETF still under-earns its distribution yield, with 3/5/10-year average annual returns of only 2.5%/5.5%/6.1%, respectively, to February 29, 2024.

I believe my main concern with the YYY ETF remains valid, as it continues to pay a distribution yield that is far in excess of its long-term average returns. As I wrote in my prior article, funds that do not earn their distribution yields are called 'return of principal' funds and are characterized by NAV being liquidated to fund its distribution.

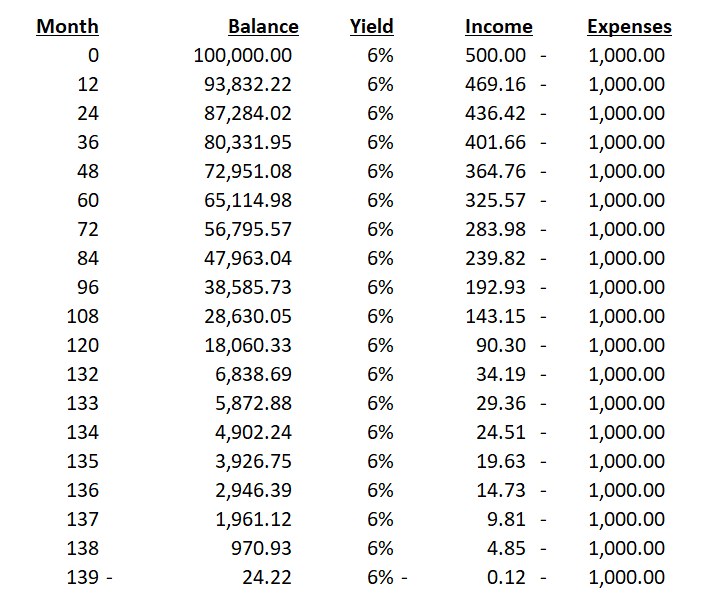

To see how this could be problematic, consider a real-life example. Assume John Doe has a retirement portfolio of $100,000 that is invested in securities earning 6% p.a (similar to what YYY has earned over 10 years). However, John has fixed monthly expenses of $1,000 (or 12% p.a. at inception, similar to YYY's fixed $0.12 / month distribution).

While John has ample retirement savings to cover the overspending in any given month, if John does not increase his returns or cut his spending, then over time, his capital will be depleted at an increasing rate. In this simple example, John's savings will be depleted in ~11.5 years (Figure 5).

Figure 5 - Hypothetical example (Author created)

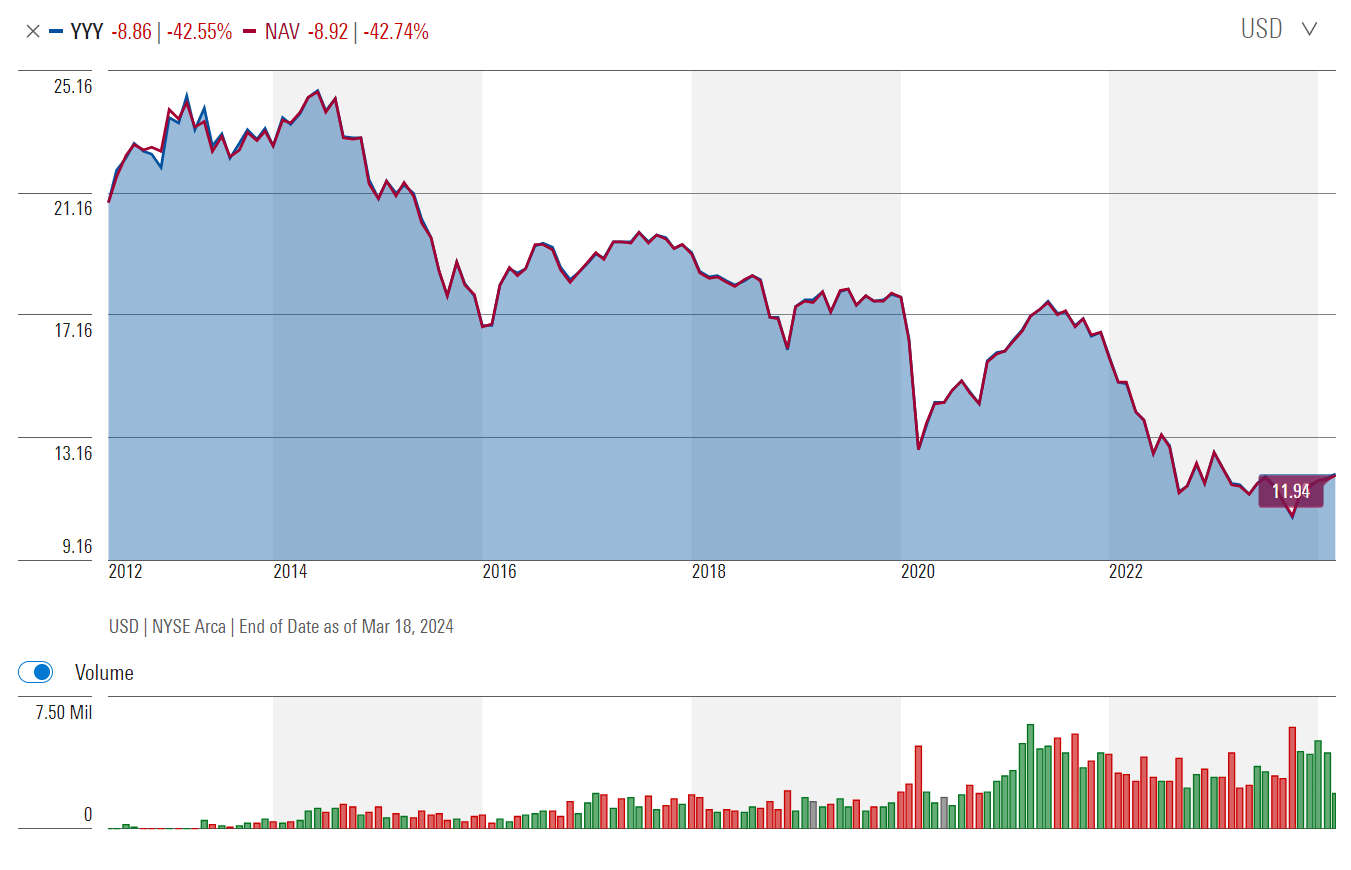

In reality, we can see that YYY's NAV has been cut by 43% since inception as the fund persistently pays more than it earns (Figure 6). While not as drastic as my simple example above, the concern is still valid.

Figure 6 - YYY historical NAV (morningstar.com)

Instead of the YYY ETF, investors interested in earning high current income from a diversified portfolio of CEFs may want to consider the Saba Closed-End Funds ETF (CEFS).

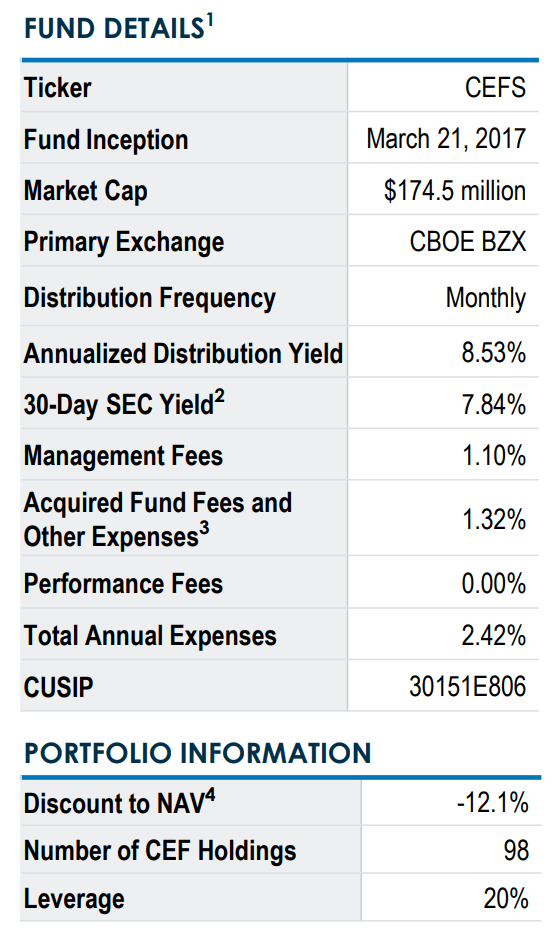

CEFS is an actively managed fund of CEFs managed by the award-winning portfolio managers at Saba Capital with $175 million in AUM paying an 8.5% distribution yield (Figure 7).

Figure 7 - CEFS fund overview (CEFS factsheet)

While the CEFS ETF does not pay as high a yield as the YYY ETF, I believe it is more sustainable, as CEFS has delivered stronger historical returns, with 3- and 5-year average annual returns of 10.2% and 10.0% respectively to February 29, 2024 (Figure 8).

Figure 8 - CEFS historical returns (morningstar.com)

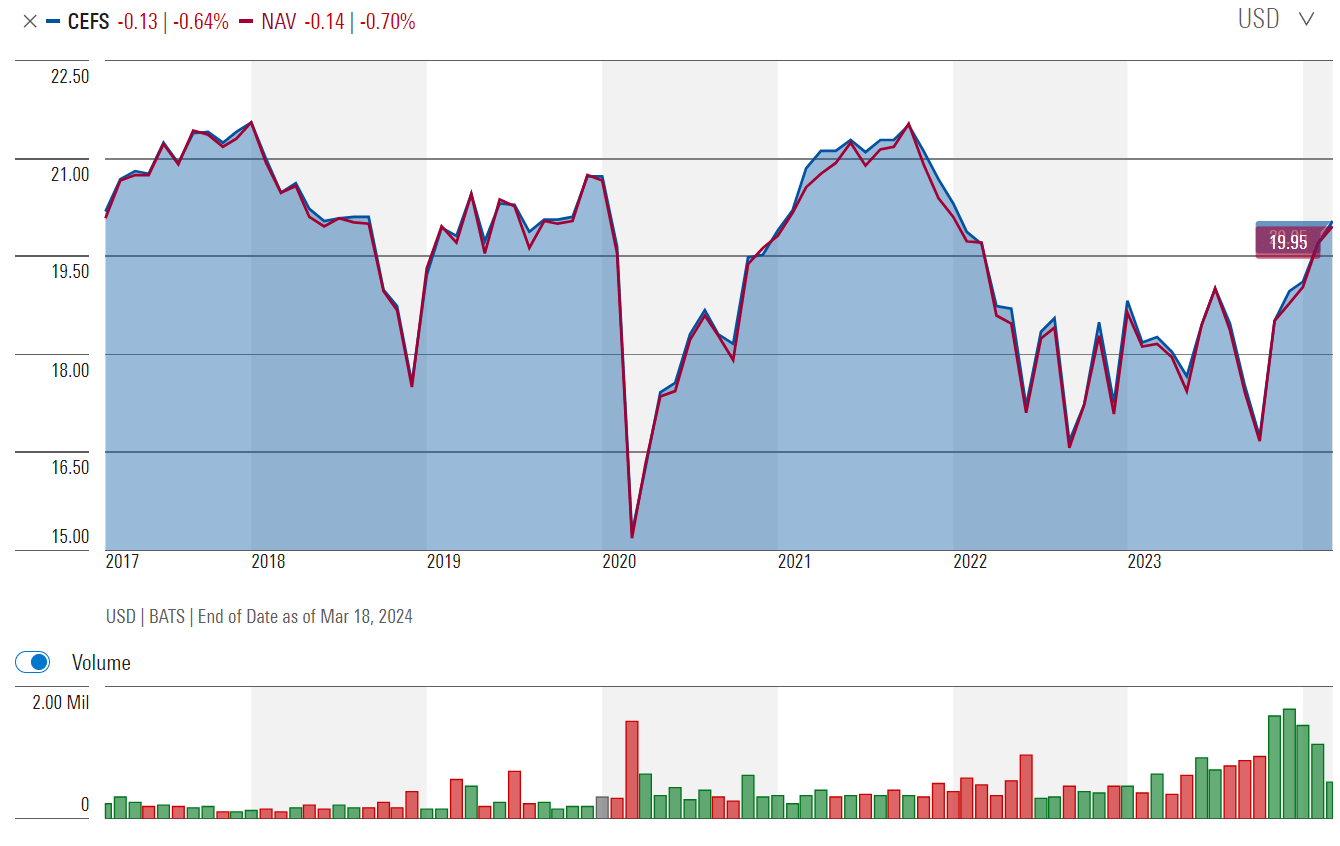

So instead of liquidating NAV to pay its distribution, CEFS's NAV has been flat/stable over the long run (Figure 9).

Figure 9 - CEFS historical NAV (morningstar.com)

I reviewed the CEFS ETF here.

Revisiting the Amplify High Income ETF, I remain concerned about the long-term sustainability of the YYY ETF's distribution. Although 2023 was a good year and the fund was able to earn its distribution, in the long run, the YYY ETF pays more than it earns.

Instead of the YYY ETF, I recommend investors interested in a portfolio approach to CEFs consider the Saba Closed-End Fund ETF, as CEFS has consistently earned higher returns while its more modest distribution policy does not deplete its NAV.

I remain cautious on YYY and rate it a hold.