The Westamerica Bancorporation (NASDAQ:WABC) Full-Year Results Are Out And Analysts Have Published New Forecasts

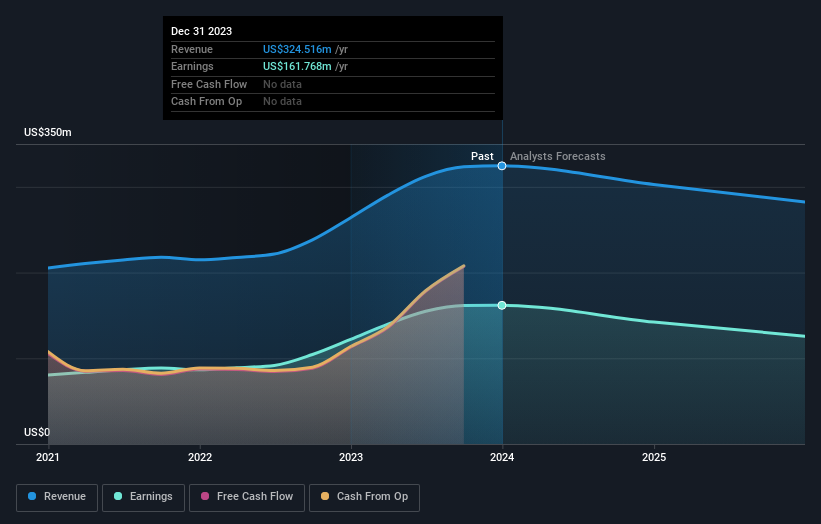

Westamerica Bancorporation (NASDAQ:WABC) shareholders are probably feeling a little disappointed, since its shares fell 8.5% to US$49.79 in the week after its latest full-year results. It was a credible result overall, with revenues of US$325m and statutory earnings per share of US$6.06 both in line with analyst estimates, showing that Westamerica Bancorporation is executing in line with expectations. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

Check out our latest analysis for Westamerica Bancorporation

After the latest results, the consensus from Westamerica Bancorporation's three analysts is for revenues of US$302.9m in 2024, which would reflect a discernible 6.7% decline in revenue compared to the last year of performance. Statutory earnings per share are expected to fall 12% to US$5.32 in the same period. Before this earnings report, the analysts had been forecasting revenues of US$309.3m and earnings per share (EPS) of US$5.44 in 2024. The analysts are less bullish than they were before these results, given the reduced revenue forecasts and the small dip in earnings per share expectations.

Despite the cuts to forecast earnings, there was no real change to the US$58.00 price target, showing that the analysts don't think the changes have a meaningful impact on its intrinsic value. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. There are some variant perceptions on Westamerica Bancorporation, with the most bullish analyst valuing it at US$61.00 and the most bearish at US$55.00 per share. With such a narrow range of valuations, the analysts apparently share similar views on what they think the business is worth.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. These estimates imply that revenue is expected to slow, with a forecast annualised decline of 6.7% by the end of 2024. This indicates a significant reduction from annual growth of 10% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 5.3% per year. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - Westamerica Bancorporation is expected to lag the wider industry.