Robert Way

Robert Way

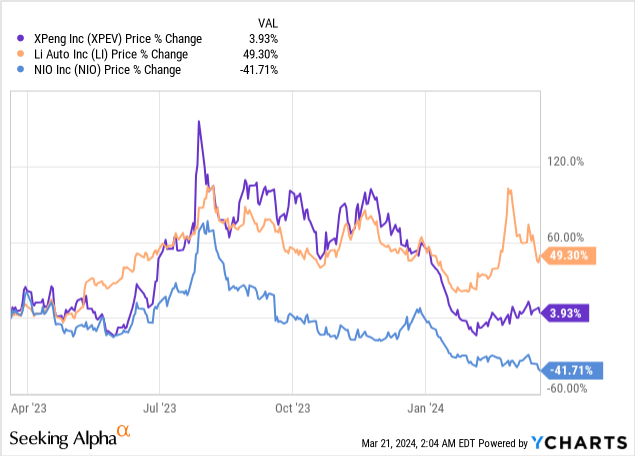

Chinese electric vehicle manufacturer XPeng (NYSE:XPEV) submitted a strong earnings sheet for the fourth fiscal quarter on Tuesday that saw a significant earnings beat, continual top-line momentum related to EV sales, and an improving trajectory in terms of vehicle margins. However, the company is still not profitable and not expected to be at least for a few more years. While the margin picture clearly improved in Q4'23, I believe XPeng's valuation especially is not attractive enough to justify establishing a long position in this EV maker at the current time. My preference in the Chinese EV start-up market, due to superior performance, better execution, and a lower valuation, remains Li Auto (LI) which I believe is still the best deal in the Chinese EV start-up niche that investors can buy!

Because XPeng was being outperformed in terms of revenue and delivery growth by Li Auto in 2023, and because XPeng had the highest P/S ratio in the Chinese EV start-up group, I only rated the EV company a hold in my last coverage in November: Margin Pressures Persist. Following the Q4'23 earnings report, we see an improving vehicle margin trend developing which I believe is a positive. However, from a valuation perspective, I still believe investors can get a much better deal with Li Auto than with XPeng.

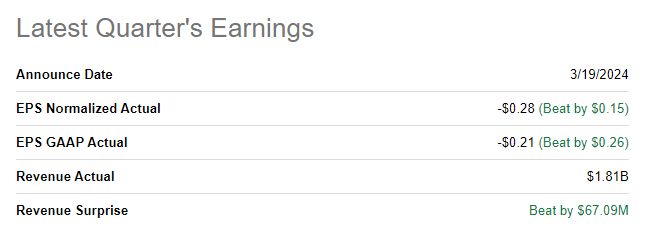

The Chinese EV maker delivered solid earnings for the fourth quarter this week that beat the consensus estimate by a considerable margin. XPeng generated $(0.28) per share in adjusted earnings on $1.81B in revenues, thereby beating the adjusted consensus prediction by $0.15 per share. The top line came in $67M better than expected.

Seeking Alpha

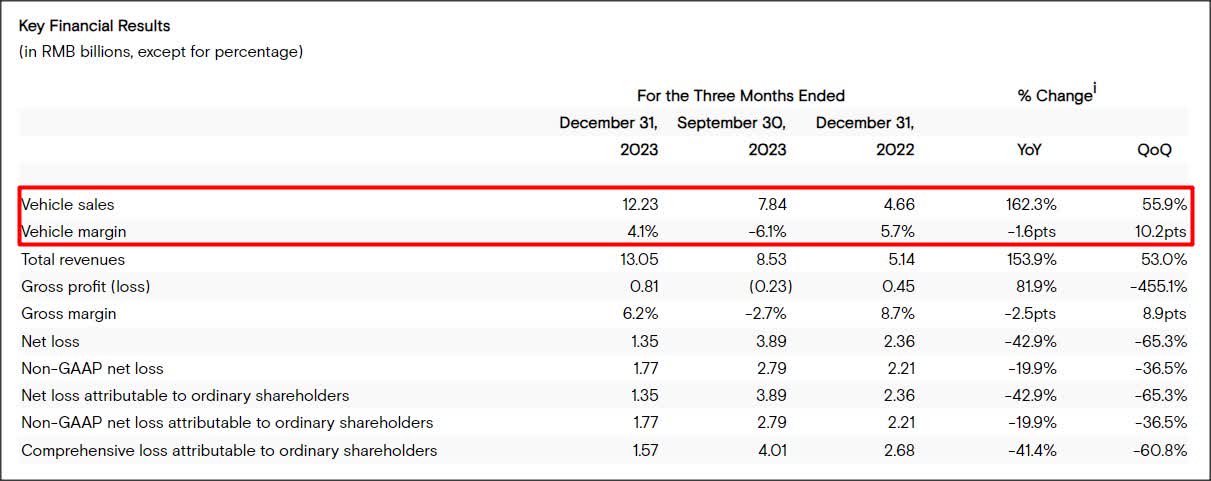

XPeng benefited from considerable top-line momentum in the fourth quarter: The EV company generated 13.1B Chinese Yuan ($1.84B) in Q4'23, showing a year-over-year growth rate of 153.9%, chiefly because EV sales gradually ramped up throughout the year. The biggest takeaway from XPeng's earnings report, however, was that the vehicle margin trend is improving. XPeng has suffered from intense price competition, which was kicked off by Tesla (TSLA) early last year, resulting in vehicle margins dropping into negative territory in 2023.

XPeng's vehicle margins in Q4'23 were 4.1%, representing a significant improvement compared to the previous quarter which is when margins were negative 6.1%. Li Auto still had the highest vehicle margins in the EV industry start-up group with a Q4 margin of 22.7%. NIO (NIO) reported a vehicle margin for the most recent quarter of 11.9% and a margin expansion in this vital metric of 0.9 PP Q/Q. Therefore, both Li Auto and NIO have significantly higher vehicle margins than XPeng, which I believe further supports my decision to remain on the fence with regard to the EV maker.

XPeng

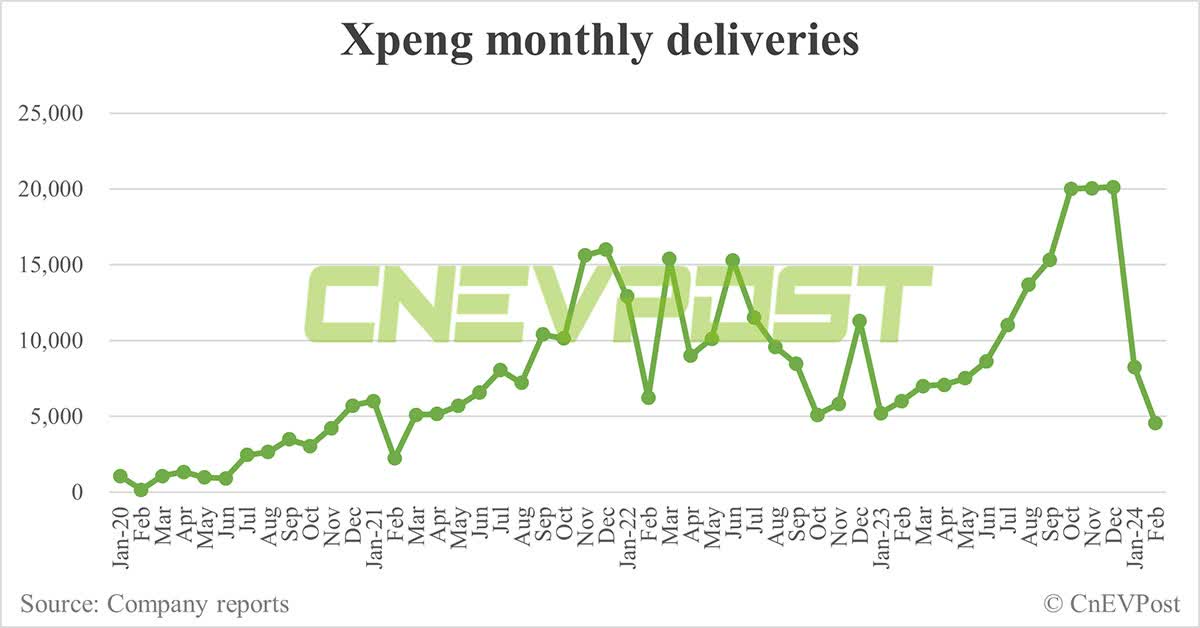

XPeng has seen a steep drop-off in vehicle sales in February as well which was related to the Chinese New Year period. XPeng delivered only 4,545 electric vehicles in February, showing a year-over-year decline rate of 24.4%. Li Auto, on the other hand, delivered 20,251 electric vehicles in February 2024, showing 21.8% Y/Y growth. NIO managed to deliver 8,132 electric vehicles to customers which represented a year-over-year drop of 33.1%.

CnEVPost

The Chinese New Year period, which falls into February, regularly leads to drop-offs in delivery volumes and they typically recover in the months after February. XPeng's guidance for the first quarter calls for a delivery volume of between 21,000 and 22,500 electric vehicles in the current first quarter, implying 19% year-over-year growth at the mid-point.

Although XPeng is seeing some decent top-line momentum and margins are expanding, Li Auto is simply executing better while at the same time offering a much more compelling valuation. Li Auto, which is also already profitable, therefore offers investors stronger delivery and top-line growth, vehicle margins that are 5.5X higher than XPeng's, and a lower valuation based off of P/S.

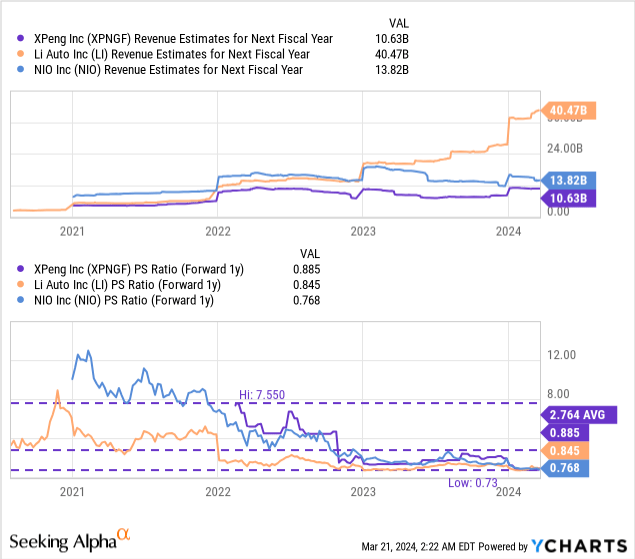

I am using a price-to-sales ratio for purposes of valuation because XPeng and NIO - two of the most highly-valued Chinese electric vehicle companies - are not yet profitable and are not expected to be for at least a couple more years. XPeng is currently valued at a P/S ratio of 0.89X, which I find baffling considering that Li Auto, despite much stronger growth and better execution, is trading at a price-to-sales ratio of 0.85X. Li Auto this week reduced its Q1'24 delivery forecast from a range of 100-103k to 76-78k, citing weakening demand in the EV market. However, despite this macro headwind, Li Auto is still, based off of vehicle margins, the most profitable EV maker in the start-up industry, and I am continually adding to my Li Auto investment holding.

NIO's shares are now at risk of falling into penny stock territory and have the lowest P/S ratio in the industry group.

The average P/S ratio in the industry group is 0.83X, so XPeng's price-to-sales ratio is slightly higher. I consider XPeng to therefore be about fairly valued at the current price level of $9.50, but I see limited upside potential until the EV firm manages to steer the company toward profitability.

There is a general risk that demand for electric vehicles is slowing down which would obviously negatively impact EV start-ups like XPeng. Another risk I see relates to pricing pressure and the margin trend. XPeng's margins just improved, so fiercer price competition in the EV market could make a dent in margins again... in which case I would also project growing headwinds for the company's valuation factor. XPeng's margin trend as well as the firm's delivery growth are two metrics that are worth tracking in 2024.

XPeng had a solid fourth quarter and the company achieved significant, triple-digit Y/Y revenue growth. The most significant takeaway from the company's fourth-quarter earnings sheet was that the margin trend is finally improving and vehicle margins returned to a positive territory in Q4. Nevertheless, XPeng's vehicle margins remained low compared to its rivals Li Auto and NIO in the Chinese EV start-up group. While the margin trend was a positive surprise, I will remain on the fence with regard to XPeng's valuation. For now, Li Auto remains the best deal for investors seeking exposure to the Chinese EV industry!