AzmanL

AzmanL

Readers may find my previous coverage via this link. My previous rating was a buy as I believed Warby Parker's (NYSE:WRBY) growth would accelerate from the low of 1H23, which should lead to a positive revision in the stock’s multiple. I am reiterating my buy rating as I remain very positive about the growth outlook of the business, expecting FY24 growth to come in at the high end and FY25/26 to grow at mid-teens (vs. the current low-teens). I don’t think the slowdown in e-commerce sales is a major problem given that it is cycling through the COVID highs and overall sales actually accelerated. With a better customer acquisition strategy and more efficient use of marketing dollars, I believe margins can expand as management has guided.

WRBY saw 4Q23 net sales grow 10.5% to $161.9 million, beating consensus expectations of 9.8%. Driving the growth was active customer growth of 2.5% to 2.33 million and revenue per active customer growth of 9.3% to $287. The active customer growth was especially encouraging, as it was a sequential improvement from 3Q23 by 1.8%. WRBY also opened 10 net new stores, ending 4Q and FY23 with 237 total stores. The slightly disappointing aspect was that GAAP gross margin declined by 125bps to 53.8%. The decline was largely due to the growth in the contact lens and holistic visioncare offerings, which are lower-margin businesses. Higher store occupancy costs were also one of the reasons for the lower margin. Overall, adjusted EBITDA margins came in at $9.4 million, a 5.8% margin. Regarding guidance, management guided for FY24 revenue growth of 12 to 13% and adjusted EBITDA margin of 8.9% at midpoint, and 1Q24 revenue growth expectation of 13.7–14.6% and an adj. EBITDA margin of ~10%.

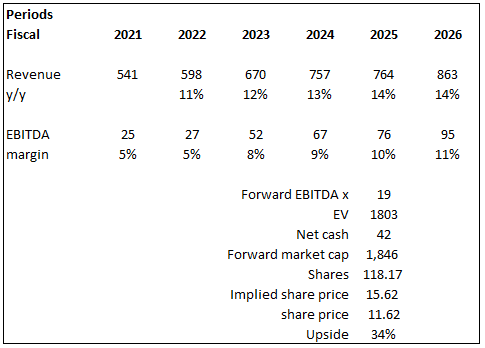

Based on author's own math

Based on my view of the business, WRBY should be able to grow at the high end of its FY24 guidance (13%) followed by sustaining a similar growth rate for FY25/26 (at 14% each), as I expect growth to be better when e-commerce growth turns from negative to positive. I think 14% is possible because 1Q24 is already expected to grow at around 14%.

On margins, the management long-term expansion target is 1 to 2 percentage points of the adjusted EBITDA margin per year. The way I see it, this is achievable given the growing efficiency of the customer acquisition strategy and the more efficient use of marketing dollars. Which means growth ahead could drive higher incremental margins.

Assuming 100 bps of expansion per month, I got 11% adj. EBITDA margin in FY26, equating to $95 million in EBITDA. If WRBY grows as expected, I think it should trade at a higher multiple than where it is today, given that in FY25, the business will have a better growth and margin profile. There might be some doubts about WRBY's ability to grow given the debate regarding sales cannibalization.

Once the market sees that overall growth accelerates, I expect the focus to shift to overall sales and margin improvement. Over the past year, WRBY traded at an average of 19x, and I expect a mean reversion.

And then guidance this year, 100 basis points roughly of EBITDA margin expansion. I know previously you've spoken to a target of 100 basis points to 200 basis points per year. Source: 4Q23 earnings

Overall, I remain positive about the business, as I am encouraged by WRBY's ability to sustain growth above 10%, ending the year with growth of 12% (140bps higher than FY22), and FY24 guidance points to the potential for further acceleration (considering that 1Q24 is expected to grow at a mid-teens percentage rate). I actually think there is potential for WRBY to come in at the high end of the guidance given that management is going to step up on marketing and be more focused on e-commerce.

Regarding marking, the plan is to focus on creating awareness by increasing media spending. This should have a very visible impact on top line growth as marketing spend is now expected to be higher than FY23 on an absolute basis, and this marketing spend ramp is against 2 years of decreasing marketing spend. However, this time, marketing spend is going to be allocated more efficiently—growth without diluting margins—and so far, it appears that management has been able to allocate marketing dollars to opportunities that have delivered returns that are pleasing.

One, we plan to increase our marketing and brand spend on a full year basis for the first time since 2021. Two, we expect to drive positive, sustained e-comm growth also for the first time since 2021.

And then as we just think about our marketing mix, we've been pleased by the returns that we've seen from our increased marketing investment, and we'll continue to deploy dollars opportunistically.

The second is deploying marketing dollars more efficiently deploying marketing dollars efficiently. And we're comping off of a period last year, where we cut marketing pretty substantially. Source: 4Q23 earnings

The second driver that should support FY24-guided growth is the improvement in customer acquisition efficiency. Recall that in the previous few calls, management has been consistently talking about being more convenient—providing locations for people to get eye exams. As such, I am very positive about the pace of store rollout over FY23, growing from 200 stores in 4Q22 to ~237 in 4Q23.

The fact that WRBY continues to open stores and is guiding to open more than 900 stores in the US is pretty strong evidence that the underlying ROI is quite attractive (FYI payback is within 20 months as per the past 2 earnings calls). I am expecting WRBY to continue opening more stores, and I think the target is not a far-fetched target given that there are more than 45,000 stores in the country.

The pushback here is that opening more stores will lead to a cannibalization of sales from e-commerce. This is not a wrong statement; overall, e-commerce sales actually fell by 6.2% in FY22 and 3.1% in FY23. However, I think investors should not be too myopic about this. I would argue that the overall business actually saw accelerating growth, and that is what matters.

Before the opening of more stores, the typical customer journey could be: (1) Check out the WRBY website; (2) Make purchases online without trying out physical products due to a lack of assessable locations. With new stores opening in the vicinity, The new customer purchase journey is likely to be: (1) check out the WRBY website or walk past a store; (3) try out the specs physically in the store to ensure fit; (4) purchase the product in store.

Notice how the origination could both be from the website, but sales are done in the store. I would further argue that the second journey is better for WRBY, as the store assistant could use that opportunity to upsell or cross-sell other products (a better lens, a better frame, etc.).

Moreover, investors should also note that e-commerce grew 25% and 83% in FY19/20 and 5% in FY21 on top of that elevated base due to COVID. FY22/23 is simply a phase where WRBY cycles through that elevated base. My view is that as long as overall revenue grows, it doesn’t matter if retail cannibalizes e-commerce since the digital space could be viewed as a customer acquisition channel.

If WRBY opens too many stores at once and demand does not materialize as expected or takes longer than expected to realize, it could put huge pressure on margins in the near term as store utilization is still immature. This could put pressure on the stock as investors look for concrete signs of margin inflection that will indicate the strength of underlying demand.

I am maintaining a buy rating for WRBY as active customer and revenue per customer growth remain strong. My view is that management's focus on customer acquisition efficiency and marketing spend will drive top-line growth, and that the e-commerce slowdown is not a major cause of concern given that it is cycling through pandemic highs. Importantly, overall sales growth is accelerating which means the strategy of opening new stores is working. The key risk is over-expansion leading to pressure on margins if store utilization falls short of expectations.