helen89

helen89

It’s been a little over seven months since I wrote my cautious piece on Weis Markets Inc. (NYSE:WMK), and in that time, the shares have returned a loss of about 2% against a gain of about 11% for the S&P 500. The company has recently reported annual results, so I thought I’d review the name yet again to see if it’s worth buying or not. In particular, I want to determine whether the shares are relatively more attractive than a risk free investment. I’ll make that determination by comparing the cash flows received by an investor in the stock and the flows earned in the 10-Year Treasury Note. As is frequently the case, I’ll ask the question “at what rate will the dividend need to grow to match cash flows received by the Treasury holder?” My regulars know that I also review the financial statements, and that knowledge creates an expectation, and I don’t feel inclined to subvert that expectation, so I’ll start with a financial snapshot.

My writing can be, uh, “laborious”, what with all the tedious jokes and proper spelling. For that reason, I put a thesis statement at the beginning of each of my articles. This allows investors to get in, get the gist of my argument, and then get out before things become too tiresome. You’re welcome. There’s much I like about Weis Markets. For instance, I really like the very strong balance sheet here. I also like the relatively low payout ratio, suggesting that the dividend is well covered in my estimation. The problem is that I can’t get past the relatively paltry dividend yield. The yield is “paltry” in the context of the 10-Year Treasury Note that is currently yielding north of 4.1%. Thus, on a risk adjusted basis, the Treasury holder does much better than the stockholder in my view. If the yield on the stock rose, and/or the yield on the 10-Year dropped, I would reconsider, but for the moment, the Treasury Note is too compelling to pass up. Thus, in the world of limited capital, I recommend continuing to eschew these shares.

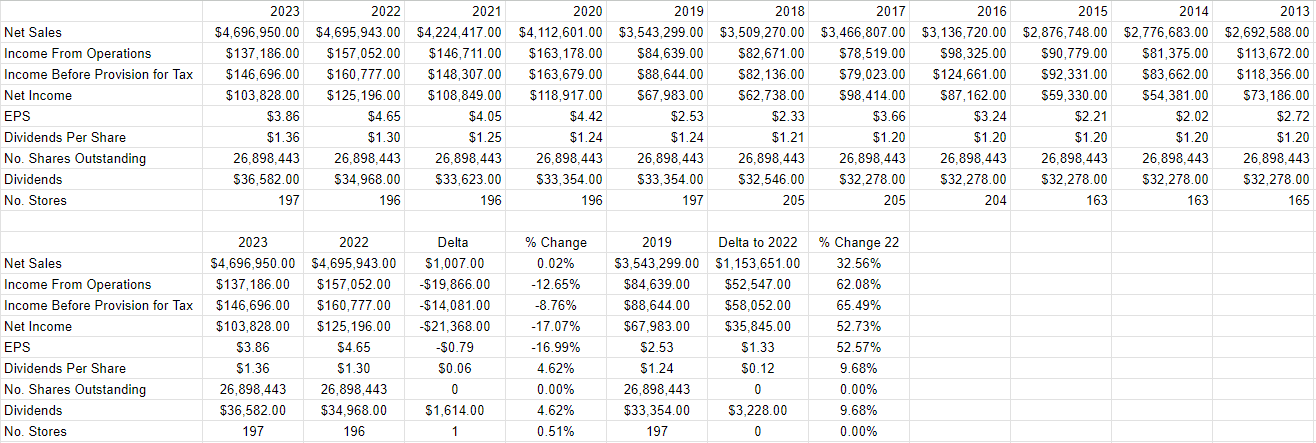

In my view, this is not a growth business, given that revenue in 2023 was up about 0.02% from 2022. Additionally, income from operations, income before tax, and net income were down 12.65%, 8.76%, and 17% respectively, and that’s troublesome. That written, the dividend remains very well covered in my view, with a payout ratio of only about 35%. Add that low payout ratio to the very strong balance sheet (see below), and we have a very strong dividend in my view. I may be hopeful and suggest that it continues to grow.

Turning to the capital structure, the company remains as rock solid as ever. There’s virtually no long term debt here, and cash and marketable securities represents about 62% of total liabilities. That is rare at the moment, and suggests that this business comes with less risk than the vast majority of them at the moment.

Given the strength of the dividend, I’d be happy to buy this stock again if it offers a reasonable risk adjusted return.

Weis Markets Financials (Weis Markets investor relations)

In my view, in the domain of investing, everything is relative. When you put your limited capital to work in “X”, you are, by definition, eschewing any number of “Ys.” I also think investors should seek “risk adjusted returns” and not just “returns.” Given the above, I decided to eschew Weis seven months ago because it was an inferior investment to the 10-Year Treasury Note. The dividend yield was just too low, and an investor could receive greater cash flows from the much lower risk government instrument. Given that yields have backed off a bit, I want to circle back to this, and work out whether or not the 10-Year Treasury is still relatively more attractive than Weis Markets shares. As I promised (or threatened, depending on your perspective), I will compare the cash flows received by shareholders over the next decade to the Treasury Note and copy my results in a handy dandy table for your reading pleasure.

It turns out that in order to match the cash flows earned by the Treasury Note investor, the dividend would actually have to grow at a CAGR of about 14.5% over the next decade from current levels. That’s a rather heavy lift in my view, and significantly higher than the 2.2% dividend growth investors have seen over the past four years.

Weis Markets v Treasury Note (Author calculations)

The challenge for many stocks is that in a world where the 10-Year Treasury Note is yielding about 4.121%. Stocks, even those with growing dividends, often offer lower risk adjusted returns. Although I think there are many positives associated with this business, I think the stock isn’t a worthwhile investment until the 10-Year yield falls, or the dividend yield rises, or some combination of the two.