stoickt/iStock via Getty Images

stoickt/iStock via Getty Images

Western Midstream Partners, LP (NYSE:WES) has outperformed the market by roughly 50% since we recommended it last November. The company has worked hard to continue executing its thesis, but its share price has benefited from rumors of a potential sale. As we'll see throughout this article, even if these rumors don't pan out, the company has the ability to drive strong returns.

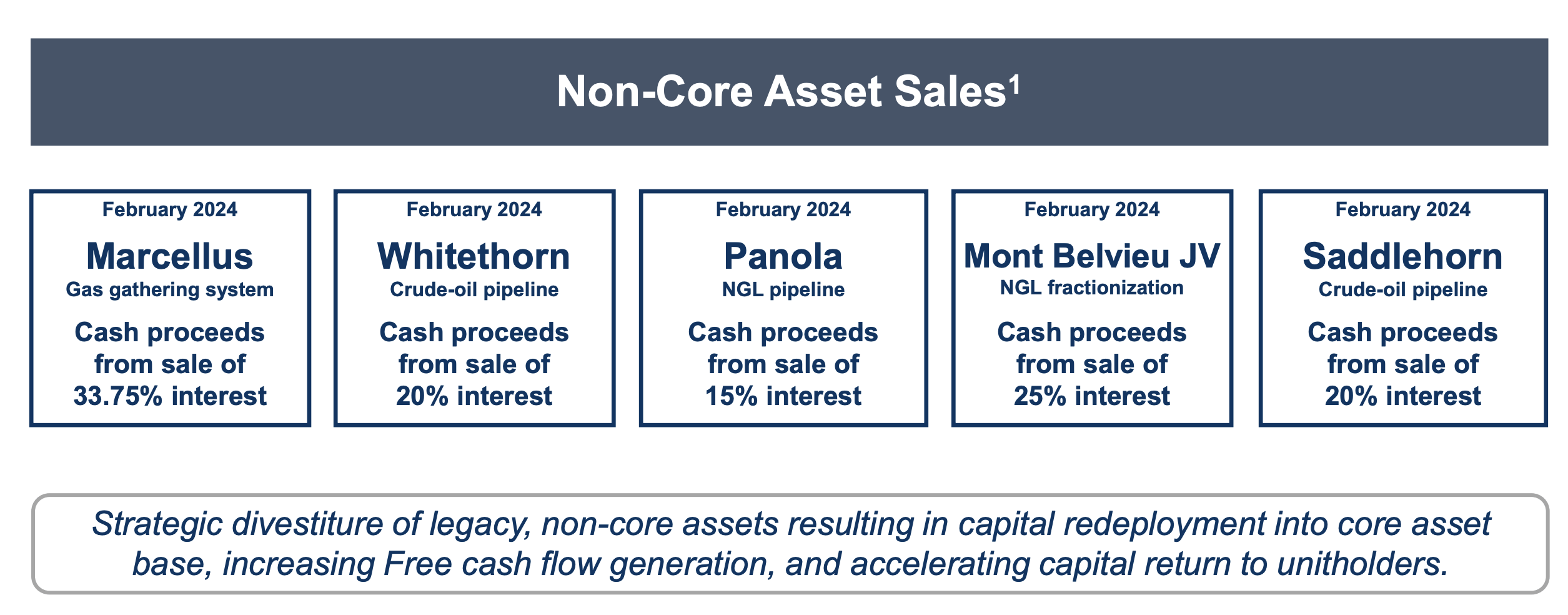

The company has started some non-core divestitures to increase the overall value of its assets.

Western Midstream Investor Presentation

The company's non-core asset sales have enabled it to raise almost $800 million as it sells non-controlling stakes. The company is redeploying this capital and given its large current size, we expect it to continue to look at strategic divestitures such as these. The company's strong history of unit repurchases also reenables it to leverage this cash received.

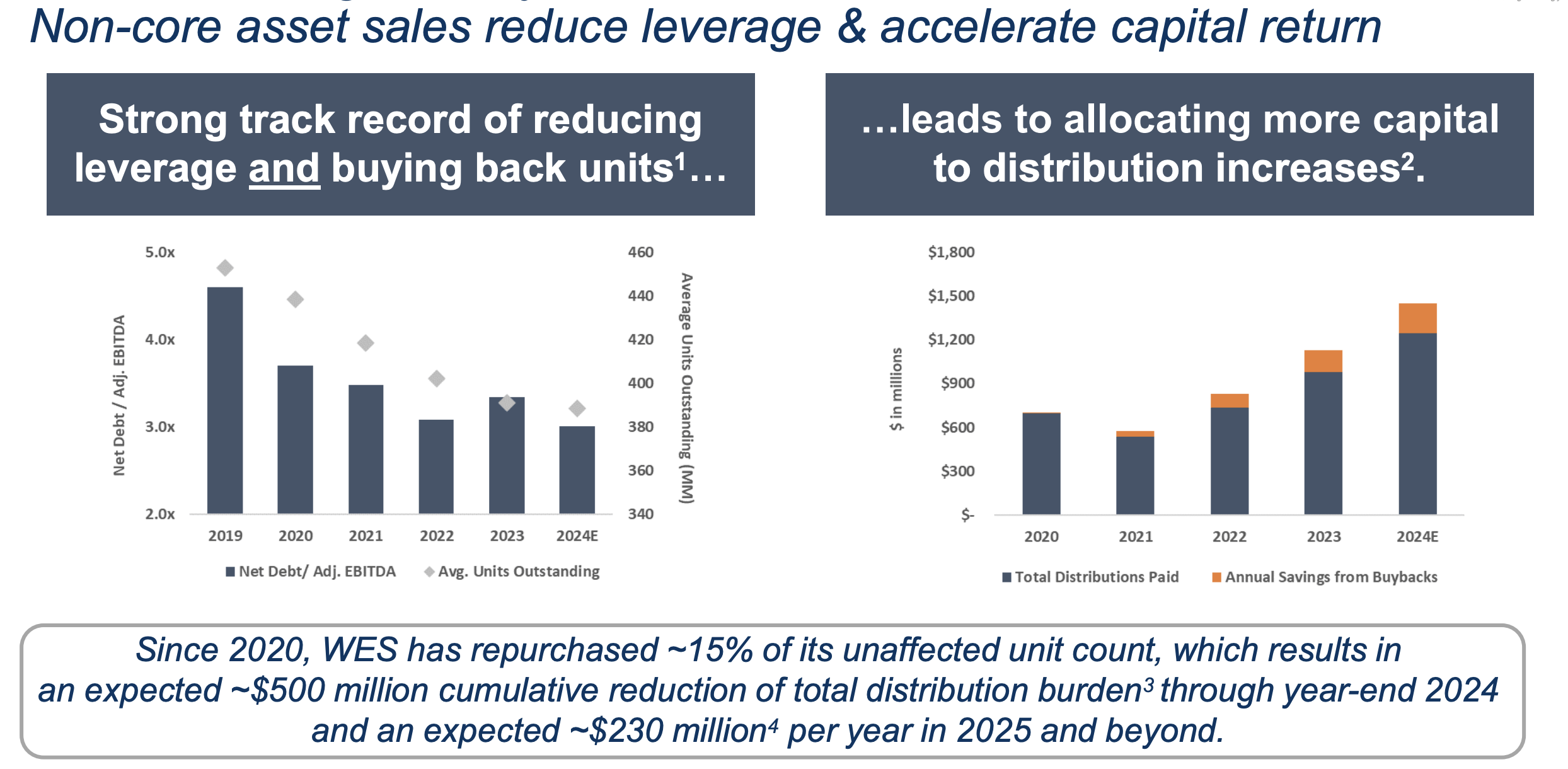

The company's focus has been on increasing return through shared buybacks, something that we think other midstream companies should focus on.

Western Midstream Investor Presentation

The company has managed to consistently reduce its leverage, and now has its net debt to adjusted EBITDA sitting at 3.0x, a level that's very comfortable for a midstream company given the reliable cash flow. That has enabled the company to put more cash towards share buybacks, and since 2020 it's repurchased a massive 15% of its unaffected unit count.

Those benefits add up, with the company's dividend savings so far at $500 million and expected to be at $230 million / year from next year onwards. It enables the company to give a higher yield at the same amount of cash outwards, while it continues share repurchases. The company's focus on overall shareholder returns is important.

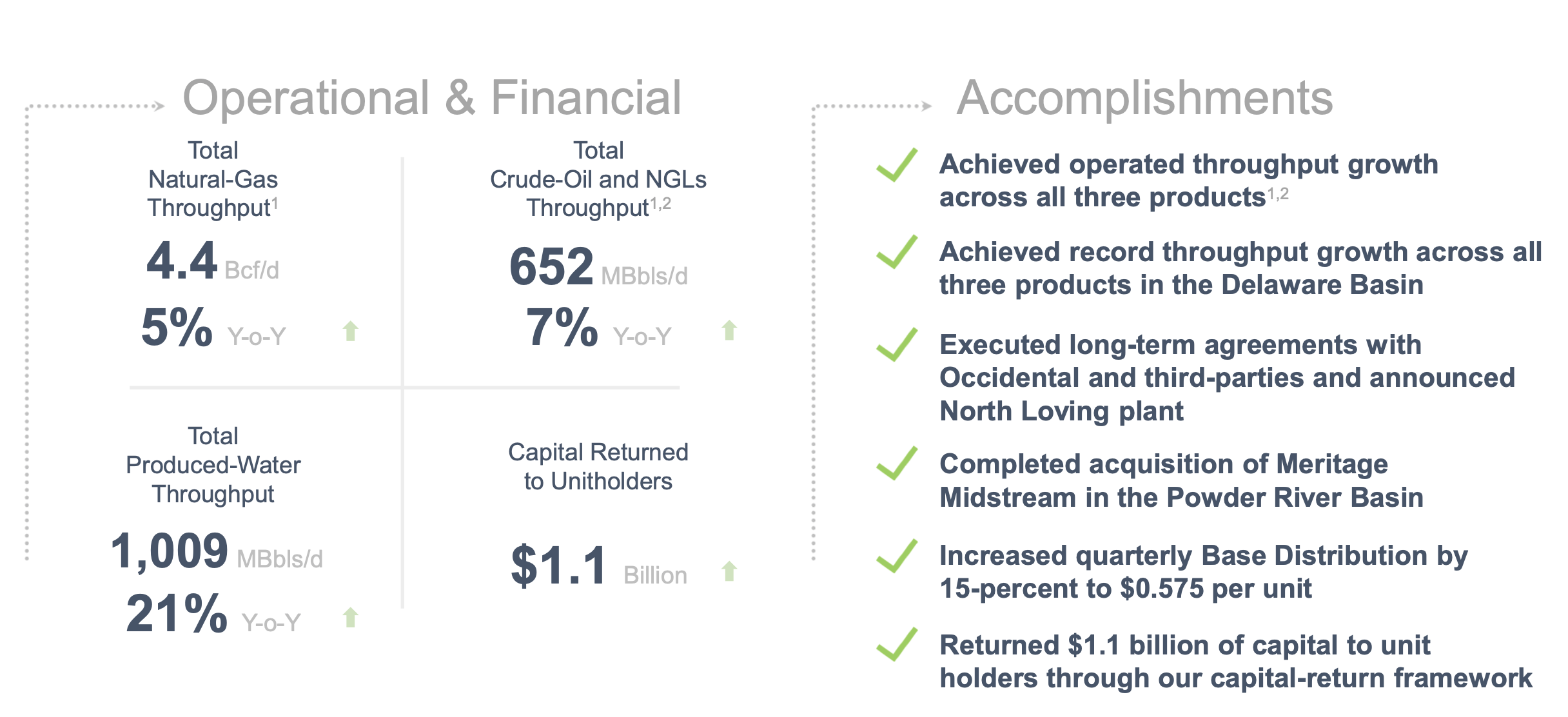

The company had an incredibly strong 2023, maintaining strong utilization in its asset portfolio.

Western Midstream Investor Presentation

The company's strong utilization has come with 4.4 Bcf/d of natural gas throughput, up 5% YoY. The most profitable, crude oil and NGL throughput increased 7% YoY to 650 thousand barrels / day, and produced water increased a massive 20% YoY to more than 1 million barrels / day. The company returned $1.1 billion in capital at a more than 8% return rate.

The company has also increased its dividend, pushing an almost 7% yield. That, combined with share repurchases, pushes an almost double-digit yield.

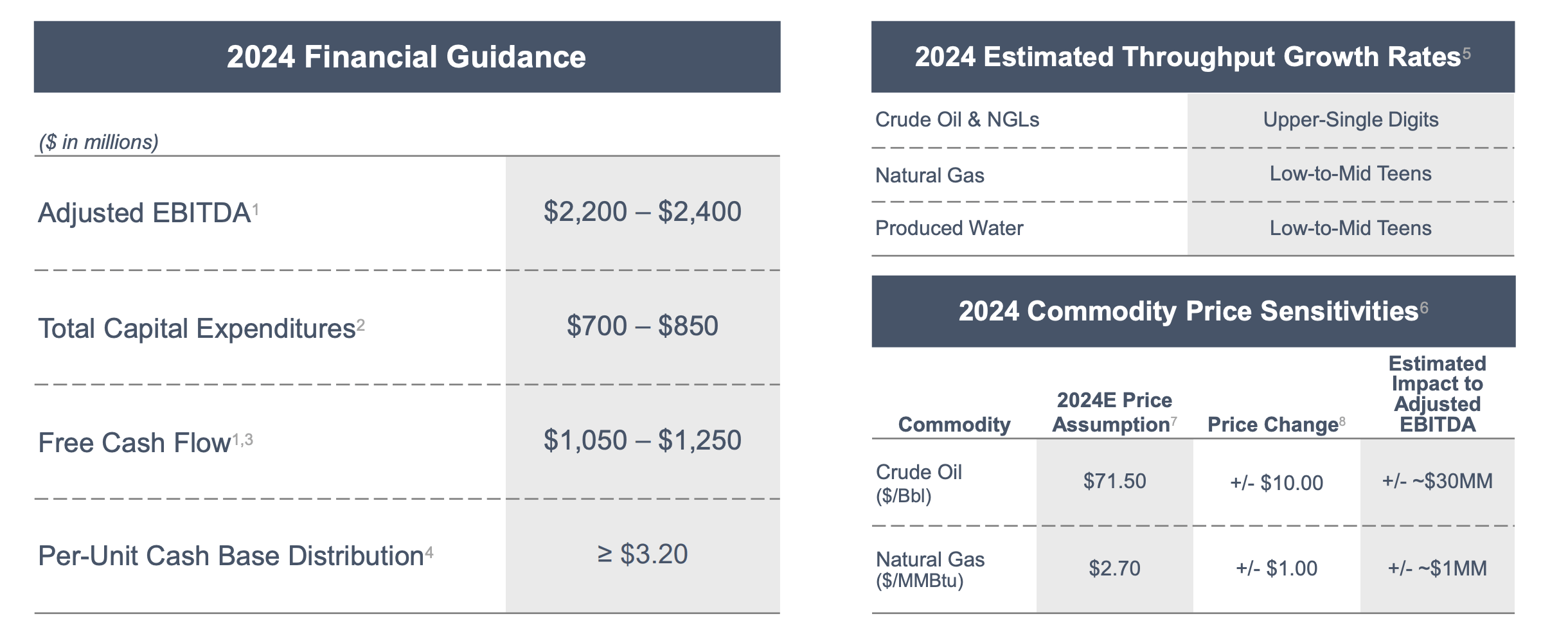

The company's outlook for 2024 shows solid growth and continued shareholder returns.

Western Midstream Investor Presentation

The company expects $2.3 billion in adjusted EBITDA, a double-digit increase from 2023, where the company went above the top-end of its guidance. The company expects ~$775 million in capex and $1.15 billion in free cash flow, or FCF. That's again a double-digit increase in FCF, which can help even higher returns for shareholders.

All of this is backed by double-digit growth rates in natural gas and produced water volumes and almost 10% growth in crude oils and NGLs. The company's cash flow is remarkably reliable. The company's base distribution will be almost 10%, and we expect the company to both pay its strong dividend and repurchase shares.

Another interesting dynamic for the company in 2024 is the potential for an acquisition. Occidental Petroleum has an almost $7 billion stake in Western Midstream that's down to a yield of just under 7%. The company has recently taken on some additional debt with the CrownRock acquisition, and in a higher yield market, selling this stake might be tempting.

Midstream companies looking to grow might jump on the opportunity to purchase a 50% stake in a large midstream company. This could lead to some volatility in share price, but also some growth.

The largest risk to the thesis in our view is that the company is still effectively a subsidiary of Occidental Petroleum. What happens to that stake remains to be seen, but the public nature of Western Midstream means it's consistently turned too as a way for Occidental Petroleum to raise cash. The risks of that can manifest in a tough market, if Occidental Petroleum needs to sell the stake for cheap.

Western Midstream has a massive portfolio of assets. The company has seen its share price outperform by focusing on what it does well, repurchasing shares, paying a strong dividend, and continuing to grow. It's rare to see a company that can pay almost 10% in direct shareholder returns, and still achieve double-digit YoY growth in FCF and earnings.

The company has already shown a proven ability from its cash flow to repurchase shares and drive long-term value. The Occidental Petroleum stake sale could provide additional immediate volatility and returns, but overall we expect it to not change the fundamental thesis around Western Midstream Partners, LP's strength and investment opportunity.