gerenme

gerenme

The Schwab U.S. Dividend Equity ETF™ (NYSEARCA:SCHD) underwent its scheduled annual rebalancing effective Monday, substituting 23/100 stocks in a significant shakeup for the most popular dividend ETF on the market. This year's changes include the removal of Broadcom (AVGO) and the addition of Bristol-Myers Squibb (BMY), now SCHD's fourth-largest holding with a 4.03% weighting and one reason for SCHD's improved 3.87% expected dividend yield. The rebalancing also improved the portfolio's forward P/E and trailing dividend payout ratio, but unfortunately, sales and earnings per share growth metrics deteriorated further. These are the tradeoffs long-term value investors must consider, and I look forward to taking you through the rebalancing in further detail below.

This year's rebalancing saw 23 additions totaling 11.25% of the current portfolio weight, as follows:

To maintain the 100-stock portfolio, the Dow Jones U.S. Dividend 100 Index also deleted 23 stocks. This list is far more exciting, but it is primarily driven by changes in dividend yield.

After some speculation, Broadcom was the major casualty. Reading other analysts' predictions, I noticed many forgot that the Index only considers securities in the top 50% by dividend yield after filtering for ten consecutive years of dividend payments. As a result, SCHD's lowest-yielding stock is DKS at 2.08%, followed by NSP and CF at 2.32% and 2.40%, respectively. It's close to the minimum I predicted, so it was never in doubt that Broadcom's 1.70% dividend yield would lead to its removal.

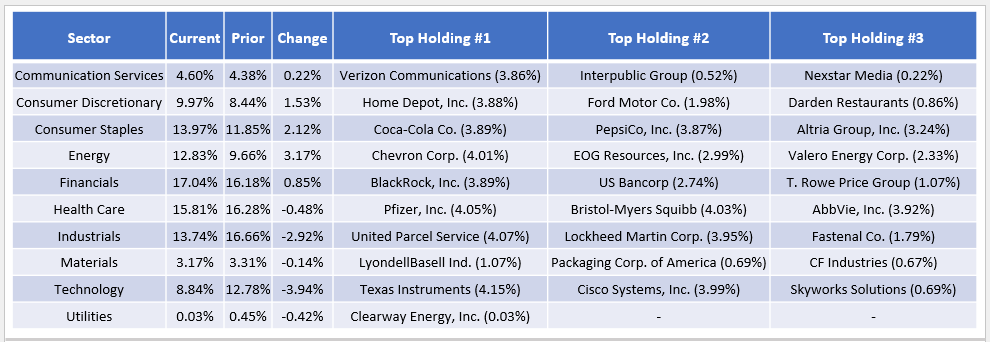

The additions and deletions noted above primarily impacted the Energy, Industrials, and Technology sectors. Here is a look at SCHD's latest sector exposures compared to before and the top three holdings in each sector.

The Sunday Investor

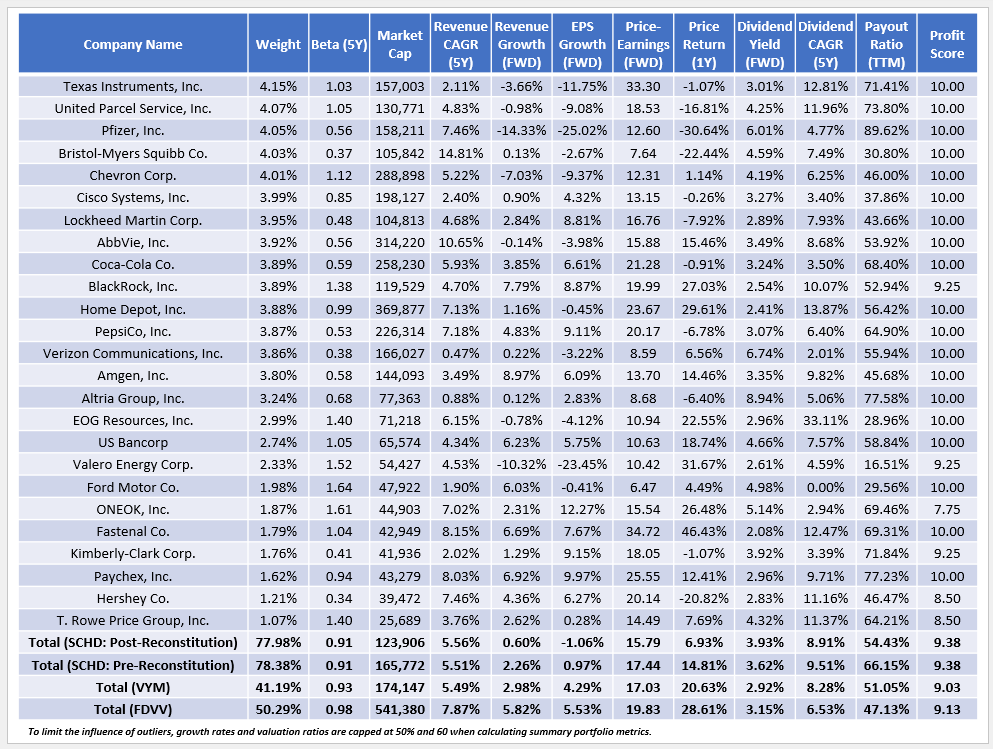

The following table highlights selected fundamental metrics for SCHD's top 25 holdings, totaling 77.98% of the portfolio. I've included the Vanguard High Dividend Yield ETF (VYM) and the Fidelity High Dividend ETF (FDVV) as comparators for those looking to combine dividend yield and dividend growth.

The Sunday Investor

Here are six takeaways:

1. SCHD's five-year beta held firm at 0.91. I've covered SCHD numerous times, and its strategy usually results in a slightly less volatile portfolio than the broader market, a nice feature for defensive investors. Since November 2011, it's delivered an annualized 12.85% gain but lower standard deviation and better "worst year" and "maximum drawdown" figures than the SPDR® S&P 500 ETF Trust (SPY). As a result, its Sortino Ratio, a measure of downside risk-adjusted returns, is competitive. Remember that SCHD is a large-cap value ETF operating in a growth-favored market, so recent underperformance is expected and typical.

Portfolio Visualizer

2. With Broadcom deleted, SCHD's weighted average market cap dropped from $166 billion to $124 billion, indicating it's relatively light on mega-cap stocks. Remarkably, SCHD only has an 8.27% overlap by weight with SPY compared to 10.86% previously, so I believe SCHD will continue to attract investors looking for a high-quality complement to their S&P 500 Index funds.

3. Income investors will be pleased to see the Index yield increase from 3.62% to 3.93%. After deducting SCHD's 0.06% expense ratio, I estimate SCHD's yield at current prices to be 3.87%, which sets it apart from competitors like VYM and FDVV. Texas Instruments (TXN), United Parcel Services (UPS), and Pfizer (PFE) drive this high yield, which involves some good fortune, as the Index is not yield-weighted. Instead, SCHD follows a modified market-cap-weighting scheme with a 4.00% cap on constituents on the reference day used for rebalancing. This means that mega-cap stocks barely meeting the minimum yield and dividend growth criteria could receive this 4.00% weighting, while high-yielding stocks fall to the bottom of the list. I prefer this approach, but funds like the iShares Core High Dividend ETF (HDV) work better for those looking to maximize yield.

4. SCHD's weighted average 66.15% trailing dividend payout ratio was getting too far stretched and likely would limit future dividend growth. Fortunately, this improved by 12% to 54.43%, despite not being one of the four screens used in the composite ranking. As a reminder, they are:

On that note, SCHD's weighted average free cash flow to total debt did decline from 12.31x to 11.08x, and its trailing ROE jumped from 26.08% to 29.04%, so for those doubting the process, it does work as advertised. However, SCHD's current constituents have only increased dividends by 8.91% over the last five years compared to 9.51% in the prior portfolio. It's insignificant, but these changes primarily reflect an improvement in dividend safety, not dividend growth.

5. Further to that point, SCHD's estimated one-year earnings per share growth rate declined from 0.97% to -1.06%, with sales growth declining even further. It's a big disappointment for me, as I've noted many times over the last couple of years how SCHD's slowing growth was a flaw. Often, value investors don't focus on growth rates, but for dividend growth investor ("DGI") investors, it's crucial because dividends are paid out of earnings. Unless a company continuously cuts costs, it'll have to grow sales to grow earnings, and since SCHD's holdings aren't doing that very well, there's no reasonable expectation strong dividend growth can continue. Fortunately, SCHD has some wiggle room with the lower payout ratio, but I suggest keeping an eye on this ratio throughout the year. It was 49.09% two years ago, and as this ratio increased, SCHD underperformed.

6. Notably, VYM and FDVV do not have the same growth issues as SCHD, so I believe they are superior choices for dividend growth investors. You would think differently by looking at the three fund's historical dividend growth rates, but that's why it's always essential to evaluate what an ETF owns today rather than what it previously owned. Consider how SCHD's one- and three-year sales growth rates are -3.80% and 9.76%, respectively, which means growth averaged 17.25% in 2021-2022 before slipping more than 20% last year. Since sales expectations are flat for 2024, we might only get low-single-digit dividend growth again until results improve.

Seeking Alpha

This year, the main changes to SCHD were the deletion of Broadcom and Merck & Co. and the addition of Bristol-Myers Squibb, which improved the expected dividend yield by 0.31% to 3.87%. Other improvements include a one-point decrease in the portfolio's free cash flow to debt ratio, a 3% improvement in return on equity, and a 12% reduction in the dividend payout ratio, a welcome change that improves SCHD's dividend safety.

Unfortunately, sales and earnings per share growth dwindled further, and I no longer see how Schwab U.S. Dividend Equity ETF™ can deliver the high dividend growth of the past without negatively impacting total returns. Therefore, I have assigned a "hold" rating to SCHD, and I look forward to answering your questions in the comments section below. Thank you for reading.