Justin Sullivan

Justin Sullivan

Last October, I wrote that CVS Health (CVS) is buyable because of growth opportunities due to the bankruptcy of Rite Aid. Walgreens Boots Alliance (NASDAQ:WBA) is a direct competitor to both, so I see opportunities here as well.

Both can acquire Rite Aid stores to grow. And geographically, acquiring Rite Aid stores is more attractive to Walgreens than CVS Health. But Walgreens must have sufficient financial resources.

WBA has struggled in recent years due to soaring prices and inflation, and opioid claims also weigh heavily on its bottom line. Now it is also suffering from rising interest rates. Over the past few years, fortunately, the debt load has decreased significantly, but interest expense rose sharply due to higher rates. The Fed (and President Biden) expect interest rates to be lowered this year, which of course is a great catalyst for Walgreens Boots Alliance.

Tim Wentworth, Walgreens' new CEO, aims to increase the value of Walgreens by, among other things, reviewing the cost base and carefully evaluating all capital investments to increase cash flows. Walgreens is on track to achieve $1B in cost savings, $600M in capital expenditures and $500M in working capital improvements.

So there are plenty of catalysts to push the stock price up in the coming years.

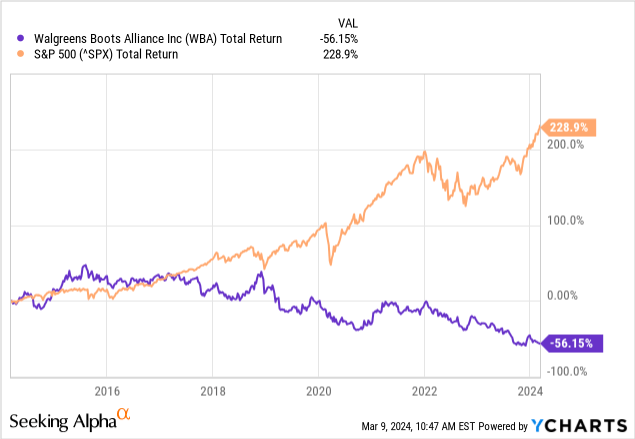

The stock price has been under pressure since 2016. Recently, Walgreens announced it would halve its quarterly dividend to $0.25 per share. Investors were clearly not happy about this. And the fact that Walgreens dropped out of the Dow Jones does not help the stock price either.

Previously, WBA was a prominent stock that had better annualized returns than the S&P500. But look at it optimistically for a moment, because the stock's valuation is a lot more favorable than it was then. Its price-to-book ratio of 0.9 is a 10-year low.

Walgreens Boots Alliance has pharmacy chains in the US, as well as in the UK and Germany. This makes WBA more diversified than CVS Health's pharmacy chain because of its international footprint.

Products are also sold through their e-commerce platform. The advantage of this is that e-commerce is hugely cost-effective because a warehouse can be set up efficiently through automation.

This year seems to be an inflection point. Revenue in fiscal 1Q24 rose sharply by as much as 8.7% year-on-year at constant exchange rates. However, operating income disappointed, declining 33% over the same period. This was mainly due to the sharp rise in inflation. Now that inflation has come down to normal levels, I am optimistic about an improvement in profits in the coming years. The higher costs were also due to the Transformational Cost Management Program and will hopefully bear fruit in the long run.

The Transformational Cost Management Program is focused on improving its cost structure and balance sheet to drive long-term profitable growth. It has been doing this since the launch of Walgreens Health in 2021; this consists of investments in VillageMD and CareCentrix. These investments will better serve health in primary care and post-acute care.

The Pharmaceuticals segment in the U.S. performed well, with sales up 10.7% year-on-year. However, the retail segment suffered from a weaker respiratory season, resulting in a 6.1% year-on-year decline in retail sales. Customers purchased fewer COVID-19 test kits, cold tablets and the like. I think this will continue to be the case for the next few years as COVID-19 seems to be over. Internationally (Boots UK and Germany) the company performed excellently with a sales increase of 4.4% year-on-year and an increase of 15% in operating profit. Internationally, the operating profit margin is slightly higher than Walgreens (2.4% vs. 2.1%). Operationally, there is still room for improvement for Walgreens.

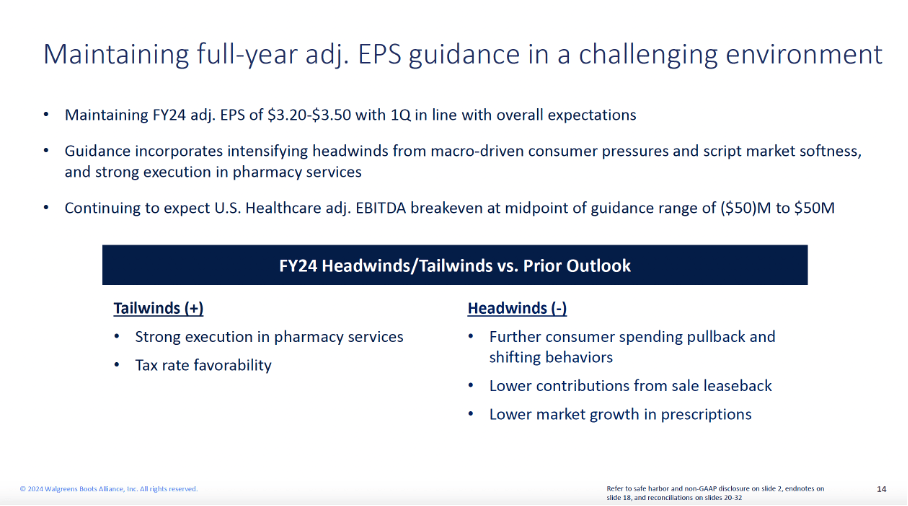

Walgreens Boots is entering a transitional year next year and expects mid-year earnings per share of $3.35 at mid-point. This is a decrease of 16% compared to last year. This is mainly due to changed business conditions and reduced demand. The forward P/E ratio then comes out to just 6.3, making WBA an interesting value play.

Walgreens is going to do its best to cut costs and improve profitability. With Tim Wentworths' experience as a healthcare executive, I expect his experience will contribute greatly to better business results.

FY2024 Full Year Guidance (WBA 1Q24 Investor Presentation)

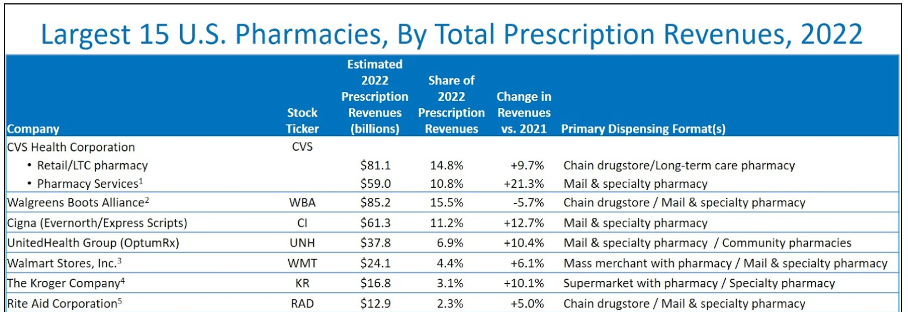

Rite Aid's bankruptcy presents opportunities because there is now less competition. The closure is especially beneficial to CVS because they overlap geographically. As a result, CVS has less direct competition.

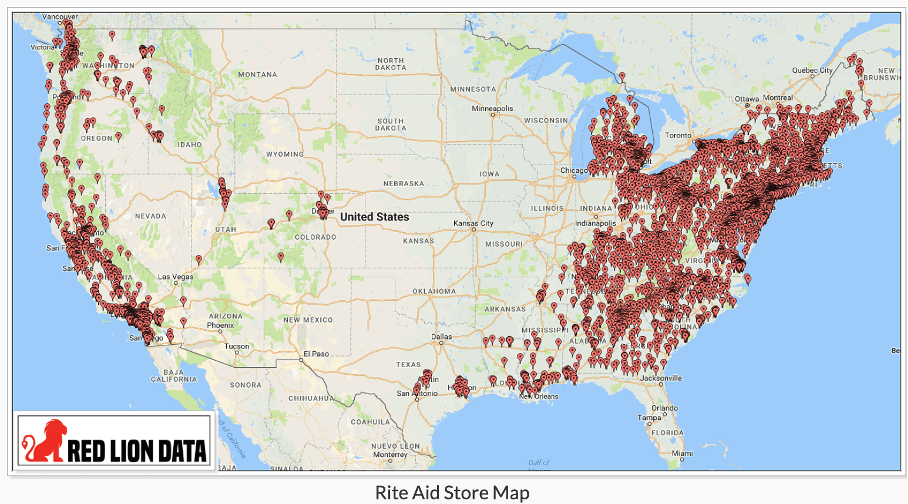

Rite Aid was the largest pharmacy on the East Coast of the U.S. and the third largest on the West Coast. This dominance presents opportunities for competitors to take over some of Rite Aid's stores. However, I don’t think it’s a good fit for CVS because the concentration of pharmacies in metropolitan areas would become too great. Walgreens' stores are better spread across the US. For Walgreens, a takeover provides opportunities to penetrate deeper into metropolitan areas. Walgreens seems better suited, but then Walgreens must have sufficient financial resources.

Largest 15 US Pharmacies (drugchannels.net)

Rite Aid Store Map (Red Lion Data)

Although several Walgreens stores are now leased through sale and leaseback, the inventory will have to be financed.

In recent years, WBA has significantly reduced its debt. In 2019, total debt was about $16.8 billion. With an EBITDA of $7 billion, WBA was able to carry the debt load just fine.

Higher costs and a low profit margin led to negative EBITDA of $2.5 billion in fiscal 2023. Still, total debt decreased significantly over the years to $9.3 billion. Adjusted operating income (excluding opioid claims) reached $3.4 billion in fiscal 2023. The interest coverage ratio is then adequate at 5.7x. I find this acceptable for a company like Walgreens Boots Alliance. WBA sells consumables that are necessary in society which guarantees continued sales.

This year, the Fed is expected to cut interest rates. This could be a nice windfall for Walgreens. TTM interest expense is now about $570 million, bringing the average interest rate to 6.1%.

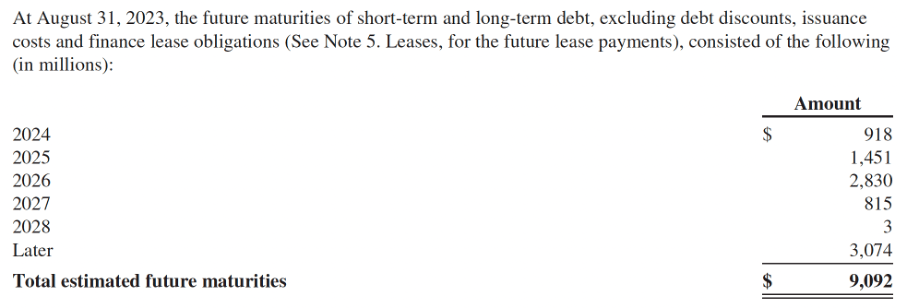

In the fiscal year 2023 report, we see that the largest debt repayment occurs in 2026. This is favorable for WBA because the Fed expects to have cut interest rates sharply to 2.9% by then. The refinancing rate will then be favorable, lowering WBA's interest expense because its current average interest rate on its debt = 6.1%.

Debt Maturity Schedule (WBA FY2023 Report)

In my opinion, there is work to be done to improve the balance sheet. Cash and cash equivalents were $784 million, up $56 million from the previous quarter, but significantly less than in previous years. And the current ratio, at 0.66, is also worrisome. The current ratio has been below 1 since 2018 and the share price has fallen significantly since then. WBA may be struggling to meet its short-term obligations.

WBA, in my opinion, has the opportunity to acquire some of Rite Aid's drugstores. Walgreens' leverage will then be higher, but the interest coverage ratio still leaves some room for opportunity. With the cost-cutting program in sight, the opportunities are even greater.

With a P/B ratio of only 0.9, we can say that WBA is clearly undervalued based on its 5-year average value of 1.6. I believe in reversion to the mean and expect WBA’s valuation to return to its 5-year average P/B ratio of 1.6.

In more than 40 years, the company has never been so cheaply valued. Are investors that pessimistic about WBA's future?

There are clearly competitors lurking, such as Amazon Pharmacy. With the arrival of Amazon Pharmacy in 2020, it could take WBA or CVS out of business. Amazon focuses mainly on e-commerce, which is a big advantage in terms of cost efficiency. WBA will have to focus more on that as well to be competitive. Amazon Pharmacy I see as a direct competitor to WBA because WBA is less established in metropolitan areas. In suburban areas, e-commerce is much more interesting. Moreover, drones could be used to deliver products.

In terms of valuation metrics, WBA is much more attractive than CVS. The adjusted P/E and P/B ratios are both about 30% lower for WBA compared to CVS. CVS, on the other hand, does own a profitable health insurer called Aetna. I think this is a strong synergy that provides a stable revenue stream. CVS's revenues are therefore also more predictable.

WBA and CVS' Valuation Metrics (Author's own calculations)

The question is whether WBA’s stock is worth buying. I think it is. WBA is currently in a transition phase where, under the new CEO, their ambition is to reduce costs significantly. In addition, WBA will benefit from favorable refinancing rates in the coming years that will lower interest expenses. This may give it the opportunity to acquire several Rite Aid stores. Moreover, the stock's valuation is very favorable, not only compared to the industry but also to its history. Therefore, I see a lot of opportunity in both the company and the share price.