da-kuk

da-kuk

I believe that cyber security is a long-term secular growth sector, which means that demand is inelastic to broader macro drivers and can sustain a high growth rate due to the ever-increasing threats via fraud, criminality, and even sabotage that can be inflicted in a world with the rapid proliferation of digital everything that is in every aspect of modern society. To this end, I searched for a pure-play cyber security fund and chose the WisdomTree Cybersecurity Fund ETF (NASDAQ:WCBR) which despite its short track record has a differentiating stock selection methodology that may provide concentrated exposure to the fastest growth companies.

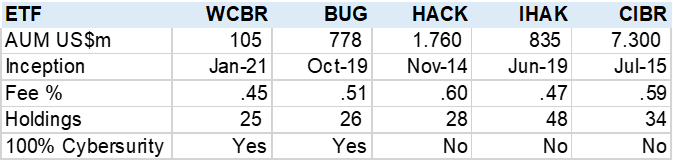

WCBR is a relatively new ETF with a three-year track record and around US$100m AUM, which pales against the sector leader First Trust NASDAQ Cybersecurity ETF (CIBR), which I recently rated a Hold. However, I identified it as one of two pure-play cyber security ETFs, the others hold about 50% in other sectors such as semiconductors and network equipment. In addition, the most distinct feature of the ETF is its stock selection methodology.

WCBR Comps (Created by author with data from Capital IQ)

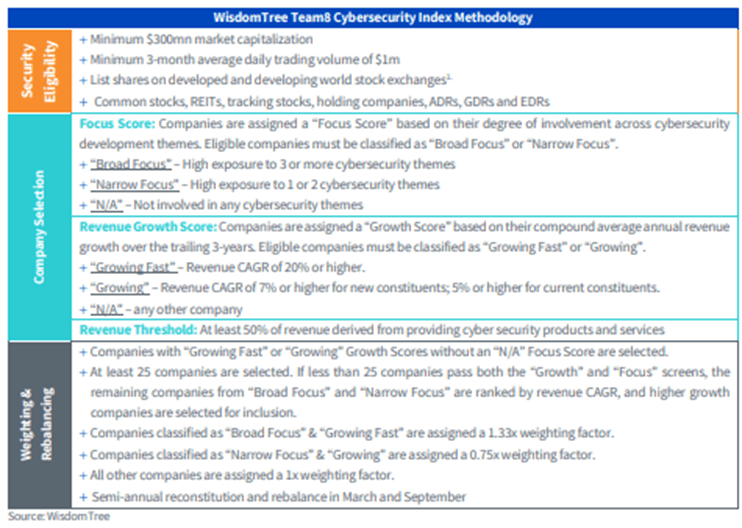

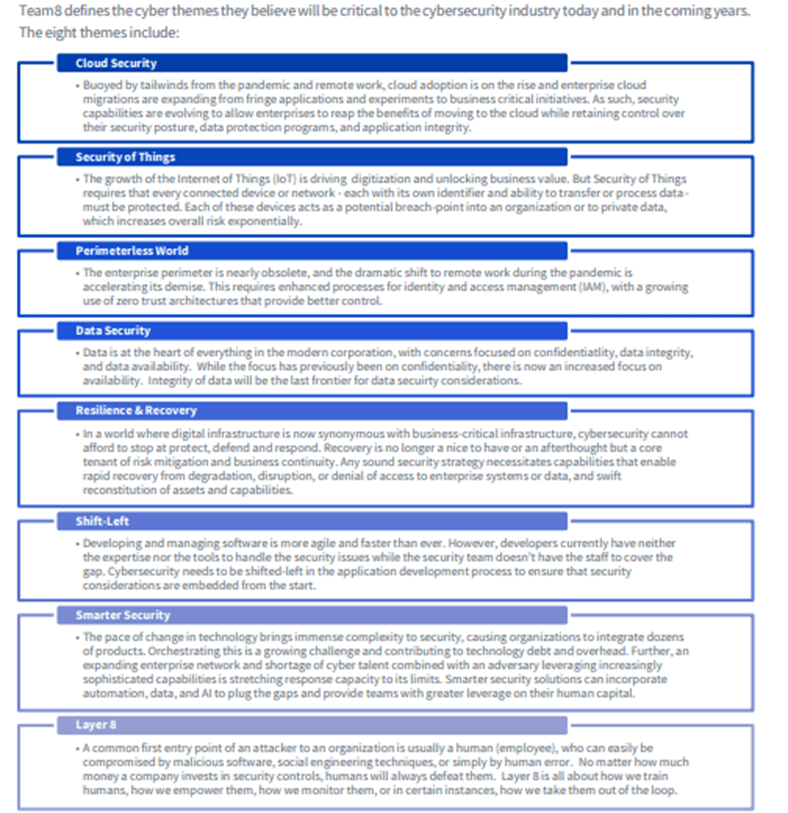

I consider this ETF a semi-passive fund in that it tracks the management company's proprietary index that selects stocks based on a very clear cybersecurity focus and those companies with the highest revenue growth rates in the past three years. There is no focus on earnings, margins, valuations, etc., which makes this a high-volatility and risk portfolio. The other focused ETF is Global X Cybersecurity ETF (BUG) which is market-cap weighted i.e., selects the larger companies independent of growth or other parameters. Below I added the full Index Methodology as well as the sub-sector focus that the index construction utilizes to select stocks. What makes this unique is the 100% revenue growth focus in selecting and weighing the portfolio holdings.

Stock Selection Method (WisdomTree)

Cybersecurity sub sectors (WisdomTree)

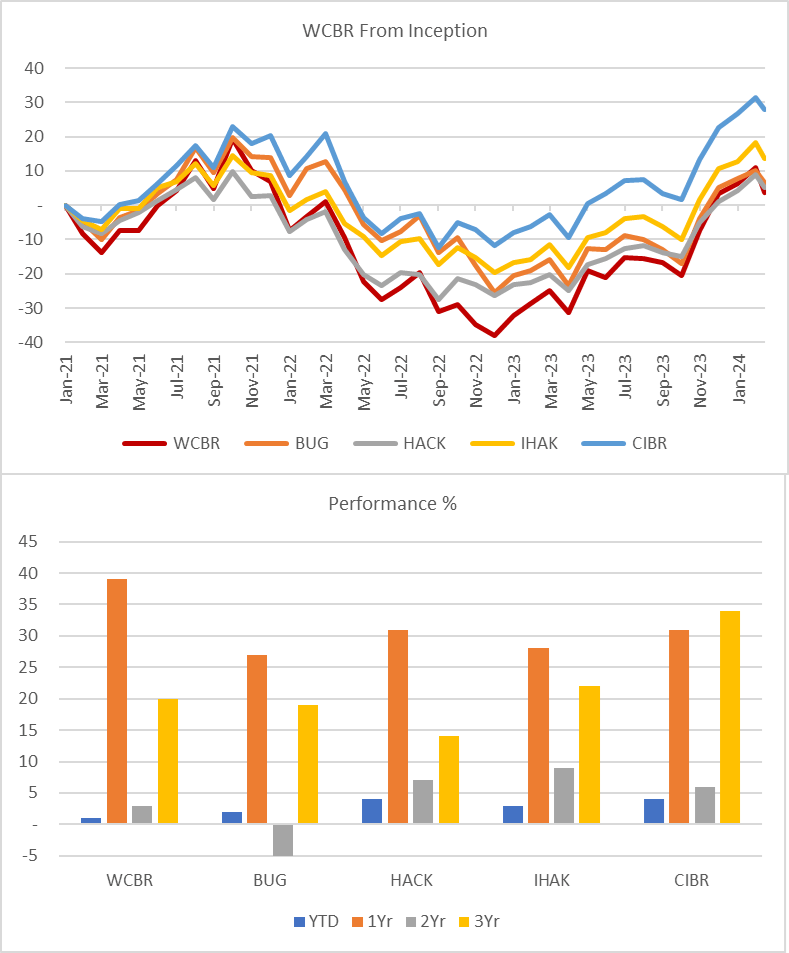

As can be seen, the ETF's short track record highlights its more volatile or risky stock selection method. The ETF saw the largest decline vs peers when the Fed began its rate hike cycle in early 2022. At the same time from the bottom at the end of 2022, it has been seen rapid price recuperation.

This ETF has an aggressive portfolio. I believe that a focus on just revenue growth in stock selection and weightings can lead to greater volatility due to far greater valuation sensitivity. The market is likely to punish more companies that do not meet revenue guidance or expectations in the absence of positive cash flow or earnings, which has been the case for SentinelOne (S) since its IPO.

WCBR Performance (Created by author with data from Capital IQ)

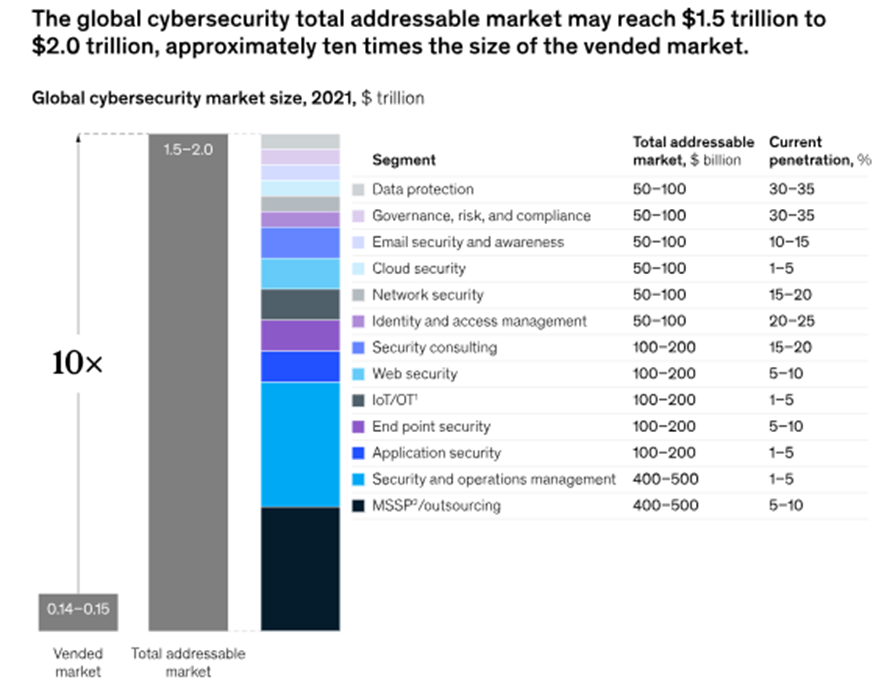

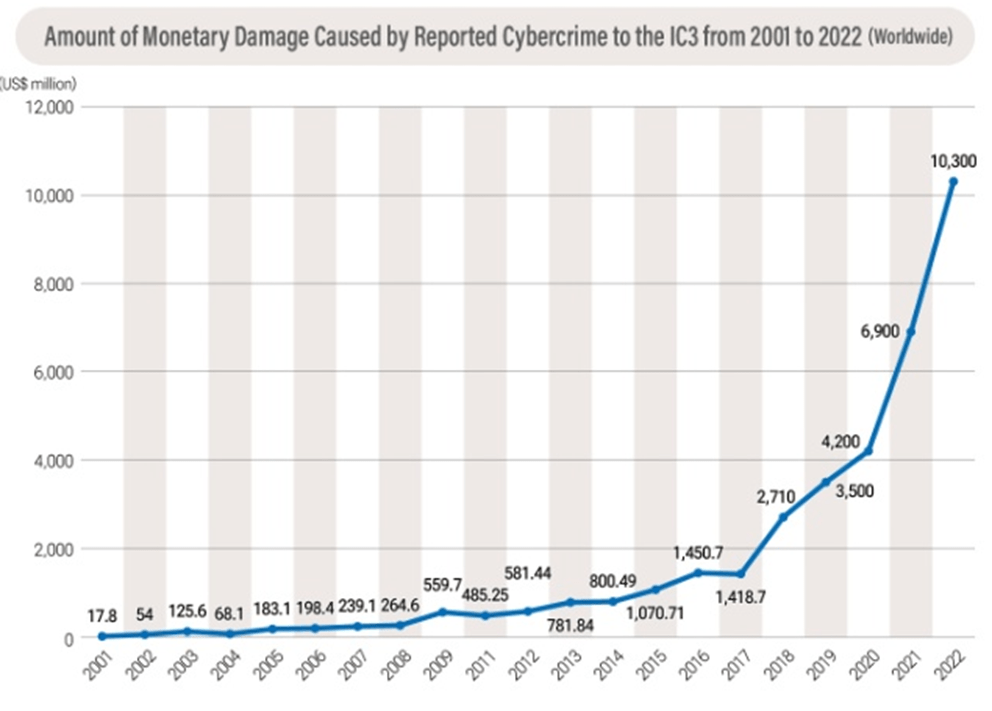

While I am no expert in cybersecurity nor the sub-sectors, products, etc. The service is increasingly in demand if not indispensable in the digital age with the TAM (total addressable market) continuing to increase the greater technology advances and penetrates most aspects of society. Below I included a chart that highlights the size and growth of the market according to McKinsey and another from JICA that illustrates the rise of cybercrime.

McKinsey

JICA

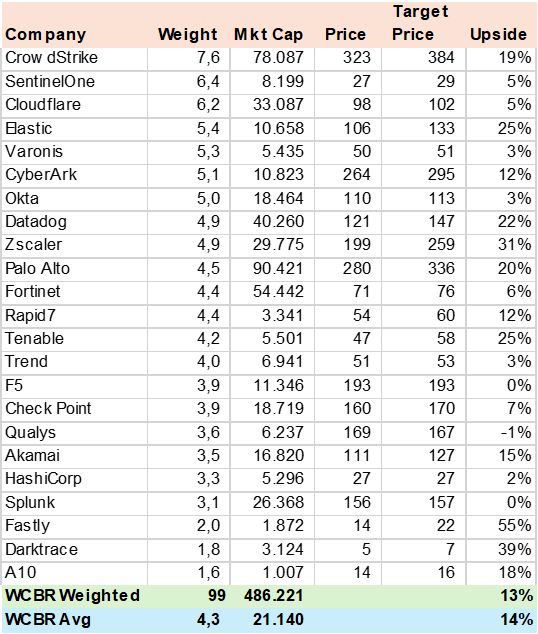

The ETF, as mentioned earlier, is 100% cybersecurity-focused and concentrated in 25 stocks selected and weighted by past 3yr revenue growth, which ignores earnings or cash flow and can be considered a high-risk portfolio in my view. Using consensus estimates for 99% of the portfolio holdings I calculated a potential upside to year-end 2024 of 13%. This may seem low given the growth and high expectations this sector has generated in the market which I believe may be more indicative of front-end loading i.e., the market is pricing up the shares on said high expectations.

WCBR Consensus Price Target (Created by author with data from Capital IQ)

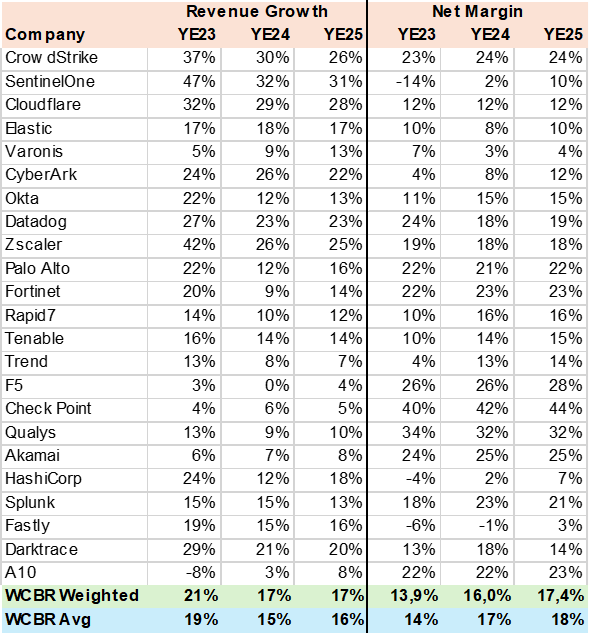

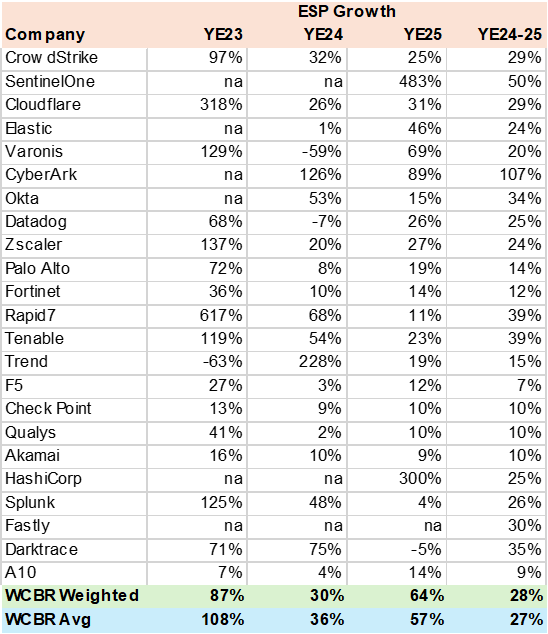

The consensus estimates that the portfolio can achieve 17% revenue growth while the top three holdings have growth rates over 25% which bodes well for the selection and weighting methodology. More importantly, the market estimates substantial margin gains rising from 13.9% in 2023 to 17.4% by 2025 and driven by SentinelOne (S) and CyberArk (CYBR). The sector's rapid growth has been detrimental to costs and margins, but it seems scale gains are being achieved that can drive EPS growth at a higher rate than revenue.

WCBR Consensus Revenue & Margins (Created by author with data from Capital IQ)

With estimated revenue growth of 17% and significant margin expansion, the consensus EPS estimate is over 28% in the YE24-25 period with YE25 EPS growth of 64% which supports the market's positive vision of the cybersecurity secular growth story and its high valuations. Note that many companies have moved from earnings losses to gains that distort EPS growth which I have adjusted from the calculations.

WCBR Consensus EPS Growth (Created by author with data from Capital IQ)

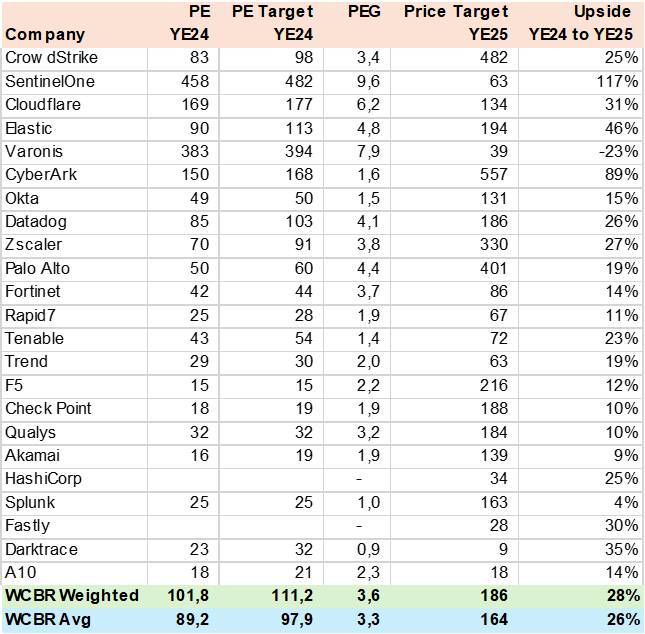

I performed a two-stage valuation analysis. The first stage was based on calculating the PEG ratio implied by the consensus year-end 2024 price targets. Then, I applied that PEG ratio to the 2025 EPS estimates to derive a year-end 2025 price target and potential upside from the 2024 price target. The results suggest that the ETF has a 28% potential upside by year-end 2025 compared to the year-end 2024 price target.

However, this exercise requires making two key assumptions that are designed to maintain a consensus view and extrapolate to 2025. In my view it is more reasonable or conservative to continue to rely on consensus estimates to derive valuations than to begin to venture into making my forecast in companies and sectors I am not yet fully qualified in. Firstly, the market will continue to value the stocks at current PEG ratios. Secondly, the companies will meet or exceed EPS forecasts. I adjusted the PEG for SentinelOne and Varonis (VRNS) to 3.6, which is the sector average, and used EPS growth for HashiCorp (HCP).

WCBR Consensus Valuation (Created by author with data from Capital IQ)

I rate WCBR a Strong Buy. The ETF offers concentrated exposure to the higher growth stocks in the cybersecurity sector via a targeted index methodology. Consensus estimates point to over 28% EPS growth in the YE24-25 period on rising margins that can support high valuations in this key secular growth opportunity. The primary risk, as seen recently in Palo Alto's (PANW) sell-off, is disappointing high revenue growth expectations, which means volatility around quarterly results may be intense.