Tramino/iStock Unreleased via Getty Images

Tramino/iStock Unreleased via Getty Images

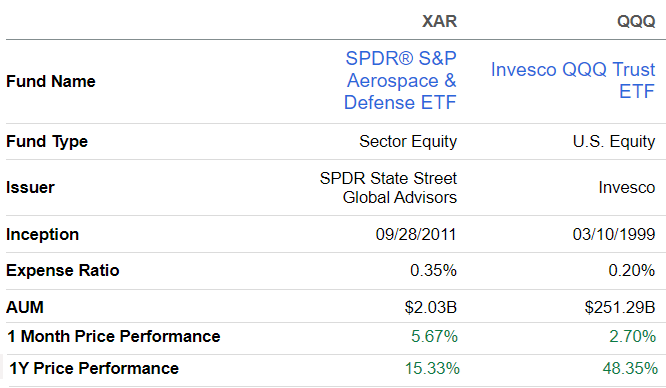

In a world of increasing geopolitical tensions and wars, investing in companies that produce weapons and related systems sounds like a good idea. For this purpose, the SPDR S&P Aerospace & Defense ETF (NYSEARCA:XAR) has outperformed the AI-driven Invesco QQQ Trust ETF (QQQ) in the last month, as shown in the comparison table below. Most of the upside occurred in the last week of January 23 and coincided with an intensification of hostilities in the Red Sea when American and British military forces started to defend maritime traffic against attacks by Houthi rebels.

Comparison of main metrics (seekingalpha.com)

However, XAR's underperformance of QQQ in the longer term (last year) shows that the upside enjoyed by the U.S. defense ETF may not be sustained. The reason is there are other factors to consider with two of them being non-U.S. contractors obtaining more contracts in a rapidly evolving European defense industry, as the Ukraine-Russia war lingers on while facing the prospect of foreign policy becoming much less accommodative towards allies who do not contribute enough. From this perspective, and also because of the emergence of geographically diversified and alternative ETFs, the objective of this thesis is to show that XAR is not a Buy.

Talking about foreign policy, former President Donald Trump remarked during a rally in South Carolina that if elected during the forthcoming elections, he will not provide aid in the event of an attack on a NATO (North Atlantic Treaty Organization) country that does not invest at least 2% of its GDP in military spending. This did have a profound effect on the European Union according to an article from the Wall Street Journal, and given that Donald Trump had already highlighted the issue of European countries not spending enough for their security when he was President, his words are being taken seriously.

Pursuing further, according to the European Defense Agency European countries collectively spent around 240 billion euros per year on military spending in 2022, or a 6% YoY increase, but remain largely dependent on the United States in many respects. Only five EU countries exceeded the 2% threshold and these are Greece, Poland, Estonia, Latvia, and Lithuania which means that many large countries like Germany and Italy do not contribute enough.

Thus, there is military dependence on the United States for everything from transport, satellite imagery, battlefield command and control, and tactical intelligence without forgetting the nuclear deterrence Europe benefits as an ally.

As a response to Trump, the European Commission President, acknowledging that Europe was facing a tougher world mentioned that the union has to increase spending, but also added that "Europe must spend more, spend better, spend European”.

This means that the way they spend will not necessarily benefit the U.S. defense industry in the same way as before given the dynamics around Made-in-Europe. For this matter, Europe counts among its ranks as the largest aerospace and defense exporters in the world with France, Germany, Italy, and the United Kingdom positioned in the top 10 in 2022. Thus, for air combat helicopters, in addition to soliciting bids from Lockheed Martin (LMT) for its 2025 New Medium Helicopter program, the U.K. is also considering European manufacturers like Italian Leonardo and Airbus Hélicoptère. Looking further, for land-based operations, in addition to General Dynamics (GD) Abrams, German Leopard 2 and British Challenger 2 have seen action in the Ukrainian battlefield with a possibility of the French Leclerc also joining them.

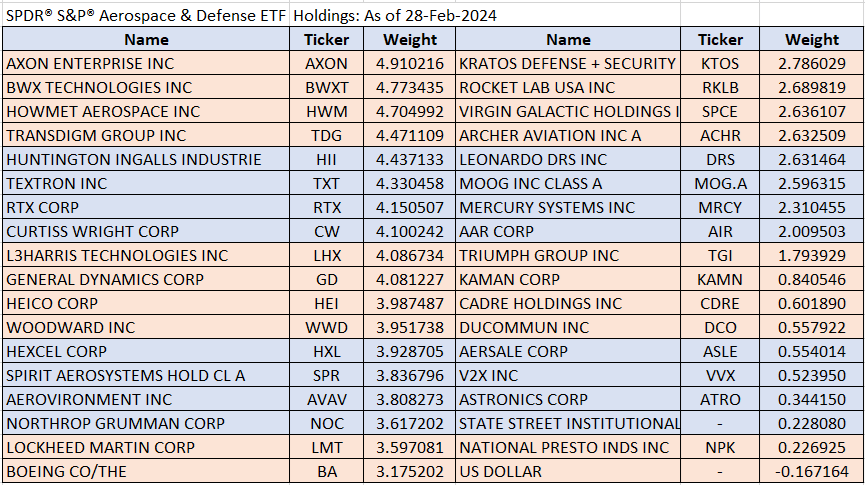

Furthermore, Italy-based Leonardo S.p.A. whose U.S. subsidiary Leonardo DRS (DRS) forms part of XAR's holdings as tabled below has called for further consolidation in the European defense sector. Thinking aloud, it could evolve in the same way that American companies went through a profound restructuring in the 1990s after the fall of the USSR giving rise to industrial giants with colossal resources like Northrop Grumman (NOC), RTX Corp (RTX), and Lockheed Martin.

www.ssga.com

For this purpose, fourteen M&A deals valued at around $2 billion were announced in the European aerospace & defense industry just in the fourth quarter of last year. This comes on the back of NATO's European allies set to invest $380 billion for defense purposes, or 2% of their combined GDP for the first time according to a statement from the organization's secretary general on 5 February.

Consequently, there is a shift in military budgets which were initially tuned to the relatively peaceful post-Cold War era to be more relevant to this new conflict-prone world.

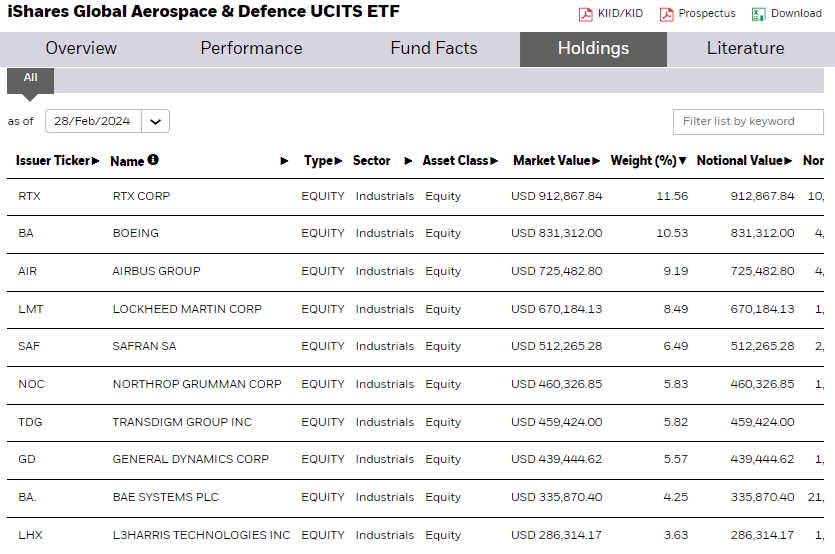

Now, to satisfy investor demand for related assets, at least three ETF issuers including one by BlackRock (BLK) have launched aerospace and defense sector-focused investment vehicles. Looking at one of them is the iShares Global Aerospace & Defence UCITS ETF listed on Euronext Amsterdam whose main holdings are listed below.

www.ishares.com

As shown above, in addition to U.S. stocks, its other main holdings come from developed markets like France and the U.K. since it tracks the S&P Developed BMI Select Aerospace & Defense 35/20 Capped Index. Also, the ticker symbols of European stocks suggest that they are not listed on the NYSE or the Nasdaq.

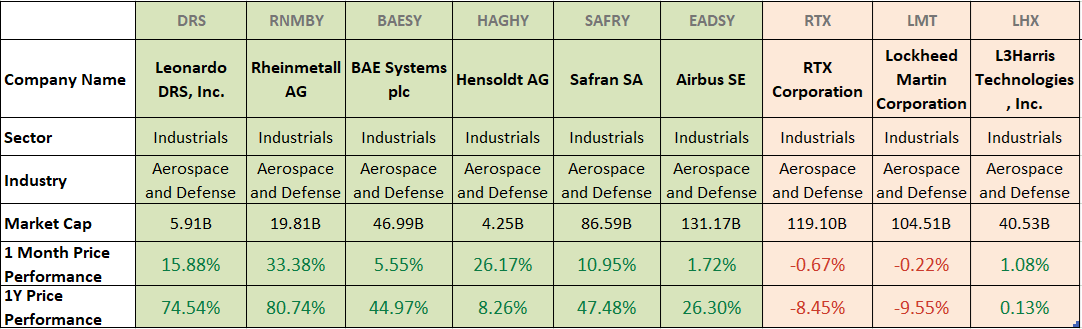

Looking at their U.S. public listings, these European companies to which I have added Hensoldt AG (OTCPK:HAGHY) from Germany have outperformed their American peers both in the short and longer terms as tabled below.

Comparison with peers (seekingalpha.com)

Noteworthily, as shown in XAR's list of holdings, these European companies are excluded given that it tracks the S&P Aerospace & Defense Select Industry Index which comprises U.S. equities. This means that XAR may continue to get some traction as has been the case during the last month when the escalation of the Middle East war to the Red Sea increases the probability of more sales opportunities. On the other hand, it may miss the higher degree of militarization underway in Europe where some countries have been substantially increasing spending and may likely have to continue.

For this purpose, on the one hand, NATO European members have to help Ukraine contain Russia while on the other they face the prospect of a dramatic shift in the level of tolerance towards those not spending sufficiently for security after the elections. This makes it imperative for Europeans to accelerate the move to become less dependent on the U.S., and, as they spend more money on military equipment, they will tend to favor domestic contractors given that the defense industry is closely associated with the industrial base of a country.

This complex pertains to the relationship between the military establishment and the defense companies that supply the weapons and the EU very recently announced that it wants to create one ready for war. Therefore, for those who want to invest, it is better to look for individual names that stand to benefit directly from the rising European military-industrial complex.

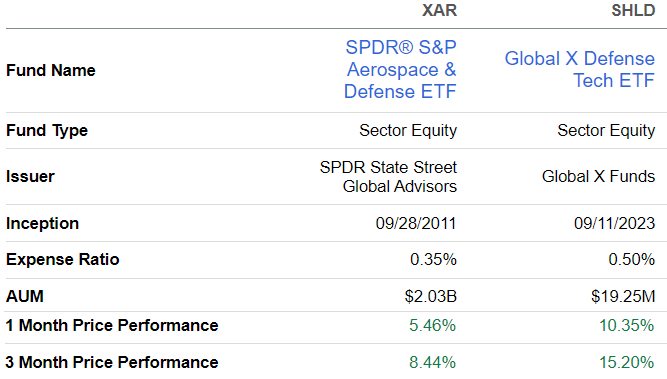

Alternatively, you can opt for another fund that is more geographically diversified like the Global X Defense Tech ETF (SHLD). As shown below, it has delivered better performance; but the problem is that it was incepted less than one year ago, and its asset under management are only $19.25 million which means that it is much less liquid compared to its SPDR peer.

Comparison of key metrics (seekingalpha.com)

This said, for those already holding XAR's shares, I am not bearish as it is unlikely for European countries to completely sideline U.S. contractors. For this matter, despite the presence of the Swedish Grippen from the Saab AB (OTCPK:SAABY), the Eurofighter from a consortium of German, British, Spanish, and Italian manufacturers, or the French Rafale from Dassault Aviation (OTCPK:DASTY), some countries like Germany or Finland have opted for Lockheed Martin's F-35 as it is already interoperable with NATO's operational tactics.

Another example is for protection against missiles where despite the SAMP/T Mamba Aster developed by France and Italy, Germany announced an anti-missile shield project including collaboration between several EU countries and Israel, while not forgetting the United States.

In consequence, I believe this thesis has shown that simply relying on increasing militarization to justify an investment in the U.S. defense sector through XAR is not appropriate, whether it is centered around the Russia-Ukraine war, the Israel-Hamas war, or because of geopolitics around Taiwan.

The reason is European defense which is at a crossroads, and Ernst and Young estimate that military expenditure in core NATO countries during the 2021 to 2025 period has to increase from 18% to 66%. Before the Ukrainian War, the increase was only 18% to 53% which means more weapon systems and logistics equipment to be purchased. In these circumstances, opportunities for U.S. defense plays are likely to be there, but not in the same pronounced way as previously because of competition from European domestic production.

In this respect, XAR's P/E already trades at a premium of 15.5% relative to its category average as per data from Morningstar which means that it does not constitute an opportunity. Moreover, with the wider availability of ETFs allowing for more targeted exposure to stocks likely to benefit from the rise of the European industrial-military complex, XAR's equal-weighted investment approach in U.S. defense may not be the right solution to profit from Europe's shift in military spending.

Finally, to be fair, whatever the outcome of the elections and even if U.S. foreign policy, especially toward its European allies, does not ultimately change, the debate around European military spending is likely to garner attention as the U.S. grapples with a sky-high budget deficit. In such a scenario and depending on investors' perception, things may become volatile for XAR, especially if a high-profile contract is awarded to a non-U.S. defense contractor.