iQoncept

iQoncept

In my previous article, I suggested investors buy the dip in the Communication Services Select Sector SPDR® Fund ETF (NYSEARCA:XLC) price. Its share price rally of 46% in the last twelve months and 20% in the last six months vindicated my opinion. Despite significant gains, I believe XLC is a solid ETF to capitalize on the potential bull run in the rest of 2024. My optimism about XLC and the communication services sector is mainly due to its robust earnings growth outlook. Moreover, market fundamentals also point to the extension of the S&P 500’s bull run.

S&P 500 performance (Seeking Alpha)

The US stock market performed exceptionally so far in 2024, notching a new high of 5150 points. Analysts are now forecasting the S&P 500 to end the year around 5400 points. The prospects for the upside are high given the robust price momentum and improving market fundamentals.

The Fed is on track to achieve soft landing because it has so far attained its objective of slowing inflation without significantly hitting the economy. Therefore, it is highly expected that the Fed will initiate rate cuts from June, with an expectation of two to three cuts in 2024. Rate cuts are likely to add to the bull run because it will increase market activity that remained muted in the past year due to credit market deterioration. On the other hand, the US economic growth has been modest given a 2.4% GDP growth outlook for the full 2024.

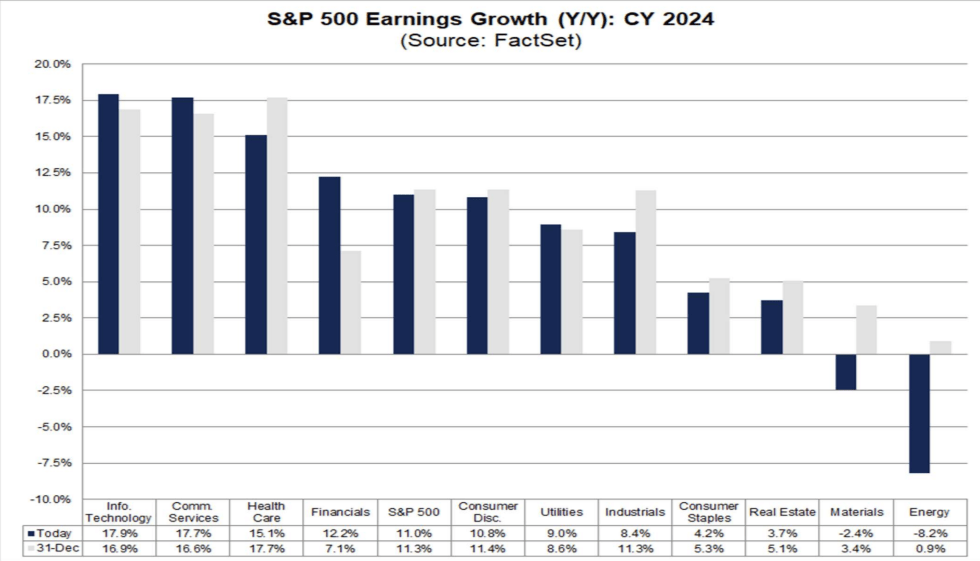

2024 earnings outlook (FactSet)

Furthermore, the whopping S&P 500’s earnings growth expectation of 11% compared to 0.9% increase in the past year is likely to be the biggest catalyst for the extension of the bull run. I also believe that the performance of mega and large-cap growth stocks from the information technology, communication and consumer cyclical sectors, which were the key performers in the past year, will be crucial for the extension of the bull run. From the earnings perspective, these sectors are likely to sustain their uptrend. The information technology and communication services sectors are expected to experience nearly 18% earnings growth in 2024. Another factor that increases my confidence in more upside is the broadening of S&P 500 performance. The sectors like healthcare and financial, which were among the laggards in 2023, are expected to generate double-digit earnings growth in 2024. Consequently, the impact of earnings growth has also begun reflecting in their share price performance. According to Morgan Stanley, the breadth of the S&P 500 improved to 70% from 55% a month ago, thanks to the robust share price performance from the industrials, energy, materials, real estate and utilities sectors.

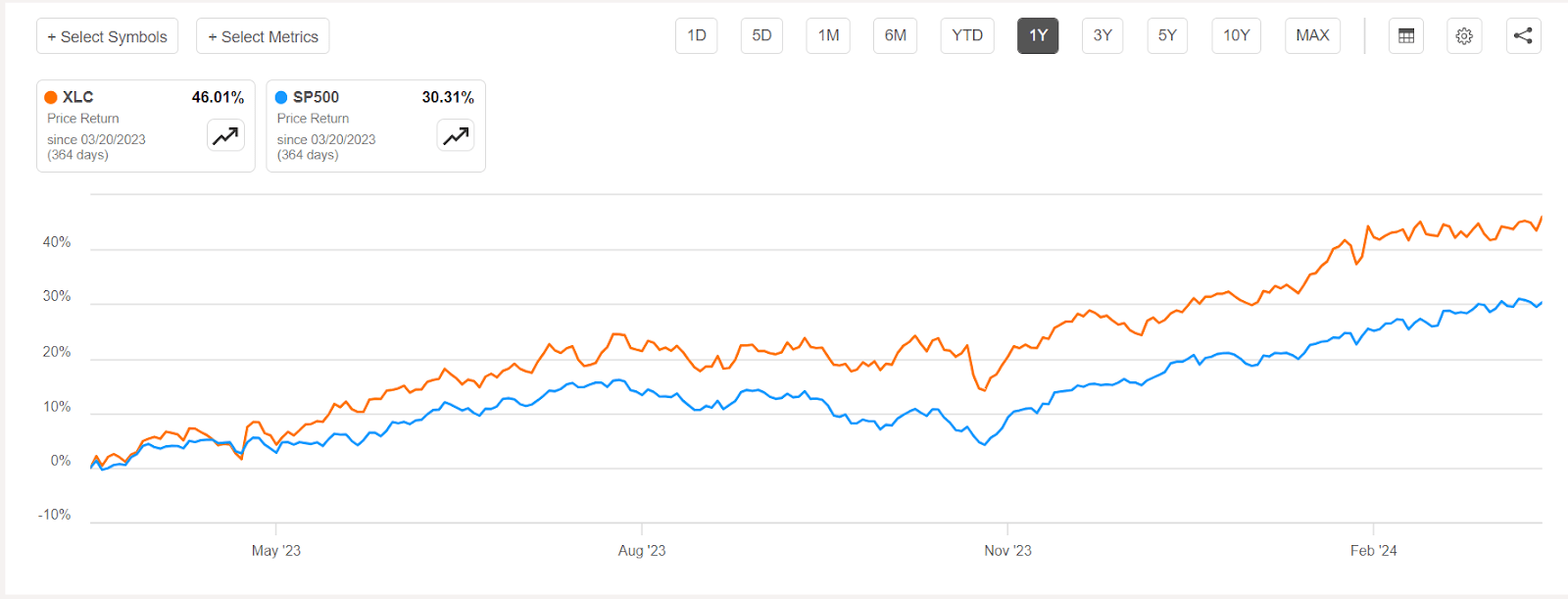

XLC Vs S&P 500 price performance (Seeking Alpha)

Despite significant gains in the past year, it appears that XLC is likely to extend the uptrend because of favorable market conditions and robust financial growth prospects of its portfolio holdings. The large number of communication services companies are poised to generate strong earnings growth. In addition, a meaningful increase in key growth metrics, such as end user and revenue growth, is also expected.

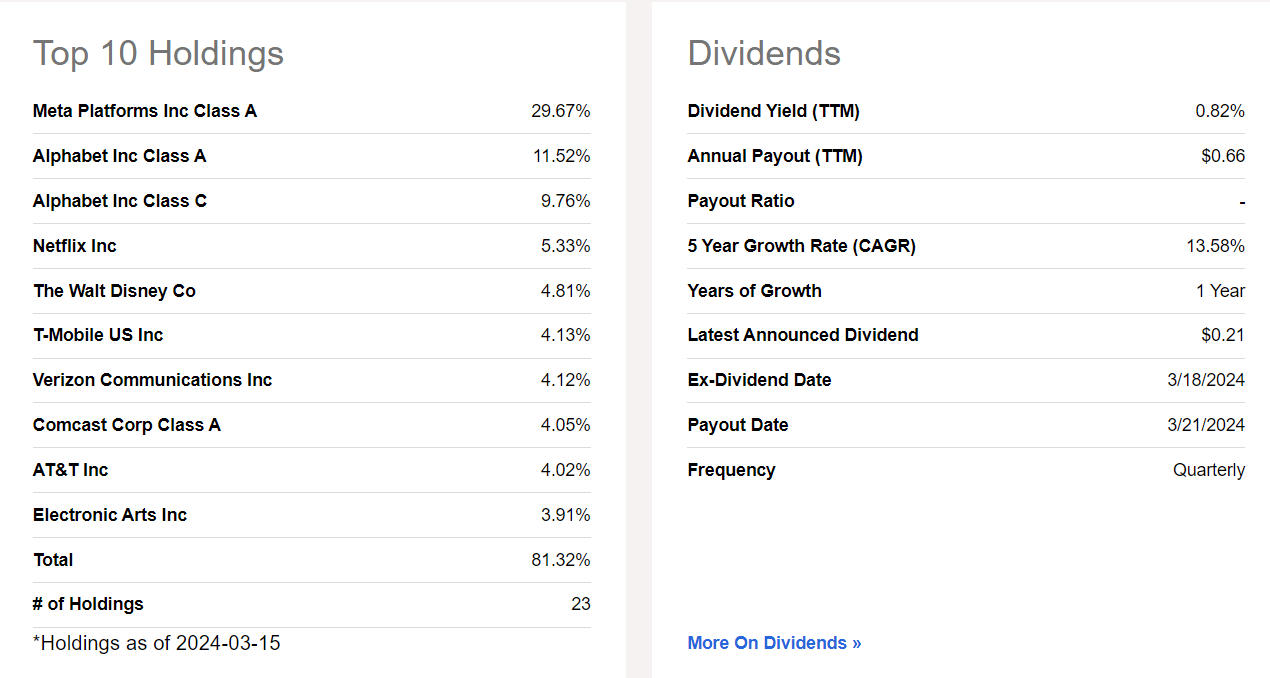

XLC top 10 holdings (Seeking Alpha)

All of the XLC’s top 10 holdings, accounting for 81% of the portfolio, are expected to generate staggering earnings growth in 2024. For instance, Wall Street expects nearly $20 per share in earnings for Meta Platforms (META) in 2024, up 34% from the past year. Its revenue is also expected to increase by 17% for the full year, thanks to growing active users, ad impressions and price per ad. Other catalysts for the stock price upside include its strategy of returning significant cash to investors in the form of dividends and share buybacks. In the fourth quarter of 2023, the company announced its first ever quarterly dividend of $0.50 per share. The company also plans to buy nearly $80 billion worth of its outstanding shares. Last year, it bought $20 billion of its common stock. Share buybacks not only help in returning the cash to shareholders, it also suggest that the company believes its shares are undervalued with significant upside ahead. Share buybacks also improves earnings per share and dividend per share.

XLC’s second largest holding is Alphabet (GOOG) (GOOGL), which is among the biggest beneficiaries of artificial intelligence and improving online advertisement demand. In the December quarter, its revenue soared 13%, operating income jumped 30% and net income rose 52% year over year. Wall Street expects 11% revenue and 17% earnings growth for Alphabet in 2024. Alphabet earned a strong buy rating based on Seeking Alpha quant system with a quant score of 4.97.

Netflix (NFLX) has also been generating staggering gains for shareholders. Its shares are up more than 100% in the last twelve months, thanks to robust user and earnings growth. In the fourth quarter of 2024, its global streaming paid memberships increased by 12.8% year-over-year to 260.28 million, the largest increase since the pandemic. Its revenue also grew at a double-digit rate, increasing 12.5% to $8.83 billion. The company expects 13% to 16% revenue growth in 2024. Meanwhile, the company’s earnings are likely to increase more than 40% year over year due to higher global average revenue per member and focus on operational efficiencies. XLC’s other top holdings, including The Walt Disney (DIS), T-Mobile (TMUS), and Electronic Arts (EA), are also poised to generate high double-digit earnings growth in 2024.

Unlike the fast-growing technology sector with significantly higher valuations than the S&P 500, the communication services sector is trading well below the broader market index. XLC is trading around only 17x forward earnings compared to the S&P 500’s 20x and the tech sector’s 28x. However, there is still a valuation risk for the sector because its largest holdings such as Meta, Alphabet, Netflix and The Walt Disney are trading at higher valuations than the sector median and the S&P 500. For instance, Meta is trading around 24x forward earnings while Alphabet, Netflix and The Walt Disney around 21x, 36x and 28x forward earnings, respectively. High valuation of fast-growing companies from the communication services sector is not surprising because growth stocks historically traded above the S&P 500 average valuations. At present, the growth category is trading around 27x forward earnings.

Nevertheless, high valuations don’t mean stocks are likely to experience a price correction or form a bear run. I believe stocks generally fall significantly when high valuation is accompanied by factors such as economic downturn, financial crises, tail event or substantial earnings decline. At present and in the near future, there is no risk of recession or financial crisis. In addition, earnings growth, which has always been considered a key share price driver, look robust. Moreover, we cannot compare the current tech-driven bull run with the dot.com bubble. At that time, shares rallied and valuations stretched only due to expectations and speculations about future profits. Meanwhile, the current bull run is fully backed by fundamental factors and actual numbers.

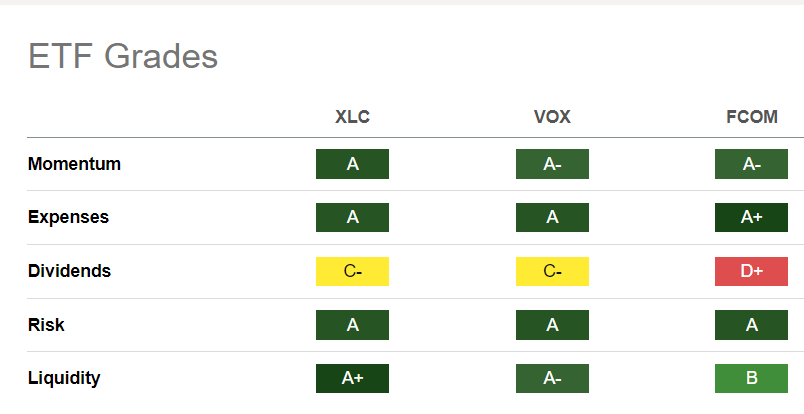

Quant Grades (Seeking Alpha)

XLC appears to be a solid ETF among its peer group based on several factors such as robust share price momentum, higher liquidity and low expense ratio. Its share price rallied nearly 46% in the last twelve months compared to a 39% price increase of Vanguard Communication Services Index Fund ETF Shares (VOX) and Fidelity MSCI Communication Services Index ETF (FCOM). In addition to a low expense ratio of 0.09%, the ETF looks like a better choice than the peers due to its high liquidity. It has $17.7 billion in assets under management and 6.14 million in average share trading volume. VOX and FCOM have $4 billion and $1 billion in assets under management along with a significantly lower trading volume than XLC. Based on a Seeking Alpha quant score of 4.13, XLC is ranked first out of 13 ETFs in its sub-asset class.

Historical trends show that a bull run can last many years and stock prices can increase significantly. The current bull run that began in early 2023 also appears long-lasting given the solid macroeconomic outlook and robust earnings growth trend. With a share price increase of 46% in the last twelve months compared to the S&P 500 gain of 30%, XLC appears like a solid ETF to fully benefit from the bull run. Its top stock holdings are poised to experience high double-digit revenue and earnings growth. Moreover, XLC’s attractive valuations along with strong share price momentum and solid liquidity could contribute to its upside.