Thossaphol

Thossaphol

It's been over two years since I last covered WEC Energy Group, Inc. (WEC) when I compared it to my two long-term utility picks, The Southern Company (SO) and Duke Energy Corp. (DUK). Back in November 2021, interest rates were still extremely low and WEC stock was trading at around $90, which at the time equated to a dividend yield of 3.0% and an enterprise value to EBITDA (EV/EBITDA) multiple of 17.2 - quite expensive for a utility, despite its high quality and solid long-term earnings and dividend growth.

My regular readers know that I am not a particular fan of investing in utilities (IDU), mainly because of their huge capital expenditure and associated high debt levels (see this article). Given the transition to a "greener" energy mix that requires significant additional investments, it's easy to see why utilities may not be the best investment going forward, at least from a shareowner's perspective. Of particular note is the fact that utilities typically do not generate free cash flow. However, it can be argued - rightly in my opinion - that some of the capital expenditure is attributable to growth and not maintenance-related investments.

Nevertheless, I think that in a broadly diversified and income-oriented portfolio, a small allocation to high-quality utilities can make a lot of sense, as long as their shares are bought at reasonable valuations and held for the long term. So far, I have been happy with the performance of my investments in SO and DUK, but I always found WEC too expensive.

Today, WEC stock is trading for $80 a share, which suggests that it is only slightly cheaper today, but keep in mind that the utility's earnings and dividends have increased substantially over the past two and a half years. While the stock is only $10, or 11%, cheaper than when I last covered WEC Energy Group in detail, it has become a considerably better deal from a dividend yield and earnings perspective: WEC stock hasn't been this cheap in ten years.

So in this update, I will explain why I recently opened a position in WEC common stock and immediately brought it to the size of my DUK and SO stock positions in terms of invested capital. While I will touch on WEC's operations in this article, those interested in an overview of WEC Energy Group and a comparison with SO and DUK should take a look at my in-depth article linked above. However, in addition to the main reasons why I recently added WEC to my dividend stock portfolio, I will take a fresh look at the company's energy mix and discuss its current leverage - after all, utilities are known for their high debt levels.

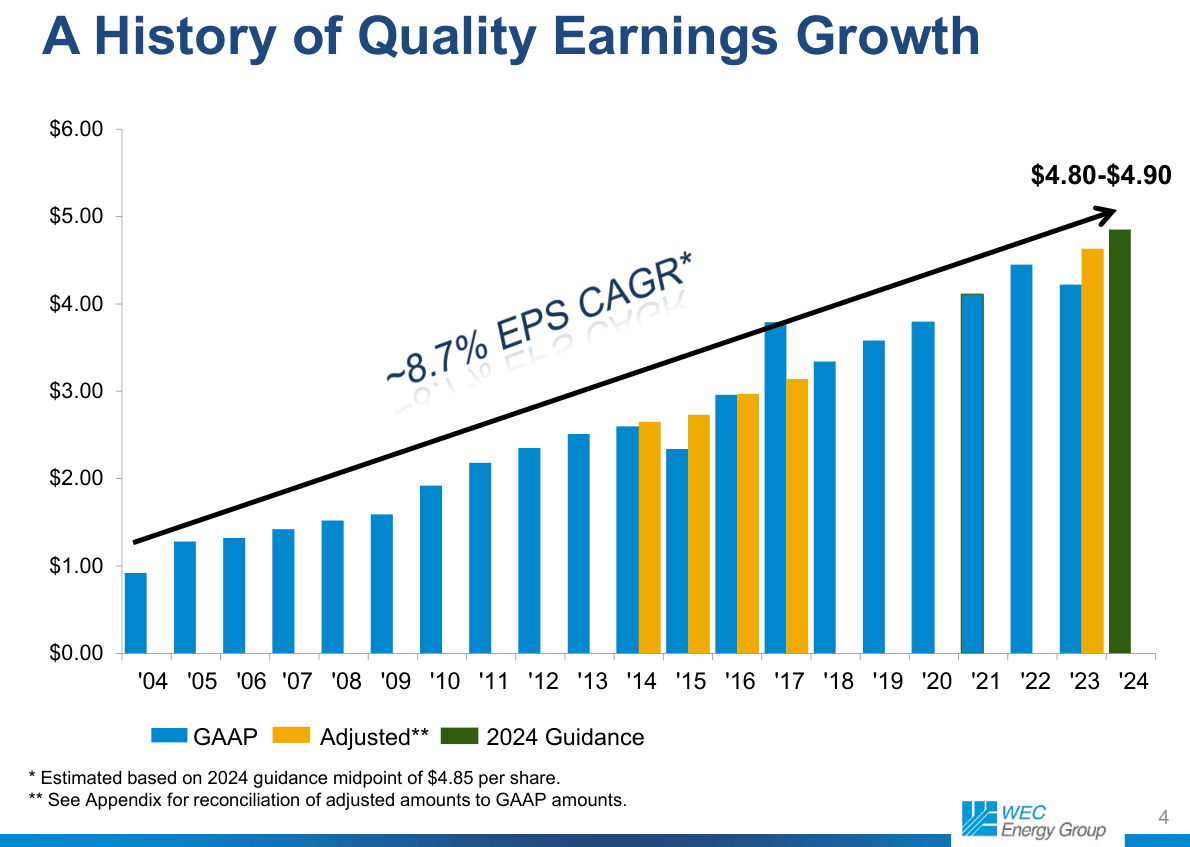

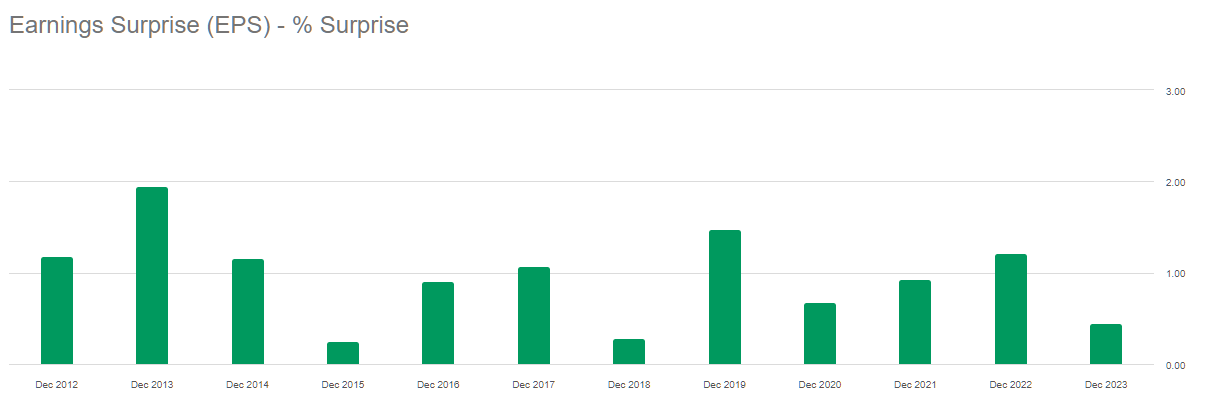

The management of WEC Energy Group has always struck me as open and honest, instead of failing to deliver on overly lofty promises. Quite the contrary, the company has always provided fairly conservative earnings per share (EPS) guidance, which it has exceeded every year since 2004 (Figure 1). According to Seeking Alpha, the company has beaten EPS estimates by an average of 1.3% on a one-year-forward basis over the last twelve years (Figure 2).

Figure 1: WEC Energy Group (WEC): Annual GAAP and adjusted – where applicable – earnings per share figures since 2004 (WEC Energy Group February 2024 Investor Book) Figure 2: WEC Energy Group (WEC): Adjusted EPS surprise in percent (Seeking Alpha)

While I'm not easily impressed given the ease with which EPS numbers can be managed, the fact that WEC rarely adjusts its EPS numbers is definitely worth highlighting. The adjustments made to GAAP EPS figures in 2014, 2015, 2016, 2017, and 2023 are transparently shown at the end of the presentation referenced in Figure 1. The adjustments were not generally positive for earnings per share - in 2017, a negative adjustment of 17% was made due to a tax benefit associated with the Tax Cuts and Jobs Act. Of course, the $0.41 charge (per share, $179 million total) taken in Q4 2023 following a negative rate case outcome in Illinois was a little disappointing, but nothing to over-interpret - more on that later.

In my view, WEC's management does an excellent job of communicating with its investors. I can only recommend listening to the earnings calls or reading the transcripts, especially the remarks by Executive Chairman Gale Klappa (who might actually extent his role beyond May 2024) and CEO Scott Lauber.

All in all, I don't think it's an exaggeration to say that WEC's management has a culture of under-promising in order to over-deliver.

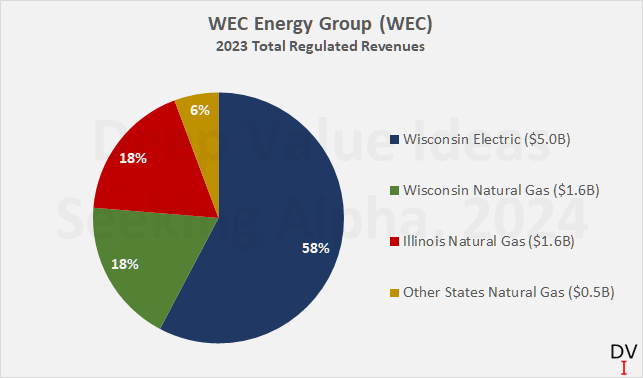

In my view, one of the most important aspects - if not the most important aspect - of utility investing is the regulatory environment. There is a positive correlation between rate decisions and long-term shareholder returns. In 2023, WEC generated $8.6 billion from its regulated utilities in Wisconsin, Illinois and, to a lesser extent, Minnesota and Michigan (Figure 3).

Figure 3: WEC Energy Group, Inc. (WEC): 2023 total regulated revenues (own work, based on company filings)

76% of 2023 regulated revenue (76/24 electricity/natural gas) came from Wisconsin, a state historically known for its constructive regulatory environment. In this context, investors certainly appreciate S&P Global's regular report on the latest developments on the regulatory climate. In 2020, Wisconsin was already one of the states with the most favorable regulatory environment. This has not changed: According to S&P's latest report in November 2023, Wisconsin is still among the states with the most constructive regulatory environment, along with Alabama, Florida, Iowa, Kentucky and Michigan. Minnesota (in which WEC generates about 6% of its regulated revenue together with Michigan) is referred to as a state with a " highly credit supportive" utility regulatory jurisdiction - the second-best rating.

As I noted in my last article, Illinois was already somewhat weaker from a regulatory perspective in 2020. The situation has not improved and Illinois is only rated as "very credit supportive" (medium rating). What sounds like a very constructive regulatory backdrop should not be overinterpreted. While S&P Global's utility ratings in the 2020 report were an assessment of investor risk associated with ownership of utility securities (i.e., equity, preferred stock and debt), the November 2023 report is a snapshot of the impact of the regulatory climate on credit ratings. As such, equity investors should take these ratings with a grain of salt. I think it is telling that the worst rating is "credit supportive" (New Mexico), while states known for an also quite challenging regulatory environment, such as Arizona, are even labeled "more credit supportive".

As the recent decision to disallow The Peoples Gas Light Service's construction costs incurred in relation with service center infrastructure (among others) shows, the outlook for utilities in Illinois is anything but positive, and that - along with the recent rebound in long-term interest rates - is likely the main reason for the poor performance of WEC stock. However, management will appeal the decision in court, and keep in mind Illinois remains a much smaller contributor to WEC's revenues than Wisconsin, accounting for only about 18% of regulated revenues in 2023, so the risk should not be overstated. Nonetheless, it is worth keeping an eye on the situation (and in particular the eventual resumption of modernization works in Chicago). I think it is sufficient to listen to management's detailed explanations in the upcoming calls. As an aside, management not only reported in detail on the proceedings in Illinois in the Q4 2023 conference call, but also provided a status update in the latest Investor Book (slide 10).

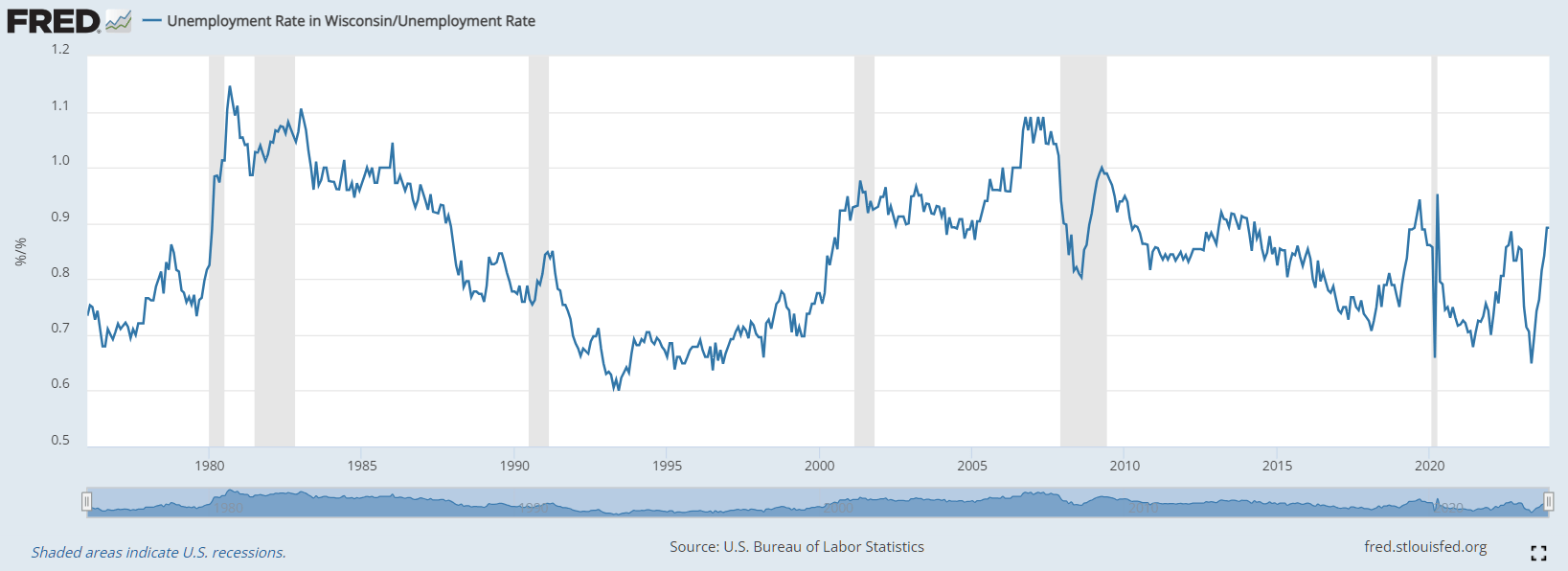

Aside from the constructive regulatory environment in Wisconsin, I think the below-average unemployment rate is worth highlighting - 3.3% in December 2023, or about 40 basis points below the national rate. As shown in Figure 4, Wisconsin's unemployment rate has traditionally been below average, with only brief periods of a slightly above average rate (1980 to 1983 and 2006 to 2007). Economic activity remains solid, as evidenced for example by Microsoft's plans to build a data center, Uline's expansion near its headquarters in Pleasant Prairie, and WestRock's intention to build a new corrugated boxes plant there as well. And although Wisconsin is not among the top 10 states in terms of inbound migration (I compared this aspect for DUK, SO, and WEC in my 2021 article), population growth remains positive (+0.34% in 2023).

Figure 4: U.S. Bureau of Labor Statistics, Unemployment Rate in Wisconsin divided by the national unemployment rate WIUR/UNRATE (retrieved from FRED, Federal Reserve Bank of St. Louis)

I have always considered WEC to be a particularly attractive utility stock because of its reliable earnings growth, which translates into above-average dividend growth. However, with a starting yield of 3.0% at the time of my original article (2021) and a yield of 3.4% when I wrote my previous article, it would have taken a very long time for the yield-on-cost to reach an acceptable level. In fact, in early 2023, I highlighted the relatively slow dividend growth in utilities such as SO and DUK as one of the reasons that kept me from adding to these positions.

With five- and ten-year average dividend growth rates of 7.1% and 7.9%, respectively, and with WEC stock currently yielding 4.2%, I would argue that the outlook for investing is much better today than it was a year ago, let alone in 2021. Granted, the regulatory environment in Illinois hasn't exactly improved, but that's nothing really new. In my view, this is a manageable risk, especially given management's strong track record and open and honest communication. Skeptical investors might also see a "higher for longer" interest rate scenario as another reason to avoid WEC stock. However, I would argue that we have much more clarity on the situation today than we did a year ago, and the margin of safety (a share price of $80 today versus $92 last year) is also much better.

If WEC continues its strong dividend growth - which doesn't seem unrealistic given management's recent comments and reiterated EPS growth guidance of 6.5% to 7% p.a. through 2028 (slide 11, February 2024 Investor Book) - investors are looking at a very solid income opportunity here.

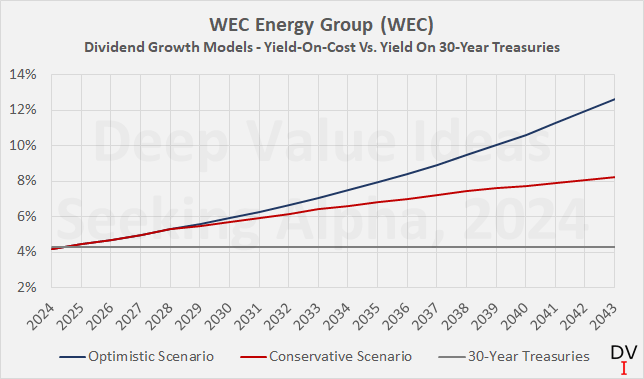

To make my case, I have modeled an optimistic scenario - namely that WEC can continue to grow its dividend by 6% p.a. over the next 20 years (slightly less than 2024-2028 average earnings growth) (blue line in Figure 5). However, to remain conservative, I have also modeled a decline in the dividend growth rate to 4% after 2028, followed by a decline to 3% in 2034 and a decline to 2% in 2039 (red line in Figure 5). While this may sound overly conservative, I would argue that WEC's earnings growth is bound to slow at some point due to external factors (population and economic growth, limited inorganic growth prospects, significant capital investment in still weakly-profitable renewables). But even under these assumptions, investors holding WEC shares for ten years would look at a yield-on-cost of 6.4% (7.1% in the optimistic case). After 20 years, WEC investors would outperform the (obviously static) yield on 30-year U.S. government bonds (gray line in Figure 5) by 8.3% and 3.9%, respectively. Of course, this thought experiment does not take taxes into account, but depending on the investor's residence, WEC dividends could even be taxed at a lower rate than bond coupons.

Figure 5: WEC Energy Group (WEC): Dividend growth models illustrating the yield-on-cost over a 20-year period, compared to the current yield on 30-year Treasuries (own work)

Put another way, an investor in WEC stock would almost immediately generate the same annualized income as an investor in 30-year Treasuries. When I wrote my last article on utilities in general and WEC, DUK, SO and Dominion Energy, Inc. (D) in particular, the breakeven period for an investment in WEC stock was still about three years.

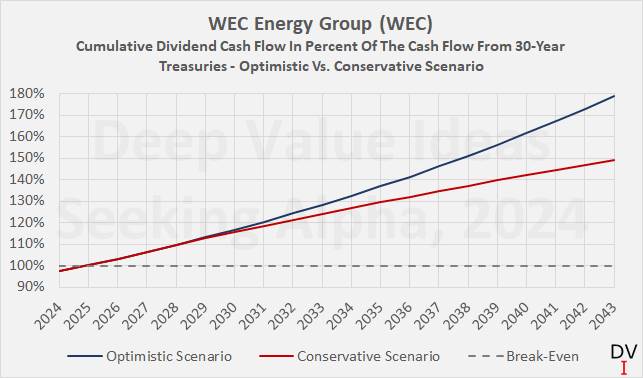

On a twenty-year time horizon, a $10,000 investment in WEC would yield between $12,800 and $15,400 in dividends under the abovementioned assumptions, compared to only $8,600 in cumulative cash flow from a $10,000 investment in 30-year Treasuries. In relative terms, investors in WEC stocks would have received 1.5 to 1.8 times the bond's cash flow after 20 years (Figure 6).

Figure 6: WEC Energy Group (WEC): Cumulative dividend cash flow in percent of the cash flow from 30-year Treasuries – optimistic vs. conservative scenario (own work)

Finally, and to conclude on a cautious note, it is of course important to remember that there is no contractual right to a dividend payment - unlike to a bond coupon payment. U.S. Treasuries, in particular, are de facto risk-free. Of course, I do not want to be misunderstood as calling WEC's dividend into question, but I think it's important to understand this key difference. Another risk worth mentioning is that, unlike bonds, equities do not mature and there is no contractual right to a return of the invested principal (consider, for example, the disaster surrounding Hawaiian Electric Industries, Inc., HE). At the same time, of course, there is consequently no reinvestment risk with equities. I don't want to go into too much detail about the pros and cons of dividend growth investments at this point, but refer interested readers to my detailed article published here on Seeking Alpha in November 2023.

Before concluding this article, I would like to provide an update on WEC's financial stability and discuss its energy mix.

At the end of 2023, the utility had $16.7 billion in long-term debt (7.6% of which matures in 2024) and $2.0 billion in short-term debt on its balance sheet. This is significantly more than the total debt of $14.3 billion at the end of 2020 (the balance sheet considered in my first article). WEC's cash position is insignificant ($25 million and $43 million at the end of 2020 and 2023 respectively), so net debt is de facto identical to gross debt.

An increase in net debt of more than 30% in just three years is quite significant and warrants a closer look. First of all, on a positive note, earnings growth has also been quite significant, albeit slightly slower - 21% EBITDA growth comparing 2019/20 and 2022/23 averages. Overall, WEC's leverage ratio in terms of net debt to EBITDA has increased slightly since 2019/20, from 5.5x to 6.0x in 2022/23.

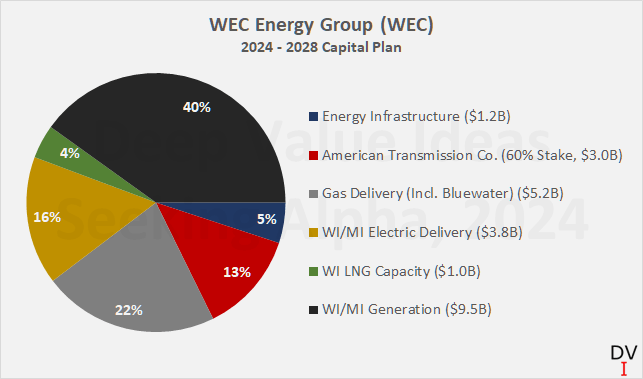

Clearly, the company has invested heavily in its portfolio and investors should not expect the aggressive capital investment to slow down anytime soon. On slide 8 of the February 2024 Investor Book, WEC sets out its updated plan for the period 2024 to 2028, according to which it plans to invest $23.7 billion (Figure 7). One of the main reasons for the substantial investment is the need to strengthen electricity distribution to support Wisconsin's economic growth. As indicated earlier, investment in Illinois will be somewhat lower until the current issues are resolved (an $800 million decrease in the plan budget).

Figure 7: WEC Energy Group (WEC): 2024 – 2028 capital plan (own work, based on company filings)

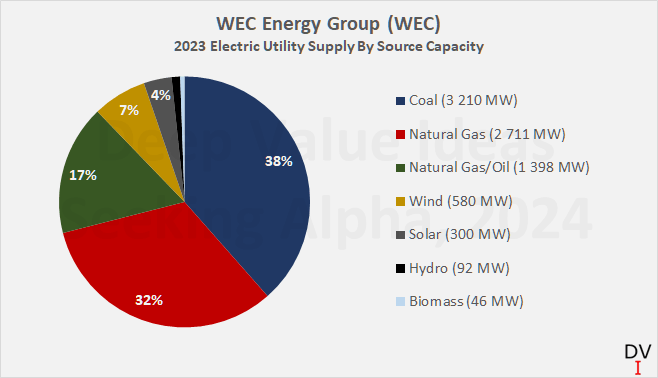

The company is prioritizing grid reliability and expansion, but is of course also continuing to strive to reduce the carbon footprint of its power plant portfolio. In my 2021 article, I pointed out that 90% of WEC's owned power plants at the end of 2020 (based on nameplate capacity) were fossil-fuel powered. Given the company's stated expectation to be net carbon neutral by 2050, it is no wonder that WEC is investing significantly in its renewables portfolio. WEC anticipates that it will no longer rely on coal as an energy source three years earlier than previously expected - by the end of 2032 - and that it will only use coal as a back-up fuel by the end of 2030.

Despite the company's expectation to eliminate coal as a fuel by the end of 2032, I hope that WEC will retain some of its coal-fired power plants as back-up or increase compatibility with natural gas to ensure energy security and reliability in the face of growing reliance on alternative energy sources, which still suffer from issues such as supply-load imbalances due to a lack of adequate buffer capacity. High-duration and/or high-power energy storage systems with appropriate response times are an important area of research, and I can only recommend anyone interested in a deeper insight into the topic to read the latest Grid Energy Storage Technology Cost and Performance Assessment. Besides well-established lithium-based battery technologies, the report goes into detail about promising alternative technologies such as for example flow batteries (in particular vanadium-based), compressed air, pumped hydropower, and gravitational energy storage systems.

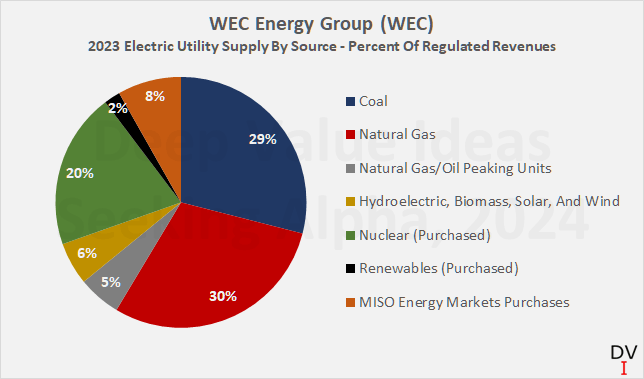

However, I do not want to give the impression that WEC's power generation portfolio is overly risky or that the returns on equity are prone to decline due to a seemingly hastened transition to alternative energy sources. Figure 7 (revenue) and Figure 8 (nameplate capacity) illustrate WEC's - in my opinion very balanced - supply mix. Of course, it is a valid argument in principle that alternative energy sources can lead to weaker profitability - at least in the near term - due to their not yet competitive EROI (energy returned on energy invested). However, in my view, investors should be aware that the evolution towards a more "sustainable" power generation portfolio is a relatively slow process. While at the end of 2020, 90.3% of WEC's own rated capacity was fossil fuel-powered, it was still 87.8% at the end of 2023 - this is certainly not a rushed transition. Moreover, it will always be a process of finding an acceptable compromise for investors and ratepayers. An energy supplier like WEC, which generates the majority of its revenue in a state with very constructive regulatory authorities, should be able to navigate these developments very well.

Figure 8: WEC Energy Group (WEC): 2023 electric utility supply by source and as a percentage of regulated revenue (own work, based on company filings) Figure 9: WEC Energy Group, Inc. (WEC): 2023 electric utility supply by source capacity, i.e., net power output under average operating conditions (own work, based on company filings)

To come back to WEC's leverage: it is to be expected that debt will continue to increase, probably somewhat faster than earnings growth. In this context, I think it should be positively emphasized that WEC is not one of those utilities that more or less constantly dilute their long-term shareholders to partially finance their capital expenditures. The company had 316 million fully diluted weighted-average shares outstanding in 2016, the same number as in 2023.

Given management's solid capital allocation track record and exposure to mostly very favorable jurisdictions, I believe WEC will continue to be able to raise debt on favorable terms. This is also underlined by its long-term credit rating of Baa1, which was last affirmed by Moody's in December 2022 with a stable outlook.

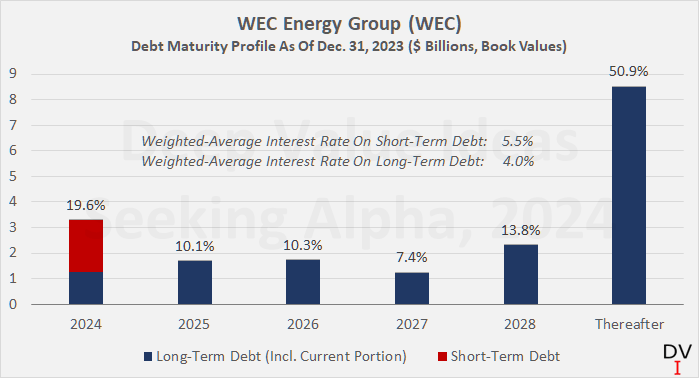

In my opinion, WEC is also quite well positioned in terms of short-term debt maturities (weighted-average short-term and long-term interest rates of 5.5% and 4.0% respectively, Figure 10) and interest expenses (approximately 20% of EBITDA).

Figure 10: WEC Energy Group (WEC): Debt maturity profile as of December 31, 2023 (own work, based on company filings)

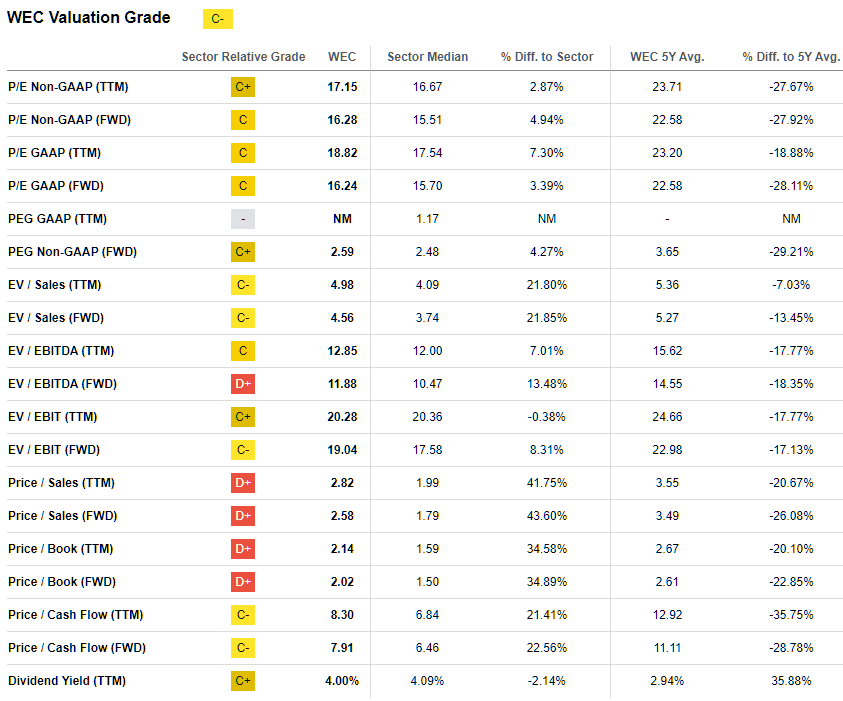

WEC Energy Group is one of the best-managed regulated utilities in the U.S. - no question about it. I first covered the company in 2021, but found the stock too expensive to justify an investment. And even as utility stocks got cheaper and cheaper in the face of rising interest rates and the "higher for longer" narrative, I held off from opening a position - mainly due to the uncompetitive dividend yield and price-to-earnings ratio in the high tens or even low twenties. Despite the undeniably high quality of the utility, I frankly never understood the premium valuation (five-year average P/E of 23.7, Table 1).

Table 1: WEC Energy Group (WEC): Valuation metrics (Seeking Alpha)

In my opinion, it was well worth the wait. As underlined by the forward price-to-earnings ratio of only about 16, WEC stock hasn't been this cheap in the last decade. The stock now trades nearly 30% below its five-year average P/E ratio and in line with the sector median, suggesting that high-quality utility WEC is mispriced.

Reasons for the undoubtedly negative sentiment on utilities in general and WEC in particular include the latest rebound in long-term interest rates from the December 2023 bottom and faded fantasies of near-term rate cuts, but more importantly, negative regulatory developments in Illinois. While I don't want to downplay the situation, it shouldn't be over-interpreted either, as Illinois accounts for less than 20% of WEC's regulated revenue. More importantly, WEC's management has a very good track record, so I am confident that the dispute will be resolved sooner or later. Management has already announced that it will appeal the Illinois Commerce Commission's November decision to disallow service center and facility construction costs.

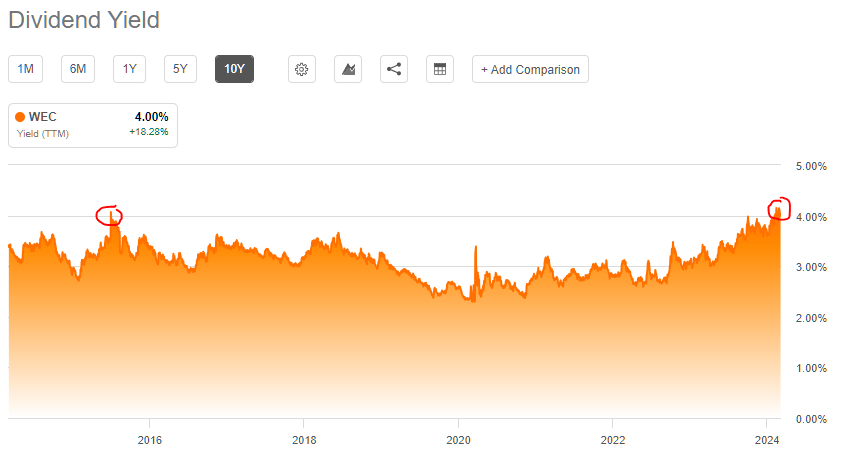

The attractive valuation is also underlined by the current dividend yield of 4.2%, taking into account the most recent dividend increase of 7% (the 21st in a row). WEC's dividend yield only briefly exceeded 4.0% in 2015 (Figure 11). From a historical perspective, WEC's yield is now almost 40% above the five-year average, which is understandable to a certain extent due to relatively more attractive bond investments.

Figure 11: WEC Energy Group (WEC): Starting dividend yield (Seeking Alpha)

However, given WEC's still very solid growth prospects, I think the choice is an easy one, especially for investors seeking to at least maintain the purchasing power of their income. While WEC's bonds naturally trade at a higher yield than Treasuries (e.g. 5.2% on the 2030 notes, a premium of about 100 basis points over 5-year Treasuries), investors should consider the reinvestment risk with bonds (what to do at maturity?) and certainly the continued strong dividend growth. My model calculations suggest that even under conservative assumptions, investors in WEC stock outpace long-term government bond yields almost immediately and Baa1-rated corporate bond yields after a few years. A yield-on-cost of well over 6% after ten years is not an unrealistic expectation, while a best-case estimate would be in the 8% range.

Of course, there are utilities like Dominion Energy D) that offer a starting yield of already nearly 6%, but I would argue that the quality of the two utilities, their management teams and especially the regulatory environment in which they operate are not comparable. However, for more risk-tolerant investors looking for higher short-term income, D might be worth a closer look. In my view, fellow contributor Ray Merola has once again provided a very balanced and in-depth assessment of the Dominion investment case in general and the latest developments in particular.

As in my previous articles, I maintain my cautious stance on utilities, primarily because of their pronounced capital intensity and debt. However, I appreciate the balancing aspect of a modest exposure to utilities in my income-oriented portfolio. I found the current opportunity in WEC Energy Group just too good to ignore and expect it to be very rewarding investment over the long term. A starting dividend yield of 4.2% and a well above-average dividend growth rate of 7% per year is a very good entry point for an investor focused on growing income through dividends, like myself.

Thank you very much for reading my latest article. Whether you agree or disagree with my conclusions, I always welcome your opinion and feedback in the comments below. And if there's anything I should improve or expand on in future articles, drop me a line as well. As always, please consider this article only as a first step in your own due diligence.