Su Arslanoglu/E+ via Getty Images

Su Arslanoglu/E+ via Getty Images

Freshpet (NASDAQ:FRPT) manufactures and sells pet food to dog owners. They are trying to take advantage of the ongoing “humanization of pets”. The company goes to market through grocery stores, discount clubs, specialty pet stores, and online. Freshpet has a premium valuation, a host of strong competitors, and no discernible moat. Daring investors should short shares at the current valuation of ~70X 2023 adj. EBITDA.

Freshpet went public in 2014 and has since grown revenue from $87M FY14 to $595M FY22. To accomplish this growth, Freshpet spent $861M on capex from 2014 – 2022. To fund capex, they have repeatedly tapped the capital markets. In 2022, Freshpet issued $350M of equity at $81 per share. The company also did a convertible debt offering, raising $391M in 2023. Based on how this was structured, it creates a dilutive overhang at $120 per share. Most of the raised money seems to have been spent on manufacturing plants and display refrigerators, as well as advertising. A significant portion of this revenue growth came from price increases. In the Q2 2023 conference call transcript management stated, “we’ve now taken price increases totaling a cumulative impact of approximately 27% over the past 18 months”. In the 3rd quarter of 2023, pricing was responsible for 7.5% of the 32.6% revenue growth the company achieved. Freshpet has achieved strong revenue growth by pouring money into capex, advertising spend, and raising prices on consumers.

At the end of 2022, Freshpet management outlined their “Fresh future” long-term plan. This includes more than tripling revenue to $1.8B and achieving adjusted EBITDA margins of 18% in 2027. For reference, 2022 results were $595M in revenue and $20M in adj. EBITDA.

This might be hard to achieve for a variety of reasons. The first is that consumer patience for price increases is wearing thin. As of May 2023, popular dog food brands had already raised prices 45.5% from 2020. As such, it seems like volume will have to drive revenue growth. It will be hard for volume to drive revenue when there is no benefit to feeding your dog fresh food. In fact, caloric density matters more than Freshpet’s marketing claims. According to Dr. Lindsey Bullen, “In terms of being nutritionally superior, fresh pet food diets are not”. So, an expensive product, that serves no purpose, and has plenty of competition is going to triple revenue while simultaneously increasing adj. EBITDA margin from 3.2% in 2022 to 18% with minimal price increases. That’s an incredibly high bar.

Even if you accept that the company can pull these projections off, you are paying a high price for 2027 results. If the company has $1.8B in revenue and 18% adj. EBITDA margins that will result in adj. EBITDA of $324M. At an EV of $4.35B, you are paying an Enterprise/adj. EBITDA multiple of 13.4x for 2027 EBITDA. Let’s compare this to other pet-related companies.

PetIQ (PETQ) manufactures and distributes pet products like flea and tick control, medications, and heartworm preventatives. They also provide veterinary services. The company reported earnings for Q3 2023 and raised their adj. EBITDA forecast to $99M - $103M for 2023. At an enterprise value of $844M, this company doesn’t need financing and trades at a multiple of 8.4x EV/EBITDA. This is 2023 EBITDA, not hypothetical 2027 EBITDA.

Petco Health and Wellness (WOOF) is a company that provides veterinary care, grooming, insurance, pet food, and pet supplies. It is expecting adjusted EBITDA of ~400M in 2023. Its current enterprise value is $3.6B. You can buy shares in Petco at ~9x 2023 EBITDA. This is 2023 EBITDA, not hypothetical 2027 EBITDA.

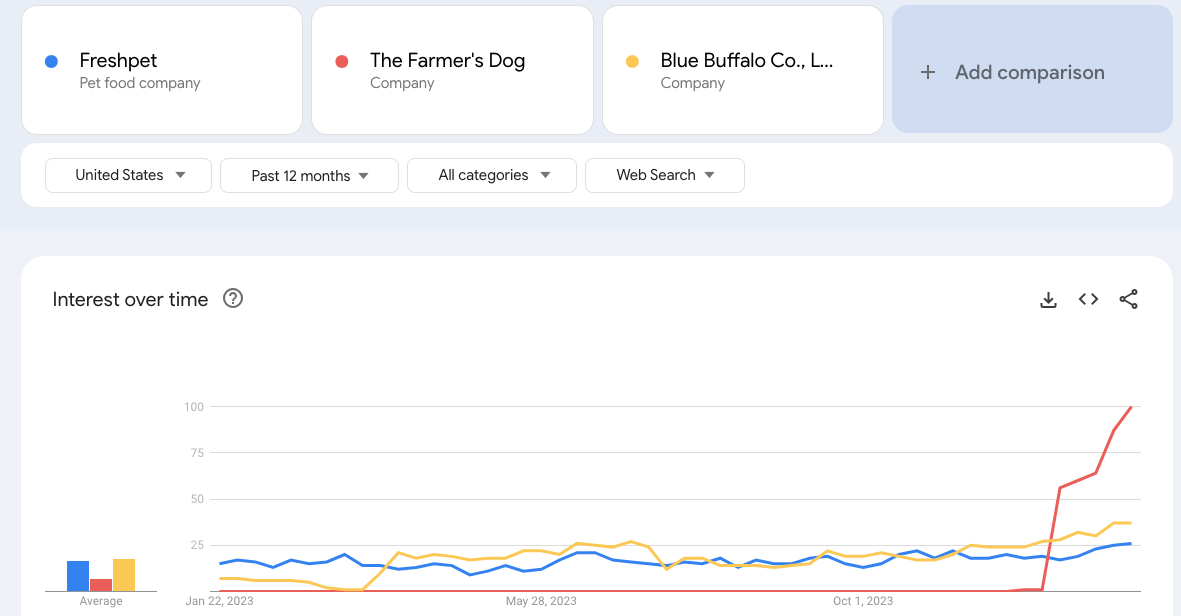

Will Freshpet be able to reach its 2027 goals? Since selling pet food is a commodity business, let’s examine competition. Freshpet’s plan is to justify premium pricing by convincing prospective buyers that Freshpet is better for pet health. This isn’t true. Another problem is that they aren’t the only company making this pitch. Two competitors who also are trying to reach health-conscious consumers are The Farmer’s Dog and Blue Buffalo. Let’s review Google Trends to see which brands are doing a better job at generating awareness.

Google Trends

It's not clear what happened with The Farmer’s Dog in November. What is clear is that Freshpet is not at the top of consumer’s minds when it comes to healthy pet food despite spending untold millions on television ads.

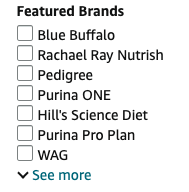

Let’s review top sellers on Amazon to see where Freshpet fits in. Bear in mind, I don’t have a dog so I’ve never bought dog food on Amazon and thus should not have biased results.

Freshpet is not listed above the fold on the featured brands menu:

Amazon

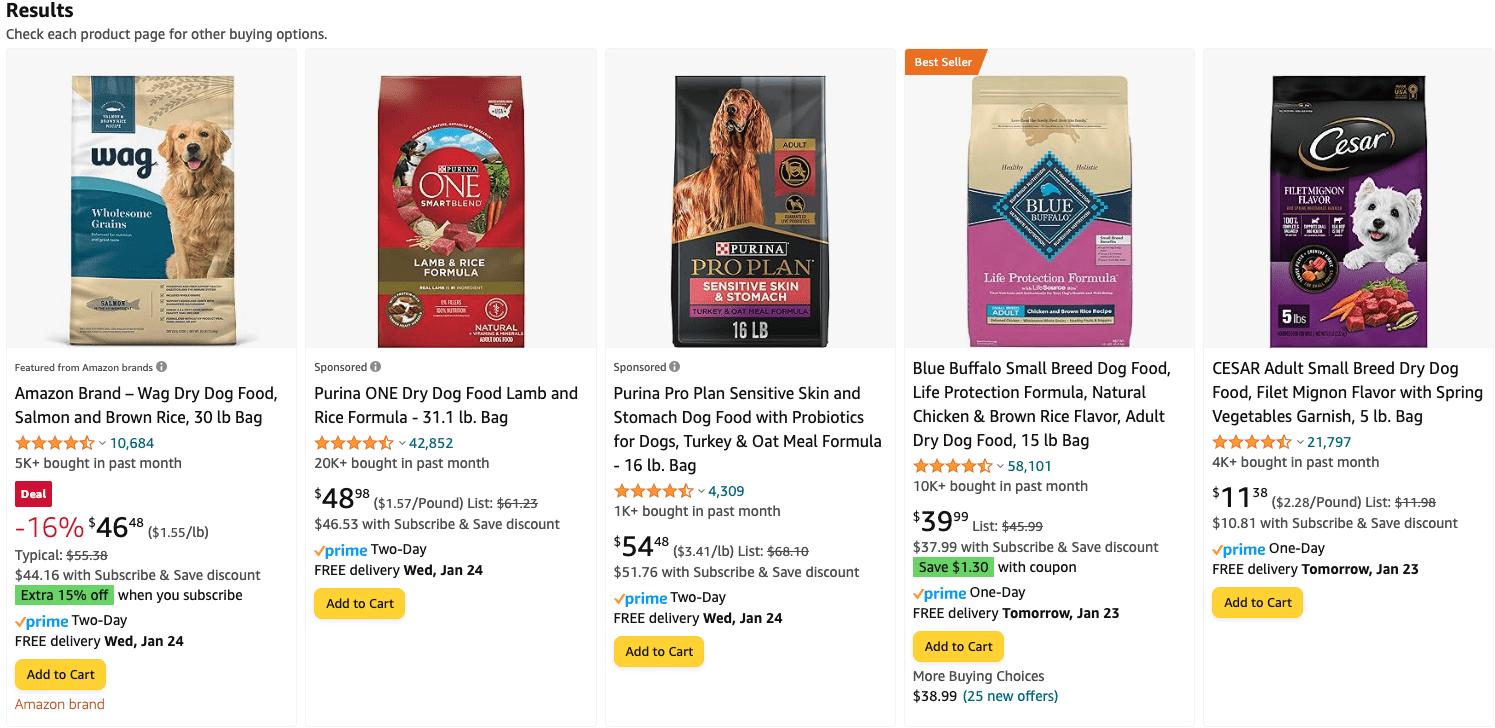

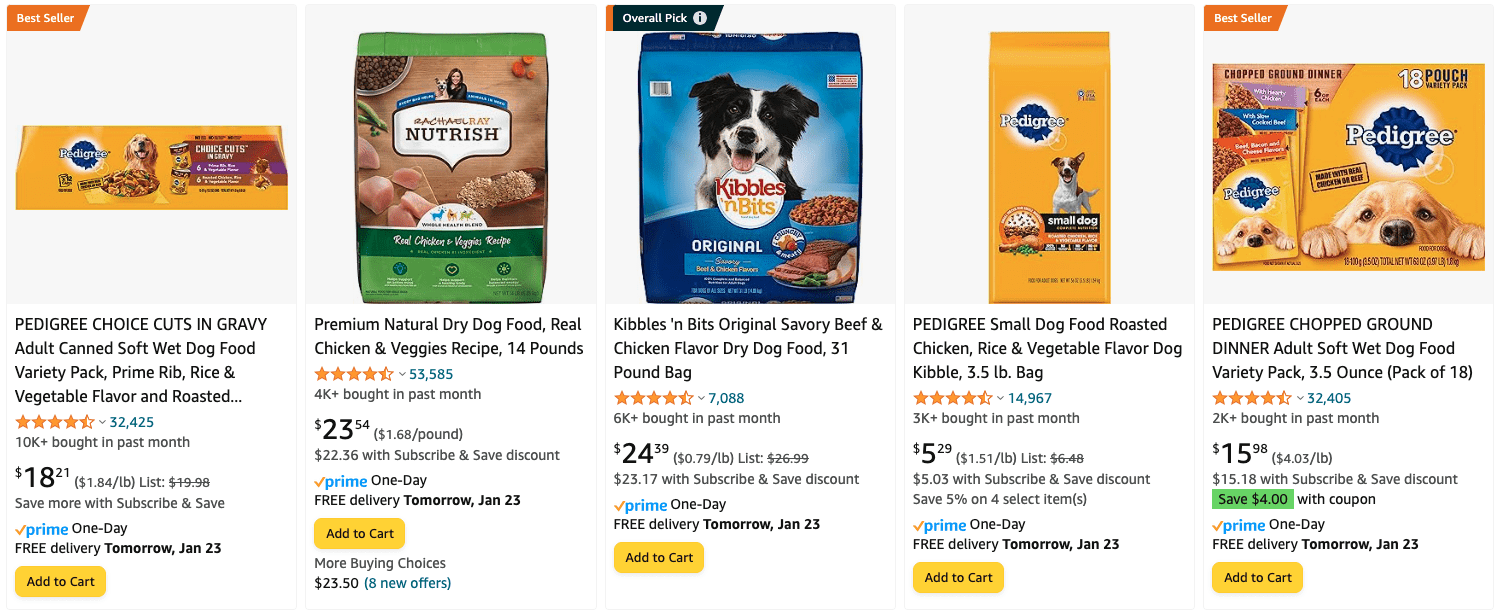

Below is a sponsored ad for Purina, none of the top ten results are Freshpet products.

Amazon Amazon

Let’s compare publicly available Similarweb data to see if Freshpet is successfully creating a brand that can justify premium prices. Here are Freshpet Healthy Dog Food and Cat Food, Fresh from the Fridge’s rankings.

Similarweb

Here are The Farmer’s Dog’s rankings.

Similarweb

Additionally, here is a chart of social media subscribers/followers in thousands for Freshpet and The Farmer’s Dog as of 1/24/24.

YouTube | TikTok | ||

Freshpet | 36 | 40 | 9 |

TFD | 344 | 6 | 145 |

While Freshpet does have a lead on YouTube that appears to be because The Farmer’s Dog has prioritized social media, where they have almost 10x the followers on Instagram and a lot more than 10x the followers on TikTok.

Whether you look at Amazon results, Similarweb data, social media data, or Google trends, it does not appear that Freshpet’s branding is resonating with potential customers.

There are a few key risks to the short thesis.

1. The short interest is already fairly high at 13.6% of shares outstanding. If the company announces good news, these short managers will have to cover and the ensuing buying pressure will force the stock price upwards.

2. Acquisition. The company has dozens of thousands of placements at big-time grocery stores. This real estate is worth something and could result in an acquisition by a large consumer goods company, regardless of the business particulars.

3. Price increases. It is possible that the extremely wealthy cohort of consumers completely buy Freshpet's marketing and will pay any price for their dog food. If the company can raise prices another 25%+ in the next 18 months, it will make accomplishing their goals more achievable.

Freshpet is a product that has no nutritional benefit to dogs, in my opinion. It sells at a premium price point and has not created the brand necessary to legitimize customers paying that much. The firm’s shares sell at a ludicrous premium to likely unachievable 2027 projections. Investors should happily short the shares at the current ~70x 2023 adj. EBITDA price.