Pla2na/iStock via Getty Images

Pla2na/iStock via Getty Images

When it comes to long-term investing, it's important to assess the "type" of stock we're dealing with. In this case, I'm not hinting at the sector a company operates in, but what we can expect in terms of returns and risks.

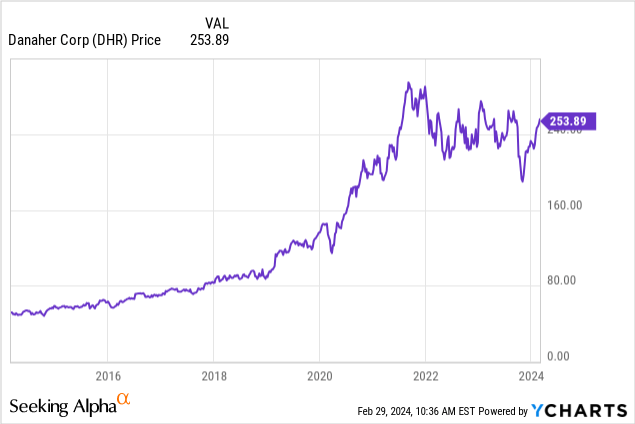

For example, I mainly invest in consistent wealth compounders that tend to rise consistently with subdued volatility. In this category, I would put healthcare stocks like Danaher (DHR), which sells equipment and supplies to drug manufacturers and a wide range of other companies.

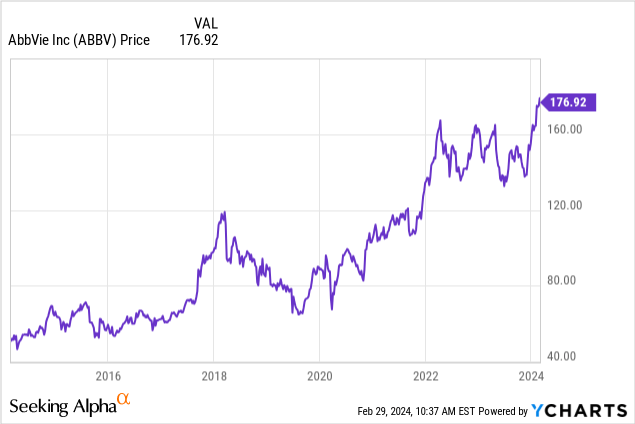

Then, there are healthcare companies like AbbVie (ABBV) with fantastic track records of dividend growth yet periods of slightly elevated volatility due to issues like patent loss risks.

However, stocks like ABBV are still blue chip stocks that should allow investors to sleep well at night and deploy cash with subdued risks.

I consider the two stocks above perfect tools for consistent dividend (growth) investing.

Ignoring stocks with no value and elevated risks, there is one more category: beaten-down value plays.

These are stocks that come with elevated risks. However, they also have enough value to make the case that taking the risk is worth it.

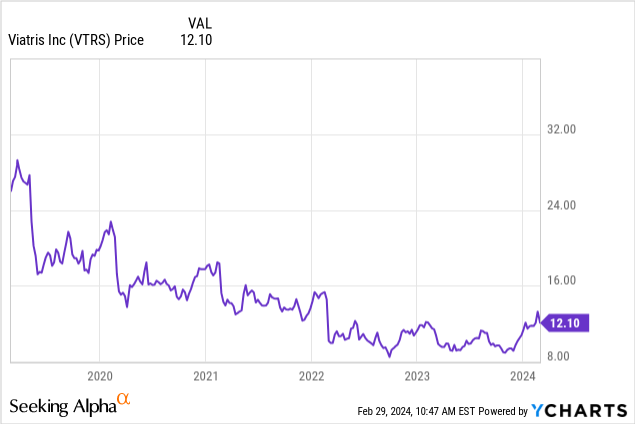

In this group, I would put Viatris Inc. (NASDAQ:VTRS), the result of the merger between Mylan and Upjohn.

I started covering this stock on September 14, using the title "Why 5%-Yielding Viatris Hasn't Doubled Yet."

Since then, shares have returned 24%, beating the 13% return of the S&P 500.

Here's a big part of the takeaway I used back then:

Viatris may not have been the most exciting stock in recent years, but it's certainly worth a closer look. Despite an elevated debt load, the company is making strategic progress, reporting strong revenues and impressive free cash flow.

Viatris is actively working on divestitures to reduce debt, and its strong pipeline indicates a promising future.

Trading at a low valuation compared to its EBITDA and free cash flow, Viatris has the potential for significant capital gains and offers a juicy dividend that seems well-protected.

In this article, I'll take another look at the company and explain why I remain bullish - despite pressure on growth and an elevated debt load, which caused the stock to perform poorly in the past.

So, let's get to it!

While Viatris is far from becoming a consistent compounder with subdued volatility, it is showing progress where it matters most: earnings growth, pipeline strength, and debt reduction.

All that matters for investors at this point is that it proves that it is able to turn its business around. That's where the most value can be unlocked.

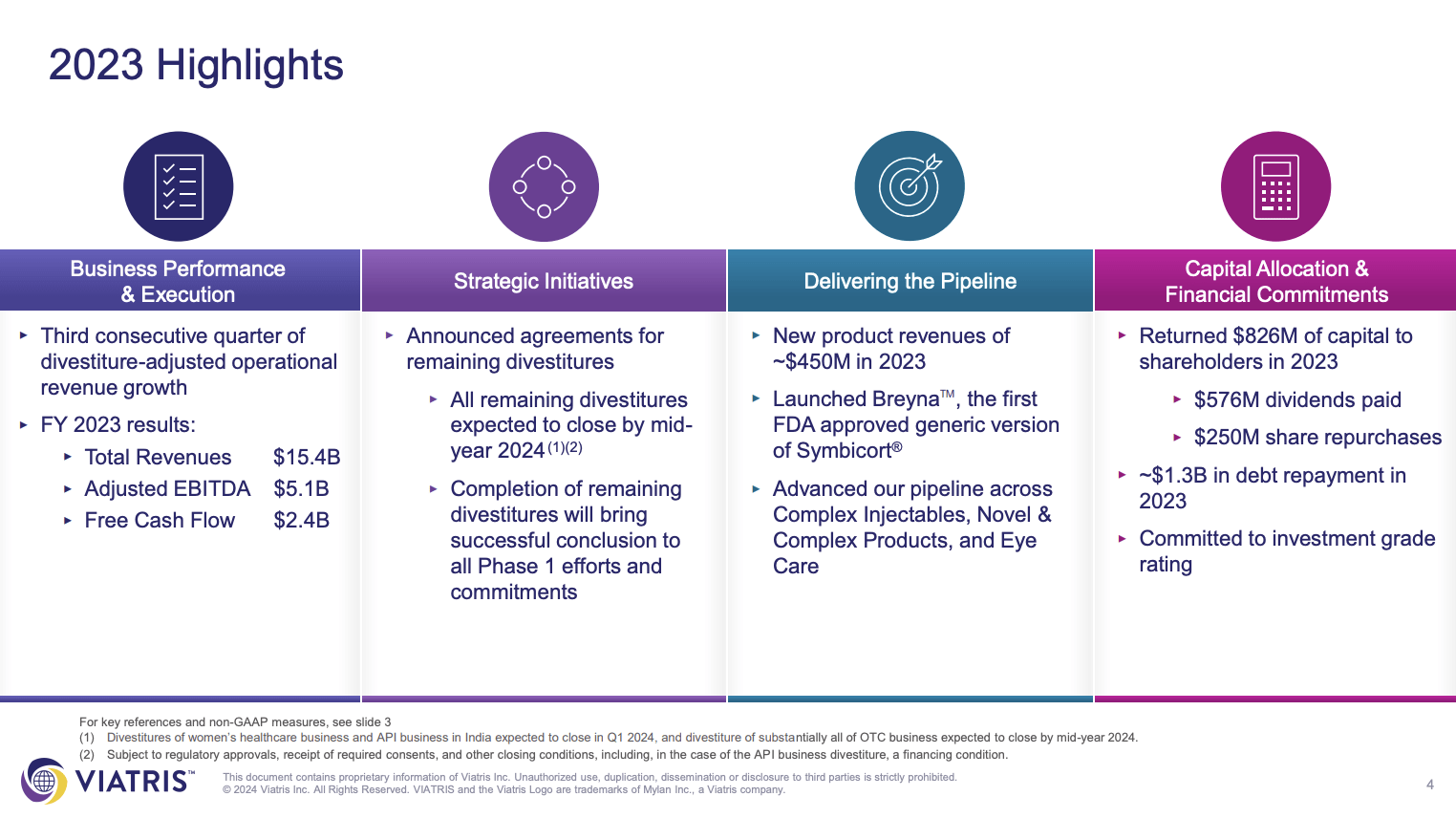

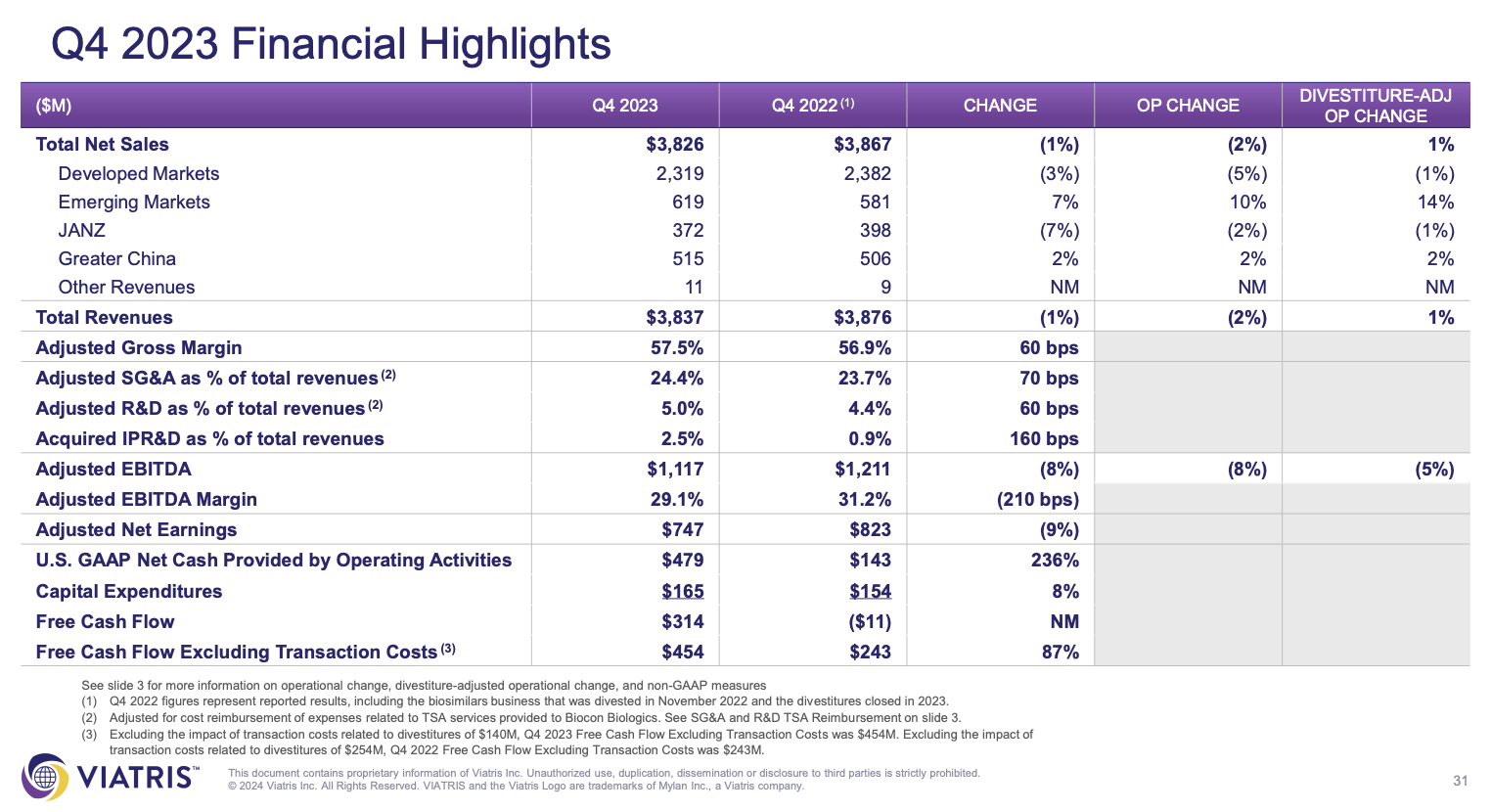

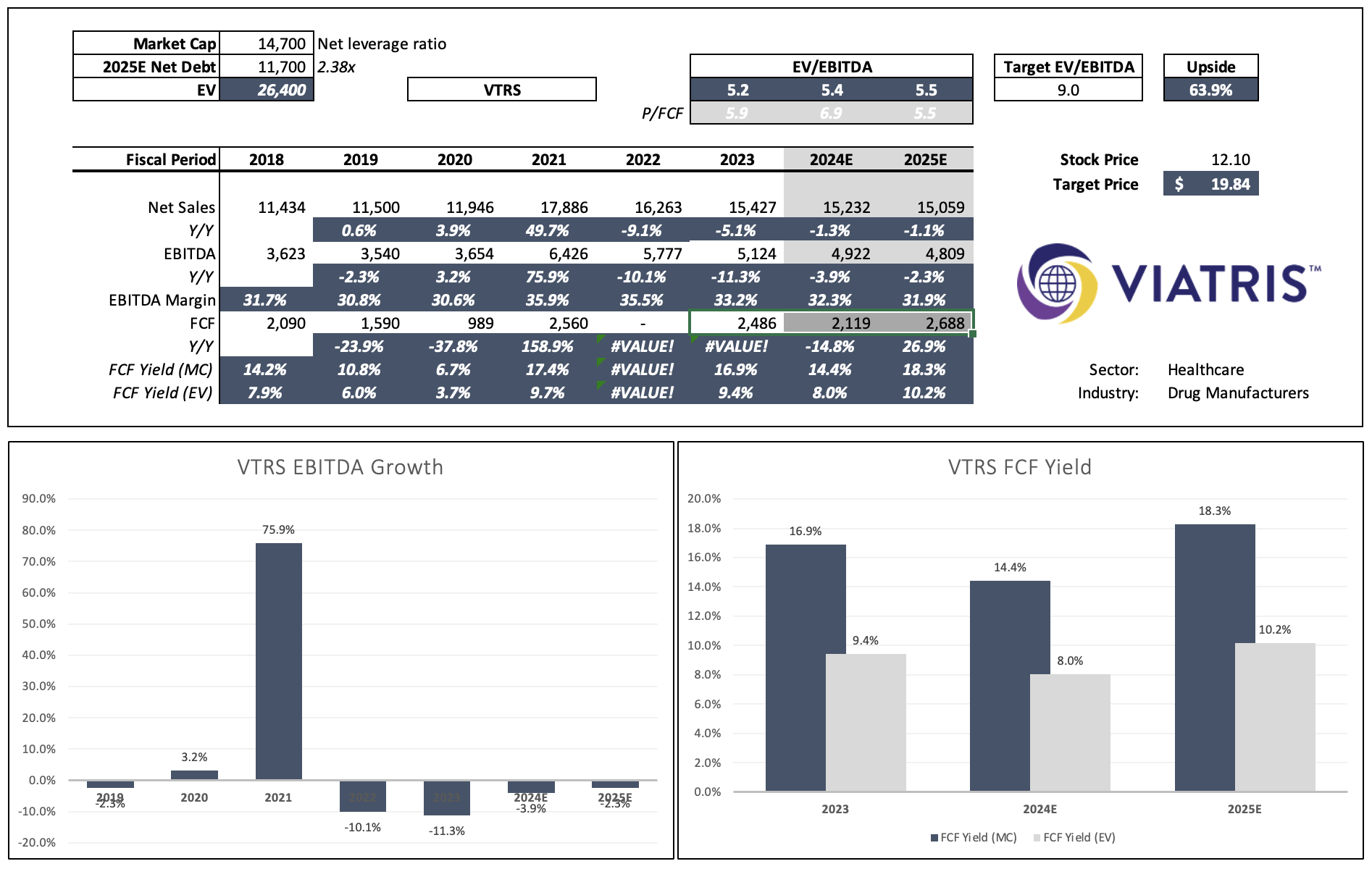

The company just released its FY23/4Q23 earnings, which showed that full-year revenues reached $15.4 billion, with an adjusted EBITDA result of $5.1 billion.

EBITDA is down roughly 11% compared to last year.

Viatris

Furthermore, free cash flow came in at $2.4 billion, which is 16% of its current market cap!

This is the highest free cash flow yield among all companies that I cover (excluding mining and energy).

However, it's only so high because the company has an elevated debt load, which means investors know that free cash flow is now mainly earmarked for debt reduction. These stocks tend to trade at lower free cash flow multiples - or lower free cash flow yields.

But more on that later.

Before we discuss debt and guidance, I need to shed some light on the 2023 performance.

According to the company, its operational (quarterly) revenue growth continued for the third consecutive quarter in 4Q23, with a solid performance across Developed Markets, Emerging Markets, and the Greater China segment.

However, in this case, a solid performance refers to the numbers being good compared to prior expectations, as divestitures-adjusted growth rates are mainly negative on a year-over-year level.

Viatris

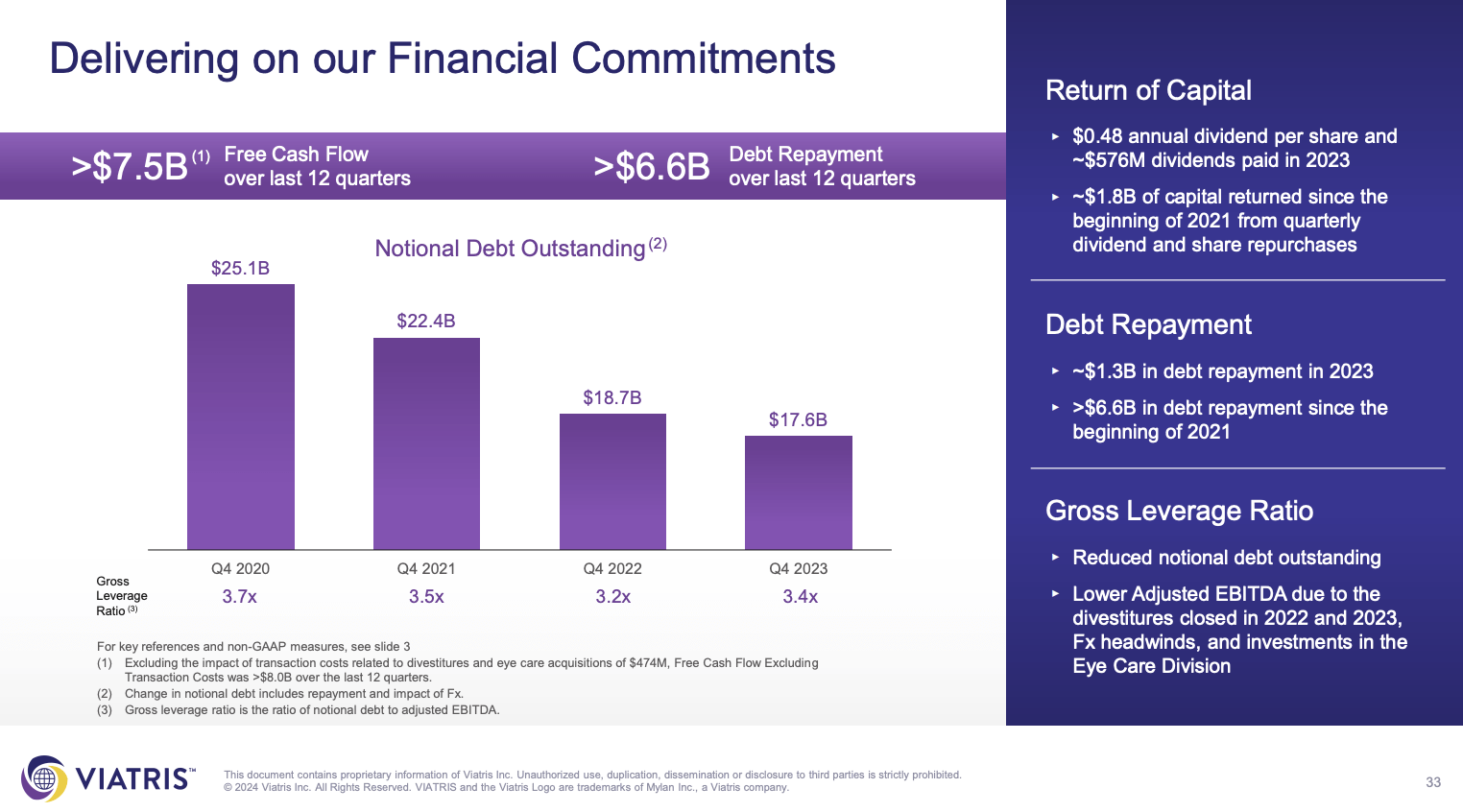

The good news is that debt reduction is going very smoothly.

Over the past three years, free cash flow generation exceeded $7.5 billion, allowing the company to reduce debt by more than $6.6 billion and return roughly $1.8 billion to shareholders.

These numbers clearly show where the priorities are at right now - especially in light of the aforementioned free cash flow numbers.

Viatris

During its earnings call, the company reiterated its commitment to maintaining an investment-grade rating and increasing shareholder distributions over time.

These positive actions taken by the company reinforce our continuing commitment to an investment-grade rating and an expectation of increasing the return of capital to our shareholders. - VTRS 4Q23 Earnings Call

Generally speaking, the company emphasized a strategic shift towards a more balanced capital allocation approach, focusing on divestitures, collaborations, and capital returns.

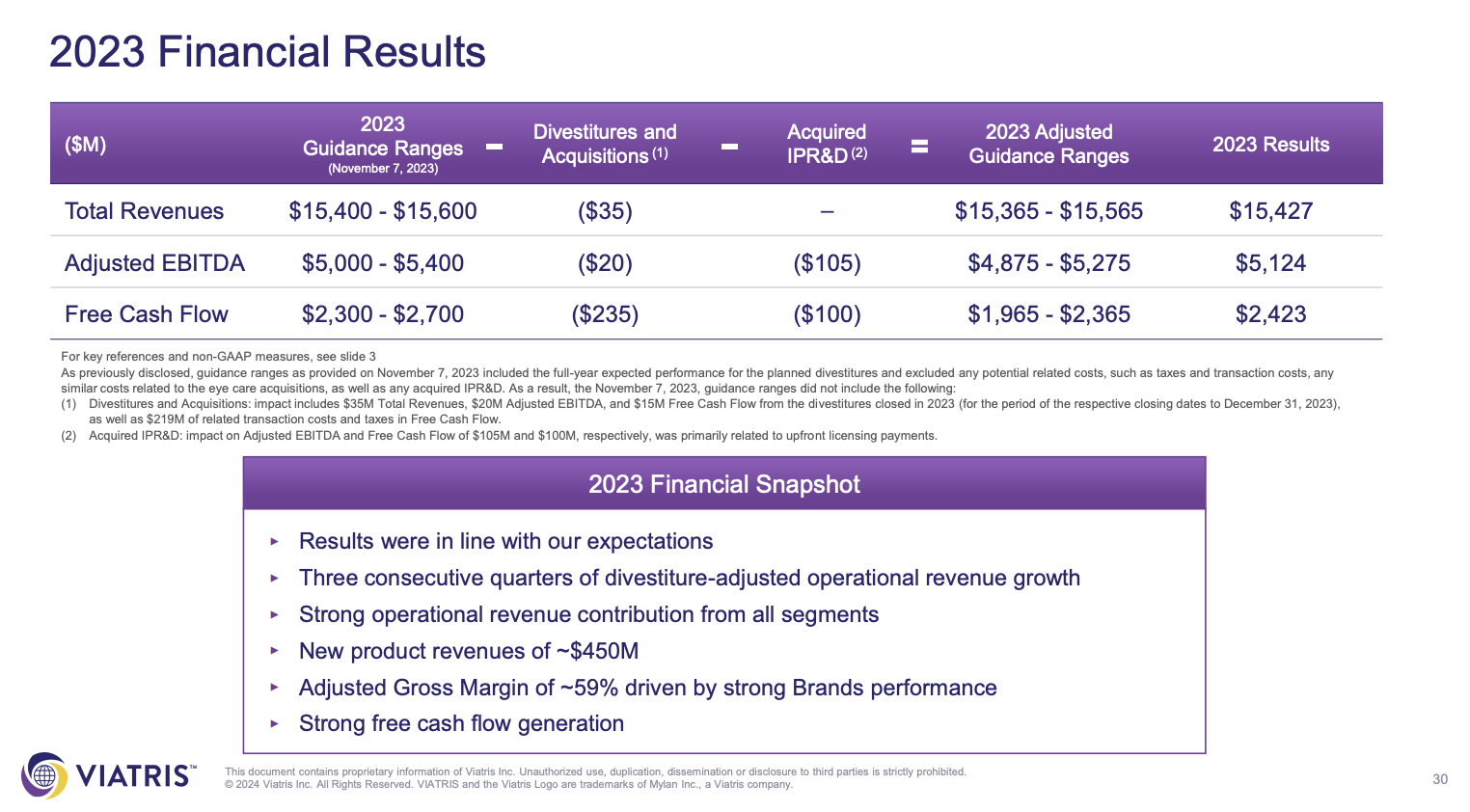

Divestitures played a significant role for the company, which impacted total revenue, EBITDA, free cash flow, and related financial metrics.

Using the data in the overview below, divestitures reduced revenues by $35 million. The impact on free cash flow was even bigger.

Viatris

The company is on track to complete all remaining divestitures by the middle of this year (subject to regulatory approvals), which means that starting next year, we'll see a bigger focus on organic growth.

Viatris believes it has a strong core business to grow earnings over time.

Essentially, it makes the case that its core business rests on three pillars.

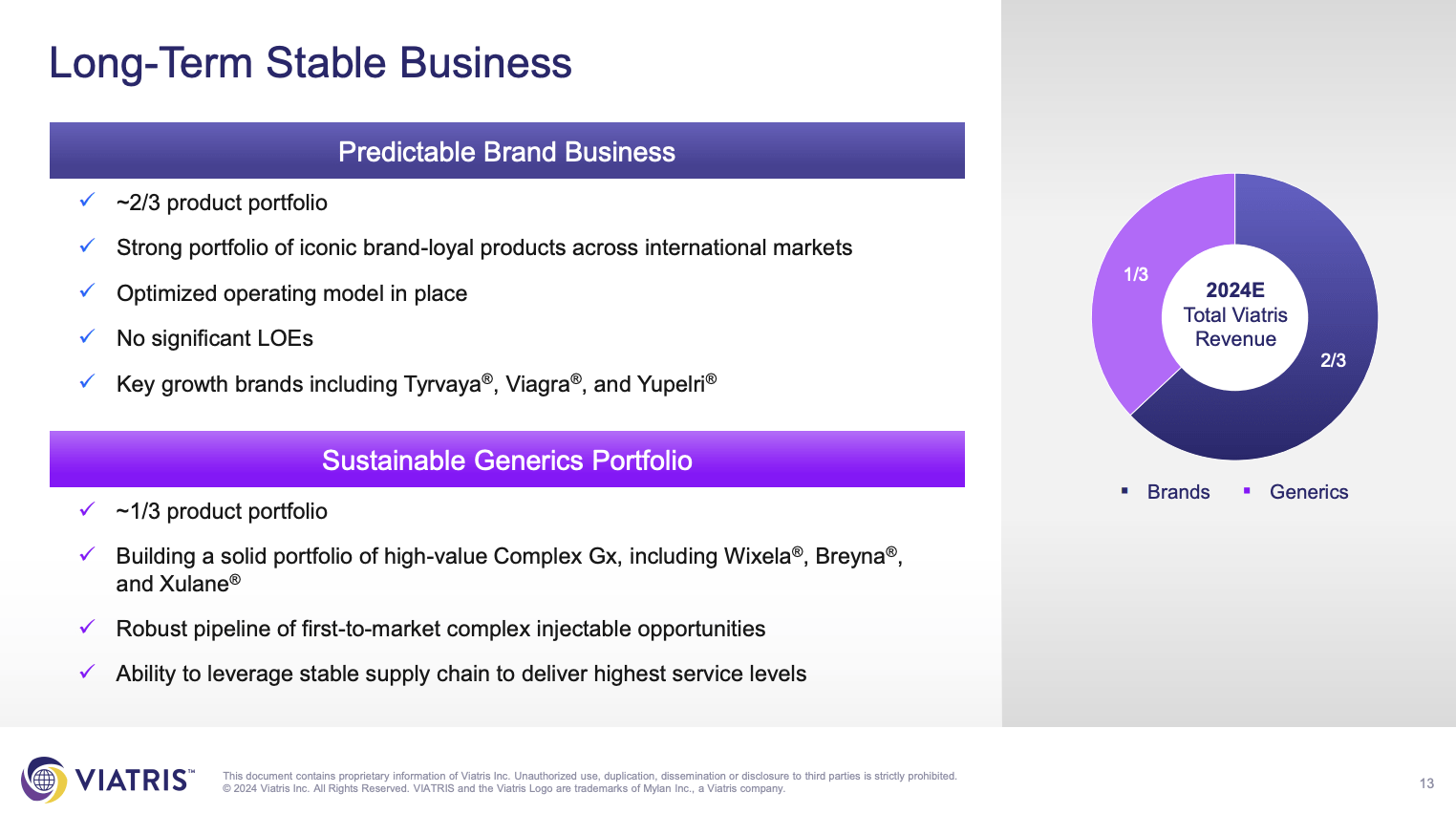

Firstly, the Brand business, which accounts for about two-thirds of the company's portfolio, sees modest growth driven by brands like Yupelri and Effexor.

This segment has subdued patent loss risks and an optimized operating model. In 2024, this business is expected to see 2% contraction due to "erosion."

Viatris

Secondly, the Generics business, which includes complex generics such as Wixela and Xulane, maintained stability due to geographic and portfolio diversity.

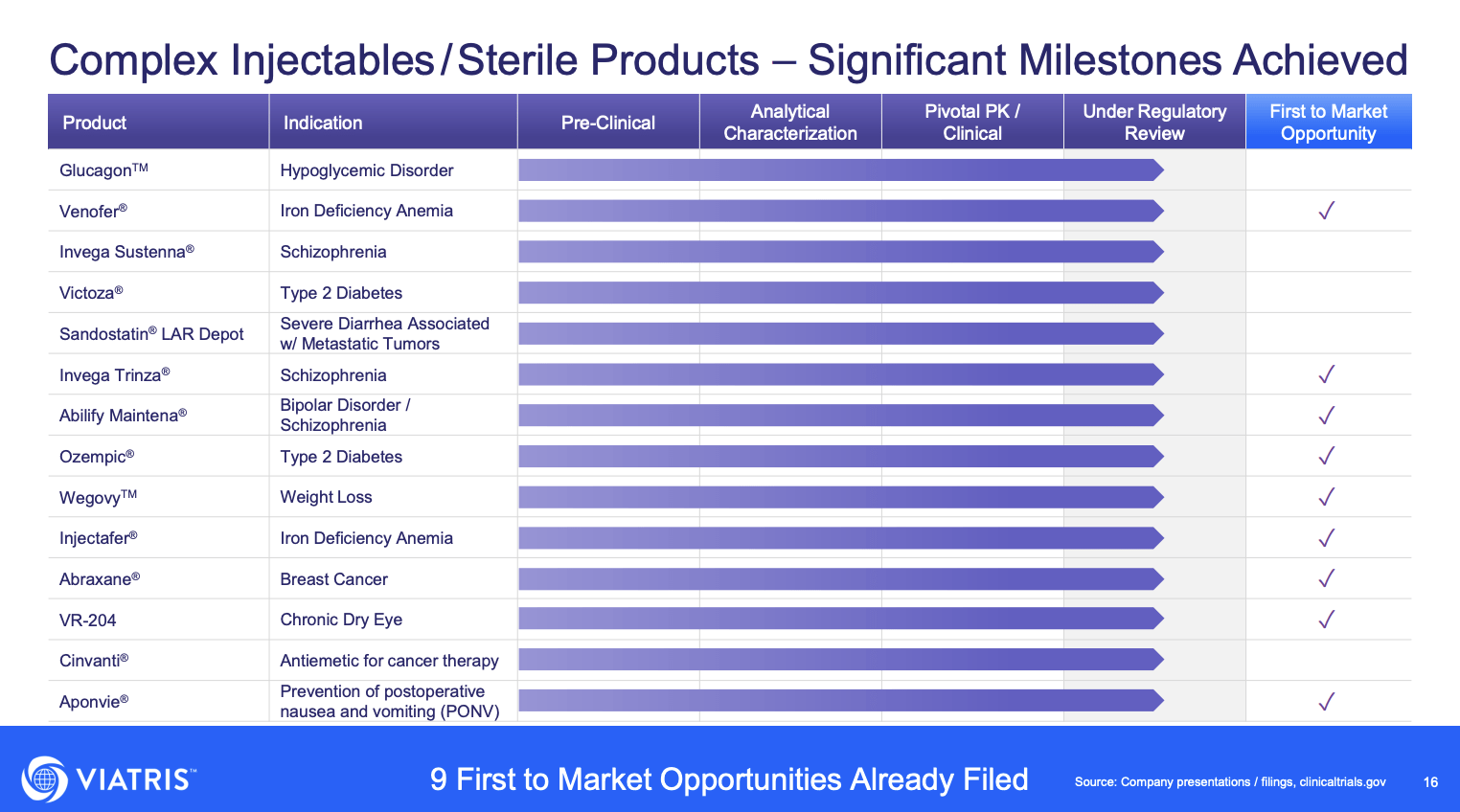

Lastly, the company's ability to execute on the pipeline is key, with significant progress in new product launches across various segments.

Speaking of its pipeline, the company used the earnings call to outline its expectations for 2024.

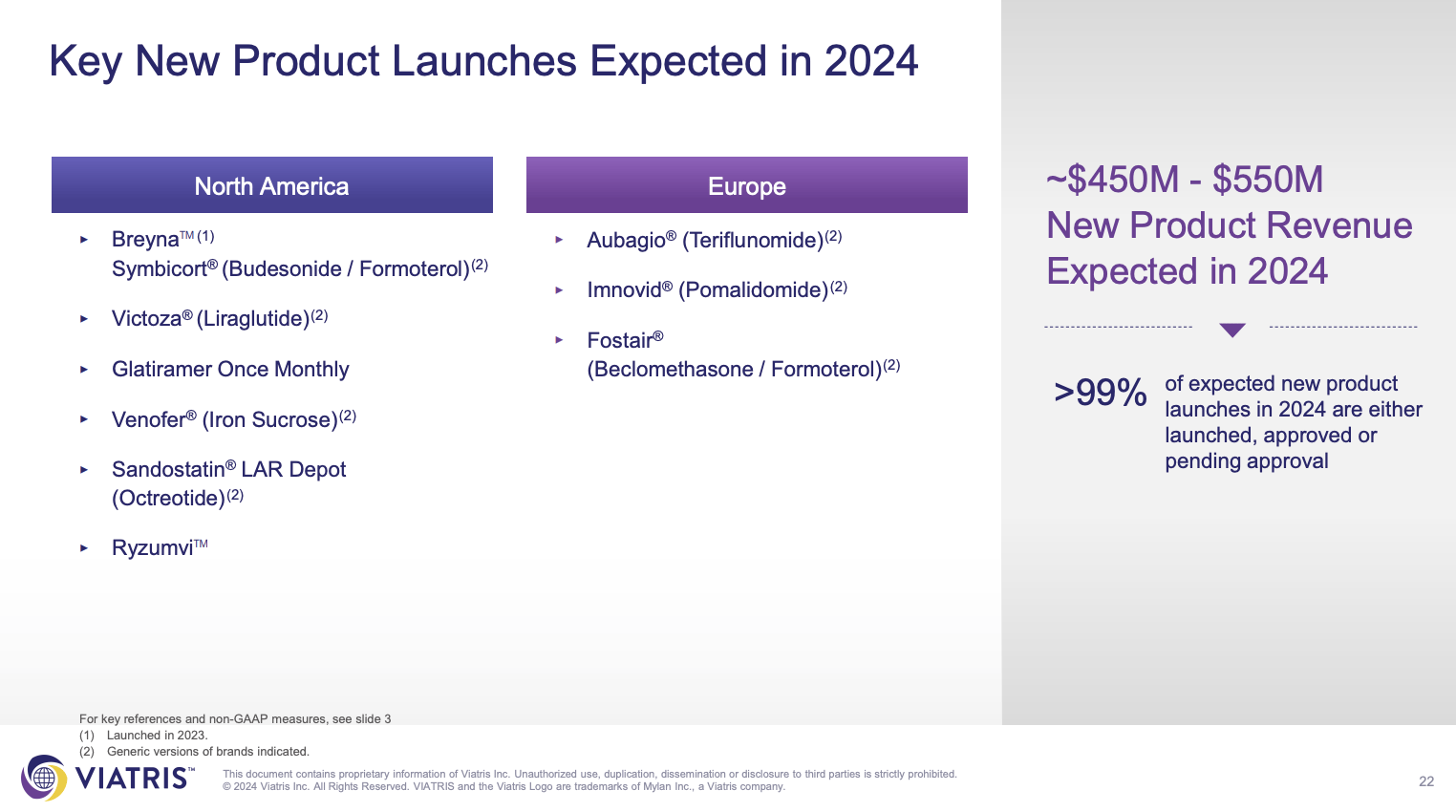

According to the company, Developed Markets are projected to grow, driven by strong performances in Europe and North America.

Europe is expected to be led by a strong brand portfolio, including products like Brufen and EpiPen, in addition to growth in key markets such as Italy and France.

Meanwhile, North America is expected to see growth driven by new launches of GA Depot, Liraglutide, and Sandostatin LAR, on top of strengthening positions in respiratory products like Wixela and Breyna.

Viatris

Emerging Markets are forecasted to experience growth primarily in the branded business, with projections indicating a 6% year-over-year increase.

However, the JANZ nations, which cover Japan, Australia, and New Zealand, are expected to decline by 8% due to government-driven price regulations.

Greater China is projected to see a 2% decline in 2024.

With regard to its pipeline, the company plans to continue delivering on its deep pipeline, including Sandostatin LAR, liraglutide, iron sucrose, and Ryzumvi, among others.

Viatris

Essentially, the company remains focused on progressing pipeline assets, with many in Phase 3 stages, particularly in eye care addressing vision-related disorders. This means that it could be close to commercialization.

From our eye care pipeline, we expect to launch Ryzumvi. And from our novel and 505(b)(2) pipeline, we are excited to bring to market our once-monthly, glatiramer acetate depot for patients with multiple sclerosis, and we are pleased to present our latest data this week at [indiscernible], a key medical conference. We also continue to be laser focused on progressing our other pipeline assets, many of which are in Phase 3 stages such as Xulane low dose, Meloxicam and Effexor GAD. We are especially excited about advancing our eye care pipeline that has several programs in a Phase 3 aimed at addressing vision-related disorders such as Presbyopia, Night Vision disturbances and Blepharitis. - VTRS 4Q23 Earnings Call (Emphasis Added)

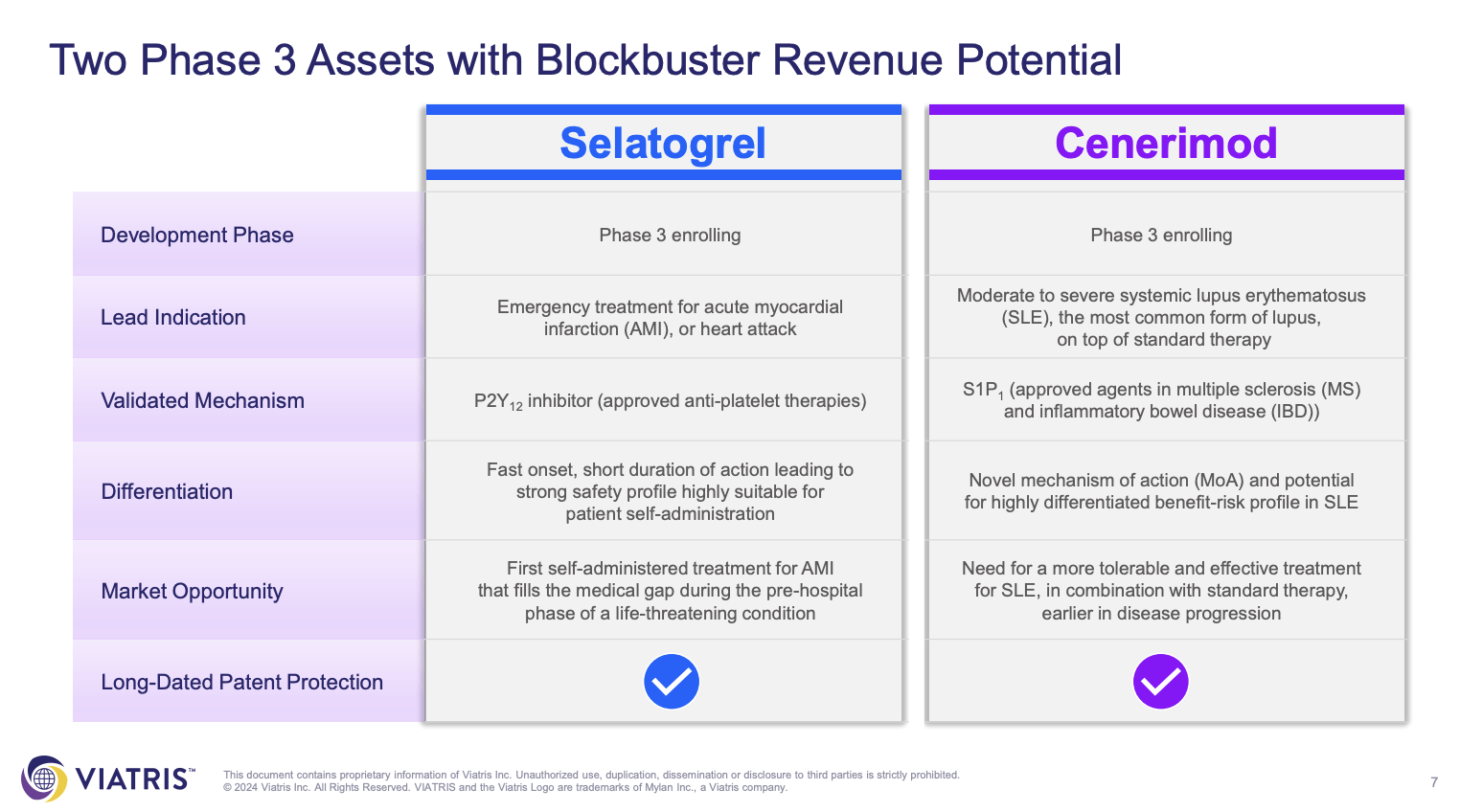

On top of that, the company is working on two "blockbuster" drugs, including Slatogrel and Cenerimod, which serve huge markets.

According to the company, it will receive exclusive global development and commercialization rights to these two assets.

Selatogrel is a potential life-saving self-administered medicine for patients at risk of recurring heart attack, while Cenerimod is a novel immunology drug that has the potential to be a first-in-class oral therapy for the treatment of SLE, which stands for systemic lupus erythematosus. That's an autoimmune disease.

Viatris

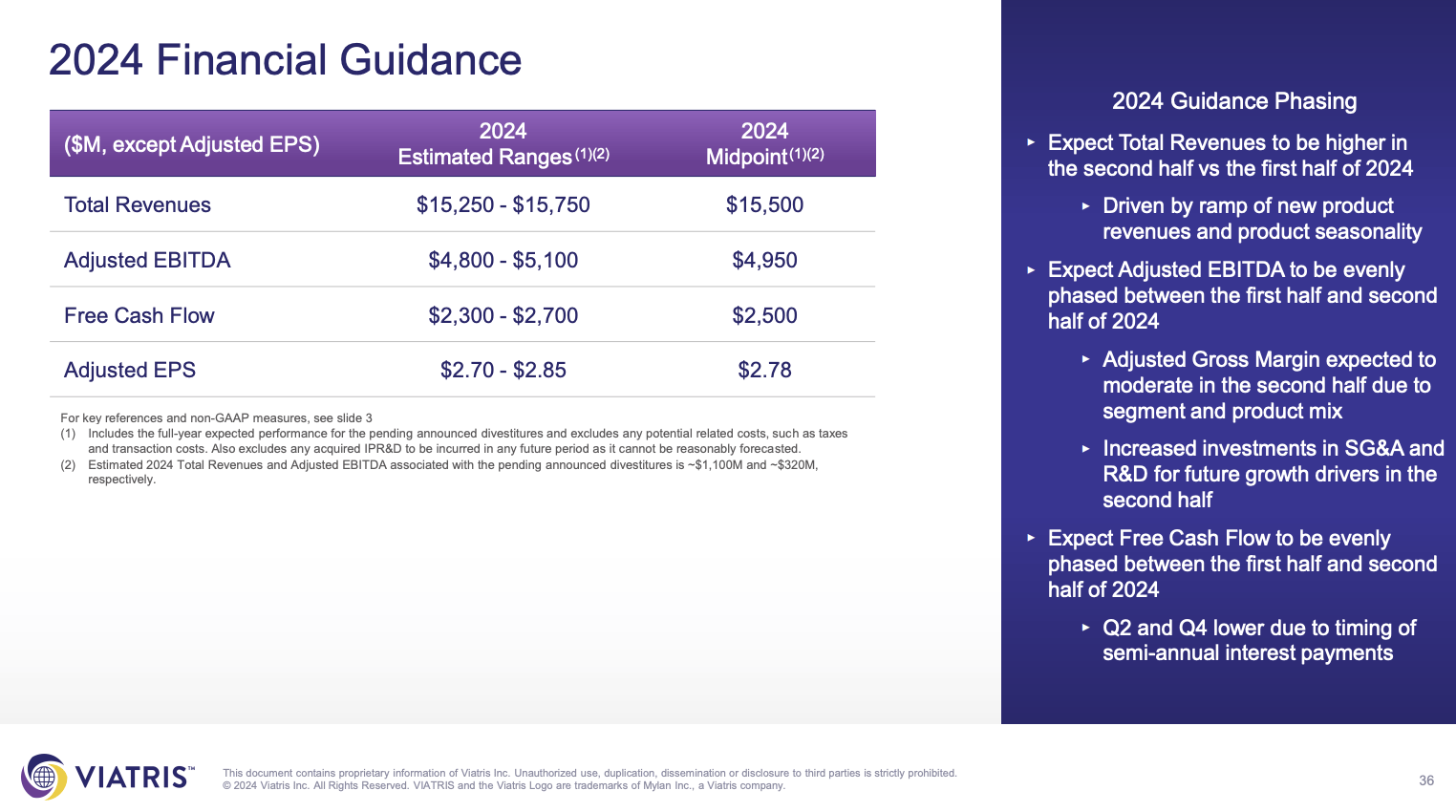

All things considered, for 2024, the company expects to generate at least $15.25 billion in revenues, including a 0% to 1% currency headwind.

Free cash flow is expected to be $2.5 billion with adjusted EPS of at least $2.70.

Viatris

To put these numbers in context, let's look at what this means for its valuation.

Analysts expect the company to see bottoming sales and related financial metrics in the years ahead.

This year, sales are expected to decline by just 1.3% to $4.9 billion, which includes divestitures. Next year, revenue growth is expected to be negative 1.1%.

The same goes for EBITDA contraction, which is expected to be in the low-single-digit range through 2025.

The good news is that free cash flow is expected to remain elevated, with $2.7 billion in expected 2025 free cash flow.

This would indicate a free cash flow yield of more than 18%. Even including $11.7 billion in 2025E net debt, the FCF yield would be north of 10%.

Leo Nelissen - Based On Analyst Estimates

In other words, the company, which has a 2025E net leverage ratio of 2.4x EBITDA, is in a great position to rapidly reduce debt, lowering financial risks and paving a path for more sustainable shareholder distribution growth.

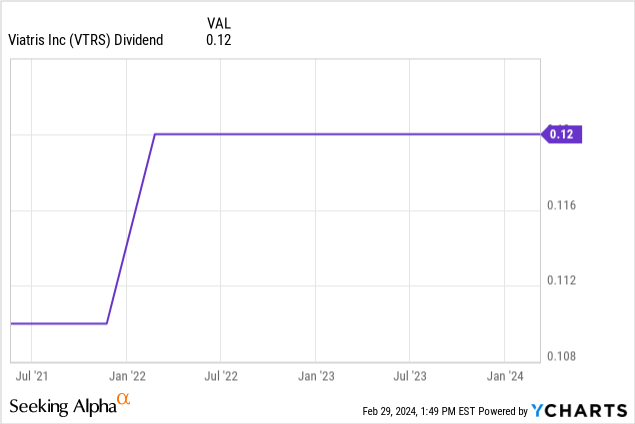

Currently, VTRS pays $0.12 per share per quarter in dividends, which translates to a yield of 3.9%.

These numbers also indicate a highly favorable valuation. As my valuation overview above shows, the company is trading at a 5.5x 2025E EBITDA multiple. Just like in my prior article, I believe that a 9x multiple is fair, which indicates roughly 60% upside from the current price.

As the consensus price target is $11.70, below its current share price, I'm an outlier compared to other analysts.

I believe the main difference between my target and the average target is that I'm looking far into the future, incorporating the company's potential growth path and use of free cash flow to lower net debt.

However, while I like the company's growth profile, it is far away from becoming a wealth compounder, which means investors need to be very careful here. Elevated return potential comes with elevated risks.

VTRS could turn into a huge money maker. However, its stock price could also suffer for a long time if the company struggles to bring new products to market and lower net debt as quickly as analysts expect.

So, please keep that in mind!

While consistent wealth compounders like Danaher provide steady returns, companies like AbbVie offer dividend growth with slightly higher volatility.

Then there are beaten-down value plays like Viatris, which, despite risks, can present significant value for patient investors.

VTRS's focus on debt reduction and strategic progress signals a promising future, supported by consistent revenues and elevated free cash flow.

While it may not be a wealth compounder yet, its potential for capital gains and a juicy dividend in the future make it worth considering, though investors should remain cautious given its elevated risks.

Pros:

Cons: