Analysts Have Lowered Expectations For Xometry, Inc. (NASDAQ:XMTR) After Its Latest Results

There's been a major selloff in Xometry, Inc. (NASDAQ:XMTR) shares in the week since it released its full-year report, with the stock down 40% to US$18.00. Xometry reported revenues of US$463m, in line with expectations, but it unfortunately also reported (statutory) losses of US$1.41 per share, which were slightly larger than expected. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on Xometry after the latest results.

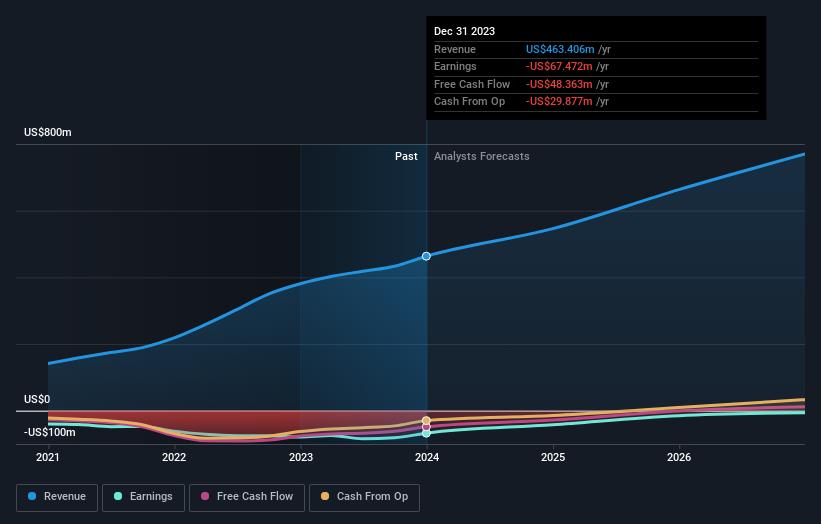

View our latest analysis for Xometry

Taking into account the latest results, the consensus forecast from Xometry's nine analysts is for revenues of US$546.1m in 2024. This reflects a notable 18% improvement in revenue compared to the last 12 months. The loss per share is expected to greatly reduce in the near future, narrowing 37% to US$0.87. Before this earnings announcement, the analysts had been modelling revenues of US$593.9m and losses of US$0.44 per share in 2024. While this year's revenue estimates dropped there was also a sizeable expansion in loss per share expectations, suggesting the consensus has a bit of a mixed view on the stock.

The average price target fell 23% to US$26.14, implicitly signalling that lower earnings per share are a leading indicator for Xometry's valuation. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. There are some variant perceptions on Xometry, with the most bullish analyst valuing it at US$32.00 and the most bearish at US$19.00 per share. As you can see, analysts are not all in agreement on the stock's future, but the range of estimates is still reasonably narrow, which could suggest that the outcome is not totally unpredictable.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. It's pretty clear that there is an expectation that Xometry's revenue growth will slow down substantially, with revenues to the end of 2024 expected to display 18% growth on an annualised basis. This is compared to a historical growth rate of 39% over the past three years. Juxtapose this against the other companies in the industry with analyst coverage, which are forecast to grow their revenues (in aggregate) 5.3% per year. Even after the forecast slowdown in growth, it seems obvious that Xometry is also expected to grow faster than the wider industry.