Brandon Bell

Editor's note: Seeking Alpha is proud to welcome Eduardo Sanchez, CAIA as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Brandon Bell

Fast food chains may seem like a simple business model with low or no potential for growth. However, for Domino's Pizza (NYSE:DPZ), it's quite the opposite. The company has shown exceptional financial performance in the past and continues to do so, indicating a positive trend.

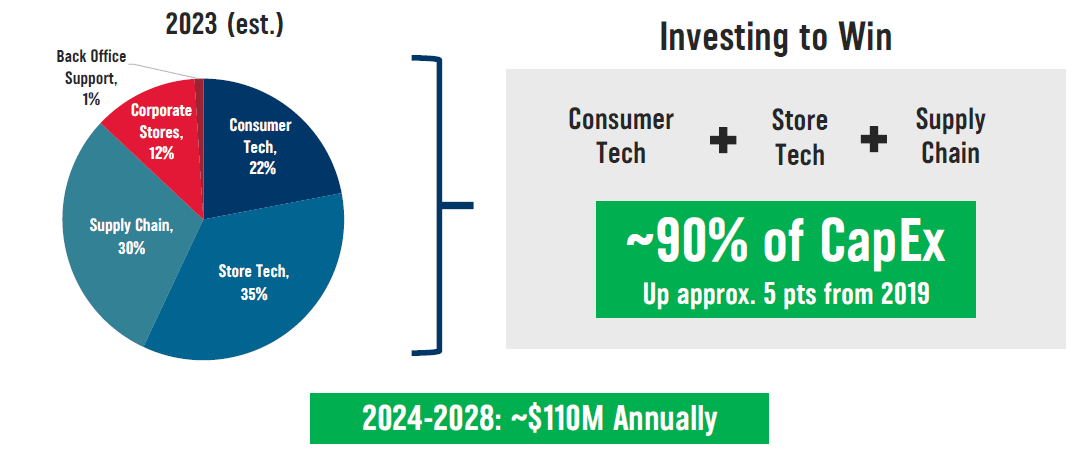

Capital expenses and improvements, including the development of a digital app and AI technology, as well as an increase in global presence, along with share buyback programs and the proven resilience of the sector in recessions, are the main drivers for remaining bullish on Domino's for your 2024 portfolio and beyond. We will discuss each of these factors in the following sections.

FactSet

Technology plays a vital role in today's business world. Companies that fail to innovate are often left behind. Domino's top management understands this well and has invested millions of dollars in their app for their carryout and delivery business. These investments have paid off, as digital sales have increased every year since the inception of the app. Digital sales now account for 85% of total sales in the U.S.

Domino's Investments aims to improve its mobile application's design, usability, and customer experience by introducing dynamic rewards and optimizing customer lifetime value. However, the company has even bigger plans. In late 2023, Domino's partnered with Microsoft (MSFT) to create an AI-powered innovation alliance that will transform the way pizza orders are placed and streamline operations.

Technology not only enhances the consumer experience but also reduces operational risks, improves margins, and increases productivity. Domino's is a unique operating system that streamlines the entire process from order placement to delivery.

2023 Domino´s Pizza Investor Day

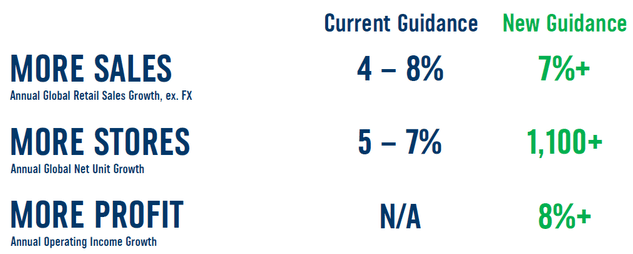

I don't know about you but seeing a large company with proven financial stability projecting a sales growth of 7% or more each year (3% above nominal GDP) makes me wonder if it's worth adding to my investment portfolio. However, growth alone shouldn't be the only factor when analyzing a company. If a business is solely focused on growth, it may shut down if not executed properly.

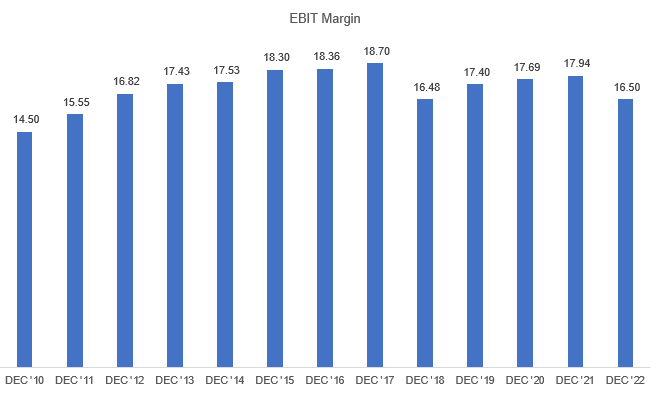

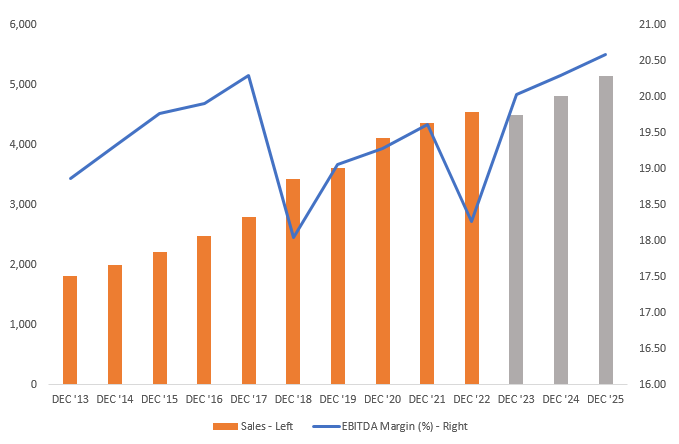

It's good to know that Domino's is now aiming to increase its profits, as the company has been struggling to maintain its margins over the past few years. Looking at the numbers, we can see that their EBIT margin has decreased from 18.7% in 2017 to 16.5% in 2022. While inflation levels in 2022 didn't help the company, it's important to note that margins were still unable to return to the 19% levels in previous years, even when inflation was under control. To boost profits, the company plans to implement digital and AI improvements, which should reduce labor costs associated with daily activities and store operations.

FactSet

Let's take a closer look at Domino's growth estimates. Since 2015, the company has experienced significant growth in global retail sales, store count, and operating income by 80%, 50%, and 100%, respectively.

Most of Domino's growth comes from its international stores. The current international QSR market is valued at USD 53 billion, with Domino's holding the #1 spot as the global player, with a market share of 16%. If you think Domino's has reached its peak, think again. The company plans to open 1,100 new stores each year, primarily in international markets such as India and China.

The target for the total number of stores in the US by 2028 is expected to increase from 6,800 to 7,700, with a long-term target of 8,500. While this represents steady growth, it is important to note that domestic growth is not Domino's primary objective. Therefore, this is not my bullish case for the company.

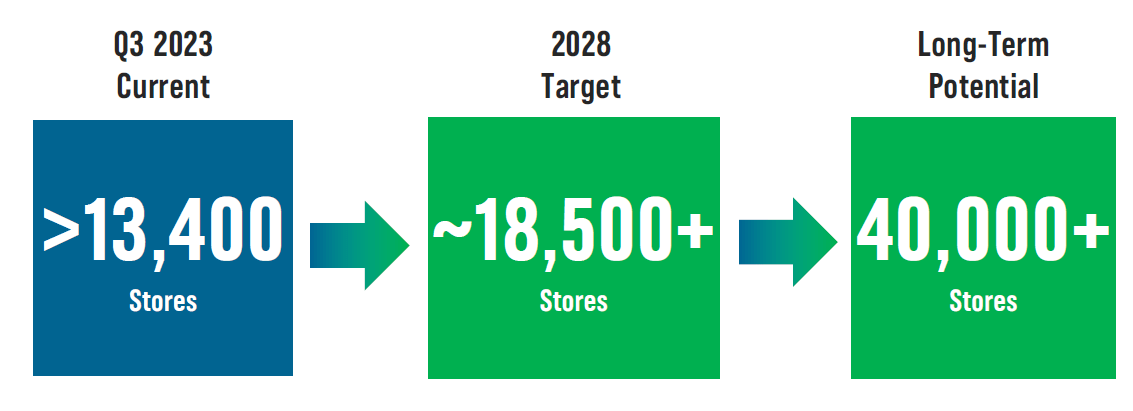

Domino's management is banking on its international business to drive growth. With over 13,000 stores worldwide, the company aims to achieve a 7% CAGR, which could result in sales increasing by more than USD 4BN in the next 5 years or 45%.

Is it impressive? Yes, it is, but the best part is their long-term potential to increase stores by more than 40,000.

2023 Domino´s Pizza Investor Day

Is it Achievable? The International QSR industry has grown at a 5.3% CAGR since 2015 and is projected to expand by 8.88% in the next five years.

Let me show you why Domino's is a sound investment. The chart below illustrates their growth potential.

FactSet

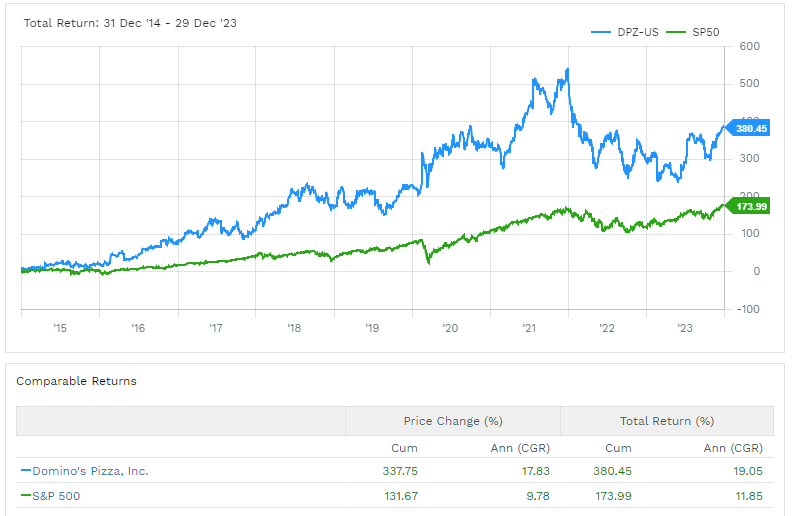

Domino's has outperformed the S&P 500 by more than 2 times over the past 8 years. According to data from FactSet, approximately 30% of the returns have been attributed to share buyback programs and dividend distributions, although there are certain outliers. During the same period, Domino's has reduced its basic shares by 35%. However, its main competitor, Pizza Hut which is owned by Yum! Brands (YUM), has decreased its basic shares by an even greater percentage (36%) but has achieved a similar return to the market. The reason for Yum Brands' performance can be explained by almost 70% of dividend distributions and share buyback programs.

FactSet

It's important to look at the bigger picture before just focusing on the numbers. Although Domino's is increasing benefits for shareholders through capital distributions, it's worth noting that 70% of the return has been attributed to growth initiatives by the management and the successful execution of their strategy over the years, which has been reflected in the upward trend of the stock price.

Current Capital Deployment Priorities are: (i) Reinvest in the Business, (ii) Return Cash to Shareholders, and (iii) Leverage at 4 to 6x EBITDA.

Domino's Pizza has reduced its outstanding shares in the market by issuing debt, as it has discovered that this method is more cost-effective. Currently, all of the company's debt is at a fixed rate, with a Weighted Average Interest Rate of 3.8%. If we calculate the cost of equity using the CAPM Model, we would arrive at a figure of 7.86%.

Cost of Equity= Risk-Free Rate + Beta * Equity Risk Premium

Cost of Equity= 4.17% + 0.83 * 4.45%

Cost of Equity= 7.86%

RF Rate = 10-Year Treasury Beta = 24M Beta

Equity Risk Premium = Implied Equity Risk Premium for February 24

By analyzing these numbers, we can easily conclude that it is less expensive for Domino's to issue debt rather than maintain high levels of capital. However, it's vital to remember the fundamentals of finance: the higher the leverage, the greater the risk for a company to go bankrupt. Nonetheless, Domino's has demonstrated a competent management team to execute these strategies and maintain financial strength simultaneously, with a current Net Debt to EBITDA ratio of 5.5x.

These buyback programs are only implemented if appropriate. According to its 2023 Investor Day:

In 2021, when interest rates were at around 0%, Domino's reduced its shares by 7%. However, during 2022, as interest rates began to increase, the buyback was only about 2% because the cost of debt would increase significantly. It is expected that interest rates will decrease in 2024 and 2025, which would boost Domino's Earnings Per Share by increasing its buyback programs.

FactSet

In 2018, the S&P 500 (SPX) experienced a 6% decline, which was attributed to the trade war between the US and China, sluggish global economic growth, and apprehension that the Federal Reserve was raising rates too fast. On the other hand, during the same period, Domino's Pizza, Inc. recorded a 31% increase in its stock value. How could such a contrasting performance be possible?

The business cycle can be a useful tool for investors to determine where to invest their money. In the event of a possible recession in the United States, it is advisable to allocate investments toward companies that have proven to be resilient. Fast food chains are a good example of such companies, as during these periods, household expenditures were largely reduced due to fear and increased savings, leading to a decline in casual/fancy dining and an increase in fast food/cheap meals. In the same year, Domino's saw a 7% increase in its global stores, which is a smaller number than in previous years, but its sales were up, almost double than in 2017.

In 2020, during the COVID-19 recession, the market increased by 16% while Domino's increased by 31%. When the market collapsed in March, it fell by 30%, but Domino's only fell by 8%. Despite global new stores growing only half as much as in 2019, sales were up almost three times. These numbers were surprising to me and indicate that Domino's was able to weather the economic downturn better than the market as a whole.

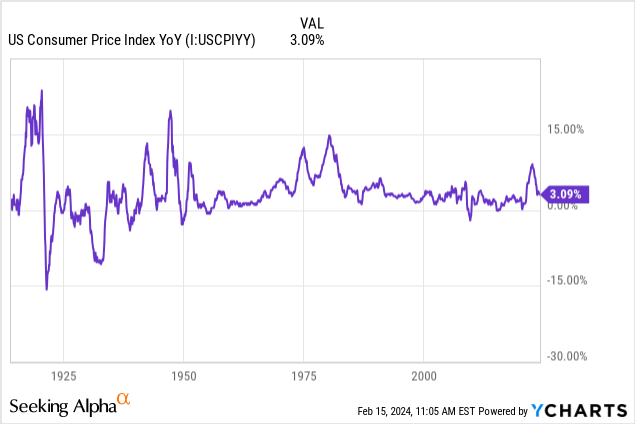

Due to the COVID-19 pandemic, the Federal Reserve and the government injected a large amount of US dollars into the market to support the economy. However, this led to inflation levels that haven't been seen in over four decades.

The latest report on CPI inflation was released on February 13th. It showed that the downward trend of inflation was slowing down with an annualized rate of 3.4%, which is up from 3.1% in December 2023. This could indicate that the Federal Reserve may maintain higher interest rates for a longer time, which could put pressure on the economy and make it a little more difficult to achieve a soft landing.

As I stated, the business model of Domino's Pizza has demonstrated resilience during economic downturns and has continued to grow at a rate higher than the nominal GDP. However, it's also crucial to delve deeper into the past and current data to gain a better understanding of the situation.

FactSet

As previously mentioned, analyzing profits is crucial. In my opinion, I would prefer a company with flat or slower growth but with higher profit margins, rather than a company that's constantly growing but becoming less profitable every year. Fortunately, Domino's Pizza Inc. fulfills both criteria. The company has been experiencing a 10% Compound Annual Growth Rate (CAGR) in sales over the last decade, and this trend is expected to continue. Moreover, the management has made it a priority to focus on increasing profits.

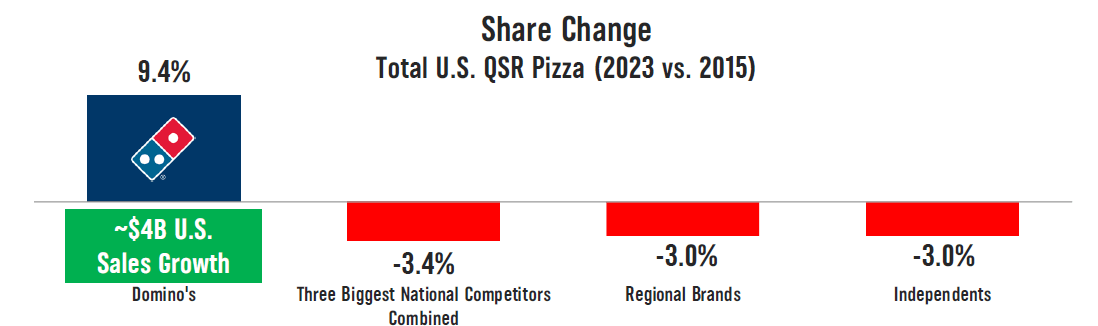

Selling pizzas may seem like a straightforward business where anyone can become a supplier. This means that the barriers to entry are low, and the business model is easy to replicate. During their 2023 Investor Day, the company presented how they had increased their market share within the U.S. from 2015 to 2023. Despite the high level of competition and low entry barriers, Domino's has managed to maintain its market share due to the intellectual property it has developed over the years. This makes it harder for new or old competitors to take away their market share.

FactSet

In my opinion, Domino's has demonstrated adequate management to achieve its goals and even surpass them. Comparing its numbers to those of its main competitors only confirms this.

FactSet

The Return on Invested Capital of the two companies, YUM Brands and Domino's, is impressive. While YUM Brands has a return of 40%, Domino's has surpassed 50%. This is largely due to both companies reducing their outstanding shares. However, Domino's has been more profitable than YUM Brands.

At first glance, Domino's Price to Earnings ratio may seem high, but when adjusting for Long Term Expected Growth, the company does not appear to be expensive. On the other hand, YUM Brands seems to be the cheapest in terms of Price to Earnings ratio.

When looking at the sales growth of these companies, Papa John's (PZZA) seems to be the cheapest.

As outlined, Domino's Pizza does not exhibit the best numbers in all areas. It is not the most affordable option in several cases and does not possess the most favorable profit margins. However, it is essential to recognize that some competitors do not follow a similar business model. For instance, McDonald's (MCD) does not offer Pizzas, and YUM does not solely focus on Pizzas as it has a diverse range of Fast Food Chains in its portfolio.

When comparing Papa John's to its closest competitor, Domino's, we can see that Papa John's has achieved higher EBITDA and EBIT growth. However, as I mentioned earlier, I believe that a company with less growth, but higher profits is more desirable. By examining the margins and ROICs, we can see that Domino's provides greater value to its shareholders.

FactSet

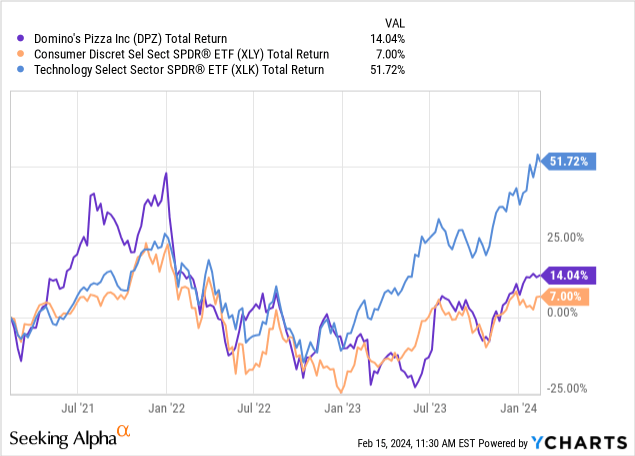

After discussing the investment thesis in detail, let's take a more technical approach. In late 2021, stocks began to surge as worries of COVID eased. Domino's outperformed the technology sector due to its digital business model and delivery services, which benefited the company as people were still hesitant to dine in restaurants. However, 2022 was a challenging year for stock investors due to fears of inflation and high-interest rates.

A year later, most investors allocated their funds to the technology sector due to low multiples, leaving other sectors behind.

And so the opportunity begins...

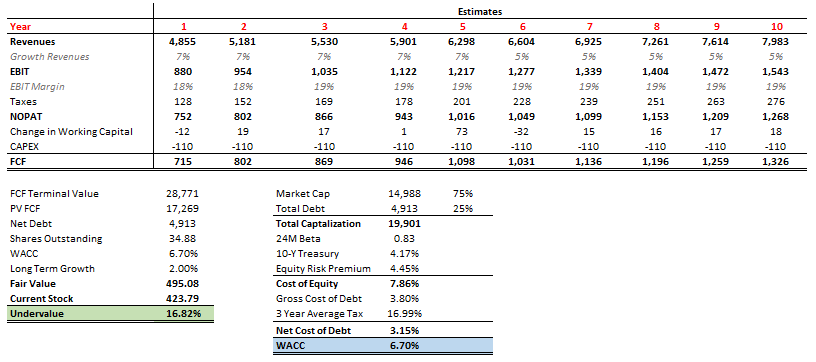

After understanding all the information given and analyzing it fundamentally, I like to use a Discounted Free Cash Flow Model to confirm if the company is undervalued or overvalued. I run a 10-year model to conclude once more if the opportunity is favorable.

For estimates, I have assumed the following:

1 - Revenue growth has been taken from Domino's Guidance for the first 5 years. From years 6 to 10, the calculation has been made through Solver to get a 5.10% CAGR Growth in 10 years (Fast Food Market Expectations).

2 - CAPEX has been taken from Domino's Guidance for the first 5 years. From years 6 to 10, calculations have been considered as if CAPEX remains the same as the 5th year.

2023 Domino´s Pizza Investor Day

3 - EBIT / Taxes / Dep & Amort have been taken from FactSet Guidance for the first 5 years. From years 6 to 10, calculations have been considered as if EBIT / Taxes / Dep & Amort % remains the same as the 5th year.

4 - FactSet Economics Research has provided the expected growth in U.S. Real GDP for the year 2028 and beyond. While some may prefer to use nominal GDP as it could yield a better number, I choose to maintain a conservative stance and keep a certain margin of error.

Damodaran, Seeking Alpha, FactSet, Domino´s Pizza

Discounted Free Cash Flow Models suffer from the disadvantage of being subject to personal bias. To mitigate this issue, I rely on external inputs such as guidance from the same company or a reliable software and financial data provider. This helps ensure that my models are accurate and unbiased.

As I mentioned previously, I am positive about the stock due to all the fundamental analyses conducted. Moreover, when I ran a Discounted Free Cash Model using external estimates, it confirmed that the company is undervalued. This just strengthens my belief that investing in Domino's is a good bet.

No, it is not. As we have discussed all the good things, it is also important to talk about the main risk that Domino's is exposed to, or that you as a potential investor could bear.

Despite having a strong brand and loyal customer base, Domino's faces tough competition in the pizza industry due to low entry barriers. However, the company's intellectual property helps to reduce this risk.

Labor costs and food costs, which include cheese, usually make up around 55% to 65% of the sales at a typical store owned by the company. This means that if inflation remains high, it may continue to put pressure on profit margins, and the company may struggle to meet its current goals.

The shift towards new trends in mind and body health poses a major threat to Domino's.

Over the years, Domino's Pizza has been a great performer in terms of stock and growth. However, in the last year, the former has been under pressure. On the other hand, the company's growth prospects are still positive, which makes it a great opportunity for new investors to enter the market or for existing investors to increase their holdings.