Ievgen Postovyk/iStock via Getty Images

Ievgen Postovyk/iStock via Getty Images

Note: Dollar amounts refer to USD. Please also note BHP's financial year ends June 30, so December 31 is the half-year period.

BHP Group Limited (NYSE:NYSE:BHP) reported its half-year earnings this past week and profits allegedly dropped by 90% on weak nickel prices:

Seeking Alpha

The negative reports may be partially why BHP's stock is down from the recent highs and close again to technical support levels. However, we need to understand the "90% profit plunge" in the proper context:

BHP

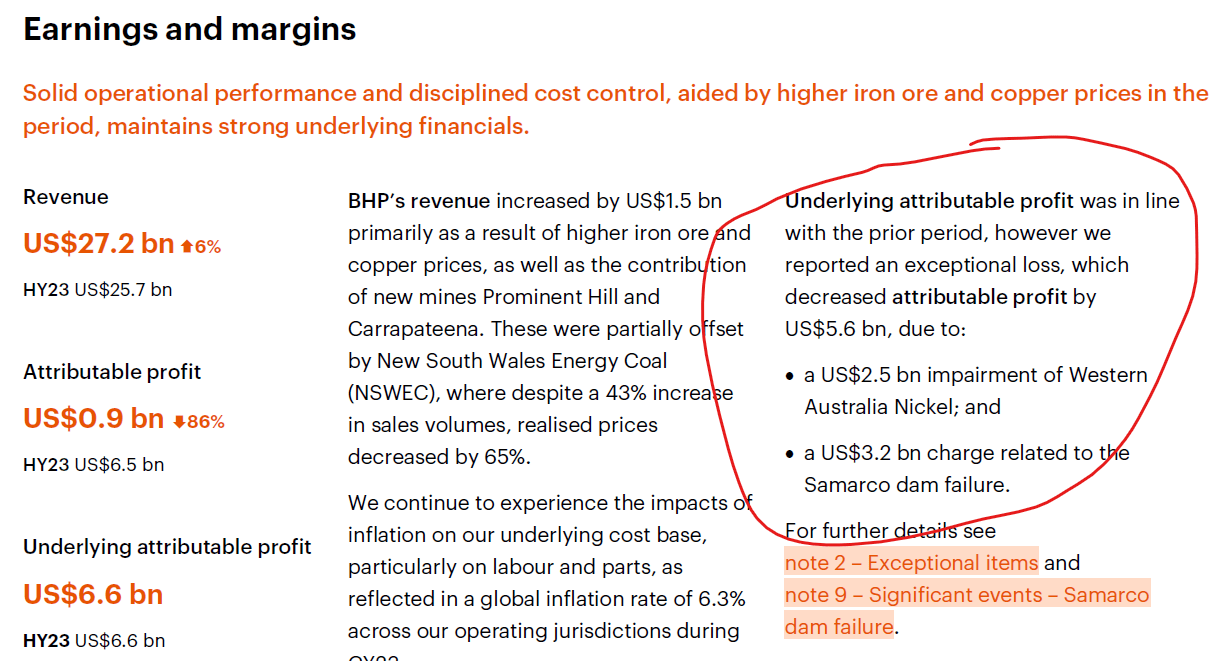

Namely, profit was basically down on two non-cash charges, an impairment of the company's nickel assets and increase in its provision (i.e., expected future liability) related to an environmental incident in Brazil back in 2015:

BHP earnings

While I don't want to completely dismiss these accounting events as they may carry some new information for investors, it should be clear that neither of them has an effect on BHP's current profits in the economic, rather than the accounting, sense of the word. Without these non-cash charges, profit was flat with the respective period a year ago ending 31 December 2022, and 2022 is a tough comparable to beat given the strong commodity prices we had back then.

Moreover, nickel itself isn't a big contributor to BHP's bottom line compared to copper (COPX), iron ore or metallurgical coal. As for the environmental liability in Brazil, more difficulties in the resolution process with the government there do indeed indicate a greater cash outlay in the future, but that is still a one-off charge. It doesn't permanently reduce BHP's earnings potential by 90%.

The pricing on BHP's core commodities remains stable and I remain bullish based on my original thesis - namely, the energy transition is providing a structural tailwind for these commodities while cyclical headwinds are about to reverse as central banks move from tightening to easing policies:

Seeking Alpha

The recent selloff on the earnings, perhaps augmented by the broader pressure on mining stocks since the start of 2024, has pushed BHP back close to what I find an important support area. We have also seen from last quarter's 13-Fs that some institutional "smart money" has started adding mining stocks. As one of the behemoths in the space BHP will benefit too from these capital flows.

I think the above confluence of events has brought us another entry point although if the mining sentiment remains poor for a bit longer, we could possibly see $54-$56 again. I can't of course predict what the market will do, but it's never a bad idea either to scale in gradually into a new position.

In one word, price:

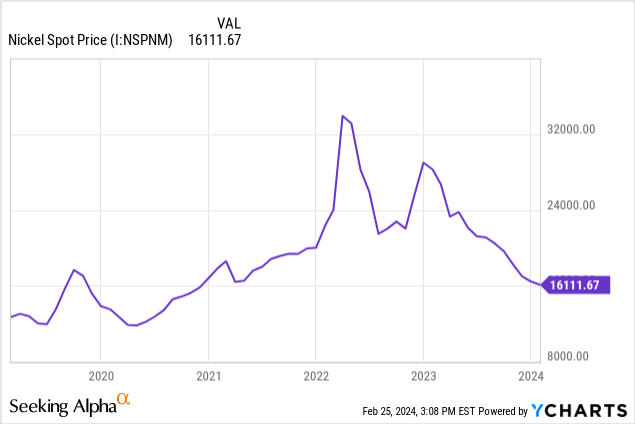

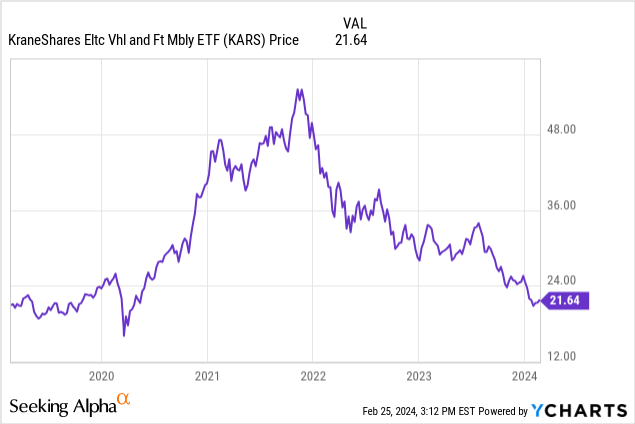

Why nickel crashed is a separate question, but from what I gather too much supply was brought online in anticipation the EV euphoria will go on. However, as electric vehicles have recently faced some headwinds, we seem to have ended up with too much nickel, at least for the time being.

Here is for example the "KARS" electric vehicle ETF (KARS):

BHP reports under IFRS (the International Financial Reporting Standards), and, similarly to US GAAP, IFRS requires management to test the carrying value of the assets on the balance sheet for impairment. When the market value exceeds the carrying value, the latter is written down the to the former, i.e., an "impairment" is recorded which is a reduction to earnings.

In this case, BHP had to write down the value of its Western Australia Nickel asset and that brought earnings down by $2.5 billion post-tax. The trigger for the impairment exercise was the collapse in nickel prices:

BHP press release

If nickel prices remain low, that will impact future profits, but the impairment itself is a non-cash charge and doesn't really impact what the company "earns" currently.

If nickel were one of BHP's principal cash cows, management stating that it believes the price collapse is permanent enough to trigger the impairment could perhaps be argued as a reason for the a selloff. However, that is certainly not the case here.

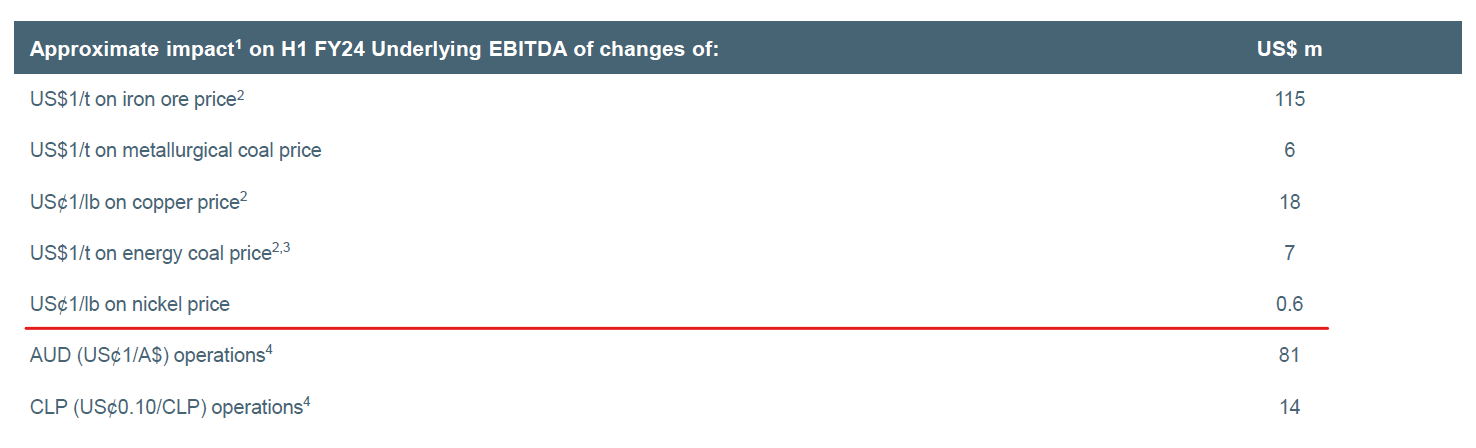

BHP's investor relations team has been kind enough to publish periodically a "sensitivity" table that shows how the company's projected EBITDA would vary with changes in the underlying commodity pricing:

BHP

The latest nickel spot prices have been around $7.70/lb. Let's suppose nickel doubles overnight. Based on the company's sensitivity chart, that would be incremental EBITDA of $462 million. Yet the latest half-year report shows $13.9 billion in EBITDA, so doubling nickel's price will increase BHP's bottom line only by about 3%.

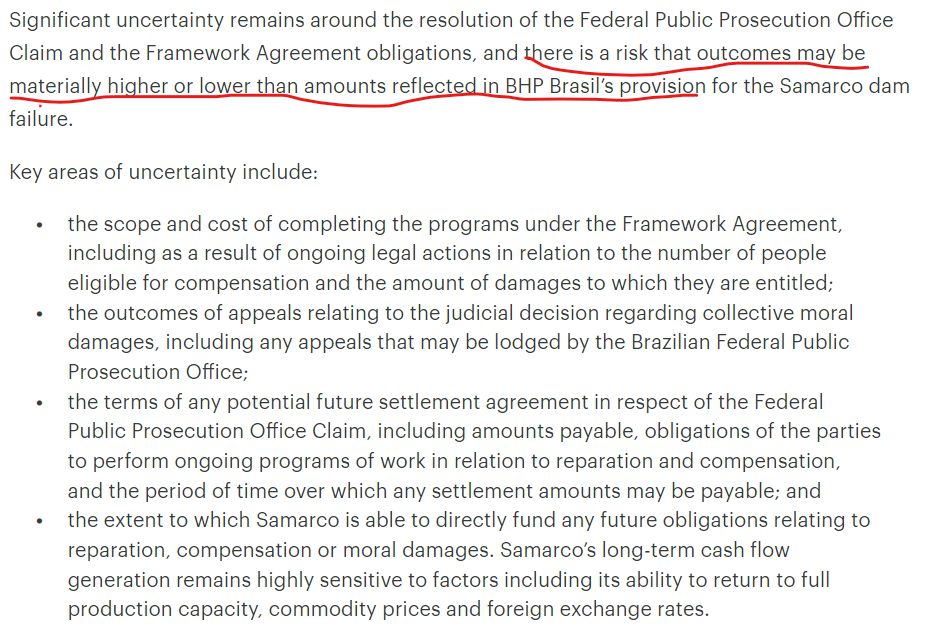

Besides nickel, accounting profit was reduced by a second non-cash charge of $3.2 billion post-tax related to BHP increasing its provision for the Samarco dam failure in Brazil. The provision is basically a reserve to cover a future liability and you can think of it as the mirror image of the nickel situation.

Samarco is BHP's joint venture with Brazil mining giant Vale (VALE) and you can read more about the 2015 dam collapse here. This event was a major environmental disaster and I am not trying to downplay it by any means. BHP and VALE will have to pay to clean up the mess plus damages, but as is common in the extractive industries getting to the final number takes a long time and estimates along the way will change.

Right now, we are almost 10 years from the original event and the matter is still not resolved. While BHP cited new progress in the judicial process as the "trigger" to increase the accounting provision, the final outcome is still uncertain and could go either way:

BHP

In any case, while I don't know anything about the legal system in Brazil and how this will play out, the fact remains this is one-time charge of about 25% the half-year EBITDA, not a recurring cash outflow as the news reporting basically implied.

From an economics perspective, assuming the market was surprised by the announcement, BHP's market cap should have dropped by 2% or so to reflect the $3.2 billion.

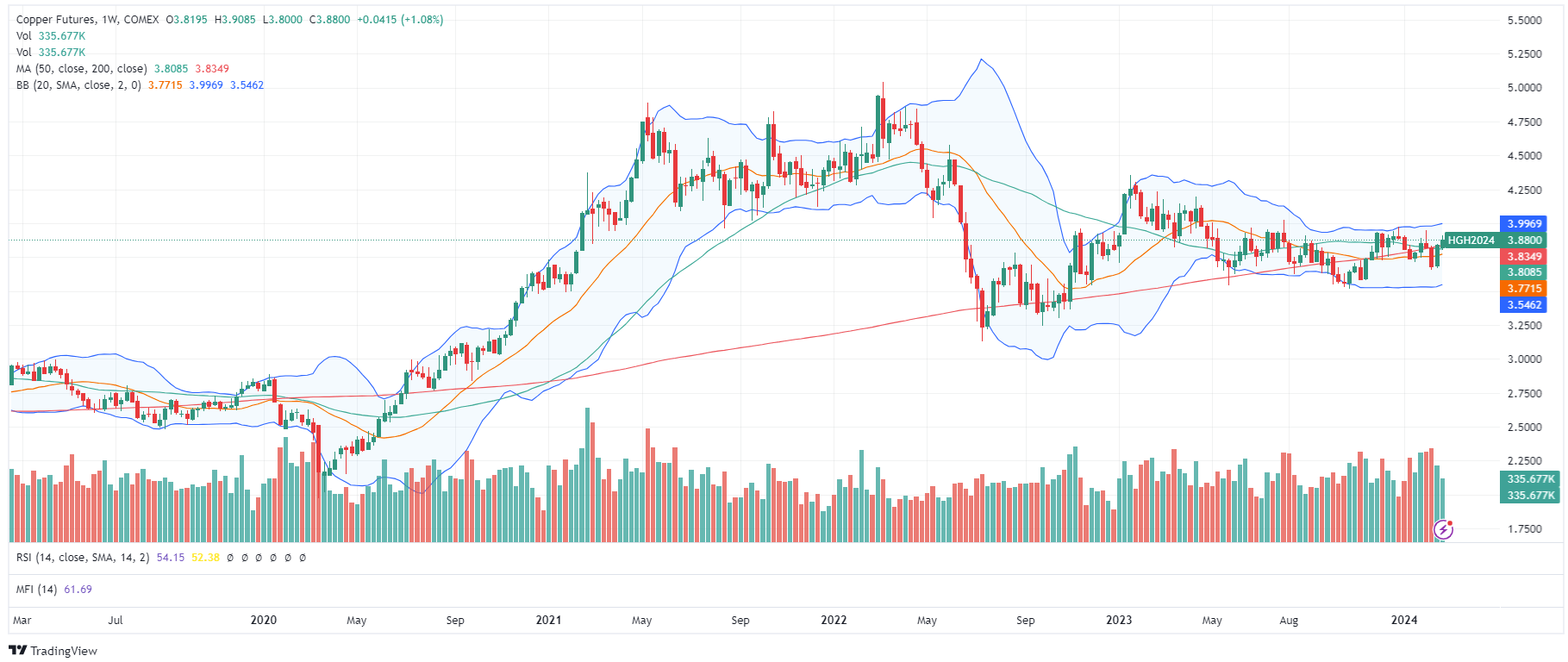

The commodities that make a big difference for BHP are copper, iron ore and metallurgical coal. All three seem to be doing fine despite the monetary headwinds over the last couple years.

Copper seems to be consolidating after coming off the 2022 highs:

TradingView

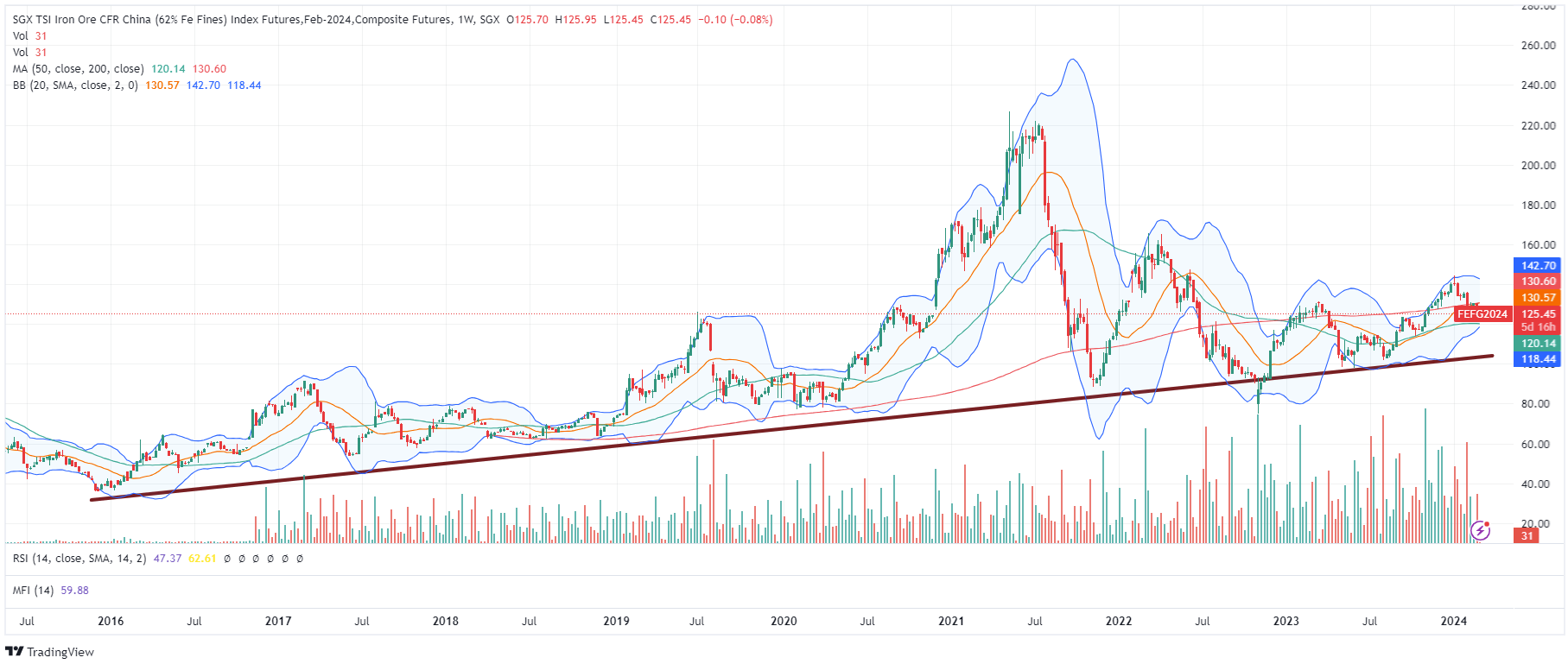

Iron ore saw a big correction when monetary tightening and the China (FXI) troubles started but on a longer time frame remains above the upward trend from the 2016 lows:

TradingView

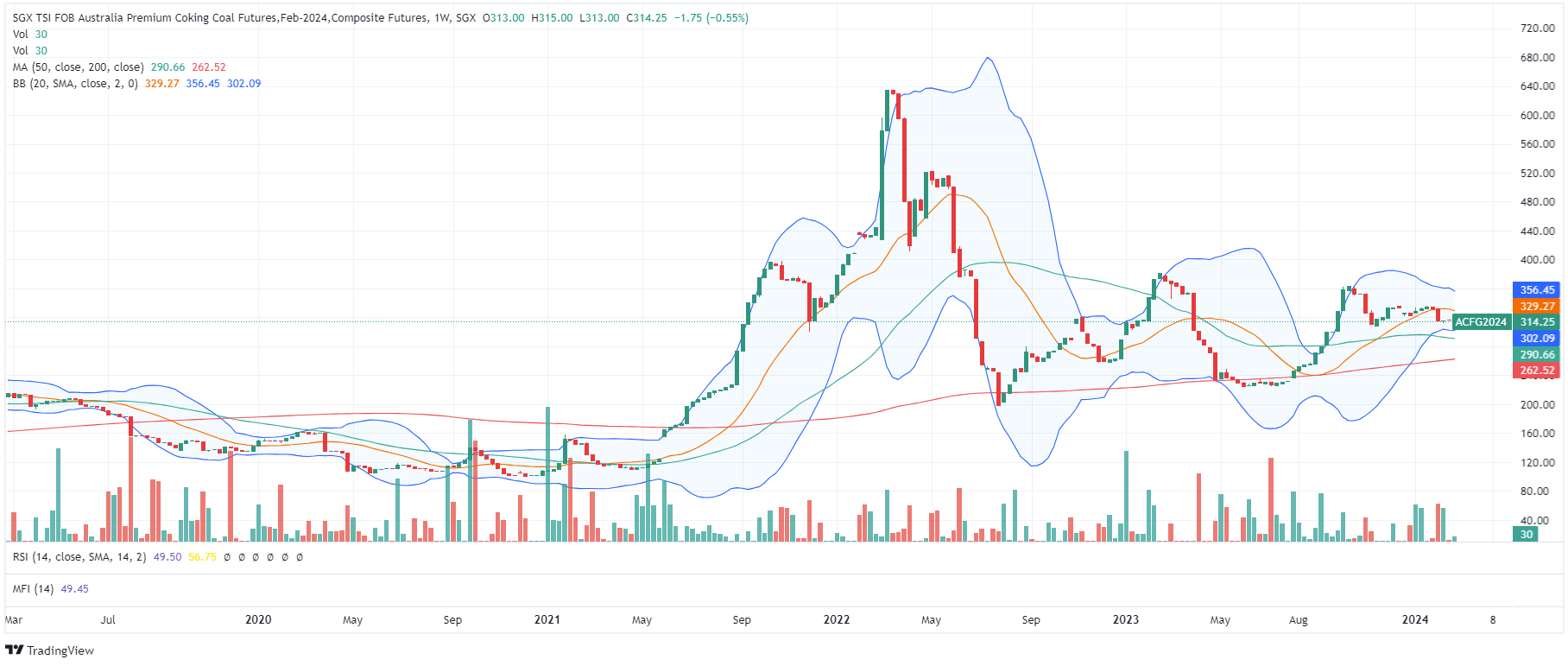

Metallurgical coal also doesn't seem to want to come back to its pre-pandemic levels:

TradingView

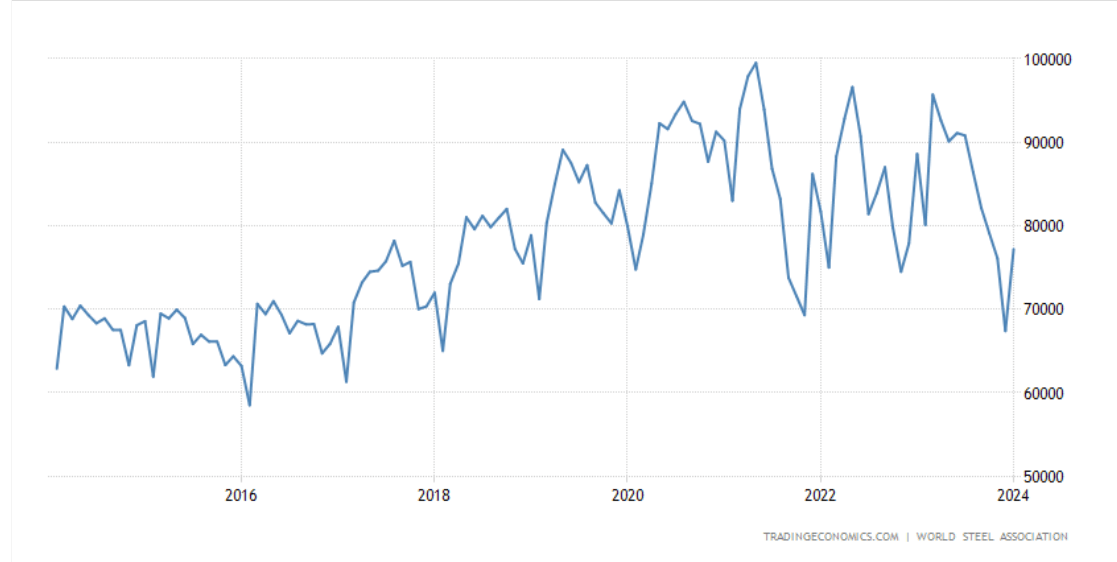

While I have argued that the copper strength may transcend the cyclical factors, iron ore and met coal are perhaps more vulnerable. Yet China's steel production may be bouncing off the recent lows too:

Trading Economics

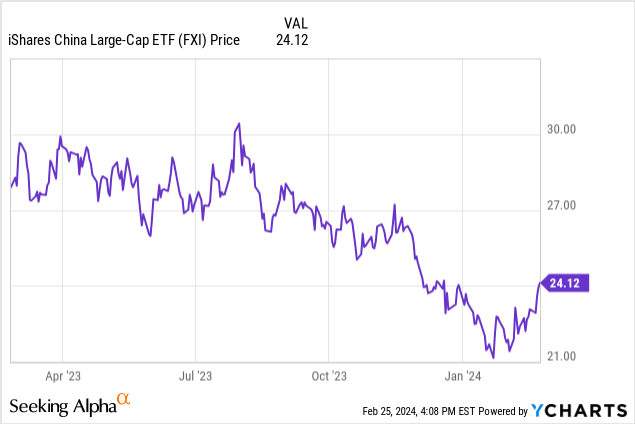

As China is a major importer of BHP's production, it is also encouraging to see Chinese equities may have finally found a bottom:

BHP's commodity outlook seems to agree with the market as it sees copper tightness in 2024 while the iron ore market should be balanced. The future of met coal is perhaps less certain but BHP also notes the prices remain relatively high in historical comparison.

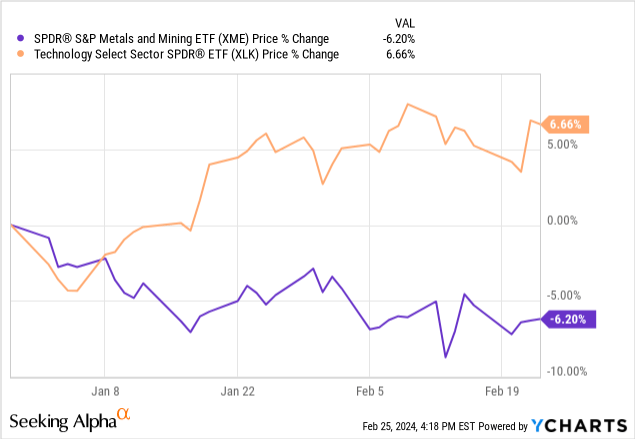

Unfortunately for mining investors (XME), the sector has been negatively correlated to technology (XLK) so far this year:

To some extent this makes sense as technology is a disinflation play while mining is an inflation hedge, but I think the algorithmic trading may be taking this correlation a bit out of proportion. Nvidia (NVDA) making new highs every day seems to be interpreted as bearish for the mining sector and I don't think that will continue for very long.

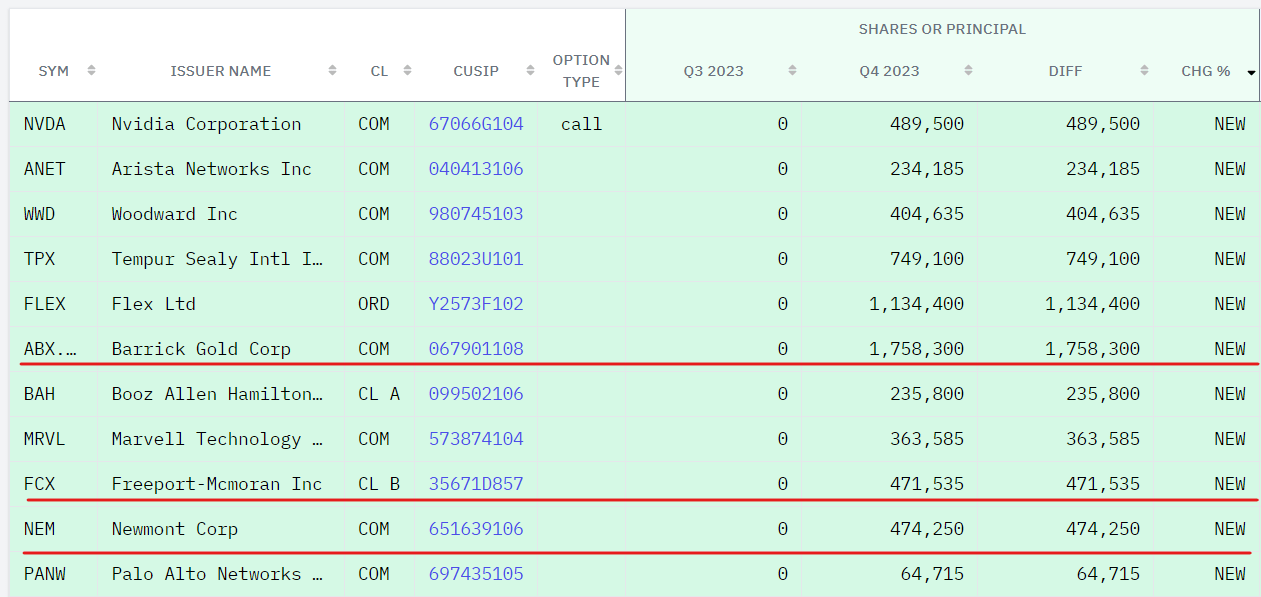

Smart money also appears to have been adding mining stocks. For example, Stanley Druckenmiller's Duquesne seems to have added Barrick Gold (GOLD), Freeport-McMoRan (FCX) and Newmont (NEM):

13f.info

I am not saying Mr. Druckenmiller is bearish on tech as he clearly bought Nvidia too, but I think it could be a sign the bigger players are taking notice of the mining sector's undervaluation.

BHP's half-year earnings were not publicized with the appropriate context, I think, at least on this platform. While the headline could be a "shocker", excluding impairments and one-off charges, the underlying economic profit of the business was on par with the very strong 2022 comparable period.

Recent negative sentiment to XME has probably contributed to BHP's correction:

TradingView

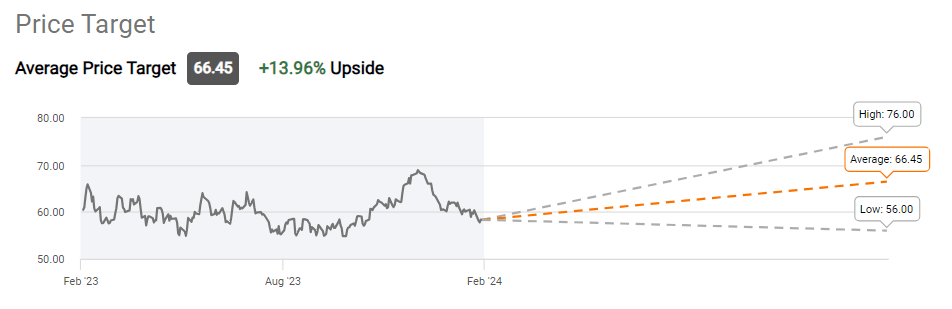

The stock is now again close to the $54-$56 support zone where I recommended it as "buy" in October.

Wall Street's targets imply a decent upside despite (in my view) analysts using rather bearish commodity price decks:

Seeking Alpha

I maintain my "buy" opinion with the caveat that technically the correction could extend a bit further.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.