West Pharmaceutical Services is a global manufacturer specializing in advanced containment and delivery systems for injectable drugs and healthcare products.

The company has a strong focus on high-value products and strategic collaborations, positioning it for future growth in the healthcare sector.

Despite current challenges and a somewhat lofty valuation, projected earnings growth suggests the potential for significant long-term returns.

Pavel Muravev/iStock via Getty Images

Introduction

After having covered a lot of energy stocks in recent days, it's time to shed some light on areas I may have neglected a bit.

Hence, in this article, we'll revisit a company I have covered just once in the past.

That company is West Pharmaceutical Services (NYSE:WST), in this article sometimes referred to as "West" or "West Pharma."

My most recent article on the stock was written on March 13, 2023, and had the title "Healthcare's Hidden Gem: West Pharmaceutical Services."

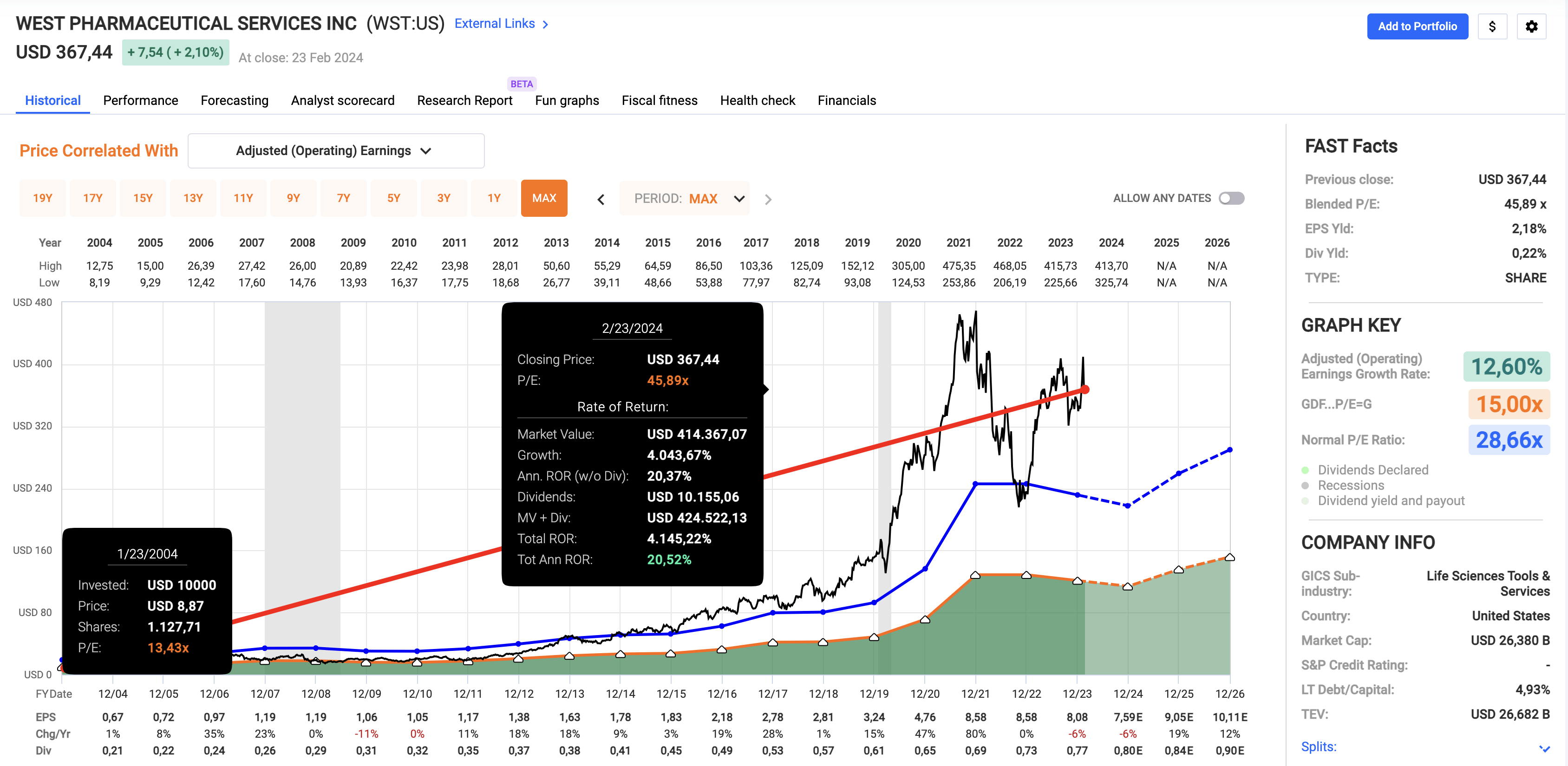

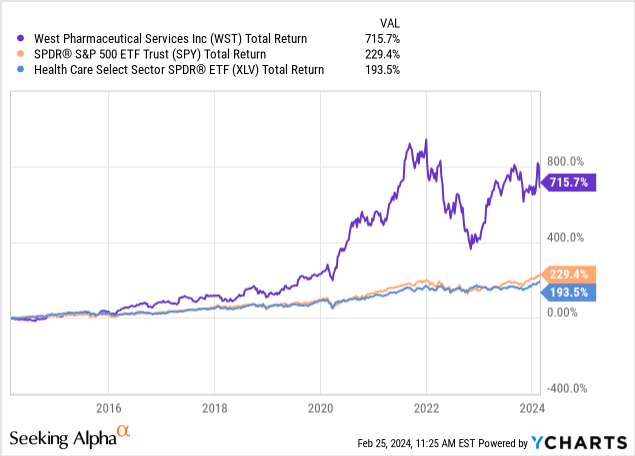

Since then, shares have returned 17.1%, lagging the 32.7% return of the S&P 500 by a wide margin.

However, this includes the most recent post-earnings sell-off, which explains why shares are currently trading roughly 12% below their all-time high.

In light of this sell-off, I decided to cover the stock again, discussing its characteristics, recent earnings, and long-term total return potential.

After all, we're dealing with a stock that has returned 20% per year over the past 20 years!

FAST Graphs

Although it may upset some people that WST yields just 0.2%, there's plenty to be excited about if you're not entirely dependent on income from your investments.

So, let's dive into the details!

Fast-Growing Healthcare

With a market cap of roughly $26 billion, West Pharma is one of the biggest companies in the medical instruments & supplies industry, which is a part of the healthcare sector.

To be precise, West is a global manufacturer specializing in the design and production of a wide range of advanced, high-quality containment and delivery systems for injectable drugs and healthcare products.

This is why the company did so well during the pandemic, as I will discuss in this article.

Essentially, the company's product portfolio includes proprietary packaging, containment solutions, drug delivery systems, and related products that are sold to a wide range of healthcare companies.

Its products are usually sold through a combination of direct sales, distribution networks, and contract agents.

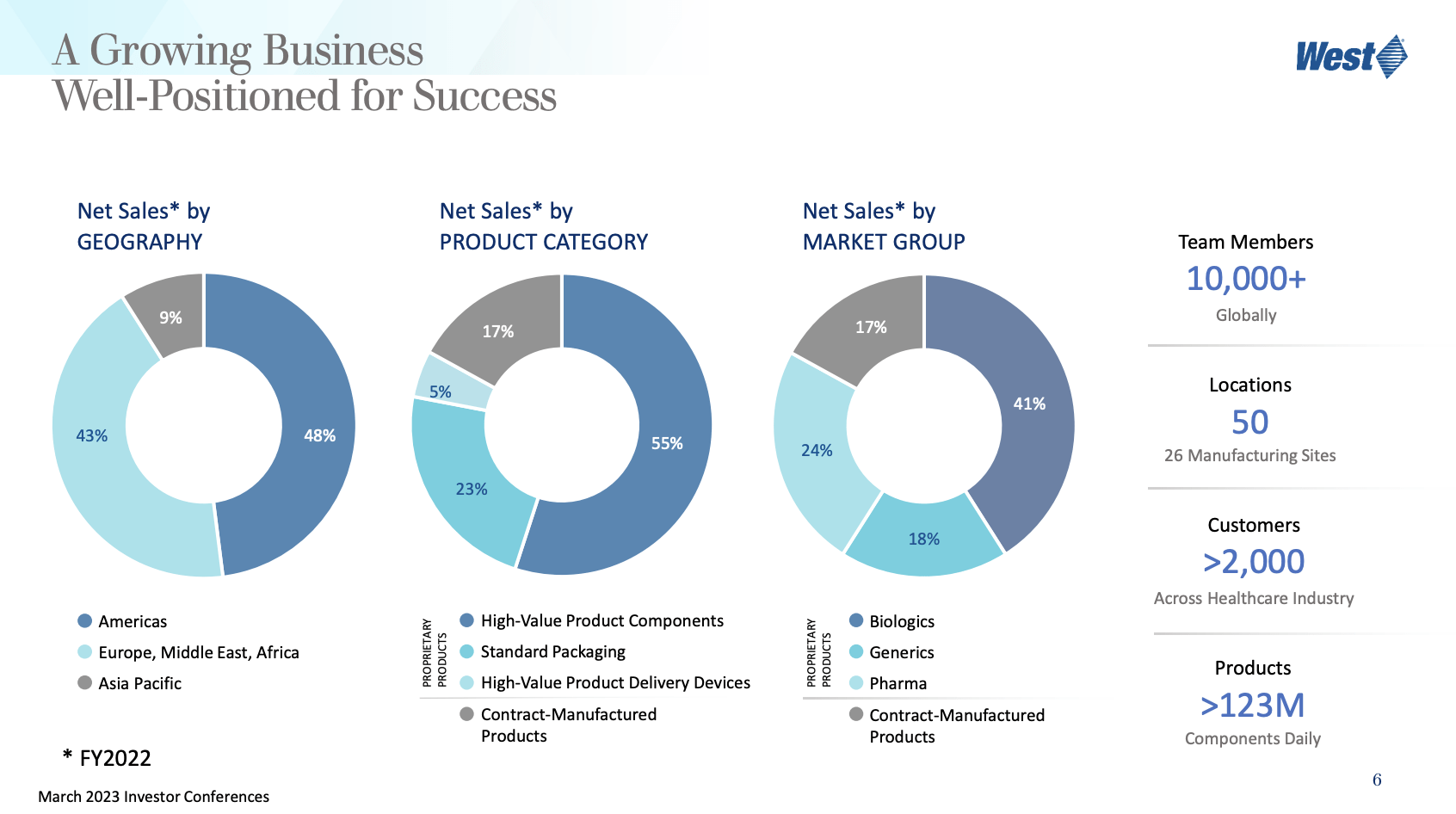

As we can see below, West operates through two primary global business segments: Proprietary Products and Contract-Manufactured Products.

West Pharmaceutical Services

Moreover, the overview above shows that the company has significant international exposure, which is managed similarly to domestic operations.

While international exposure opens up new opportunities, it also adds currency risks, which is quite common in the highly globalized healthcare sector.

Adding to that, the company faces competition in both its proprietary and contract-manufactured product lines. In order to combat these competitors, it sees product design, consistent quality improvement, regulatory compliance, and innovation as clear differentiators.

West Pharmaceutical Services

Furthermore, to remain competitive, the company uses its position as a supplier of key materials to improve its relationship with customers.

Essentially, through collaborating with customers and investing in strategic initiatives, the company aims to develop new products and solutions to stay on top of its competition, which is not only smart but a topic I studied in great depth when I was finishing my master's degree on this subject.

Here are a few benefits from a supplier's point-of-view that I have worked on in recent years:

Increased innovation: Access to customer insights and feedback helps suppliers to innovate with specific market needs in mind. This also lowers risks.

Enhanced market access: Suppliers gain valuable insights into customer preferences and specific market trends. This, too, lowers risks and makes it easier to expand certain production lines.

Reduced development costs: Sharing resources and expertise with customers can lead to cost savings.

Improved brand reputation: Active involvement in customer-centric co-development enhances a supplier's image and strengthens the relationship. In times of distress (like a pandemic), these relationships are highly valuable.

In other words, West Pharma is strategically using its relationships to grow its footprint in the industry and become increasingly important for its customers.

That's a win-win and has resulted in West becoming a highly diversified player, as we can see in the overview below as well.

West Pharmaceutical Services

Furthermore, as I wrote in my prior article, it also comes with higher margins:

In 2016, only 15% of products sold were high-value products. In 2022, that number was 20%. In terms of sales, 45% of total sales were high-value products in 2016. In 2022, that number was 63%.

West Pharmaceutical Services

In addition to that, the company looks for opportunities for acquisitions, partnerships, and licensing agreements to further improve its product portfolio and capabilities.

As a result, the stock has been an outperformer. Not only did it return 20% per year since 2004, but it also returned 716% over the past ten years, leaving the S&P 500 and the SPDR S&P Healthcare ETF (XLV) in the dust, both of which had stellar performances.

However, the stock has been struggling recently, although "struggling" may be a bit too harsh.

The stock is up roughly 4% year-to-date and unchanged since mid-2021, which is mainly caused by the mind-blowing performance during the pandemic, which stretched the valuation, as the stock went 3x between early 2020 and mid-2021!

That's also the reason why my first article on the stock had a neutral rating, as I didn't like the valuation.

Temporary Post-Pandemic Headwinds

Like many of its peers, the company is still stuck in the post-pandemic rut.

As one can imagine, the company's stellar performance during the pandemic was caused by the fact that it sold the required supplies for vaccines (and so many other products).

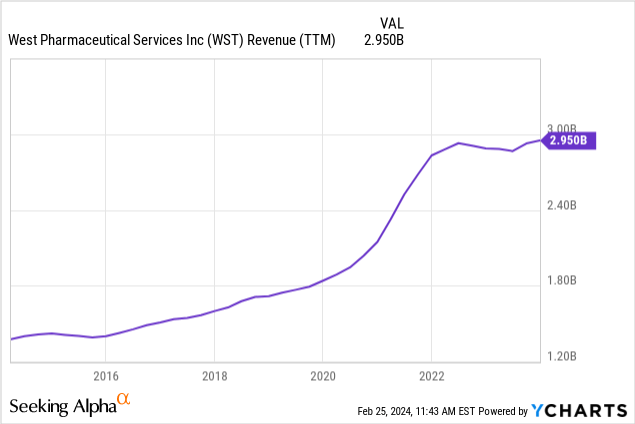

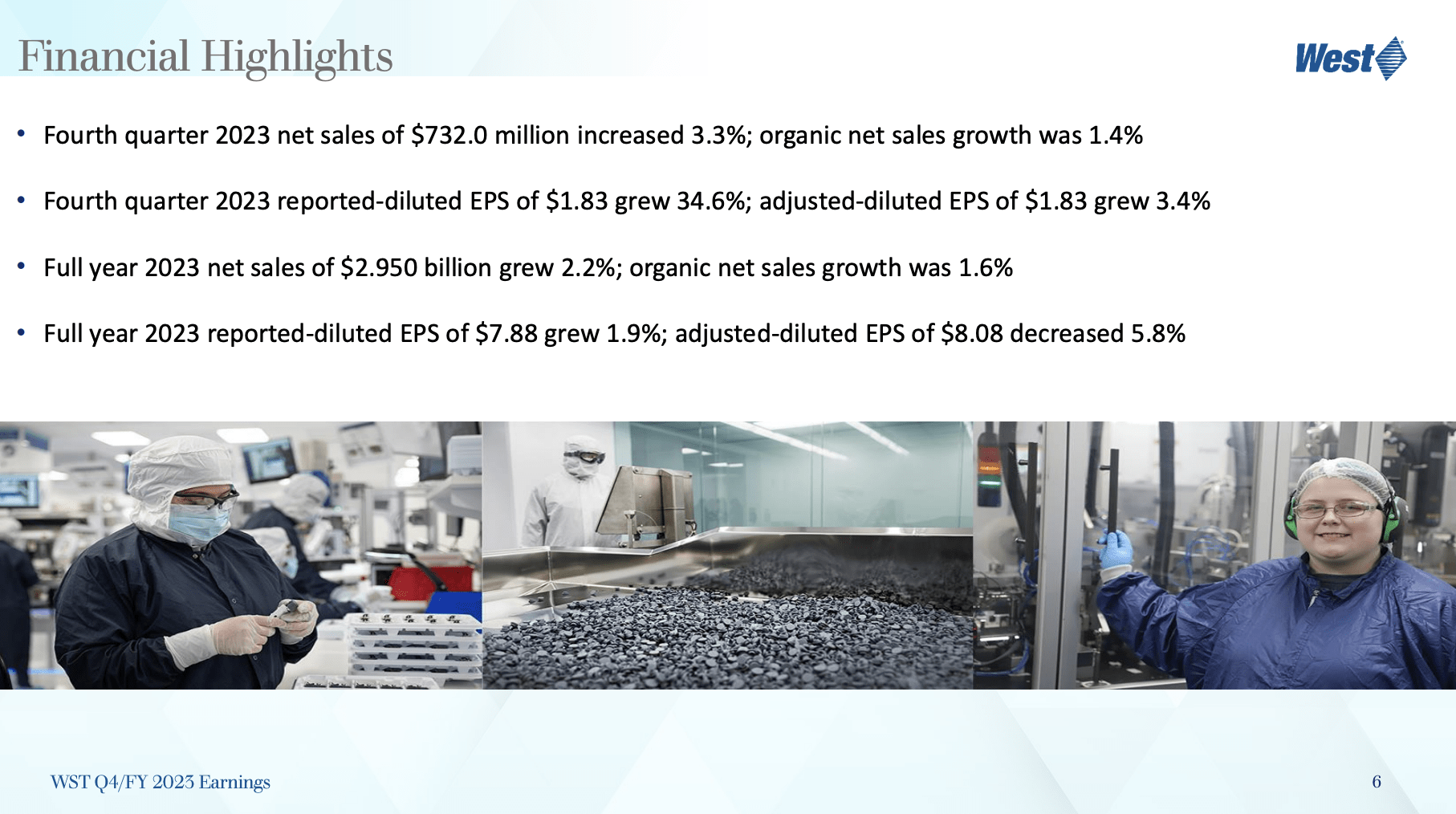

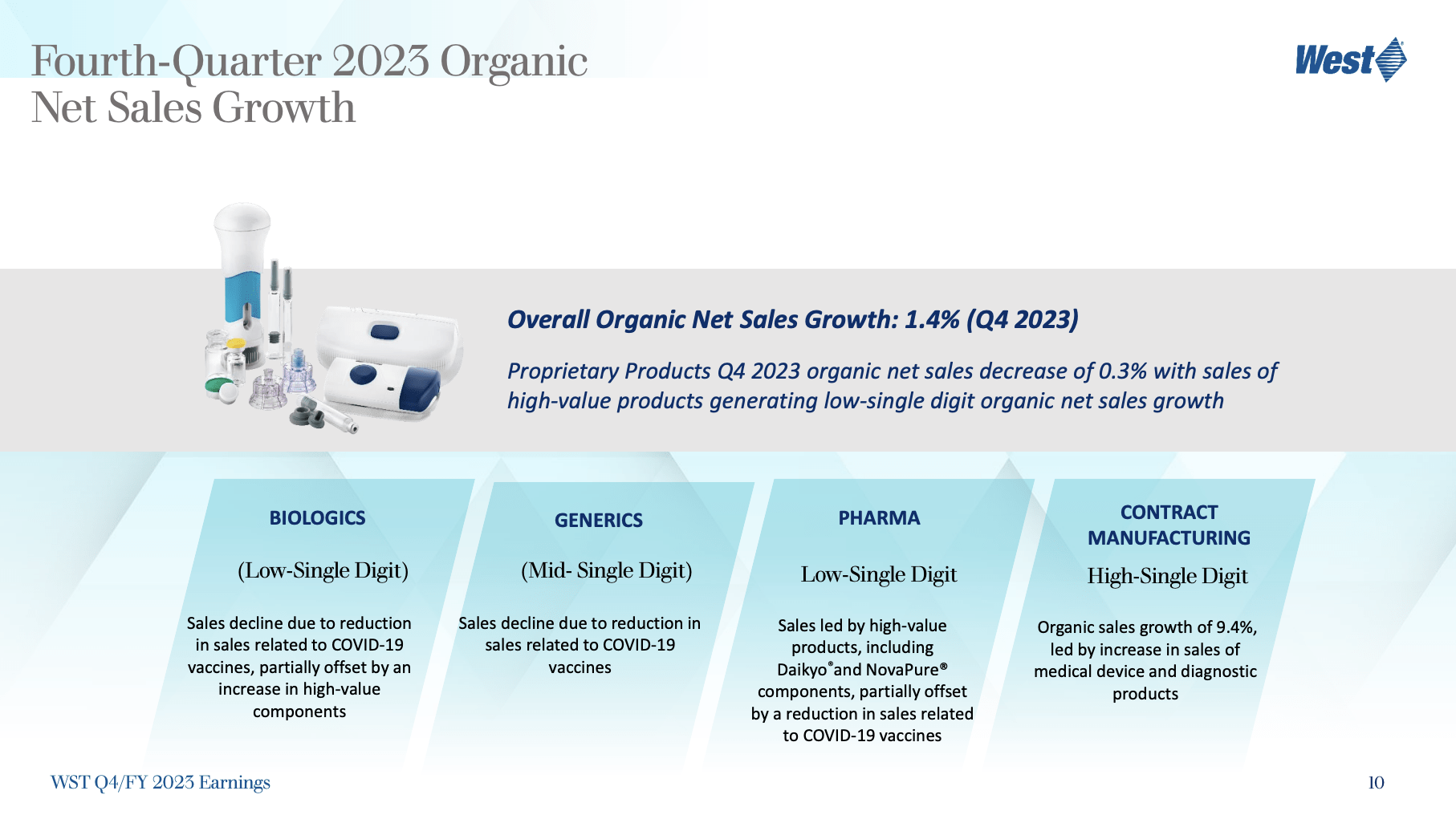

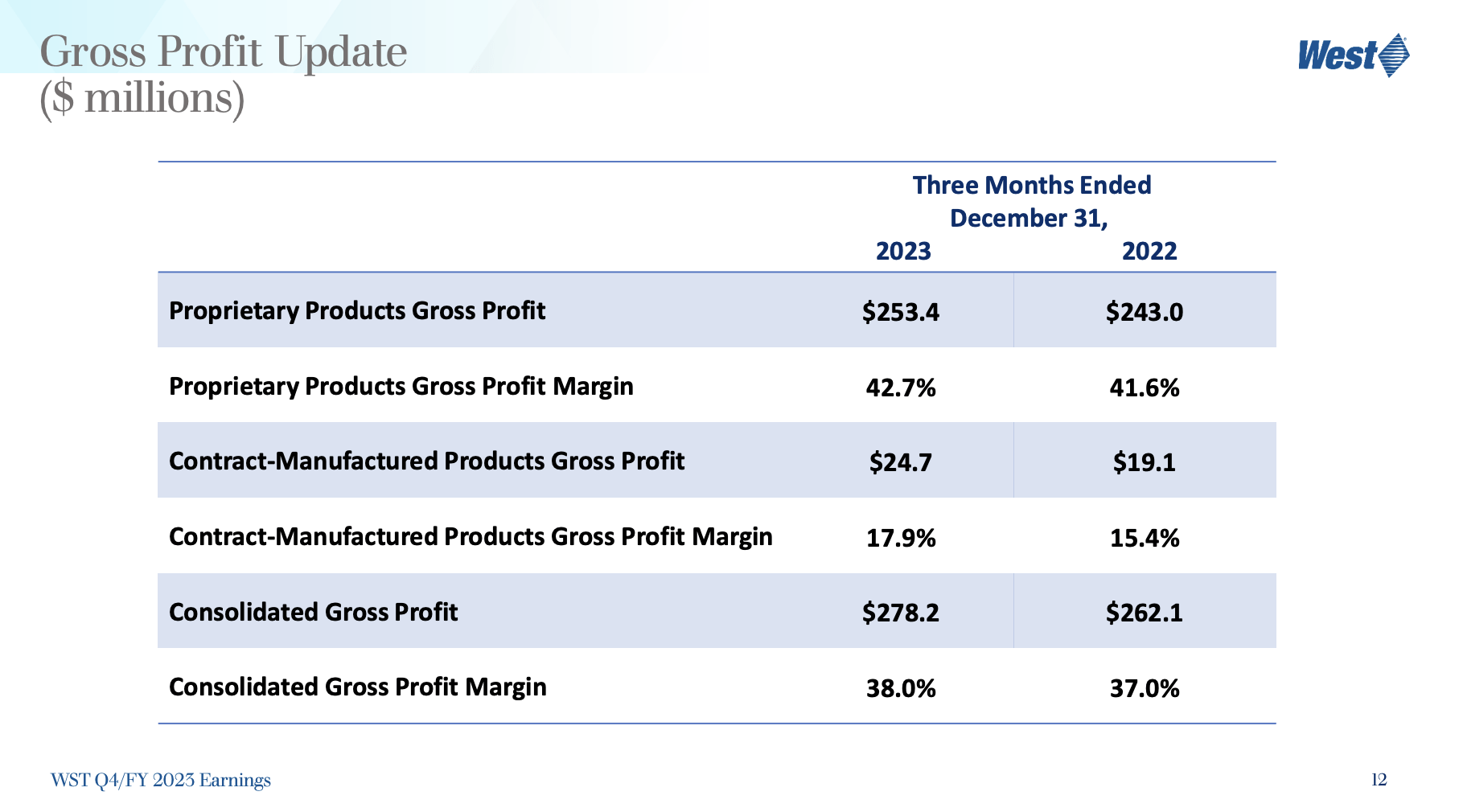

For example, in the fourth quarter of 2023, the company reported net sales of $732 million, with organic sales growth of 1.4%.

Growth was pressured by a decline in COVID-related net revenues, which the company estimates to be roughly $48 million compared to the previous year.

West Pharmaceutical Services

Moreover:

Within the company's proprietary products segment, organic net sales declined by 0.3% during the quarter. This decline was primarily attributed to COVID-related factors and inventory destocking among certain customers.

However, high-value products, which account for about 75% of proprietary product sales, saw low single-digit growth. This growth was driven by customer demand for HVP (high-value product) components and devices.

According to the company, and with regard to my prior COVID comments:

Looking at the performance of the market units, the pharma market unit had low single-digit growth led by demand for Daikyo and NovaPure components, partially offset by a reduction in sales related to COVID. The biologics and generics market units experienced low single-digit and mid-single-digit declines respectively, due to a reduction in sales related to COVID-19 vaccine. - WST 4Q23 Earnings Call

West Pharmaceutical Services

Furthermore, the good news is that the gross profit margin for the quarter improved to 38%, which is a 100 basis points improvement compared to 4Q22.

As a result, the company's adjusted operating profit rose to roughly $160 million, with a margin of 21.8%.

West Pharmaceutical Services

Adjusted diluted EPS increased by 3.4% in the fourth quarter, which indicates overall profitability improvements despite some demand headwinds.

I can live with that.

What's Next?

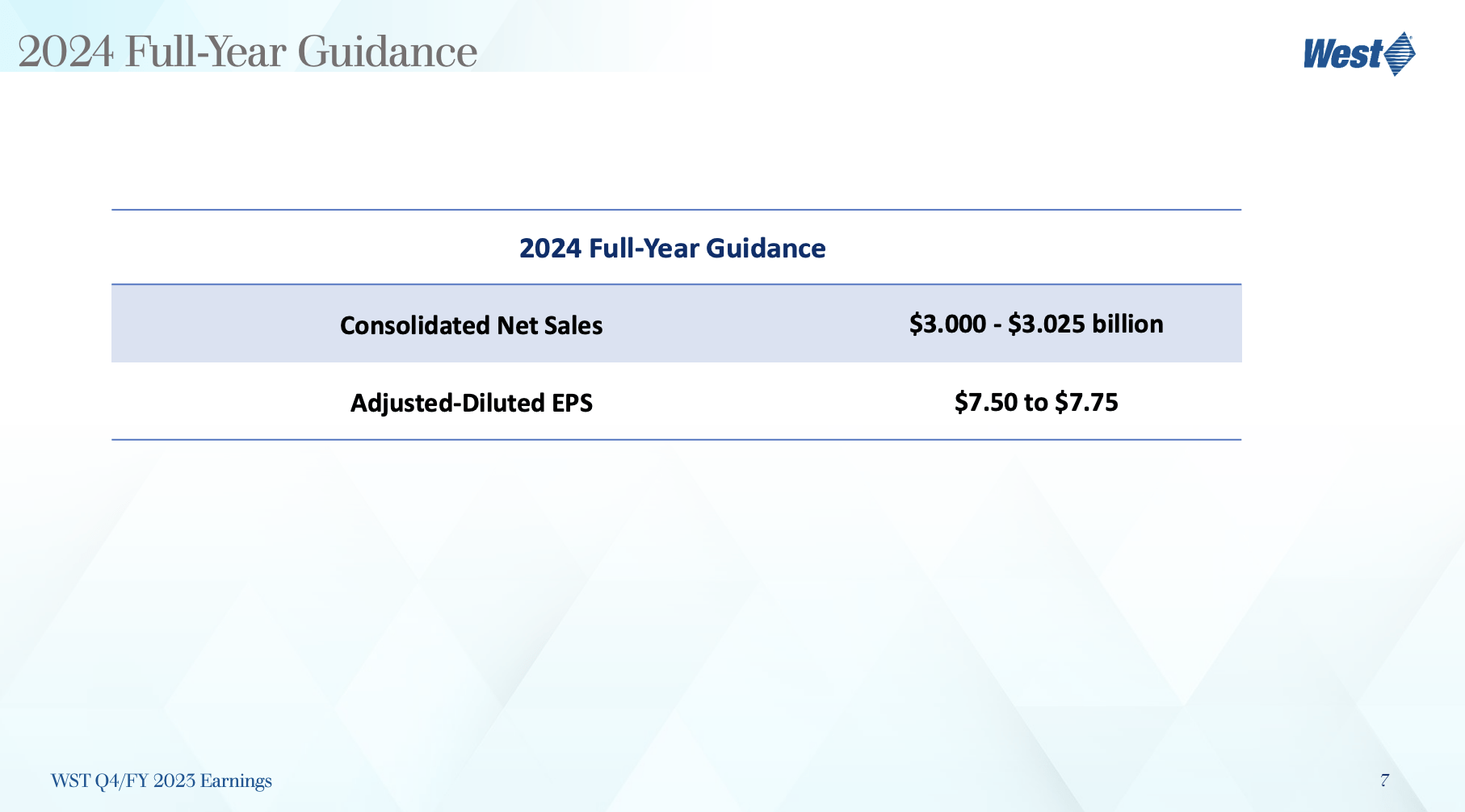

During its earnings call, the company provided guidance for the full-year 2024, expecting net sales of roughly $3 billion.

Furthermore, organic sales growth is expected to be somewhere between 2% and 3%, leading to an adjusted diluted EPS guidance of $7.50 to $7.75.

West Pharmaceutical Services

Analysts expect $7.59 in 2024 EPS.

In 2023, the company generated $8.08 in EPS, which would make 2024 the second consecutive year of 6% EPS contraction.

The reason why the stock sold off after earnings isn't just that these numbers are somewhat poor, but that the company revised its outlook for organic sales growth, expecting it to be lower than previously anticipated.

Several factors contribute to this revised outlook, including a continued decline in COVID-related sales, delays in the manufacturing capacity for certain devices, timing issues with customer upgrades, and widespread destocking across the industry.

Nonetheless, while the company expects the first quarter of this year to be the most challenging, it remains very confident in its growth prospects beyond 2024.

Analysts agree with this assessment, as we'll see in the valuation part of this article.

However, before we get to that, I need to mention that the company is very committed to expanding its industry-leading capacity to support future growth.

For example, major expansion projects in HPV capacity are underway in various locations, including Jersey Shore and Eschweiler.

HVP devices, which include injection delivery device platforms and containment solutions, saw double-digit organic sales growth in 2023 and now represent 10% of the company's overall sales.

Moreover, to meet higher demand for its products, the company is investing in expanding capacity for multiple product ranges, including SmartDose, SelfDose, and admin systems.

Furthermore, ongoing expansion projects, like the one at the Dublin facility dedicated to future injection device manufacturing, are expected to be completed in 2024 and put the company in a great spot for continued growth in 2025 and beyond.

West Pharmaceutical Services

In addition to all of this, certain drugs, like the ones used to treat diabetes and obesity, are expected to see further accelerating growth and enhance demand for WST's products.

Valuation

The valuation is still lofty. However, it's getting better.

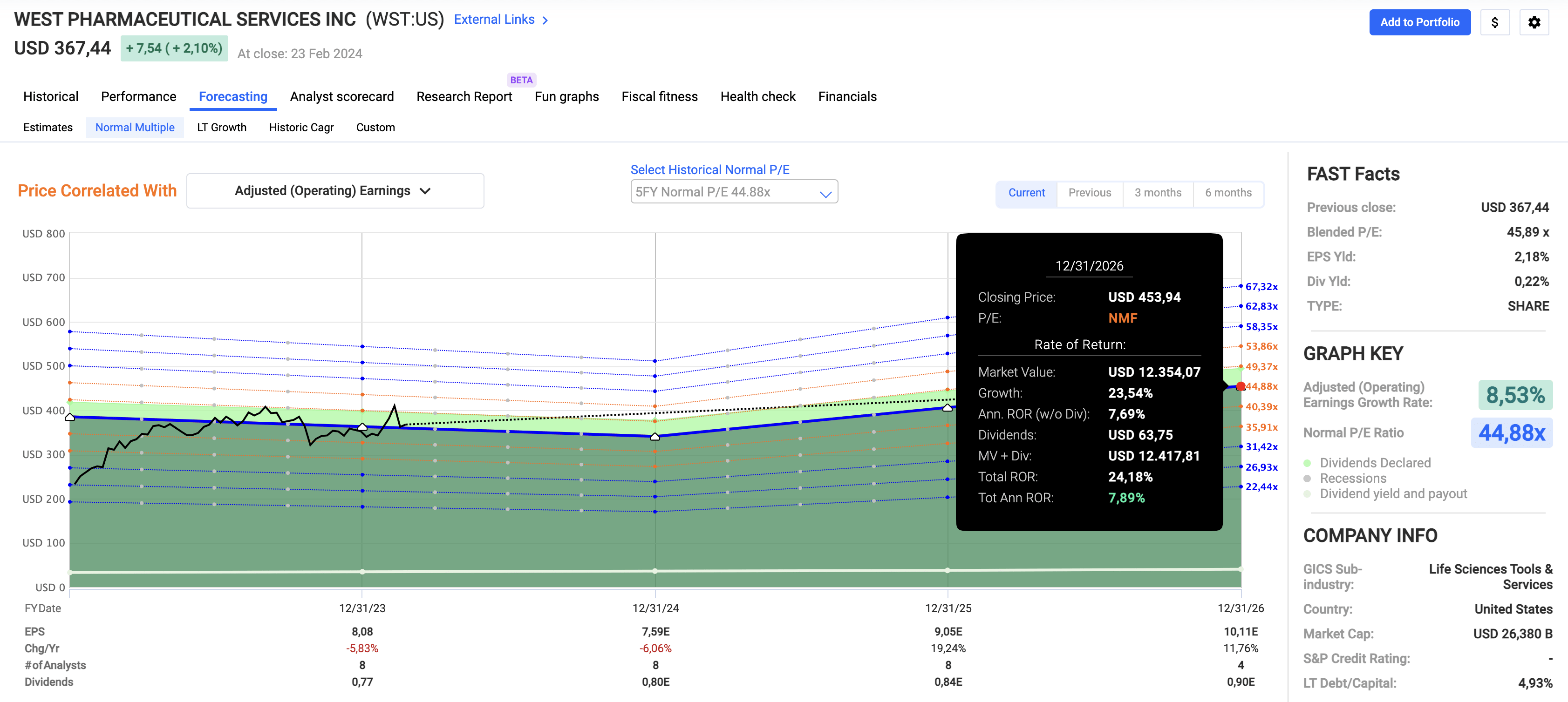

WST currently trades at a blended P/E ratio of 45.9x.

Its normalized P/E ratio over the past five years is 44.9x.

Analysts expect EPS growth to accelerate to 19% in 2025, potentially followed by 12% growth in 2026. I expect these elevated growth rates to continue ignoring new potential supply headwinds.

FAST Graphs

In other words, I will give the stock a Buy rating with a potential total return of 7-10% in the years ahead.

This is based on its expected EPS growth and its 45.9x normalized multiple, which can be seen in the chart above as well (7.9% annual return).

The only reason why I haven't bought a position yet is that I have a lot of stocks on my watchlist and that I have not yet decided how I want to structure the healthcare segment in my portfolio.

So far, I already own a healthcare supplier (Danaher (DHR)), which is also dependent on healthcare innovation demand, to put it bluntly.

That said, I am very upbeat about the future of WST.

Despite current headwinds, I believe the stock is in a great spot to outperform the market on a prolonged basis and by a significant margin.

Takeaway

Despite recent challenges, including post-pandemic adjustments from customers and supply chain disruptions, West Pharma remains a key player in the healthcare sector.

Its focus on high-value products and strategic collaborations positions it well for future growth.

While the current valuation may seem lofty, projected earnings growth suggests the potential for substantial returns on a long-term basis.

Pros & Cons

Pros:

Resilient Business Model: West Pharma has shown resilience, with a history of elevated (read: sky-high) returns.

Focus on High-Value Products: The company's emphasis on high-value products contributes to its competitive edge and growth potential.

Strategic Collaborations: Strategic collaborations and investments in innovation enhance its position in the healthcare sector.

Projected Earnings Growth: Despite current challenges, projected earnings growth suggests the potential for significant returns in the future.

Cons:

Valuation Concerns: The current valuation is somewhat lofty, which could impact its shorter-term stock price performance.

Post-Pandemic Adjustments: Like many peers, WST is navigating post-pandemic adjustments, leading to some uncertainty in its near-term performance.

Supply Chain Disruptions: Supply chain disruptions pose ongoing challenges and could impact operational efficiency.