Sucharas wongpeth

Sucharas wongpeth

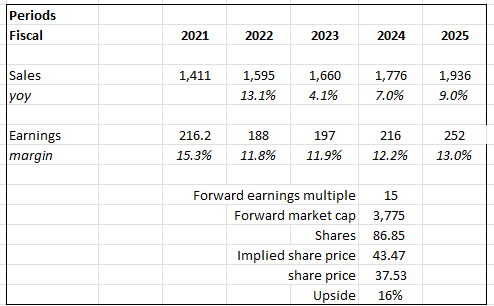

Readers may find my previous coverage via this link. My previous rating was a buy as I believed YETI Holdings (NYSE:YETI) would see growth acceleration due to the new product launches and investment into marketing, and also see a near-term growth boost as it benefits from the sell-in motion to retailers when they stock up. I am reiterating my buy rating for YETI, making the assumption that the key reason for the underperformance was due to a misstep in execution, which can be fixed. FY24 should also benefit from retailers restocking, which drives growth. Looking ahead, I expect YETI to gradually accelerate growth towards low teens, stemming from consumer demand recovery as macro recovers and its M&A strategy to expand its portfolio. While my earnings expectations have lowered, the sharp drop in share price has also reset expectations lower. Assuming YETI were to trade at 15x forward PE, the 1-year upside is still attractive at 16%.

YETI reported 4Q23 adj. revenue growth of 6.3%, which was disappointing when compared to consensus expectations of 10.2%. Gross margin did beat expectations, where the business saw 590 bps expansion to 60.2%, ahead of consensus of 58.8%. However, EBIT failed to meet expectations given the stronger-than-expected OPEX growth, driving the adj. EBIT margin to 19.8%, below consensus of 21%. YETI reported adjusted 4Q23 EPS of $0.90, below consensus of $0.96. For guidance, management guided FY24 EPS of $2.45 to $2.50, stemming from adj revenue growth of 7 to 9% and adj EBIT margin of 16%.

Based on author's own math

Based on my view of the business, I think it is appropriate to be more conservative in my assumptions. Previously, I expected strong growth in FY24 because of new product launches, marketing investments, and retailers restocking their inventories. However, the poor execution seen from the product relaunch (the M-series soft cooler) and the overall weakness in consumer demand led me to believe growth is not going to be that great. Management FY24 guidance also indicates soft growth ahead (5 to 7% organic growth + 200 bps M&A contribution). Turning more conservative, I modeled 7% growth in FY24, followed by a modest recovery in FY25 as YETI grew towards low-teen percentage growth. I have also reset my margin expansion expectation since YETI needs to further step up in marketing to drive growth in FY24. Management guided FY24 adj net income of $216 million, which equates to 30bps expansion. I expect FY25 to see a larger expansion as it does not need to do another round of step-up marketing to address the M-series soft cooler issue; it should benefit from fixed cost leverage as sales volume recovers; and I expect the red sea situation to be resolved by then, which will result in a lift in gross margin as freight costs come down.

All in all, my earnings expectation for FY25 has lowered from $287 million to $252 million, and because of a lower earnings growth expectation, I think YETI should trade at a lower multiple than I assumed previously (18x forward PE). My expectation is that YETI will continue to bounce around the current 15x forward PE until it convinces the market that it reports double-digit percentage top line growth, with margin recovering mid-teens percentage level.

I was honestly disappointed in the top line miss that was driven by Coolers & Equipment's y/y sales decline of 4%. The slowdown was dragged down by a slowdown in consumer spending on big tickets and a sharper slowdown than expected in 4Q23 due to a tough comp (vs. FY22). What was even more disappointing, which caused a major dent in my bullish view, was that management noted sales of newly reissued M-series soft coolers (which were recalled in early 2023) underperformed YETI’s expectations in the quarter due to low awareness and limited color options. This performance has raised two red flags on execution:

The good news is that this is a matter of execution and not a matter of weak demand (assuming the reasons provided by management are true). If that is the case, then what YETI needs to do is simply increase marketing and roll out more color options, and this is exactly what management intends to do. As such, I would not extrapolate this weakness for FY24. In addition, to drive growth in this end-market, management is making changes to some existing cooler products to create new pricing tiers for 2024 product launches. From a macro standpoint, I would say this is a good decision as it would be able to capture a wider range of consumers (vs. just one price point that captures a certain group of consumers).

We expect to fire up our marketing engine to drive deeper awareness of the return and expansion of our soft cooler M Series with extended colorways. Source: 4Q23 earnings

Assuming that the M-series soft coolers issue is fixed, I am pretty confident that YETI can meet its high-single-digit percentage growth guidance. Note that the 7 to 9% guide includes a 200bps contribution from the recent acquisition of Mystery Ranch and Butter Pan, which means organic growth is only expected to be ~5 to 7%, which has an easy comp compared to FY23 4.1% growth. Remember that I mentioned previously that YETI is going to benefit from sell-in motion as retailers restock? Management 1Q24 commentary suggests that this is indeed going to happen. They anticipate a more robust growth rate in 1Q24, thanks to improved wholesale sell-in opportunities than the previous year. The expectation is that POS and shipments will match (sell-in = sell-through) in 2024, but 1Q will see elevated growth as retailers re-stocking after the holiday season.

This relative strength in Q1 largely reflects better wholesale sell-in opportunities as our inventory in the channel is in a much healthier position coming out of this holiday season versus the prior year. Source: 4Q23 earnings

Moreover, this guide does not assume new M&A, which I expect will become a more integral part of YETI’s growth strategy as they seek to expand their product portfolio. This could be a major growth driver, as the M&A logic is to target brands complementary to the YETI portfolio. YETI could become a roll-up company, acquiring brands and leveraging its existing distribution network and brand to drive revenue synergies. There are many instances of CPG companies utilizing such strategies, so I do see a chance for YETI as well, provided it is well executed. With M&A in the growth equation, I believe YETI could achieve its long-term double-digit (probably low-teens) revenue growth target, which management reiterated today.

And then when you add in our philosophy and our approach to M&A as an innovation extension, we announced the Mystery Ranch acquisition and the Butter Pat acquisition really as expansionary in the product portfolio. Source: 4Q23 earnings

I think the key risk here relates to execution. The misexecution regarding the M-cooler series was pretty major, and if such mis-execution continues, it would definitely impact growth. Importantly, it will likely lead to management’s losing creditability, which will lead to investors taking a more conservative stance in their expectations, even when guidance points to strong performance.

I maintain my buy rating for YETI despite a weak 4Q23, as the stock's upside remains attractive after expectations have reset. While disappointed with the top-line miss driven by Coolers & Equipment sales decline, particularly in the M-series soft cooler relaunch, I attribute this to execution missteps that can be rectified. Management's commitment to increasing marketing and expanding color options is a positive response to address the issues. As consumer demand recovers (as the macro environment recovers) and management executes well on the M&A front (that leads to a broader product portfolio), I see potential for YETI to achieve its long-term double-digit revenue growth target. The key risk lies in execution; continued missteps could impact growth and erode investor confidence.