Wirestock/iStock via Getty Images

Editor's note: Seeking Alpha is proud to welcome Counterflow Capital as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Wirestock/iStock via Getty Images

Wingstop (NASDAQ:WING) has seen tremendous growth out of the back-half of 2023, consistently beating earnings while establishing a strong brand name with low operational costs. Despite the success, WING is now priced at extremely high valuations: 23x sales, 150x earnings, and 83x EBITDA. The sustainability of these multiples is clearly unrealistic, especially considering its position within a highly competitive and saturated market. If management even slightly lowers guidance or they miss earnings, I expect a significant negative price response. Given these factors, I recommend selling Wingstop shares with a price target of $270 indicating a potential 28% downside.

Wingstop operates as a fast-casual franchise with a global presence, including 1,877 locations in the US, 288 internationally, and 49 company-owned stores. This structure supports an asset-light business model, though it depends heavily on franchisee performance. Franchisees are required to pay an upfront fee of $30,000 ($10,000 development + $20,000 franchise), alongside 11.3% of gross sales as royalty (6% for sales and 5.3% for an advertising and technology fund). Despite the minimal staff requirement (4 per store), thanks to a digital-first approach, the menu remains small, with only wings, tenders, sandwiches, and fries. On a financial level, 2023 system-wide locations brought in $3.5 billion in sales with $460 million attributable to Wingstop.

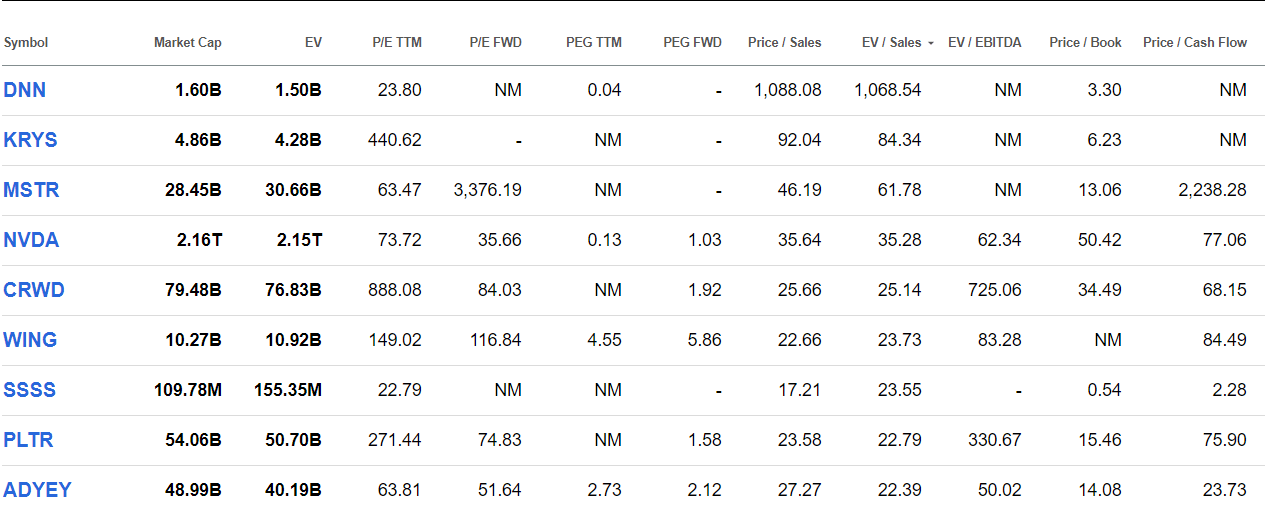

To understand Wingstop's positioning, we can start with Seeking Alpha's stock screener. On a screen that includes coverage by SA and Wall Street analysts, I sorted high-to-low by price-to-sales ratios. I used this multiple because of Wingstop's high growth and position within the consumer space. Excluding the skewed results and differentiated industries (i.e. biotech), the first notably firm that appears is Nvidia (NVDA). The current leader of AI is trading at 35x sales, 73x earnings, and 60x EBITDA. Moving further down we see fintech leaders like Adyen (OTCPK:ADYEY), cloud leaders including Cloudflare (NET), and of course Palantir (PLTR). Then, we have Wingstop, a company that sells wings, trading at 23x sales, 150x earnings, and 84x EBITDA. This positions it at higher multiples than Snowflake (SNOW), Mastercard (MA), and ServiceNow (NOW). If we move down to the restaurant level, the next closest comps are McDonald's (MCD) and Chipotle (CMG). MCD trades at 8x sales, 25x earnings, and 19x EBITDA, then CMG trades at 8x sales, 60x earnings, and 40x EBITDA. Even on a growth-adjusted basis WING trades at a premium to not only the fast-casual space, but even leading technology companies.

High-Low P/S w/ positive P/E (Seeking Alpha)

Now that you understand Wingstop's AI level valuation, let's try to understand why. Starting with expectations, since Q2 2022 WING has double beat earnings every time, by a significant deviation. This has led to a ~320% return over the period vs the S&P at just ~31%. Still, analysts remain relatively bullish with 8 strong buys, 14 holds, and only 1 sell.

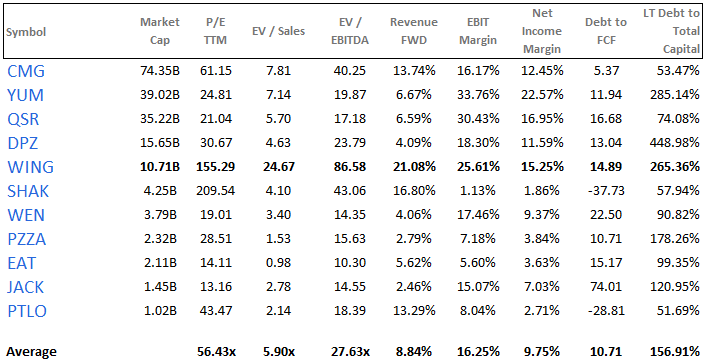

Next, we can look at consensus over the next three years compared to the last three. On the top line, the street is forecasting sales of $727 million by 2026, implying a CAGR of ~16%. Over the last three years the CAGR was ~22%. Looking at operating margins, they dropped from 26.11% in 2021 to 24.47% in 2023 and are forecasted to expand to 27.53% by 2026. EPS is expected to grow at a CAGR of 22% entering 2026 vs. 44% over the previous three years. Looking across the industry, average sales growth for 2024 is expected to be ~8.84%. Then looking at high-growth players, Shake Shack (SHAK) is expected to see 16.80% and Chipotle is expecting 13.75%, vs Wingstop at 21.36%. Financially WING has remained strong, it's been able to grow while keeping costs down, a difficult challenge as a discretionary company.

Despite this optimism, the sustainability of Wingstop's high valuation is difficult to defend, particularly considering potential expansion challenges. Comparatively, Wingstop's menu diversification and TAM fall short against large-players like Chick-fil-A, Chipotle, and KFC. The focus on a niche market without broadening its menu through different offers limits its growth potential and exposes it to market cannibalization and intensified competition.

Wingstop has been targeting higher income demographics yet lacks evidence to show these customers will continue returning. The specialized nature of its menu restricts TAM growth, as consumer preference for diversification in fast-casual dining is a standard. Industry leaders highlight a trend towards menu variety as a key factor in attracting a wider audience. In contrast, Wingstop's focus remains narrowly on wings, which will lower its ability to compete effectively with more diversified chains. From a consumer perspective the main reason to choose Wingstop is wings. Until they prove significant penetration in the chicken sandwich and tender market, they remain highly levered toward consumer preference. Furthermore, looking to Wingstop's main customer base, we know the NFL is one of the main drivers of wing consumption. This most likely means the main demographic is lower income males aged 25-55, equating to about ~50 million or ~15% of the US population. While a generalization, it highlights the realistic nature of the TAM which lacks high-income consumers and females. Other players like Chipotle and Chick-fil-a have more diversified menus, healthier options, and better service. This means their TAM is significantly higher, creating a more maneuverable business model.

Wingstop's strategy of rapid expansion alongside a lack of menu diversification presents risks of cannibalization, particularly in saturated markets. Data from the fast-casual sector indicates brands with broader menus tend to perform better in terms of market penetration and customer retention. For example, chains like McDonald's and Chipotle report lower instances of cannibalization due to their ability to appeal to a wider range of consumers. In contrast, Wingstop's limited menu offerings may lead to self-competition as it expands, potentially diluting brand value and lowering returns at new locations. This issue was recently seen in Shake Shack during early 2020. It's challenging to determine the exact tipping point, but it seems that Wingstop is approaching it. Presently, Wingstop has 1,877 stores in the US, while Chick-fil-A and Chipotle have approximately 3,000 and 3,300 locations, respectively. With an anticipated consensus store expansion rate of about 12% per year, Wingstop is projected to reach the 3,000 store mark within the next 3 to 4 years. This level of growth raises concerns about the feasibility of expanding without encountering significant competition and potential cannibalization.

The catalyst behind my thesis is likely going to be from a shift in earnings expectations or challenges during periods of rapid growth. First, looking at the macroeconomic environment, we have only been in a period with the FED funds rate above ~5% for a year. While consumers have remained resilient, any emerging vulnerabilities in the data could lead to a significant drop in Wingstop's stock price.

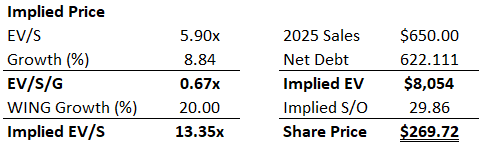

For relative valuation I analyzed a set of 10 similar fast-casual restaurant chains and chose to focus on EV/Sales. Considering revenue as a primary driver and discrepancies in debt use, I felt this ratio was optimal. Additionally, I applied a growth adjustment reflecting the expected comparable company growth for 2024, so an EV/S/G ratio. Including Wingstop in this average calculation inflates the figure further, allowing more room for error. The average EV/Sales ratio was calculated at 5.9x, with a forward revenue growth expectation of 8.84, implying a multiple of 0.67. Considering consensus revenue growth of approximately 20% for Wingstop, this results in an EV/Sales multiple of 13.35x. Then based on projected 2025 sales of $650 million, this implies a share price of $269.72, indicating a potential 28% downside. Moreover, when comparing to 5-year multiple averages, Wingstop still continues to trade at a premium of 20%-40%.

Seeking Alpha

Excel Calculation

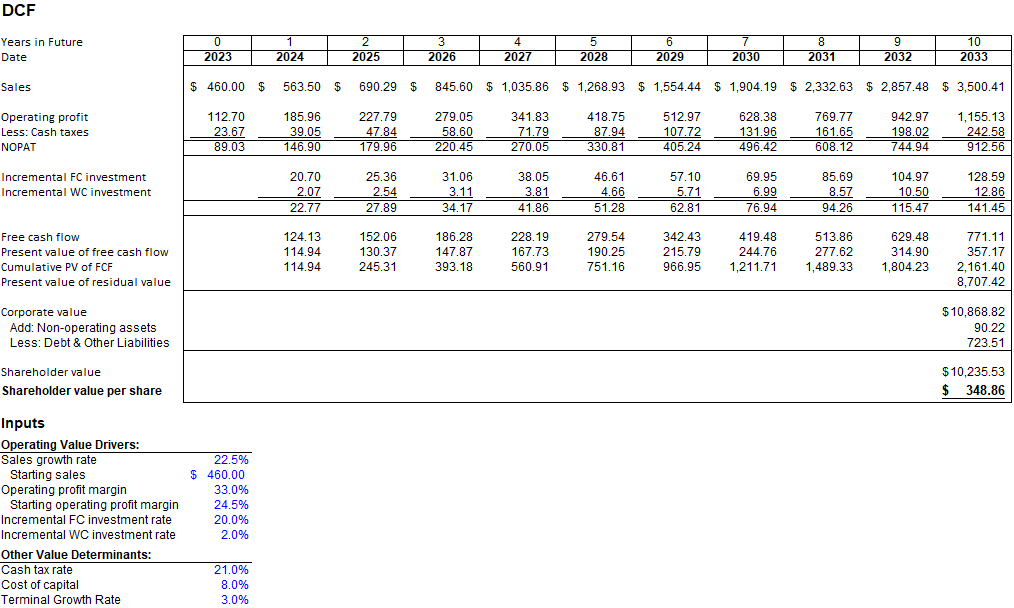

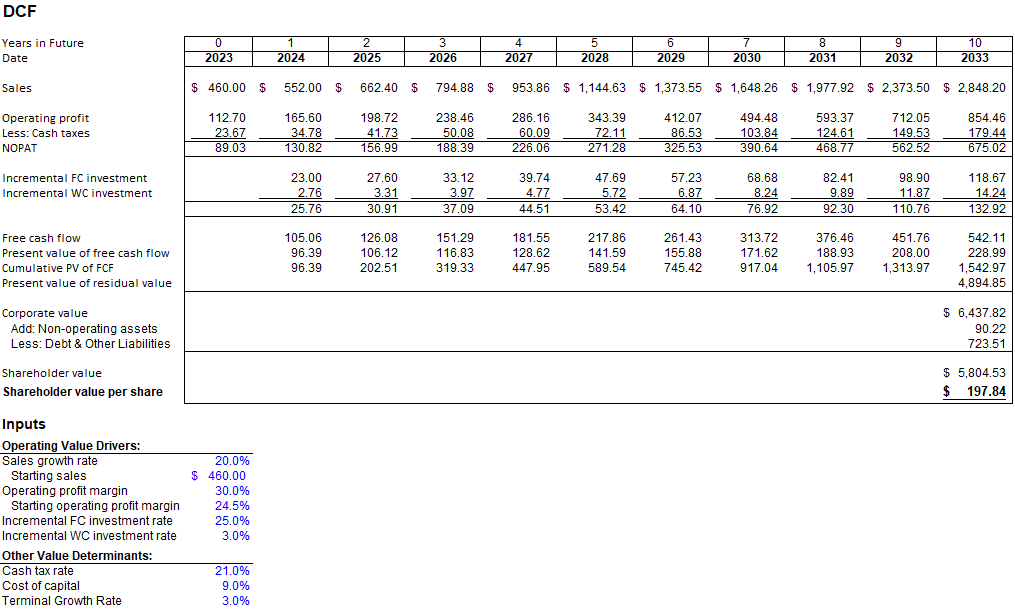

For intrinsic valuation I built two DCF models, one to justify the current stock price and another that presents a more realistic scenario. To support the current share price of $350, the DCF analysis assumes bullish inputs, including a cost of capital of 8%, a terminal growth rate of 3%, a CAGR for revenue of 22.5%, and long-term operating margins of 33%. These assumptions are extremely optimistic, but necessary to sustain a share price of $350. Transitioning to the DCF I consider more plausible involves having 20% revenue growth over ten years, a 30% operating margin, a 9% discount rate, and a 3% terminal growth rate. This approach yields a share price of $197.84, suggesting a potential downside of 43.47%.

Despite the numerous arguments behind using DCF models, they provide insight into the necessary financial performance inputs to justify current stock valuations. The analysis implies that maintaining a $350 share price demands consistent outperformance. Any deviation, such as an earnings miss or a change in management guidance, could lead to a significant price correction. Furthermore, even my plausible case remains extremely bullish, especially when considering sustainability for 10 years.

(It's worth noting that due to Wingstop's franchise-based business model, the requirement for capital reinvestment is minimal)

Current Price DCF Assumptions (Excel DCF)

Realistic Price DCF Assumptions (Excel DCF)

The main risks associated with my thesis is continued and consistent financial outperformance. If Wingstop continues to double-beat earnings and meet their guidance targets, the stock will continue to trade at an elevated valuation. Additionally, management has outlined clear plans to expand internationally, and if successful I see further price support. Finally, there's a possibility that wing consumption drastically increases, and consumers begin going to Wingstop for items beyond just wings. The market clearly views Wingstop as a great company, and there is a chance shares will remain inflated for the foreseeable future.

Despite Wingstop's consistent outperformance I see no reason for the valuation to remain elevated. Even if the company meets current expectations, I still see market correction reverting shares to a more reasonable growth-adjusted multiple. On a fundamental level, it's clear Wingstop has an inherently small TAM due to a lack of menu diversification and specific brand-focus. The fast-casual industry remains highly competitive with many large players that retain strong brand loyalty and have more menu options. In terms of catalysts, it will most likely stem from a change or miss in expectations alongside further expansion issues. In summary, if any cracks begin to form, I see significant potential for Wingstop Shares.