Graphicscoco/E+ via Getty Images

Graphicscoco/E+ via Getty Images

Wave Life Sciences (NASDAQ:WVE), an RNA-focused, clinical-stage biotechnology company, is trending after reporting on Wednesday that it is entering the obesity field. Per their report:

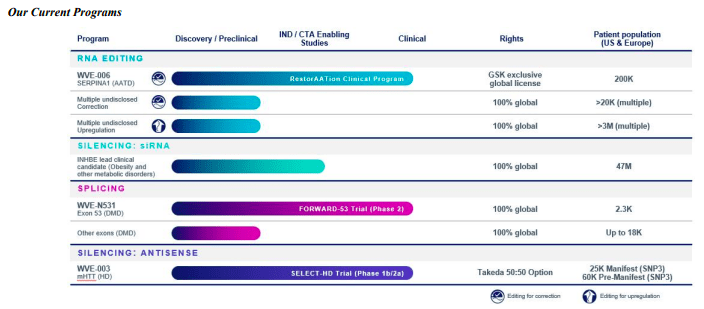

INHBE lead clinical candidate selected; potential best-in-class treatment for obesity with potent and durable silencing, weight loss with no loss of muscle mass, reduction of visceral fat, and every-six-month or annual subcutaneous dosing; clinical trial initiation expected 1Q 2025.

Their clinical candidate is based on years of research into the loss of function (LOF) of the INHBE gene. RNAi-based therapeutics company, Alnylam (ALNY), discussed the Nature Communications publication in 2022 and announced their intentions to pursue a clinical candidate themselves.

According to the publication, "(...) carriers of INHBE pLOF variants have a more favorable metabolic profile and estimated lower odds of CHD and T2D than non-carriers. Importantly, by reducing abdominal fat, drugs targeting INHBE would have a distinct biological mechanism to existing drugs for CHD and T2D and may complement current therapies."

Another RNA company, Arrowhead Pharmaceuticals (ARWR), has also discussed its intention to pursue INHBE loss of function.

So, there is a lot of competition within this class of medicine itself. Outside, of course, they will also fight with behemoths like Novo Nordisk (NVO) and Eli Lilly's (LLY) GLP-1 for share within the obesity field, among dozens of other companies vying for attention. Although INHBE-related therapeutics are theorized to compliment existing obesity drugs, reasonably, this is something that can, at the very least, carve its own niche in a massive market. But Wave seems a little behind in this regard and faces intense competition from companies like Alnylam that have successfully brought an RNA-based therapeutic to market.

Wave Life Sciences 10-K

Moving on to other pipeline updates: The company continues to make progress in their treatment, WVE-006, targeting alpha-1 antitrypsin deficiency (AATD). Wave is partnered with GSK plc (GSK) in this indication and is currently dosing healthy volunteers in a Phase 1 study. The goal here is to provide "proof-of-mechanism as measured by restoration of wild-type alpha-1 antitrypsin (M-AAT) protein in serum." Vertex (VRTX) recently dropped out of this race after their "AAT corrector" caused liver issues. Gene therapies, like Wave's, may offer more effective and safer treatments. Others developing gene therapies for AATD include Beam Therapeutics (BEAM), Intellia Therapeutics (NTLA), and Takeda (TAK). So, again, we have a crowded field of players and Wave is not the frontrunner here.

In Duchenne muscular dystrophy, Wave is testing WVE-N531 in the FORWARD-53 clinical trial. The company anticipates data ("dystrophin protein expression from muscle biopsies at 24 weeks") in the third quarter of this year. This figures to be a major event for Wave, but, again, there is very tough competition in DMD (e.g., Sarepta, NS Pharma, Pfizer, REGENXBIO), and it is a complicated disease.

Looking at Wave's balance sheet, cash and cash equivalents equal $200.4 million. Total assets outweigh total liabilities: $274.949 million/$227.445 million. The current ratio (current assets divided by current liabilities) totals 1.26. This is an adequate value and indicates the company's ability to pay its short-term obligations.

Over the last year, Wave used $19.4 million in operating activities, indicating a monthly cash burn rate of approximately $1.6 million. This burn rate, when analyzed against the liquid assets, suggests a cash runway of about 125 months. However, it's crucial to note that these figures are based on past performance. For example, Wave's own cash runway estimate, based on future assumptions, extends into the "fourth quarter of 2025."

Based on the information above, the odds of Wave requiring additional financing within the next twelve months could be considered medium.

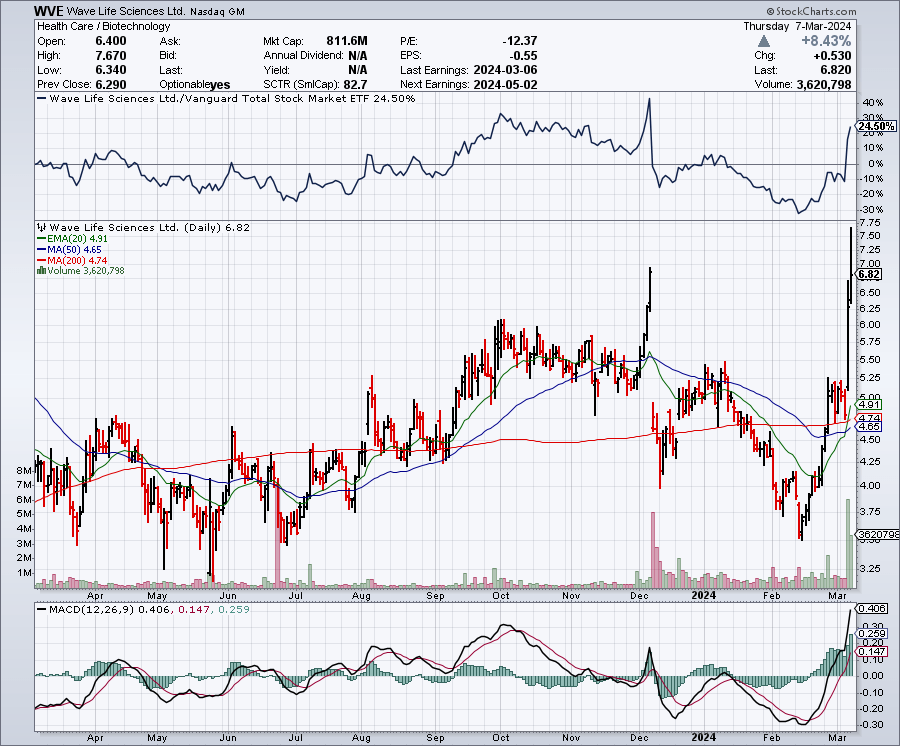

According to Seeking Alpha, Wave's market capitalization stands at $768 million, indicating a mid-small cap status. Compared to the SP500 (SPY), Wave's stock has underperformed in the short term (-8% over 3 months) but shown strength over a year (+49%).

StockCharts.com

Per Fintel, the short interest is 2,505,484 shares, equivalent to 3.75% of the float, indicating moderate bearish sentiment but not excessively high risk. Institutional ownership is significant at 76.59%, with new positions (8,623,072 shares) outpacing sold-out positions (166,975 shares), highlighted by major stakeholders such as RA Capital Management, Maverick Capital, and Adage Capital Partners showing increased confidence. Insider trades (which include major purchases from RA Capital) over the past 12 months reveal a net positive activity, with 4,262,938 more shares bought than sold, reinforcing a potentially positive internal sentiment.

Given these dynamics, the company's market sentiment can be qualified as "robust."

Seeking Alpha

Relative to peers like Intellia Therapeutics ($2.88 billion), Arrowhead Pharmaceuticals ($4.39 billion), and Beam Therapeutics ($3.01 billion), Wave sticks out with its lower market capitalization of $768 million. However, unlike Wave, Arrowhead and Intellia have drugs in pivotal-stage trials. So, this likely accounts for some of the difference in valuation between the firms. Looking at stock momentum, both Wave and Beam stick out with YTD returns of 35% each, while Intellia and Arrowhead underperform. Quant Factor Grades comparing "growth" and "profitability" are not quite relevant yet, as these companies primarily derive the little revenue they receive from collaborations.

In conclusion, there's nothing about Wave Life Sciences that stands out to me as promising. The venture into the obesity market doesn't set Wave apart, as this is an intense and crowded field. Moreover, even the rare disease markets like AATD and DMD are filled with able-bodied contenders as well. So, the pressure is really on Wave to differentiate their gene therapies from others. This is a formidable task.

Financially, Wave appears to be on solid ground. The cash runway is comfortable and revenues from collaborations help reduce the burden of R&D investments. It also provides some credence to their technology.

Although I am not fond of their prospects, Wave does not appear expensive relative to peers, and market sentiment is positive. So, it's difficult to take a negative stance on Wave. Given these considerations, the safe play on Wave right now is a "hold," with an emphasis on monitoring the company's progress on clinical developments and strategic initiatives for potential future reassessment. I'm looking for some differentiation here and I'm just not seeing it yet.