Smith Collection/Gado/Archive Photos via Getty Images

Smith Collection/Gado/Archive Photos via Getty Images

Williams-Sonoma (NYSE:WSM) is one of the most popular retailers for individuals looking for high-quality home furnishing and kitchenware. Even though I typically steer clear from retailers due to their tight relationship with economic trends, I am considering buying shares in Willams-Sonoma. This consideration is mainly driven by the company's competitive advantage, effective management team, and good financials, all of which can contribute to the company's resilience during economic uncertainties.

I will discuss the stock price, the business, and the financials. I will then consider growth opportunities and possible risks and I will finally conclude with a valuation.

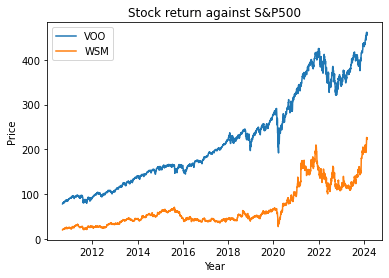

During the last 15 years, the stock price appreciated by more than 2600% while the S&P500 grew by only 480%. It is not that frequent to find a company's stock outperforming broader market indexes, such achievement is usually the reflection of a strong brand and a fundamentally sound company. Now, let's delve deeper into the factors contributing to this performance.

Stock Quotation VS S&P500 (Author's calculation with a Python script using Yfinance library)

Williams-Sonoma is a retailer that specializes in high-quality products for the home through nine different businesses.

Company's Businesses (Company's Investor Relation)

These brands create a good competitive advantage for two main reasons. First of all the company's focus on a digital channel strategy, which now represents around 70% of total sales. This achievement is attributed to a brand-new e-commerce platform and a global 'multi-tenant' platform utilized across all of the company’s brands, providing a competitive edge in terms of innovation. The platform allows the company to test a new idea or feature on a single brand, assess it, and swiftly implement it if proven effective, allowing it to enter the market much more rapidly than competitors. Moreover, the use of an e-commerce platform allows the corporation to gather valuable customer data to enhance the company's marketing strategy and overall boost sales.

Moreover, the company's in-house design allows it to cover all the product phases, from the idea to the realization to the sale, in contrast with the vast majority of competitors that are sourcing the design of the products across several areas of the world. Insourcing allows the company to develop and establish an incredible level of efficiency that allows it to produce higher-quality products while controlling operation costs.

The global furniture industry was $541.52 billion in 2023 and is expected to grow at a 5.36% CAGR until 2030 to $780.43 billion. These figures are in line with the company's expectation of a mid to high- single-digit growth rate in revenues over the long term.

The industry is cyclical, during times of crisis people tend to defer household expenses to more favorable times. However, the company's good financial position and the management team's ability to navigate through difficult periods ease my worries.

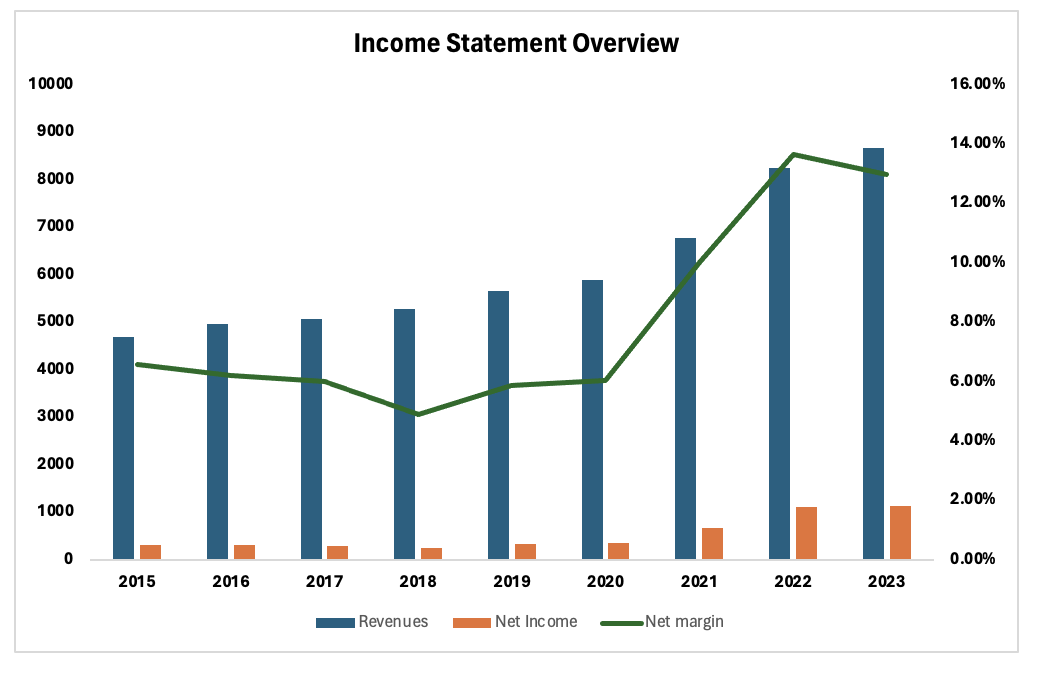

Over the last nine years, the company increased its revenues at a 7.05% Compound annual growth rate while its net income grew at around 15.48% CAGR. The net margin passed from 6.57% in 2015 to an impressive 13% during the last fiscal year. It is important to analyze these increases considering the effects of the pandemic, during which a lot of people, spending more time at home decided to modernize their living spaces. I anticipate a normalization of the data for 2024 and a gradual return to growth for the company after the FED starts lowering interest rates. This is expected to result in households saving money on mortgages and loans, making them more inclined to buy furniture, electrics, and cookware. The company in my opinion is well-positioned to stabilize its profitability at these levels over the next couple of years.

In line with this reasoning, during Q3 2023 the company reported a decrease in comparable brand revenue of 14.6% while beating the profitability estimates. These results show the strength of the company to generate solid bottom-line numbers also during tough times.

Income Statement Overview (Author's Excel sheet using Seeking Alpha data)

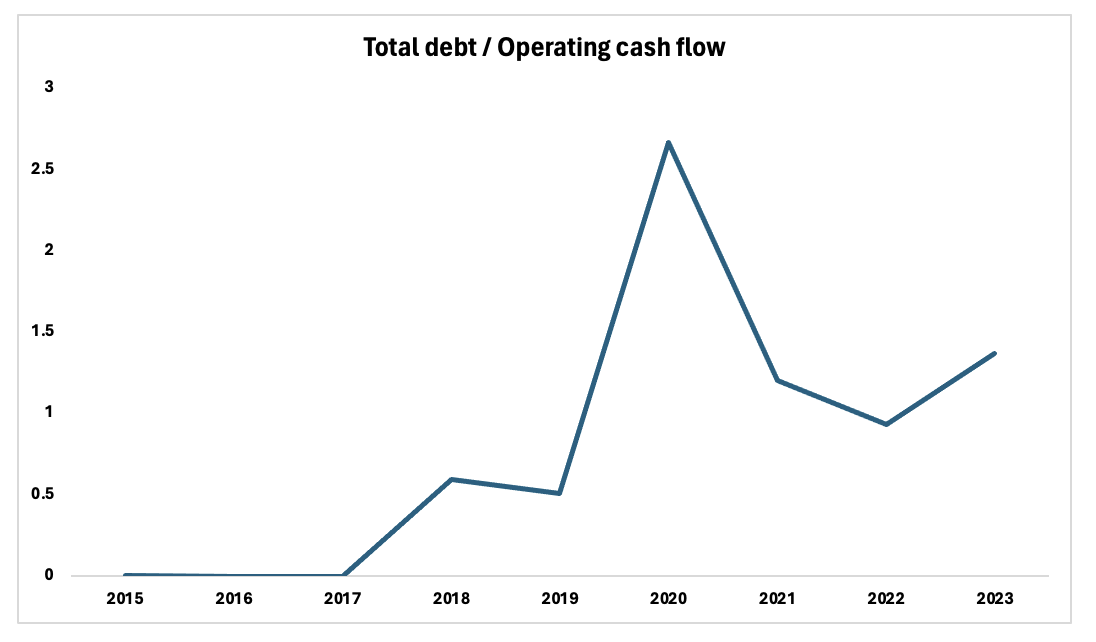

Over the last few years, the company paid back all its long-term debt resulting in an incredibly lean and healthy balance sheet. The total debt outstanding was just 1.37 times bigger than the operating cash flow, this situation allows the managers to not worry about debt outstanding and focus on the business, allowing them to compound over cycles.

Total debt/Operating cash flow (Author's calculation using Seeking Alpha data)

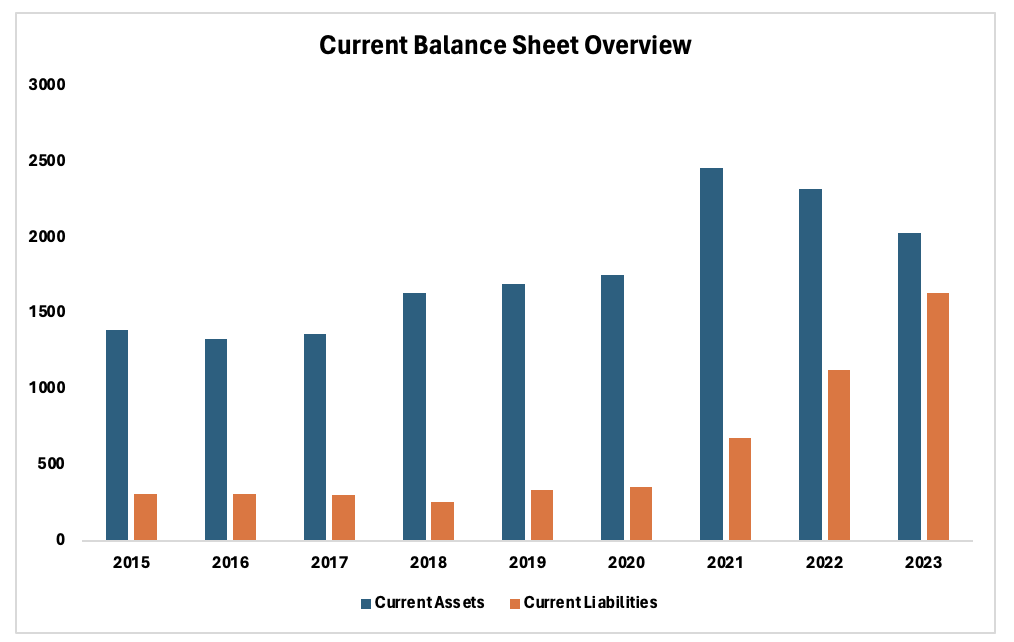

The company is also starting to better manage its working capital as we can understand from the reduction of the current ratio from 4.51 in 2015 to 1.24 last year.

Current Balance Sheet (Author's Excel sheet using Seeking Alpha data)

The cherry on top is represented by the cash flow statement. At the end of the day, the most important metric to me is how much cash a corporation can generate throughout a year. The cash flow from operations increased at a 9.59% CAGR since 2015 and free cash flow at an 11.76% CAGR. The company transitioned from a business model primarily based on physical stores to one more reliant on e-commerce and digital sales. As a consequence, managers were able to control its capital expenditures resulting in a growing free cash flow.

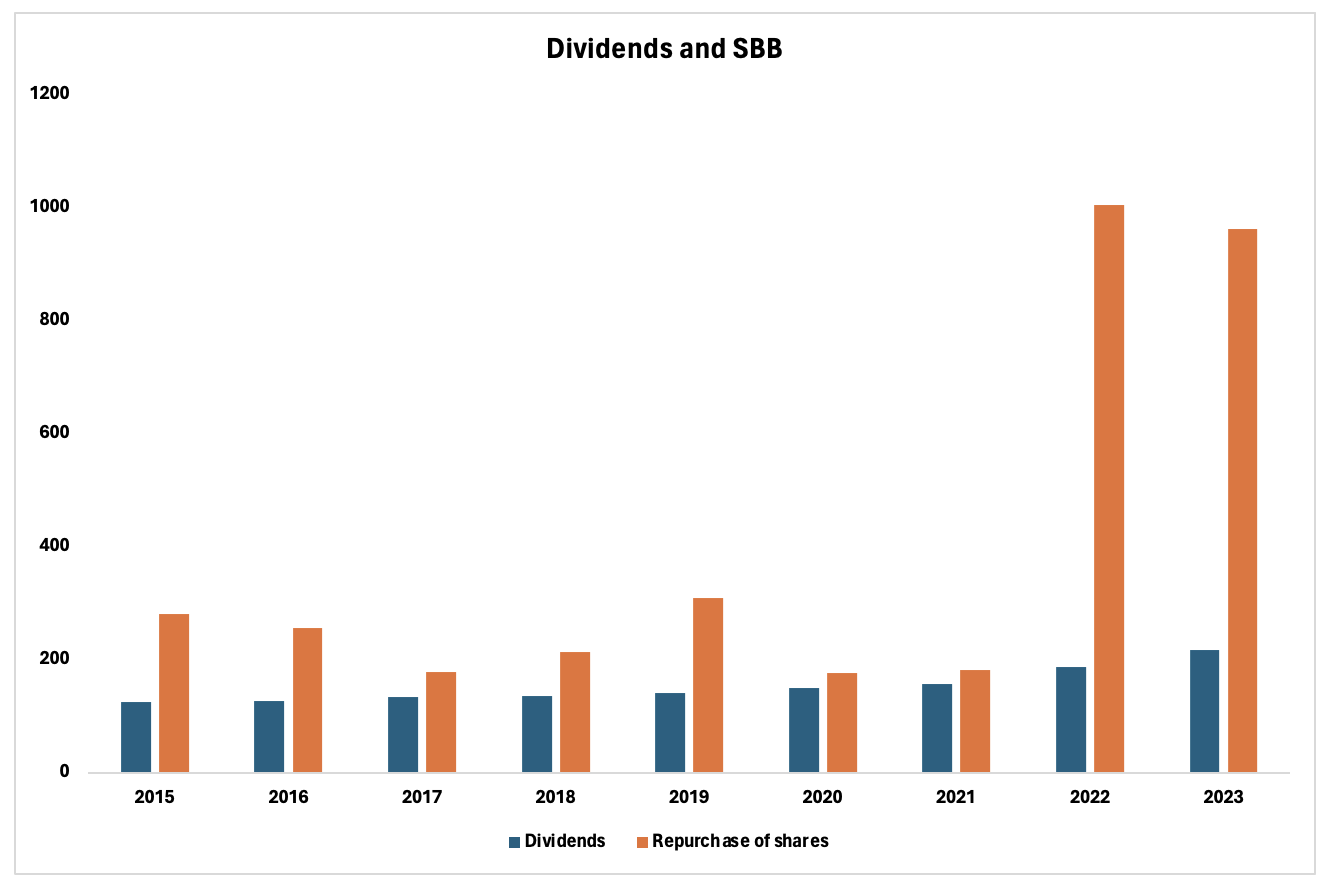

The company is focused on rewarding shareholders through buybacks and dividends. Since the company usually trades at pretty low multiples, share buyback has been a lot more aggressive lately. It is important to note that, as the stock price has increased in the last months, the company decided to pause the stock repurchase plan. I like the management team's rationale in this case, they place a lot of attention on how rewarding effectively shareholders. As the company in the last nine years repurchased shares for a total of around 24% of its current market capitalization, the dividend per share has significantly increased while the effective amount paid is almost the same every year. As a consequence, the dividend payout ratio is just around 23%, meaning that it is completely safe and there is also room for an increase in the future years.

Dividends and Shares Buyback Summary (Author's Excel Sheet using Seeking Alpha data)

Data coming from the past is not a guarantee of success in the future but the company has some really interesting growth opportunities ahead.

As the company continues to execute its current businesses, they are also trying to understand how to implement AI in its operations. The company began collaborating with Salesforce (CRM) to make its marketing campaigns more efficient, gaining greater visibility among customers and delivering more targeted messages. The company says it eventually plans to leverage generative AI capabilities to deliver even more personalized communications. This should allow the company to increase its revenue and profitability while also saving on marketing expenses.

Moreover, the company has spent a lot of energy in the last quarters trying to understand its pricing power. When we contemplate the furniture industry, the initial thought often revolves around the multitude of sales advertisements saturating various platforms – from the internet and TV to billboards. However, Williams-Sonoma research revealed that most of the sales are not efficient both from a short and long-term point of view. The CEO, Laura Alber, efficiently discussed during the last conference call the consequences of sales in the short term:

If you have less people buying furniture, you just reduce the price 20%, you get a 20% more people buy it, just to be even, right? So you may think you’re doing something, it’s what retailers do. They mark stuff down when they want more sales, and it’s not necessarily the case. In fact, we’ve done a lot of testing up and down to see where that sensitivity is.

In the long term, this approach proves inefficient because the company is positioned as a high-quality, high-design retailer. Hence, sales and discounts are not what mainly attract customers to the corporation.

I like the CEO's rationale around sales and I highly suggest watching her interview at the World Economic Forum where she talks about AI and pricing strategy if you are considering investing your money in the corporation.

The complete list of risks is described in the company's financial report (pages 9-28). In this article, I am delving into two current risks that might affect the company's operations in the short term.

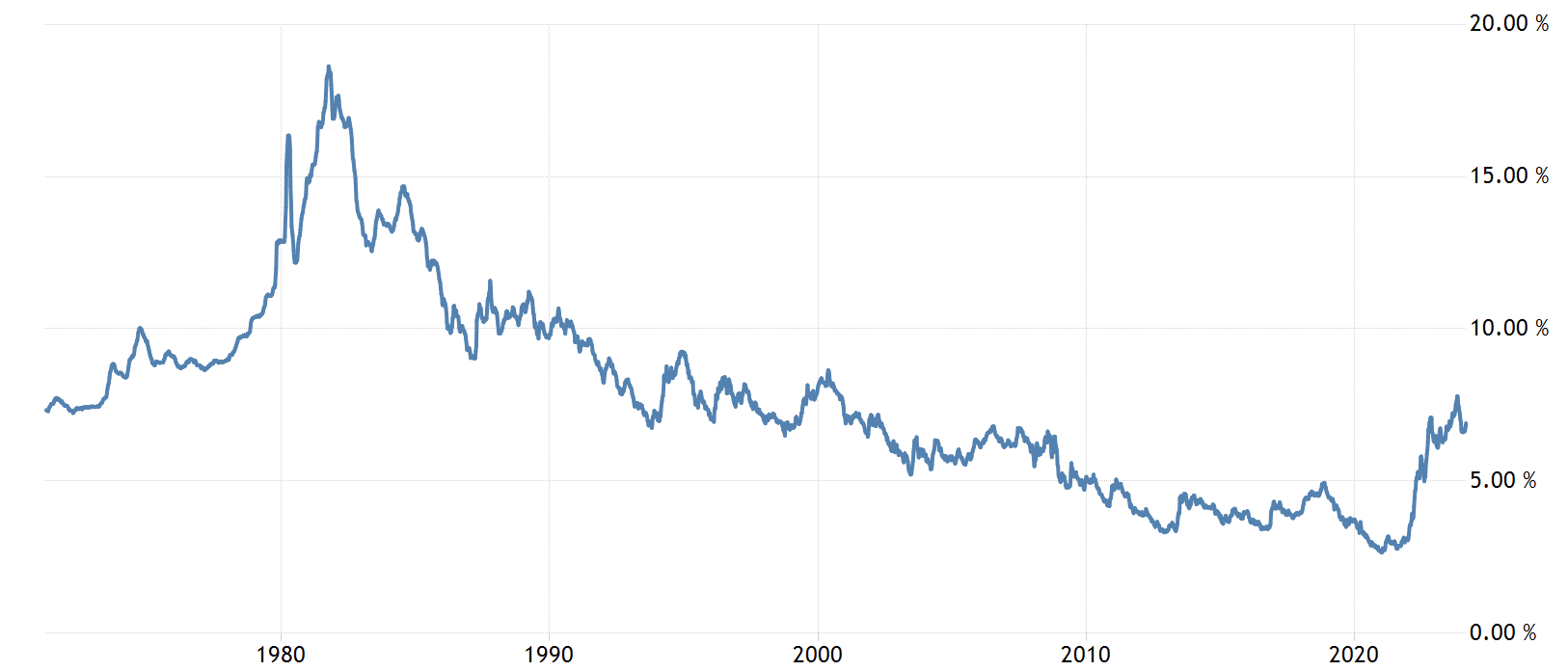

First of all, I don't appreciate the company's tight relation with general economic conditions, in particular interest rates. As mortgages are becoming more expensive, households have less money to buy furniture and expensive cookware, thus cheaper alternatives become more attractive during periods with high rates.

US 30 years mortgage rates (tradingeconomics.com)

The company is grappling with shipment issues mainly stemming from the Red Sea crisis which is slowing the shipments and is likely to increase costs over the next quarters. This situation might also affect the brand's image as customers have to wait more time for their purchases to arrive.

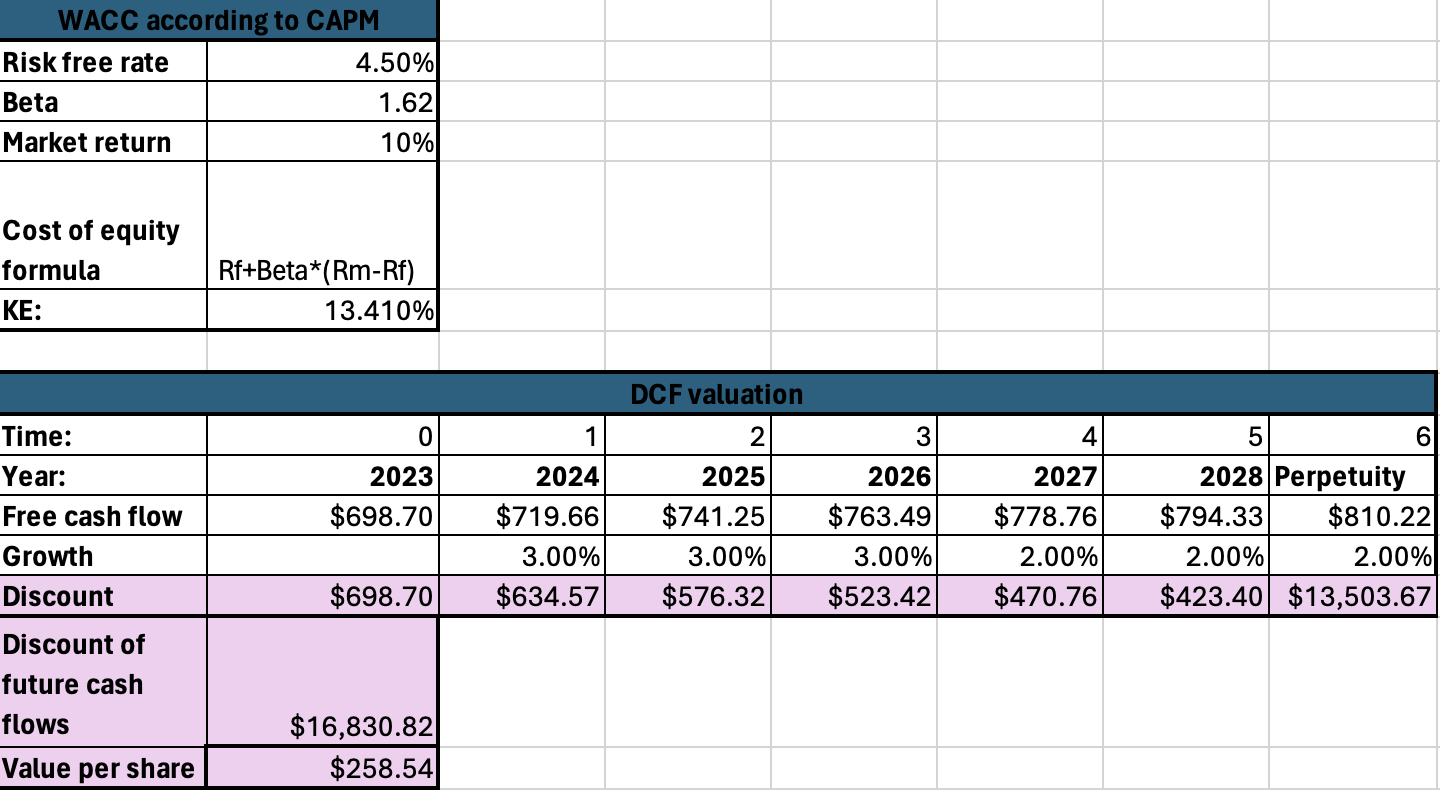

Since the company has a good cash flow and I expect it to be able to continue generating money at a good level also in the future, I will evaluate it through a discounted cash flow model.

In the first part, I computed the discount rate. Since the company has almost no long-term debt outstanding, I decided to use the cost of equity instead of the weighted average cost of capital. Considering a risk-free rate of 4.5% in line with the current macroeconomic conditions, a company's beta equal to 1.62, and a market return of 10% per year, I obtained a cost of equity of 13.41%, which I used as a discount factor.

Discounted Cash Flow Model (Author's Calculation)

To be as conservative as possible I decided to project moderate growth considering a 5% revenue increase per year, in line with the long-term firm's expectation. I obtained the free cash flow considering 4.2% of revenues in capital expenditures, constant over the years, and 2.5% of revenues in depreciation and amortization. I finally projected a 2% perpetual growth rate in line with the long-term FED inflation goal.

I obtained a fair value of $258.5 per share, showing a huge undervaluation of the stock, which is a buy in my opinion.

The undervaluation may be attributed to the high volatility of the stock price, primarily linked to the cyclicality of the business. Considering that the company is currently facing some challenges, mainly driven by a challenging macroeconomic environment, I see this as a compelling long-term buy opportunity to capitalize on future periods of economic expansion. Moreover, the company's strong balance sheet, cash flow generation, and amazing management team alleviate my concerns regarding economic cycles.