PETER PARKS/AFP via Getty Images

Editor's note: Seeking Alpha is proud to welcome Bargain Buyer as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

PETER PARKS/AFP via Getty Images

I believe Weibo (NASDAQ:WB) is an undervalued, dominant player in the Chinese social media market that happens to be a low-risk, high-uncertainty bet at current prices. I think the market has priced in all the risks, yet has left out all the rewards. Given the share price trades at an all-time low, I am of the view that the market is undervaluing Weibo's strong earnings power and sticky user base. In my opinion, Weibo continues to grow users and create engaging content to drive value for shareholders by finding and maintaining unique ways to monetize user engagement.

Weibo is a leading social media company in China that allows users to create, share, and discover content. It contains content ranging from news, entertainment, education, from a variety of industries. In some sense, it's like the "Twitter" of China. Weibo's revenues are split up into two segments: Advertising and Value Added Services. The advertising business is explained in the 2022 annual report as

We seek to provide advertising and marketing solutions to enable our customers to promote their brands and conduct effective marketing activities. We provide our customers with analytical tools to enable them to track and improve the effectiveness of their marketing campaigns on our platform".

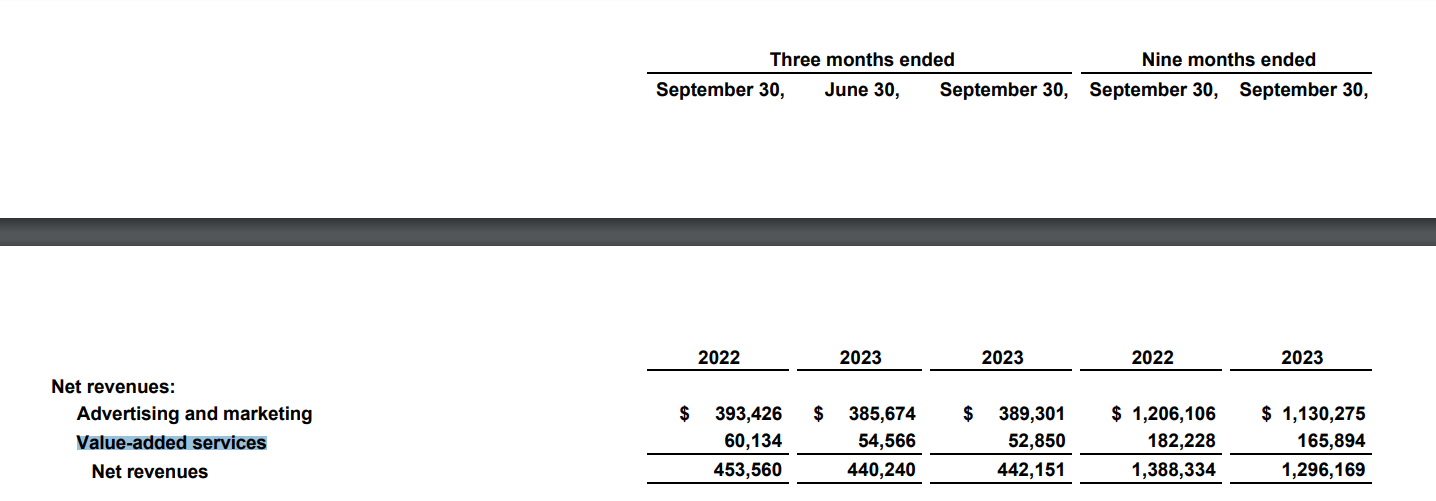

Weibo sells advertisers social display ads that appear on the main page, promoted marketing that involves things like branded hashtags and managing sponsorships, and other various ways of helping spread image and reputation on Weibo's platform. Advertising revenues make up 87% of revenue for the nine months ended Sept, 2023.

Weibo's Third Quarter 2023 Unaudited Financial Results

The value-added services consists of membership fees, live-streaming fees, e-commerce, and Weibo Wallet. This makes up the remaining 13% of total sales for the nine months ended Sept 2023. According to the 2022 Weibo annual report, "For value-added services, we mainly offer membership services, online game services, social commerce solutions and live streaming tools to users that enable them to conduct related activities on our platform." These services help maintain user engagement by sort of locking them in, as they receive many benefits of being a member such as ad-free browsing, post editing, and exclusive emojis and stickers. Furthermore, there's e-commerce solutions that Weibo provides so that users can purchase products directly on the Weibo app. Weibo has integrated its platform with other e-commerce sites like Taobao and JD.com (JD), which allows a very seamless shopping experience.

Weibo continues to offer a lot of value and firepower for the advertisers on its platform. Because of its large user base, there's pretty much a niche audience that advertisers can tap into using Weibo's targeted advertising tools. Keep in mind that 95% of users on Weibo are mobile, and that 76% are under 30 years old. These tech-savvy young consumers are exactly what advertisers are looking for, so they are willing to spend good money to get their attention.

In addition to a diverse user base, offers highly intelligent demographic targeting to find exactly the audience advertisers are looking for. Once advertising campaigns are underway, Weibo offers data analytics and marketing tools to tailor your ads more effectively.

To make sure there's a price for everyone, Weibo has very flexible pricing and ads for all kinds of customers. There are Weibo News Feed Ads, which for $15 you can enhance your current Weibo posts to over 10,000 users. Then there's search promotions, which for a fee advertisers can put their content at the top of the search list, similar to Google Search. Many other types of ads exist to appeal to any kind of need that fits the advertiser's budget.

Weibo charges the advertisers in one of two ways: Cost Per Thousand Impressions (CPM) and Cost Per Engagement (CPE). Impressions means views, whereas engagement means someone actually clicks on the ad. On average it costs 10 RMB for 1000 impressions on Weibo, and 0.5 RMB for each engagement. Needless to say, the more users on Weibo will directly affect how much impressions and engagements happen for advertisers, which then makes revenue for Weibo grow.

Weibo continues to see positive momentum in its user base. According to the Q3 2023 Earnings Transcript, "In September 2023, Weibo’s MAU crossed the 600 million milestone, reaching 605 million, and average DAU reached 260 million, representing a net addition of 21 million and 8 million users on a year-on-year basis, respectively."

I believe this growing user base will likely continue to sustain strong financial performance for Weibo because it bolsters the network effect that attracts both new users to join and content creators to promote themselves on the platform. In my view, the positive feedback loop that occurs between new users and content creators is very hard to disrupt, because it continues to snowball as long as there are new people who want to join the ecosystem. In the long term, this will build more value and attract advertisers to promote themselves on the platform with the widest reach, leading to higher revenues and profits for Weibo as they continue to monetize these interactions.

As the user base continues to move, content creators and KOLs are unlikely to abandon their loyal following on Weibo because it would seriously disrupt their brand image and reputation. Therefore, the KOLs are sort of locked in on the platform as they are stuck with their following on Weibo, and cannot easily replace their content and history on the platform somewhere else.

Weibo can leverage AI in a new way to create content that is more efficient, interactive, and of higher quality. In the Q3 2023 earnings call, CEO Gaofei Wang said, "So, for instance, the contents generated by AIGC have more user stickiness and also interactive rates and very efficient as well. So in Q3, so we have been actively applying the LLM, a large language model on different verticals to increase the efficiency of the content generation."

AIGC (AI Generated Content) can radically change how content is generated on social media platforms like Weibo. This should help Weibo monetize users by creating more precise targeted advertising to users based on their data while giving them higher quality content and that is more personalized. Weibo has already begun several AI initiatives, one of which tests a content creation tool with select users. Considering Weibo's historical innovation in creating new revenues streams, I believe the management at Weibo can use AI to increase creators' earnings, which will lead to a more loyal creator base and continue to retain the already massive user base.

Markets are concerned about Weibo's competitiveness, and major players like Douyin and Kuaishou have emerged in China's social media space. Despite the growing concern over competition, I believe that multiple players can coexist without necessarily hurting one another's unique value proposition. Weibo continues to differentiate itself by sticking to its traditional roots as a microblog, giving real-time news and social commentary about many diverse topics.

People say that WeChat is competitive with Weibo, but actually there are several differences between the two. Many social media apps can thrive in China's big market because they all differentiate themselves to specialize in some unique way. This phenomenon allows multiple winners, which leads me to believe competition is not a threat to Weibo's unique model. Among all the apps, I believe Weibo is the best choice for visibility and discovery for advertisers because of the high user to user engagement. Chinese consumers still prefer getting influenced by the vast amount of celebrities and KOLs that are on the platform. According to Statista, "From the consumer perspective, KOL marketing has become the most preferred marketing channel. A 2023 survey reported that influencer endorsements worked particularly well in promoting fashion and beauty goods."

In my view, Weibo will continue to hold a traditional role as a microblog that is discussion oriented, almost like a digital town square. The other apps and social media platforms serve different purposes, like short-form entertainment for Douyin and authentic real-life content for Kuaishou. People often choose to download multiple social media apps, so it's not necessarily a zero-sum game. Weibo continues to be a major news source for Chinese people, while the other social media platforms serve different purposes. For example, in the USA Snapchat (SNAP), Instagram, TikTok, can all co-exist without it necessarily being a zero-sum game in which a winner happens to take all. The same can be said for China, in which Weibo is like "Twitter" and continues to be the main place for social discussion. I believe that in China, the social media "pie" is big enough and continues to grow for multiple players to specialize and make money.

Many will readily point out the political risk in China, arguing that crackdowns from the Chinese government can at any moment punish China's big tech companies. Although true, I believe most of this "crackdown" is over for Weibo at least, since no major fines or regulatory changes have happened recently to Weibo. I still believe that the Chinese government wants to support its economy through the rational regulation of its tech companies. Chinese Premier Li Qiang has spoken about the importance of its tech companies in the economy's growth. They do these regulations to protect consumers, enhance financial stability, and mitigate potential negative externalities. Although controversial, this presents what I believe to be a low-risk, high uncertainty bet at current prices.

The range of future outcomes may be diverse, but the odds of losing money at sub $9 per share is actually quite low. Risk, being the permanent loss of capital, is actually low at these prices because most of those fears are already priced in. Weibo currently trades at an all-time low in its history.

Despite this, Weibo shares still face potential for decline. Most of the risk for Weibo comes mostly from external influences rather than internal. Several things could cause a price decline, including further tech regulation which restricts Weibo's ability to monetize, competitive risks from other social media apps, and a lack of catalysts for the stock to move. Weibo has been cheap for a while, and may remain so in the future.

Other worries include the worsening relationship between US and China, which could destabilize the trust and investor sentiment in the Chinese markets. Chinese macro headwinds include high unemployment, record levels of debt, low birth-rates, and a real-estate crisis.

On top of this, Weibo is subject to strict censorship rules on anti-PRC content, and is under constant scrutiny by government officials. Because of this, it may be hard for people to voice their true opinions on Weibo as they face punishment. This balance between political propaganda and free-speech is something that even the US social media companies are struggling with. In China, limited freedom of speech exists as the Chinese government will clamp down on anti-China views or news stories. If Weibo fails to censor illegal content deemed by the government, they may face future penalties.

Not atypical to most social media companies, consumers are wary of privacy issues and Weibo is no different. It has a lot of power tracking and storing people's data. However, it should be noted that according to Weibo's privacy policy the data is collected fairly and lawfully, with full transparency on how the data is used. But, should the Chinese government tap into this database, it could make Weibo users uncomfortable and want to delete the app as they don't want the government tracking their daily life.

Finally, in the future the Chinese government may regulate the amount of time children under 18 are allowed to be on social media. Recent past regulation proposed to limit children's playtime on online video games, and a similar rule could pass that limits their time on social media. 32.5% of Weibo users are under 24 years old, making this a potential risk to user growth and engagement for minors on Weibo.

All of the following are serious downsides and are worth considering carefully.

Starting with TTM revenues of $1.7 billion, I forecast a revenue growth of 5% for the next 3-5 years. I believe this is very fitting because Weibo is at a mature stage in its lifecycle and will unlikely be hitting double-digit growth any time soon. Weibo achieved peak revenues back in 2021 of $2.25 billion, and I do believe with enough time the company can return back to this level. After 3 years of 5% revenue growth, $1.7 billion becomes around $2 billion. Apply a net margin of 20%, and you get profits around $400 million. Divide by shares outstanding of 235.8 million and you get around $1.7 EPS by 2027.

To give some wider range, I will now assume a modest $1.5 to $2 in earnings power consistently for the next few years, which hovers around my $1.7 EPS. Apply a forward multiple of 10x on the lower end, the stock is easily worth at least $15 per share. Having a margin of safety of almost 50% is quite safe, despite the high uncertainty of future outcomes. At $9/share, the bad is already priced in, which leaves the good as potential upside. Given both a conservative earnings estimate of $1.5, which is below Wall Street expectations, and a below average earnings multiple of 10x, Weibo shares should be worth at least $15 (1.5 x 10).

Profitability metrics are still holding strong, with net margin at 23% compared to a 5-year average of 20%. Weibo is still generating very good cash flow, over $500 million consistently for the past 4 years. Management is sitting on $2.8 billion in cash and cash equivalents, many of which can be used to buy back stock. At these prices, buybacks would be great for shareholders in reducing shares outstanding. Even if the business does not grow, and even declines a little, I believe that major buybacks alone can be enough to drive EPS growth.

Also, the tangible book value of $13 per share is a good safety net, so buying below book gives the investor another margin of safety. Most of the assets on the balance sheet are cash ($2.8 billion), receivables (~$900 million), long-term investments (~$1.3 billion), which are pretty valuable and likely worth close to their stated values. Debt is ~$1.6 billion, which is very much below the cash position so the company is very solvent.

Also, investors today are also buying at a significant discount to what Alibaba paid in 2013. For a 18% stake in Weibo, Alibaba paid $586 million, equaling a $3.25 billion valuation. Markets value Weibo at around $2 billion, which is a ~40% discount to what Alibaba paid for Weibo in 2013. Anyway an investor slices it, the stock is very cheap and should re-rate higher through a multiple expansion and strong future earning power.

CEO Gaofei Wang has proven to be an innovative leader, starting as a General Manager at Weibo back in 2012. Since his tenure began, he managed to grow revenues almost 6x from ~$300 million to ~$1.8 billion. Users went from under 200 million to over 600 million, a 3x increase. Mr. Wang has the ability to unlock new monetization opportunities such as live-streaming, content creator partnerships, and entering new industries and markets for advertising such as healthcare and automotives.

I believe Mr. Wang to be determined and reasonable in growing the business while keeping all stakeholders' interests in mind. He wants to create an open and transparent platform where everyone is encouraged to speak, while balancing the interests of the Chinese government. This new real-name initiative for accounts with 1 million followers or more creates a safe environment where people can trust information coming from a certain account to be real. A more trusted environment will likely increase user engagement as people trust and believe what they see on Weibo to be verified if they can see a real name behind the account. This will reduce the amount of misinformation and fake rumors being spread from impostors, leading to a better platform for news.

Weibo is, from a historical perspective, very cheap and continues to offer upside from these levels. Its dominant position as a social media company will likely continue given more users, better AI to efficiently create high quality content, and a diverse social media industry which fosters multiple platforms serving different purposes. I believe Weibo is worth at least $15, giving an investor around 66% potential upside. Ultimately, if the users keep growing, the business will likely generate consistent earnings, many of which could be used to buy back more stock. At current prices, in my opinion, Weibo is a low-risk, high-uncertainty bet for those who can withstand short-term volatility.