Brad Barket/Getty Images Entertainment

Brad Barket/Getty Images Entertainment

After a few tough years, Yext (NYSE:YEXT) finally appears back in growth mode. The AI search business has already become highly profitable, as the company spent some time stripping out costs and improving sales efficiency. My investment thesis remains ultra Bullish on the AI search company trading at multi-year lows despite hinting at returning the business to growth this fiscal year.

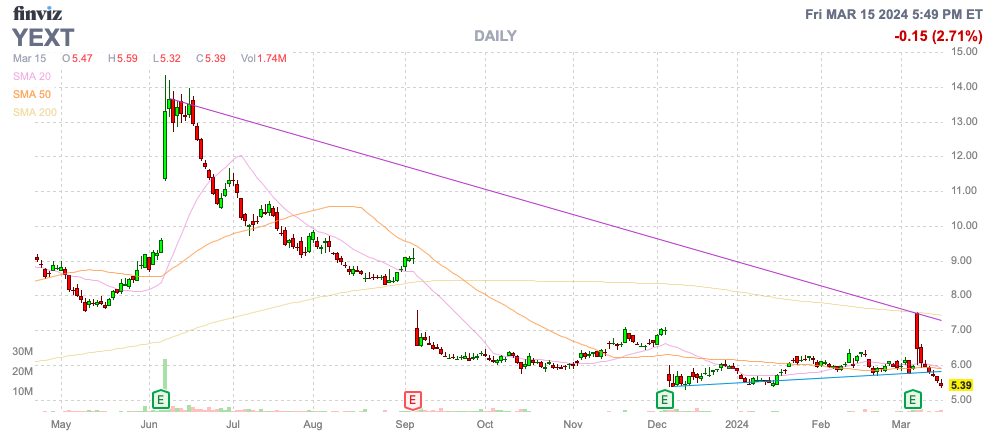

Source: Finviz

The market had a positive reaction to the FQ4'24 earnings report from the AI search company with signs Yext is finally expecting to return to growth after a trough in Q1'25.

Yext press release (YEXT): Q4 Non-GAAP EPS of $0.10 beats by $0.03.

Revenue of $101.1M (-0.8% Y/Y) beats by $0.47M.

The company reported a small beat for FQ4 with revenues of $101 million and a solid EPS beat. Yext has become highly profitable in the last fiscal year leading to operating cash flow of $46 million in the last year on an EPS of $0.34.

Naturally, the market has some concerns with Yext reporting FQ4 revenues dipped nearly 1% and the guidance for FQ1 has to provide concerns. The company faces an ARR hit of $10.8 million from the loss of a big customer, but the market was initially positive on the stock based on the commentary of ARR gains as the year progresses.

Per CEO Mike Walrath on the FQ4'24 earnings call:

But all of that is baked into our guidance, and we do anticipate that in spite of that, we'll see reacceleration of ARR growth into the high single digits by the end of the year.

Yext guided to FQ1'25 revenues of only $96 million in what initially appeared very negative considering the company generated sales of $99 million last April quarter. The market definitely picked up on the FY25 guidance for revenues of $400 to $402 million indicating a positive revenue trend for the year as follows:

A scenario where Yext reports record FQ4 revenues of $105 million and guides towards ARR/revenue growth in FY26 close to 10%, the stock should trade far higher than the current price at only $5. Yext entered the earnings report with an EV of ~$500 million with a sales target of $400 million for a highly profitable company.

Yext has struggled for several years now, but these numbers are the first indication of the company improving sales efficiency and now moving towards reinitiating growth. Now though, the company generates lots of positive cash flow.

The stock immediately jumped to nearly $6.50 on news of the business returning to growth, but the market sold off Yext due to the projected growth cadence. Investors and analysts started plugging in the forecasts and quickly realized the 1H numbers weren't very impressive due to the lost big customer.

Yext starts the year with revenues down YoY, but the company guiding to $3 million in quarterly revenue boosts will alter the investment story. If the company can achieve ARR growth approaching 10%, the stock will be rerated to a higher valuation multiple.

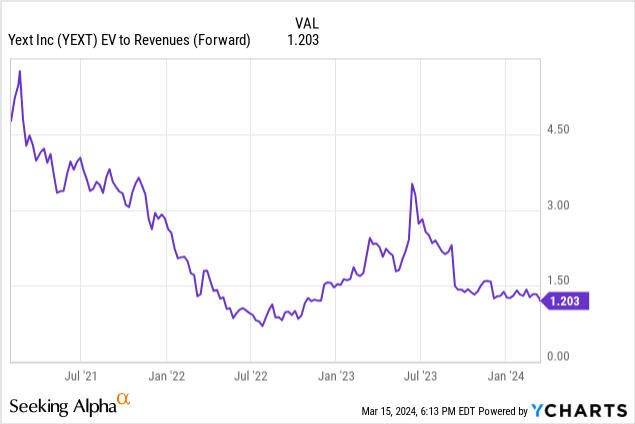

The company currently trades at a forward EV/S multiple of 1.2x. Once factoring in 10% growth and even just a an EV/S multiple of 3x and Yext trades at vastly higher prices.

If the company can just garner market excitement for their generative AI-powered Search product, the sky could be the limit. An AI stock with questionable technology like C3.ai (AI) trades at over 10x sales targets and even has a smaller revenue base closer to $300 million, but the stock is worth $3.5 billion.

While C3.ai has done a better job outlining generative AI pilot deals set to drive growth, Yext is already highly profitable and the company could quickly fall under the Rule of 40 software concept. Assuming the company hits 10% growth rates next FY, the profit margin defined by the 15% adjusted EBITDA margin would already place Yext at the 25 threshold.

The stock multiple would definitely become more valuable with profitable growth and an AI angle. The great unknown is just how high the stock could be rerated, but of course the biggest risk is that Yext doesn't actually return to growing the business.

The key investor takeaway is that investors should use the current weakness to load up on Yext. The company gave every sign the business was returning to growth and the combination with the strong cash flows should warrant multiple expansion. The stock would appear to have limited risk with a $200+ million cash balance while producing solid cash flows, but Yext could just as easy flounder around $5 for years.