frantic00/iStock via Getty Images

frantic00/iStock via Getty Images

This is the first rattle out of the box for coverage of the SPDR® S&P Oil & Gas Equipment & Services ETF (NYSEARCA:XES). If you catch them right, exchange-traded funds, or ETFs, can be a good way to ride a sector move higher without single company risk. Many of the holdings of the XES have been featured in our Investing Group articles recently with...

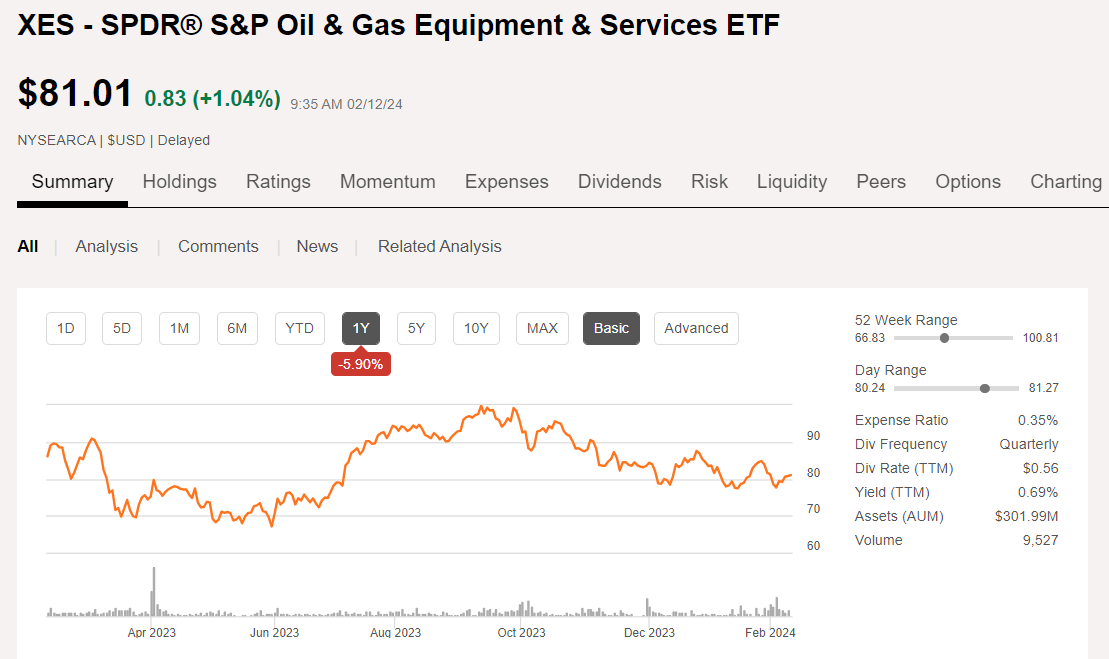

XES ETF price chart (Seeking Alpha)

favorable ratings. Noteworthy among these might be our article Monday on Halliburton Company (HAL). This makes a review of this particular ETF particularly important, as these companies continue largely to languish in the current bearish environment for OFS companies, thanks to anemic oil and gas prices. But they could be poised for a rally in the next few months.

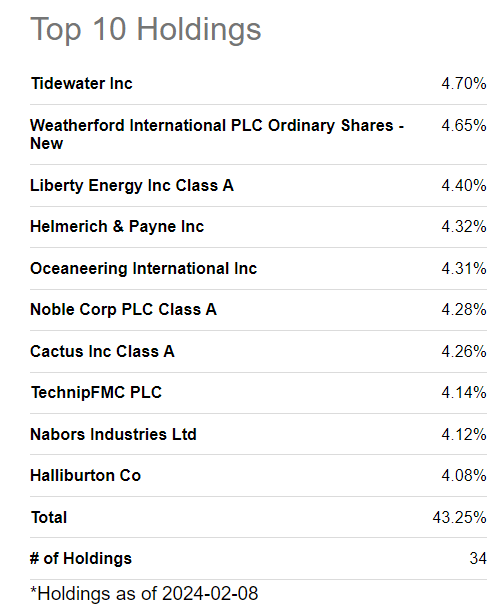

XES Top Ten holdings (Seeking Alpha.)

Part of the troubles that the XES ETF has had is a big chunk of its portfolio is North American-centric. Halliburton, Liberty Energy (LBRT), Helmerich & Payne (HP), Nabors (NBR), and Cactus Drilling (WHD) are largely dependent on North America. Many of these companies are down more than the 20% slide seen in the XES, and it has the holdings targeted more to the offshore recovery to thank for that outcome. Oceaneering (OII), TechnipFMC Plc (FTI), Noble Corp (NE), Tidewater (TDW) and to an extent HAL are positioned for a recovery in offshore drilling. There is also a sprinkling of larger cap companies in addition to HAL, like Schlumberger (SLB) and Baker Hughes (BKR). These provide some exposure to international markets and dividends.

The one-year price return of the XES is below water, no great surprise given the state of the industry. All of the North American-focused companies are under pressure from a declining rig count, and the offshore recovery is nascent. As an example, Noble (a company we covered recently) is off 15% from September highs in the middle 50s, despite turning in a pretty good report for Q3 2023.

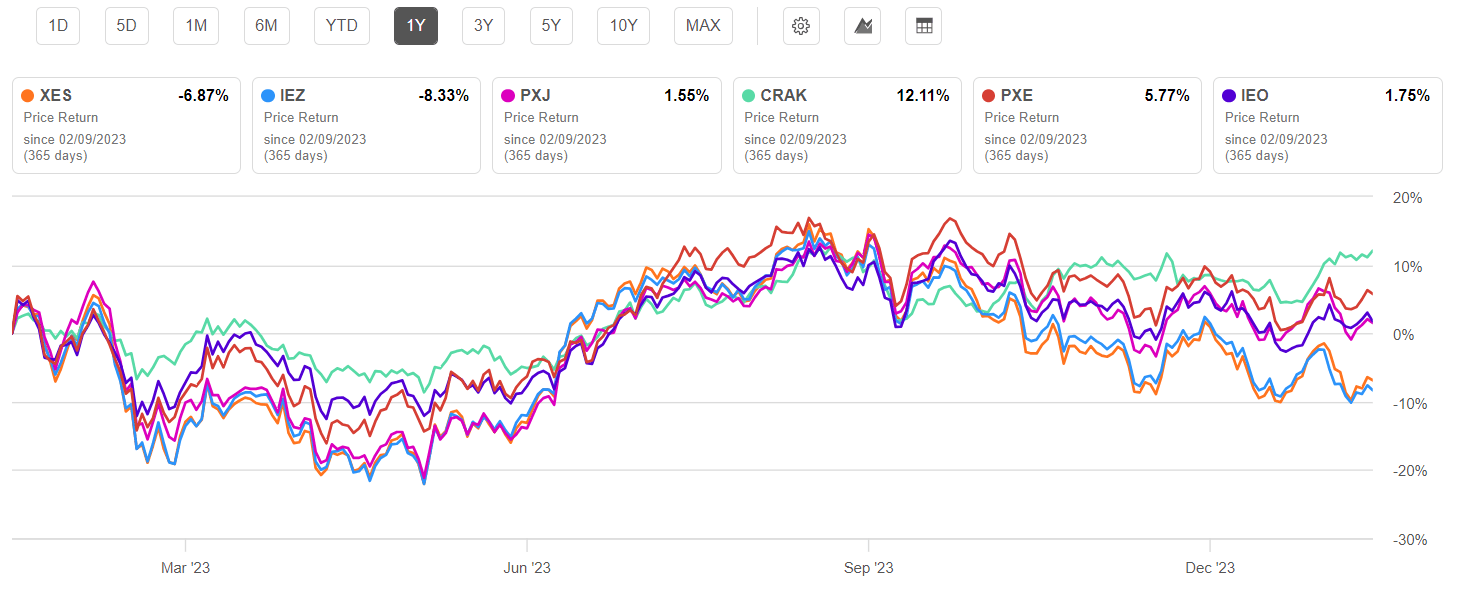

Nor does the fund compare well with other midcap funds in the energy sector, none of which have lit up the market with success, but the XES has dragged the bottom of the barrel.

Sector ETF comparison chart (Seeking Alpha)

From the fund's fact sheet, the originator - State Street - provides the following information on the XES.

The SPDR S&P Oil & Gas Equipment & Services ETF seeks to provide investment results that, before fees and expenses, correspond generally to the total return performance of the S&P Oil & Gas Equipment & Services Select Industry Index (the "Index") Seeks to provide exposure to the oil and gas equipment and services segment of the S&P TMI, which comprises the Oil & Gas Drilling sub-industry and the Oil & Gas Equipment & Services sub-industry Seeks to track a modified equal weighted index which provides the potential for unconcentrated industry exposure across large, mid and small cap stocks Allows investors to take strategic or tactical positions at a more targeted level than traditional sector based investing.

The XES carries a 0.35 expense ratio, which is in the middle of energy sector ETFs. Ten stocks comprise about half its equity stake, with another 23 comprising the balance at lesser percentages. See the ETF's Q3 2023 Holdings.

Something I like about the fund is its exposure to fracking companies - Liberty Energy (LBRT), ProFrac Holding (ACDC), and ProPetro (PUMP). When you add Hally into the mix, you've got an option on ~80% of the North American fracking sector, which has bottomed recently and is now beginning what could become a ramp higher in the months to come, as the recent Primary Vision release points out.

As the prospectus notes, the XES is a good vehicle for tactical investors looking to capitalize on a move in the energy sector. I think there is one coming and have discussed this previously.

Drilling activity has been on the decline since the end of 2022, as companies have shifted capital allocations to maintaining production at current levels, paying down debt, and funneling cash to shareholders. Since peaking post-Covid at ~780 rigs in late 2022, by the middle of 2023, the U.S. rig count had declined to ~621, where it essentially remains today. Rigs drilling for gas have dropped at a proportionately higher rate than rigs targeting oil.

As previously noted, thus far the decline in shale activity hasn't adversely impacted production, but obviously this can't go on forever if output is to be maintained. This is a point Vicki Hollub, CEO of Occidental Petroleum (OXY), noted in recent sideline remarks at Davos. Hollub was quoted as saying:

"In the near term, the markets are not balanced; supply, demand is not balanced," adding that: "2025 and beyond is when the world is going to be short of oil."

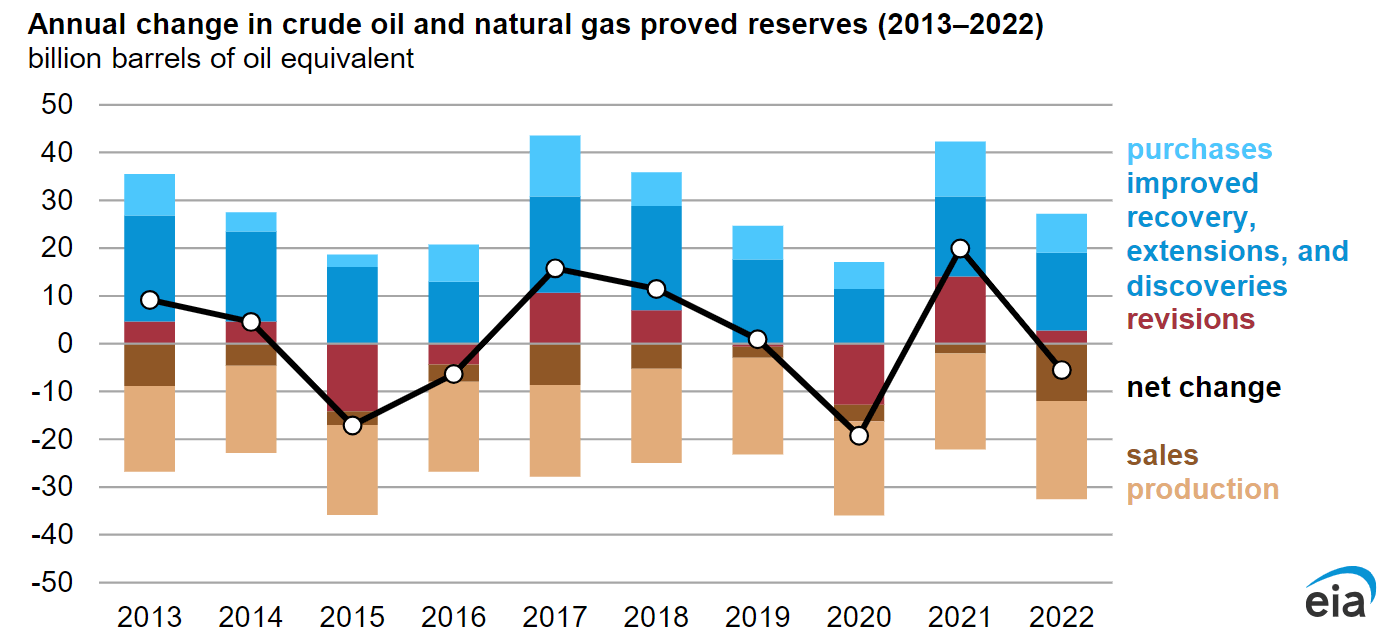

The EIA graphic below puts Hollub's comments into context. The data isn't in for 2023 yet, but there is little doubt that when the EIA updates this graphic, proved reserves will take another year-over-year dip. With the declines in activity over the last couple of years, conceptually this could be a big dip. One that could shock the market out of its current complacency regarding crude supplies.

EIA chart on proved reserves (EIA)

Over the past few years, I have made frequent observations, suggesting that years of under-investment would lead to shortages in the future. If Hollub is correct, the future of tighter oil and gas supplies could be just around the corner.

If we do get a measurable decline in shale production, these companies, which have been beaten down by low oil and gas prices, will rally. This should provide uplift for the XES.

The key risk to this thesis would be further weakness in WTI and Brent. Recently these commodities have firmed up in the middle $70's and low $80's respectively. Any reversion toward January pricing would weaken the underlying stocks and splash over onto the XES.

SPDR® S&P Oil & Gas Equipment & Services ETF has rallied a bit higher in recent days, and is up today in the market open. There no particular news driving this move, so I doubt it has staying power. While I think the fund is attractive at this level, as there is no significant dividend associated with it, price improvement is our only lever for profits.

Accordingly, in spite of the nearly 20% decline in the XES, I would rate the fund as a hold. A move back into the sub $80's might trigger a buy, though. As with all things, patience and timing are essential components of making money in equities. Put the XES on your watch list for a downdraft if this sort of investment interests you.