yasindmrblk

yasindmrblk

The multifamily segment of Commercial Real Estate - apartments - is holding up better than office, retail (the Brick-and-Mortar Meltdown since 2017), and lodging, though it's cracking too with some spectacular defaults over the past 12 months or so. Yet, US banks and thrifts and foreign banks hold only a small-ish portion.

Total mortgages backed by multifamily properties rose by 4.4% year-over-year in Q4, or by $88 billion, to $2.09 trillion, according to the Mortgage Bankers Association, based on its own data, and on data from the Federal Reserve, Trepp, and the FDIC.

Of those mortgages:

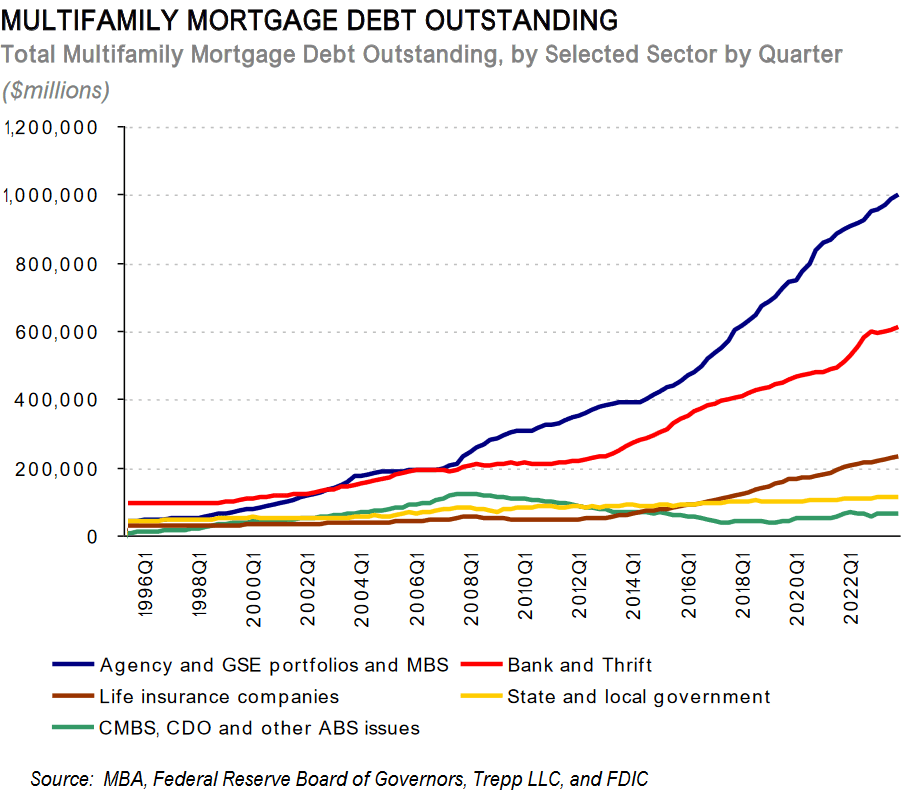

The blue line represents federal government-backed entities - including MBS issued and guaranteed by those entities. Quite an interesting trend (chart via MBA)

The MBA excludes loans for acquisition, development and construction, and loans collateralized by owner-occupied commercial properties.

For about a year, we've been reporting on how non-bank entities, from CMBS holders to PE firms, were on the hook for office and other CRE mortgages, how the biggest losses have hit these investors, particularly the CMBS investors, and not banks. And among the banks that it did hit, there were a slew of foreign banks.

But with the multifamily segment of CRE, it's mostly federal, state, and local government entities, including their pension funds that are on the hook - meaning the taxpayers are on the hook for 54.8% of all multifamily mortgages.

Most of the mortgages that taxpayers are on the hook for are held by the GSEs (such as Fannie Mae) that securitized the mortgages and sold these "agency CMBS" to investors. The Fed bought about $10 billion of them in the spring of 2020 and still holds about $8 billion of them. If landlords default on the underlying mortgages, it is the taxpayers that carry the credit risk, not the holder of the agency CMBS.

The Fed is worried about the banks, not a few individual banks, but about contagion across the banking system triggering a banking panic. But with the 4,026 US banks with $23 trillion in total assets holding only $612 billion in multifamily mortgages - well, that's less than 3% of their total assets. In other words, the banking system overall isn't fundamentally threatened by bad multifamily loan.

Even if many of the banks' $612 billion in multifamily loans default, they're secured by multifamily buildings with some value, so the losses are going to be only fraction of the $612 billion, spread over 4,026 banks with $23 trillion in total assets.

As always, some smaller banks with concentrated exposure in some markets may eventually topple under defaulted multifamily loans. Fitch thinks 49 tiny banks are heavily exposed to troubled multifamily loans, and some of those banks may topple. In nearly every year, some banks toppled, and it's just part of the risks in the banking system, and it's the FDIC's job to mop up those local messes at investors' expense.

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.