vchal/iStock via Getty Images

vchal/iStock via Getty Images

On November 11, 2022, exclusively here on Seeking Alpha, I penned my original piece on Encore Wire (NASDAQ:WIRE): They Built A Better Mousetrap.

See below:

Seeking Alpha

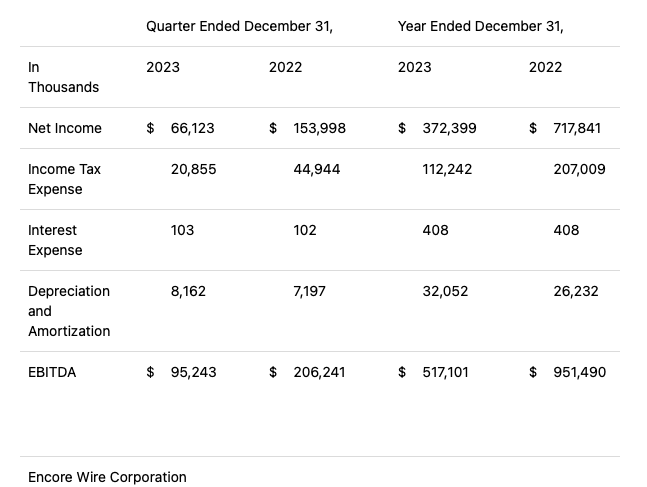

At the time of publication, I provided the then, as in that moment in time, sell side consensus estimates for FY 2023 Adj. EBITDA. At that time, FY 2023 consensus Adj. EBITDA estimates were $418 million. I wrote a fairly in-depth and lengthy piece that focused on the qualitative aspects of the business and highlighted how exceptionally adept this management team was then and remains today. Lo and behold, on February 13, 2024, after the bell, it turns out that WIRE deftly executed the 'high wire act' and posted $517.1 million of FY 2023 Adj. EBITDA.

Encore Wire's Q4 FY 2023 Earnings Report

With the proliferation of online sports betting, notably when it comes to the NFL, you can bet the over or under (on the total number of points scored, in a specific game relative to the Las Vegas line). Well, in that parlance, and in stock market terms, at the specific company level, I bet the 'over' that WIRE would post greater than $418 million of FY 2023 Adj. EBITDA.

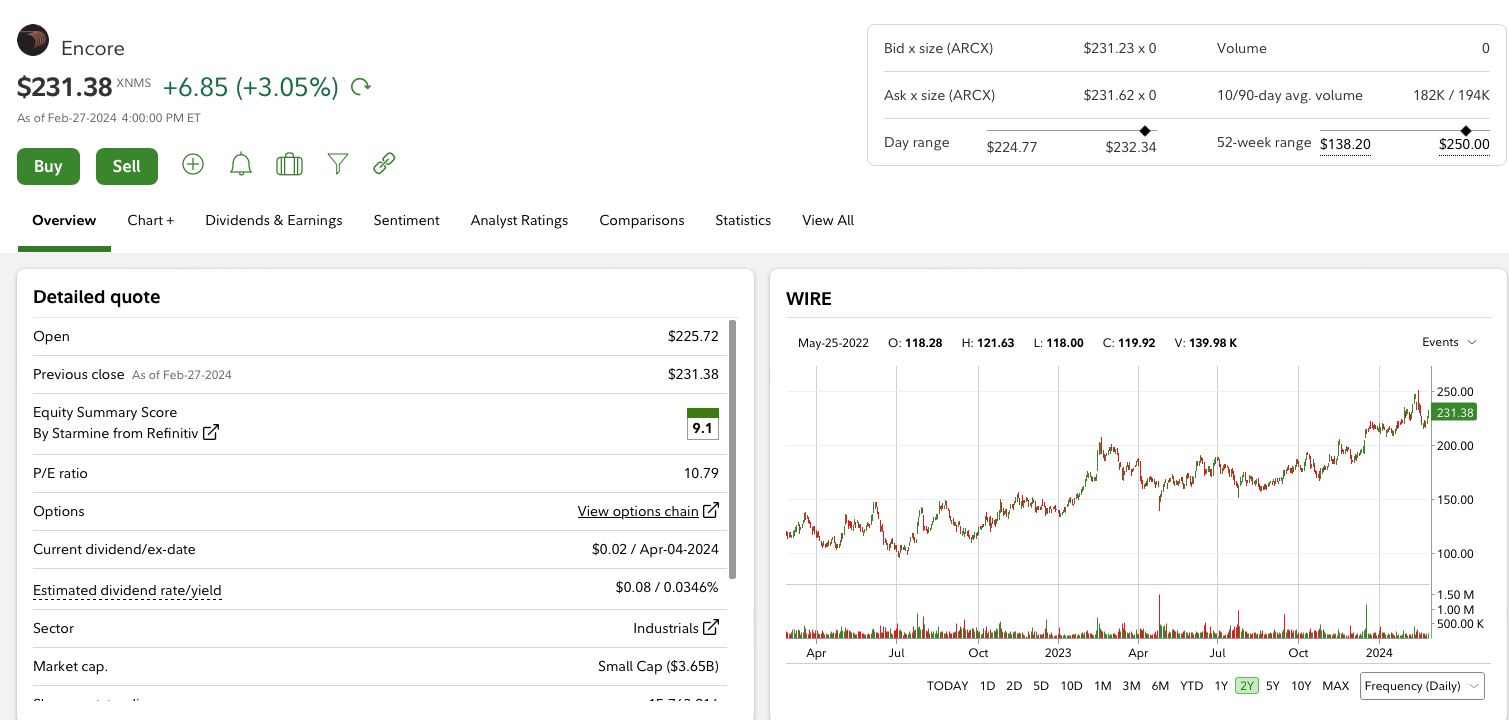

And when a company beats consensus Adj. EBITDA estimates by north of 23% ($517 million of actual vs. $418 million (consensus estimates, as of 11/11/22), you guessed it, the stock price tends to go up. And since I'm in the game of stock picking, we tend to like it when stock prices, at least if we own them, go up. Moreover, it is even better when a good fundamental thesis plays out and the stock price goes up in lock step. Speaking of stock prices, WIRE shares are up 58% since the time of the November 11, 2022 article.

Fidelity

If past history was all that is needed to play the game of money, the richest people would be librarians. (Warren Buffett)

However, as the great Sir Warren Buffett famously said, you can't get rich studying the history of stocks and companies.

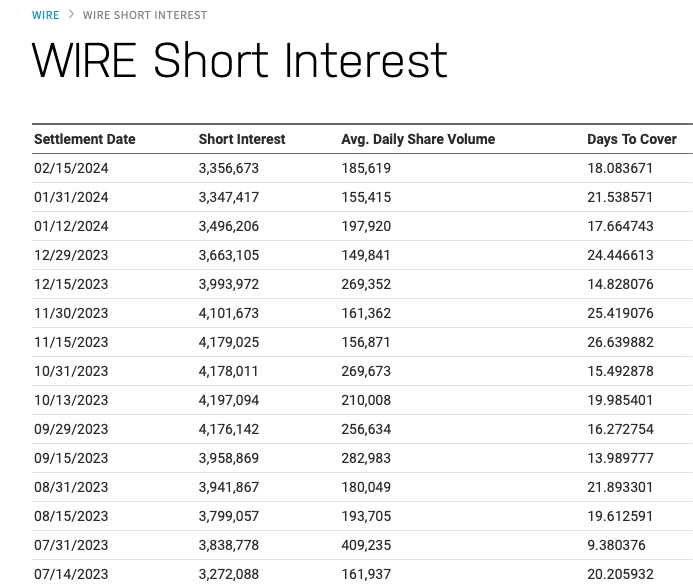

The reason for my updated piece, today's piece on WIRE, is to bring to readers' attention that the shorts are trapped in WIRE. The short thesis has been proven incorrect and yet, quite remarkably, in fact, they are ridiculously offsides and still way too short this company.

As of February 15, 2024, and by the way I intentionally waited for 2/15/24 data to be published, and it was last night, there are still a remarkable 3,356,673 shares of WIRE sold short!

That's simply astonishing!

Nasdaq.com

Let me walk readers through how offsides the shorts are here.

As of February 15, 2024, and per WIRE's FY 2023 10-K, there are 15,763,916 shares of WIRE in existence. Long time and super smart CEO, Daniel Jones, is long roughly 740K shares.

As of December 30, 2023, passive ETF holders, Blackrock Inc., Vanguard Group Inc. and State Street Corp. are collectively long roughly 5 million shares.

So 15.76 million shares - Mr. Jones' 740K shares - 5 million shares held by passive ETFs equals a true float of only 10 million shares.

YahooFinance

According to Fidelity, WIRE's 90-day average volume is only 194K shares. How on God's green earth can you possibly even attempt to cover 3.35 million shares when the true float is only 10 million shares and the stock doesn't trade much average daily volume?

Secondly, and I'm not sure how the shorts didn't work this out, WIRE has generated prolific free cash flow, has no debt, and has aggressively bought back its on stock.

Just to jog market participants' memories, in FY 2023 alone, the company retired 2,661,792 shares. And it gets worse for the shorts. As of February 13, 2024, the date WIRE reported its Q4 FY 2023 results, its Board of Directors recharged its buyback authorization for an additional two million shares.

And guess what?

As of December 31, 2023, WIRE has no debt on its balance sheet and $560.6 million of cash. At last night's current price, $231.38, WIRE has the cash on hand to fully fund this buyback program. That said, realistically, because the float is so small and the stock is (relatively) thinly traded, WIRE's management has executed this buyback methodically and taken advantage of down days and any opportunistic sell-offs, as they are very good allocators of capital and want to maximize their buyback firepower and retire as many shares as possible, at the best and most reasonable price points practical.

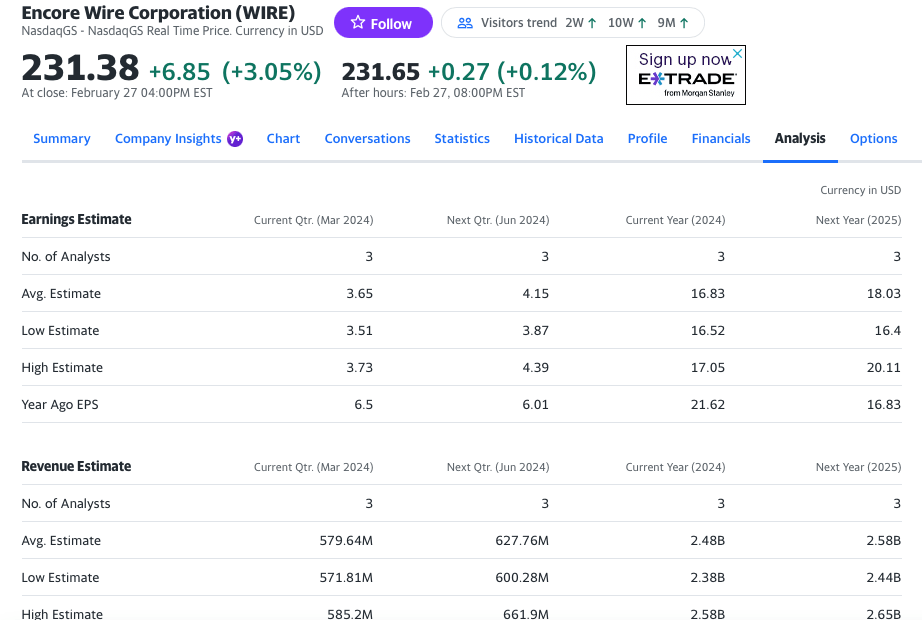

Encore Wire Q4 FY 2023 Earnings Press Release

In FY 2023, WIRE earned $21.62 EPS compared to $36.91 EPS, in FY 2022. As of last night, consensus estimates are calling for FY 2024 EPS of $16.83.

In other words, the stock is currently trading at a P/E ratio of 13.74. And if you closely follow this company then you should be well aware that they never provide forward guidance as copper prices and copper spreads are just too volatile. Instead, management is laser focused on operating its business exceptionally well, controlling what they can control, and blocking and tackling as well as possible within its eco-system of partners (think customers, suppliers, employees, etc.). Like Bill Belichick in his prime, when Tom Brady was wearing number 12 and was a New England Patriot, Daniel Jones and his team are just that good when it comes to this business. Said slightly differently, the shorts must have completely underestimated just how good a 'mouse trap' Jones and his team have built over the span of twenty five plus years.

YahooFinance

Qualitatively, and this is an area where I seem to synthesize a whisker or two better than many market participants, albeit often, and certainly not always, let me quickly explain why it is crazy to be short this company. Again, we already covered the low float of only 10 million shares, the 2 million share re-upped buyback authorization, through 3/31/2025, and that the stock is trading at only 13.74X FY 2024 consensus EPS estimates.

I'm going to distill it down to three critical factors.

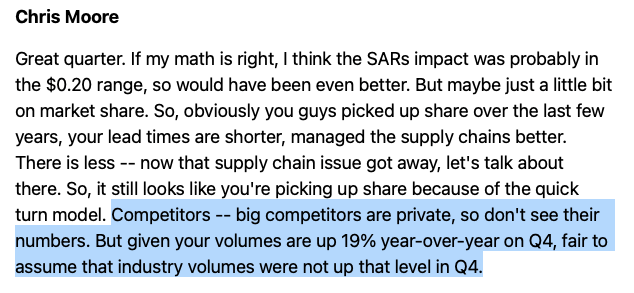

See this analyst Q&A exchange, as it frames the issue nicely.

Here is the analyst's question:

WIRE Q4 FY 2023 Earnings Conference Call Transcript

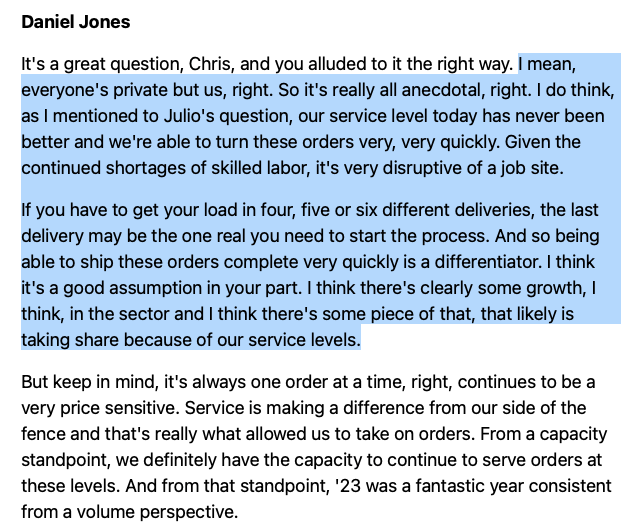

And here is how Daniel Jones answered it:

WIRE Q4 FY 2023 Earnings Conference Call Transcript

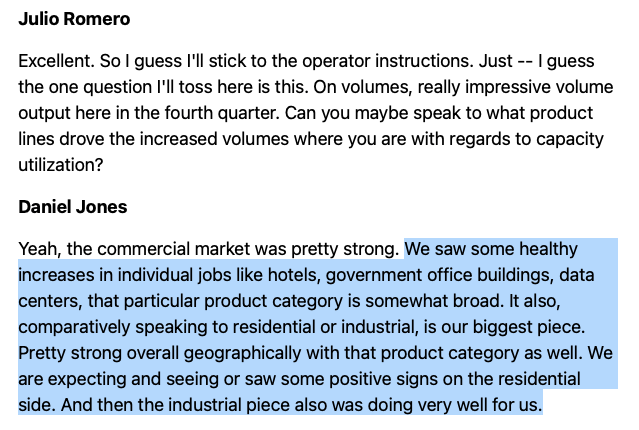

Exhibit A - Growing demand for data centers and renewable energy electrification

We believe our focus on fill rates continues to provide a competitive advantage in the marketplace. We also believe that our one location business model affords us a higher level of agility in adapting to changing market conditions, structuring our operations to quickly service areas of new and growing demand such as data centers and renewable energy, while servicing our core market segments.

As noted above, demand for our copper wire and cable products remains strong in 2023 and our build to ship model combined with the throughput of our modern service center positions us well to compete for future demand. We believe that we have made and will continue to make appropriate, sustainable investments to meet future demand, will facilitate the broad electrification of our economy.

Additionally, we believe that the current federal legislation providing funds for the infrastructure needed for broad electrification should bolster demand for our products. We firmly believe that our historical, recent and future success is a direct reflection of our unique culture and the strength of our experienced team. We also believe that our one campus location, deep vertical integration, strong supplier and customer relationships and our ability to quickly shift complete orders will remain critical differentiators in our future success.

(Source: WIRE Q4 FY 2023 Conference Call)

Exhibit B - WIRE's cross-link polyethylene XLPE compounding facility came online in Q4 FY 2023

In 2022, we began construction on a cross-link polyethylene XLPE compounding facility to deepen vertical integration related to wire and cable insulation. XLPE insulation is used in many applications, including data centers, oil and gas, transit, wastewater treatment facilities, utilities, and wind and solar applications. As Daniel mentioned, the new facility was substantially completed in the third quarter of 2023.

(Source: WIRE Q4 FY 2023 Conference Call)

Exhibit C - Across the board demand strength and even residential (usually 25% to less than 30% of overall revenue is showing green shoots)

WIRE's Q4 FY 2023 Earnings Transcript

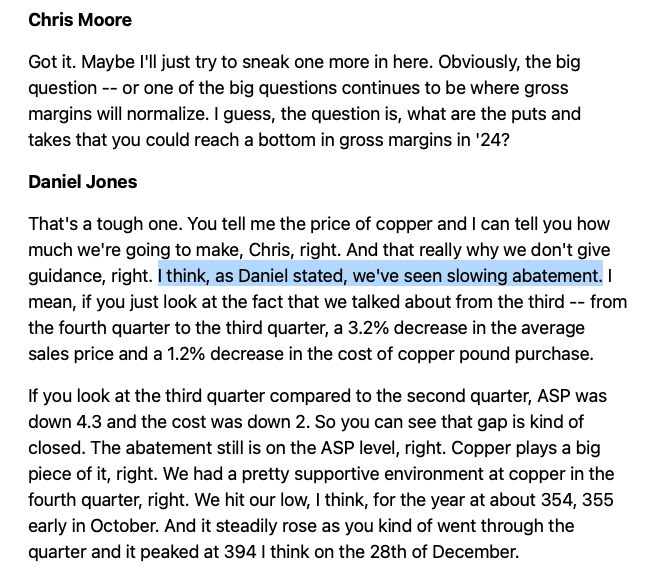

Exhibit D - The copper market is incredibly tight (only 3 days of physical supply). This bodes well for (relatively) stable/ higher copper prices

Other than all the hype and the talk that goes into the political atmosphere, we have no control over whatsoever. The things that we have to say in right now Julio, I think we've got a pretty good handle on. We've got the right guy or the right girl with backups in each spot. And the momentum that you were talking about in '23 for us anyway certainly has not been a let up starting off this year. We're just anxious to see where this copper thing ends up. Super tight.

Around three day’s supply above ground in the world. It's an incredibly tight situation, It's fun. It's a robust market. We're having a lot of success with our partners and we've got a great team around us in all aspects and we'll see where this takes us.

WIRE's Q4 FY 2023 Earnings Conference Call

It is truly astounding how offsides the shorts are here, short over 3.3 million (as of February 15, 2024) shares, which is roughly 33% of the true float, for a company with only a 194K 90-day average daily volume. WIRE's true float, net of passive ETF holders and CEO, Daniel Jones, and his stake, is only 10 million shares. WIRE has a recharged 2 million share buyback authorization, and they have been consistent and aggressive buyers of their stock. Despite all of the badly misplaced and bearish mean reversion, macro fears, and other misperceptions, WIRE is the little engine that could. The company has no debt and trades at a P/E of less than 14X.

If people that actually dig in or that get in the weeds and that do real fundamental work then they will quickly work out that copper spreads (the inherent gross margins between the price of commodity and WIRE's realized finished good selling price) peaked in 2021. Despite copper spreads contracting from those nose bleed levels (record gross margins), WIRE has taken material market shares and grown its volume nicely. Look no further than its recent 19% volume growth, in Q4 FY 2023. What are the shorts thinking after seeing those market share gains?

Think about it - when you are taking a lot of market share, this is the most compelling testament to the strength/quality of your business relative to your peer group. WIRE isn't competing on price per se. Yes, they have been in the ball park of price, but the secret sauce is having the industry's best service levels, the ability to fulfill upper 90% of all taken orders and on a coast to coast basis, and in the shapes needed for a diverse set of end demand markets.

Simply put, I'm upping my price target to $300.