PM Images

PM Images

I feel as if covered-call exchange-traded funds, or ETFs, are losing their appeal, considering there are many new products that incorporate different strategies to try to add a level of risk mitigation to the market. At the upcoming FOMC meeting this week, the market is also looking for Fed Chair Powell to expand on his testimony on the Hill about what data would instill a level of confidence that would make the Fed members feel confident that a decision to start the rate cutting cycle is appropriate.

As we exit a rate tightening cycle that took rates to over 500 bps at a record pace since the early 1980s, traditional income-producing equities will start to look more attractive as their yields won't be overshadowed by the risk-free rate of return. While ETFs such as the Global X S&P 500® Covered Call ETF (NYSEARCA:XYLD) haven't really expanded their assets under management (AUM) I still think XYLD can deliver further upside and above-average yields throughout 2024.

To be fair, XYLD is not an investment that will appeal to the masses, as it's an income-focused investment. If you're looking for capital appreciation that will replicate the market, I don't believe XYLD will accomplish that goal. If you're an income investor who is looking for an ETF that can help diversify your income mix and generate above-average distribution income from a yield perspective, then XYLD may be an interesting position. Ultimately, I think XYLD is going higher with the market, and its monthly distribution will satisfy income investors as the risk-free rate of return declines.

Seeking Alpha

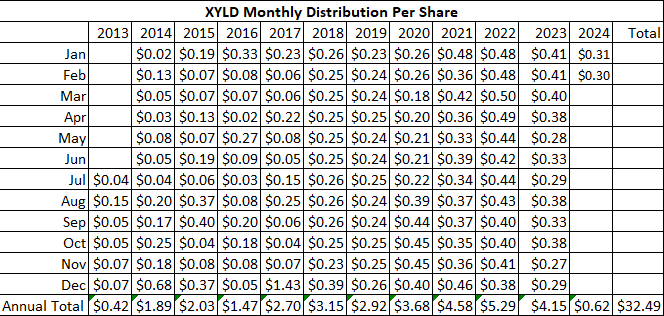

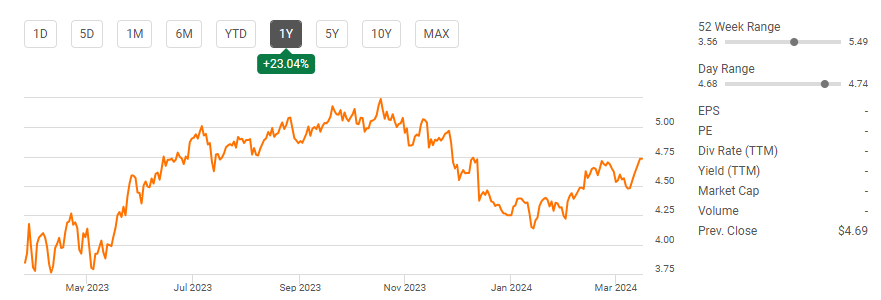

Since my last article about XYLD which was published on 12/25/23 (can be read here), shares have appreciated by 2.37% compared to the S&P 500 (SP500), climbing 7.53%. XYLD's total return when the distributions are factored in is 4.73%, as it generated a monthly distribution of $0.31 in January and $0.30 in February. In my previous article, I discussed how XYLD faired in 2023 after distributing $3.86 from the first 11 monthly distributions declared in 2023. I am following up on this idea as we have an FOMC meeting this week, and it looks as if we are closer to a Fed pivot, where we will see rates start to decline. I think income-producing ETFs, especially covered call ETFs will become more popular in the 2nd half of 2024.

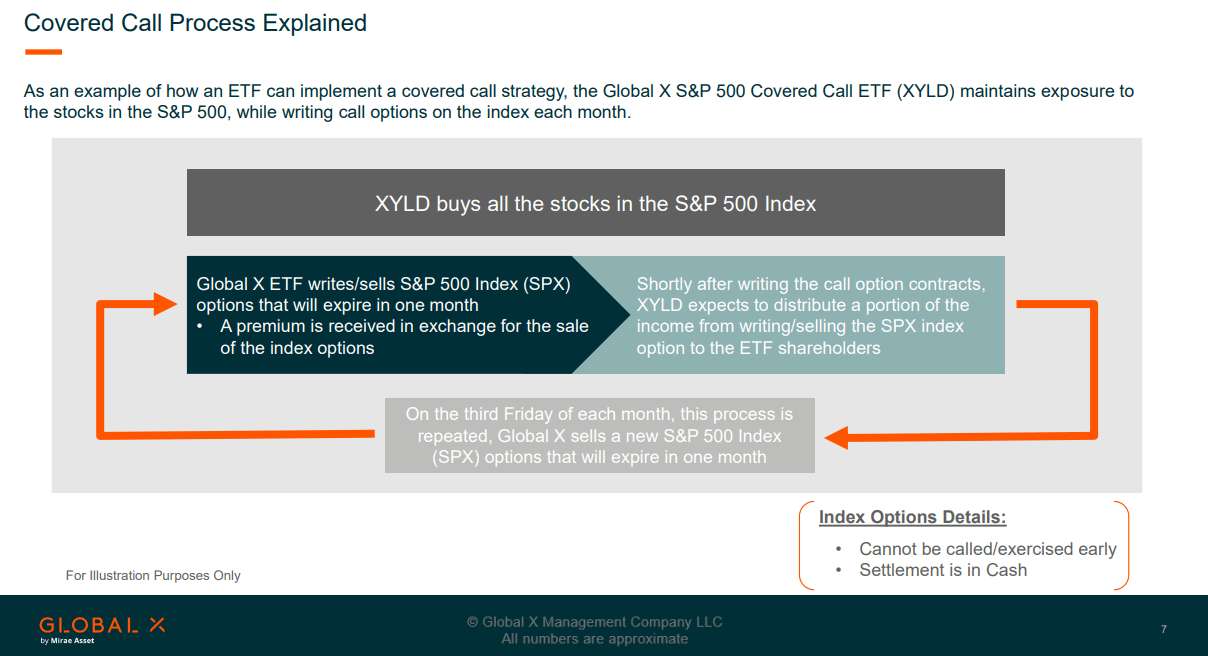

XYLD is an equity-focused ETF that writes covered calls against its portfolio of underlying assets. The risks are similar to those of a standard S&P index fund because if the market declines, so will XYLD, as it holds all of the companies in the S&P 500. While there is the traditional equity risk from market fluctuations and directional trends, XYLD has an added level of risk as the covered calls are limiting its upside potential. By writing covered call contracts on the S&P 500 index, XYLD is exchanging most of the upside potential in an appreciating market for immediate income, which is distributed to shareholders through monthly distributions. This can create a significant opportunity cost, and that's why I indicated that investors who are looking to maximize capital appreciation should probably look for a better fit than investing in XYLD. By investing in XYLD, your accepting that the balance of your investment will not replicate an S&P 500 index fund as you are trading that appreciation for immediate monthly income.

Global X

XYLD had another strong year for generating income as it generated a total of $4.15 per share when you combine the December 2022 distribution that was declared at the end of 2022 and was paid on 1/9/23, with the remaining 11 distributions that were declared and paid throughout the rest of 2023. On 12/28/22, shares of XYLD traded for $39.44, and shares traded ex-dividend the next day on the 29th. If you had locked in the distribution rate at a cost of $39.44, XYLD would have generated 10.42% in forward distribution income after generating $4.15 over the next 12 months. No matter what an individual opinion is on the mechanics of how XYLD generates and distributes income, the facts are that on 12/28/22, XYLD traded for $39.44, and over the next year the distributed income correlated to a 10.42% yield on cost.

If you purchase a 10-year bond, you're not expecting the face value to appreciate when the maturity date hits. You expect to get the face value back on the investment while having collected 10 years of interest payments along the way. Today the 10-year bond yield (US10Y) is 4.31% and in the summer of 2013, the 10-year had a yield of around 2.5%. If you had purchased $4,000 worth of 10-year bonds in July of 2013, you would have collected $100 per year in interest for 10-years, totaling $1,000 of income. After these bonds had matured in July of 2023, if you rolled them into more 10-year bonds, you would have locked in a yield of around 4%, which would generate $160 of income on an annual basis and $1,600 of income during the duration of these bonds until the next maturity date in July of 2033. Over 20 years, you would generate $2,600 in income from the $4,000 in 10-year bonds.

XYLD IPO'd at $40 per share and has paid 130 monthly distributions since going public. If $4,000 was put into XYLD rather than a 10-year bond in July of 2013, 100 shares would have been purchased. These shares would be worth $4,055 today, an increase of 1.38%, while having distributed $3,249 from the monthly distributions without factoring in reinvesting the distributions along the way. In less than 11 years, XYLD has paid 81.22% of its initial IPO price in distributed income, and for an investor that purchased 100 shares of XYLD rather than putting $4,000 into 10-year bonds, they would have already generated an additional $648.70 than the $2,600 of income 2 consecutive 10-year bonds would have generated since July of 2013. Suppose you have a long-term investment horizon and can stomach share price fluctuations. In that case, XYLD has been an incredible proxy for allocating capital to risk-free investments such as bonds or CDs from an income perspective.

Steven Fiorillo, Global X

The T-bill and chill methodology picked up a lot of steam in 2023 as investors were able to lock in more than 5% at times on the 2-year notes (US2Y) and over 4% on the 10-year notes. While investors were clinging onto a large risk-free rate of return after coming off the S&P 500 declining by -19.44% in 2022, the S&P 500 left the high-yield environment in the dust, having appreciated by 24.23% in 2023. Nobody can predict the future, but the S&P 500 is already up 7.28% YTD, and it doesn't seem like the trend is going to reverse into the negative. The CME Group is predicting that there is a 98% chance that rates remain the same after the FOMC meeting this week, but there is a 58.8% chance that the rate-cutting cycle will have started by the June meeting.

XYLD's income-generating ability isn't tied to collecting dividends, as its strategy of writing call options against its portfolio has established a long track record of generating above-average yields. In recent years, XYLD has generated around a 10% annualized yield and has sustainably generated more income than many individual equities in addition to risk-free assets. I think that the market is going higher in 2024, and that should create minimal upside for XYLD, but I think their assets under management, or AUM, will grow as more investors look to recreate the amount of income they were generating from the risk-free rate of return and realize that XYLD has delivered continuous monthly income that surpasses the yield from many other investments.

Seeking Alpha

While there are many investment products that are geared toward manufacturing income on the market, I am still bullish on one of the pioneers in the space, XYLD. If you're not focused on manufacturing income, then XYLD isn't going to be an appealing investment for you. I fully expect XYLD to trail the market because much of the upside is capped from writing covered calls against its positions despite replicating the S&P 500 index with its investment mix.

With the risk-free rate of return projected to decline in the 2nd half of 2024, I think there will be a focus on recreating yields that investors were accustomed to generating and that XYLD could become more appealing in the income investor community. I am long XYLD as part of an overall income strategy mix as it's produced over a decade of monthly distributions.