Rob_Ellis

Rob_Ellis

Note: This article should be seen as continuation of my prior coverage of this ticker.

W&T Offshore (NYSE:WTI) reported earnings this past week. I doubt anyone cared much about the EPS miss as the company is not profitable on a GAAP basis so that is largely a meaningless statistic right now.

However, investors may have been disappointed with the guidance in the press release which doesn't show any visible catalyst that could lead to a repricing of W&T's deeply undervalued reserves.

Most importantly, the promising Holy Grail drilling prospect, which was already delayed last year into 2024, is now getting pushed out again, at least until 2025:

In addition, given our recent acquisitions and the current acquisition opportunities in the Gulf of Mexico, we have decided to defer the drilling of our Holy Grail well until 2025, which will reduce our drilling and capital investment plans for 2024 to between $35 million and $45 million.

Without the Holy Grail, which would likely lead to a significant increase in production and cash flow, it is not clear who would show interest in the undervalued assets at this point in time.

My prior articles highlighted W&T's undervaluation relative to its asset base. This part of my thesis hasn't changed and there are multiple paths to show W&T Offshore's enterprise value should be 2-3x times higher.

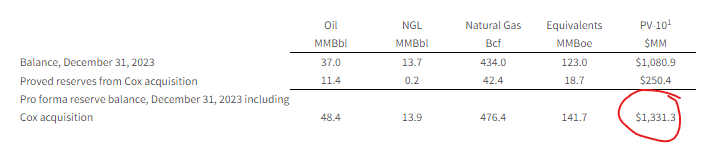

For example, just the pro forma PV-10, including the assets acquired this January from the privately held Cox, exceeds twice the enterprise value:

W&T Offshore

However, the market isn't willing to value these reserves higher because W&T's production is declining, even with the bolt-on acquisitions the company is prioritizing:

Production for the fourth quarter of 2023 was 34.1 MBoe/d compared with 35.9 Mboe/d for the third quarter of 2023 and 38.6 MBoe/d for the corresponding period in 2022.

Free cash flow is also at a low point compared to the prior few years:

Seeking Alpha

The "opportunistic acquisitions" W&T touts are basically mitigating the production declines (which per the company are 15% overall and 10% for the Mobile Bay gas assets), but don't seem to be generating incremental growth.

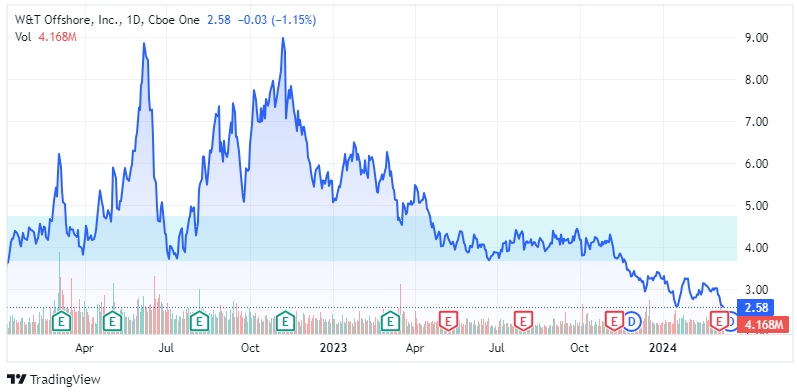

When I covered W&T last year, the stock was at an important support area, so the upside from a Holy Grail announcement seemed to make for a good risk-reward tradeoff.

However, W&T has now broken below this support region and is in search of a new bottom that may even take us back to the 2020 pandemic levels:

TradingView

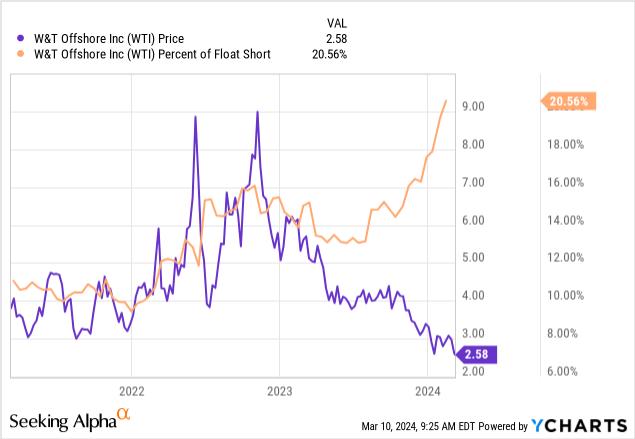

Perhaps, on the positive side, short interest, which has historically been high for W&T, has risen to a multiyear high:

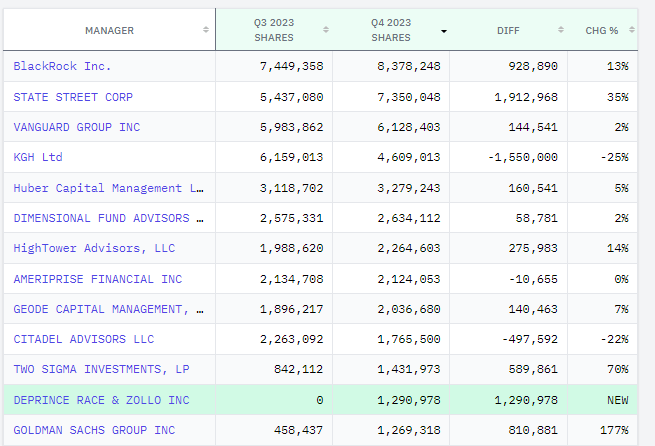

That is clearly not sustainable as most W&T shares, apart from the 1/3 owned by the CEO Tracy Krohn, are institutionally owned, so the marginal sellers will run out at some point:

13f.info

So there is always the hope for some squeeze upward. However, even that would require some catalyst, and, with management reluctant to clarify what the end game is for this company, I am not sure any longer what that might be or when it would come.

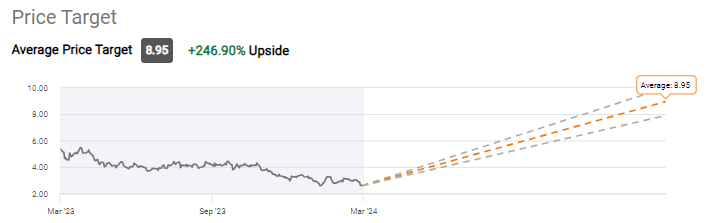

The few Wall Street analysts who cover the ticker remain at strong buy and long-term that makes sense in view of the underlying asset value I highlighted:

Seeking Alpha

But that value won't get unlocked by itself without a production increase or perhaps someone even buying the company if Mr. Krohn is looking to retire.

W&T's earnings obviously disappointed, but my take is that was more from a forward guidance than from a look-back perspective. As a portfolio of Gulf of Mexico oil and gas assets, W&T remains deeply undervalued. However, the market isn't willing to apply higher multiples without some tangible action that shows the path to higher production, more cash flow and ultimately shareholder returns.

My biggest hope was on the Holy Grail, but now that it has been postponed again, I fear W&T may be stuck in limbo for a while. I retain a small long position in the stock as at some point that could go double or triple, but if you want to avoid dead money you may also consider waiting for something to happen before you buy.