designer491

designer491

This is a follow-up to my previous TIPS articles, the most recent being Revisiting TIPS Returns in the Decade Ahead. TIPS real yields have come down from last October, but are still near 14-year highs, with the 10-year at 1.81%. The 10-year nominal Treasury bond yield is 4.13%, resulting in a breakeven inflation rate of 2.32%. If inflation exceeds this level, TIPS held to maturity will earn more than nominal Treasuries. It looks like a reasonable bet given the current inflation of 3.1% and the 30-year average rate of 3.8%.

FRED

However, there are some troubling factors. Elevated stock market valuations, weakening economic indicators, enormous federal debt, domestic and global unrest, and signs of a Fourth Turning should give pause to all but the most aggressive investors. My investment orientation is capital preservation, with a contrarian and value bent. I carry a substantial allocation to TIPS in my all-weather portfolio as described in my SA articles.

As such, I have become increasingly concerned about the potential for a "three-sigma" (rare, but possible) unfavorable financial environment. A reader of one of my TIPS articles recently posed this question: "What if rates go deeply negative next time?" This and the following questions are worth considering:

How will TIPS perform under duress? What if inflation surges or there is a deflationary depression? What if the government defaults on its debt, either explicitly or by devaluing it?

This article is for TIPS investors who share these concerns and who prioritize capital preservation and income over speculation.

First off, I will assume readers have a working knowledge of TIPS. They can be complex. If you aren't that familiar or would like to go deeper, I highly recommend the excellent TIPSwatch site authored by David Enna.

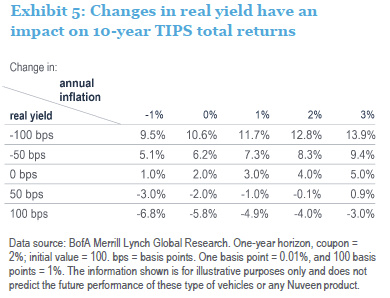

But here I'll share a few key points that will help frame the scenarios below. TIPS returns are driven by two main factors: changes in interest rates and changes in inflation expectations. These can work together or against each other, leading to very different results. The table below from a Fixed Income Perspective: Treasury Inflation-Protected Securities by Nuveen, illustrates the interplay.

Fixed Income Perspective: Treasury Inflation-Protected Securities, Nuveen

For example, if the real yield on the 10-year TIPS goes from 2% to 3% (100 basis points) and inflation goes up by three percentage points, the TIPS price change would be -3.0%. This shows how unfavorable rate increases can overwhelm the benefits of higher coupon payments from TIPS principal adjustments due to higher inflation.

Other return factors are investor risk appetites, TIPS supply, market liquidity, and investor funds flow. Ultimately, while one "can do the math," investor sentiment rules.

With this in mind, let's explore some extreme but possible scenarios and how TIPS might fare.

The pandemic, a once in a hundred-year event, provided us with a good example of what could happen. At its onset, the economy went into a deep recession, with unemployment reaching depression-era levels. The Federal government and the Fed responded with historic and massive stimulus.

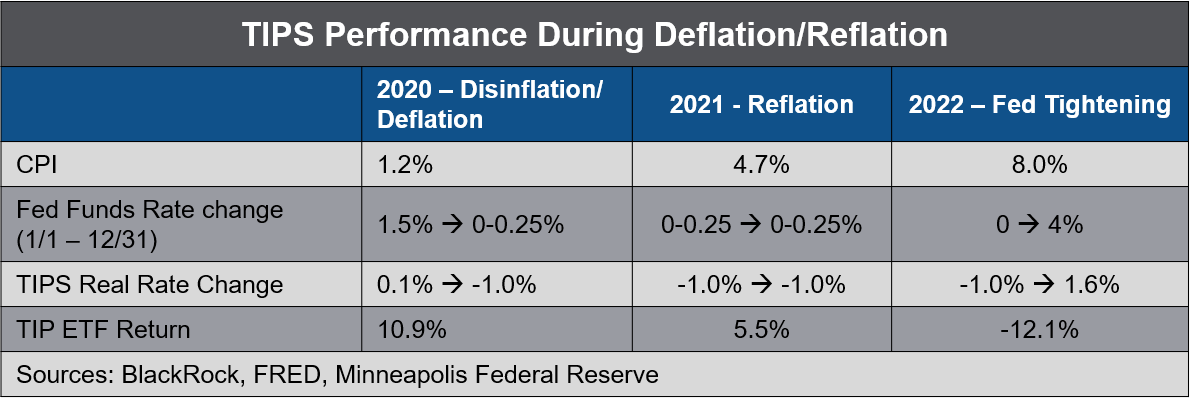

BlackRock, FRED, Minneapolis Federal Reserve

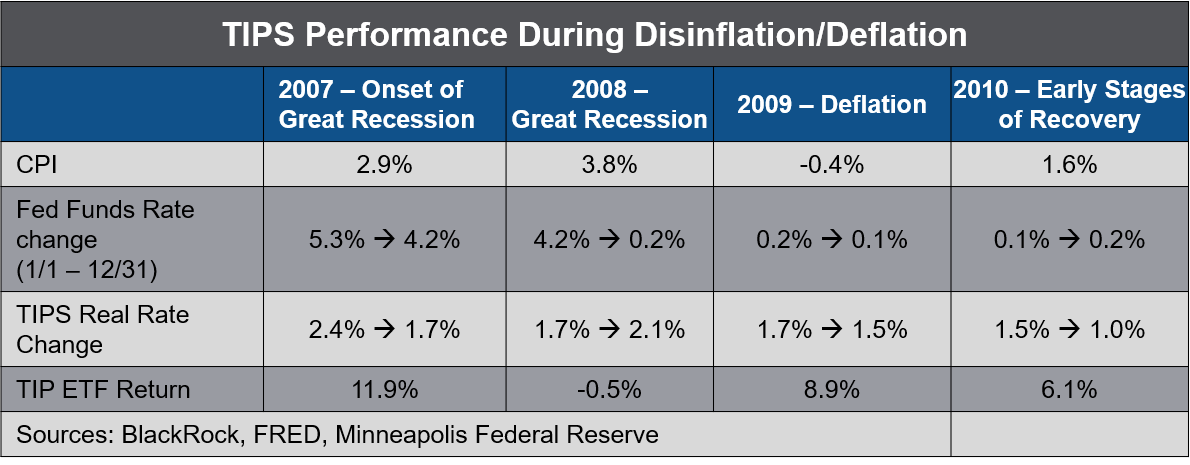

The table shows the behavior of inflation, the Fed funds rate, the TIPS real rate, and total returns for the TIP ETF (a reasonable proxy for TIPS returns). Initially, TIPS fared well, even though inflation declined in 2020 from an already quiescent 1.8% in 2019. TIPS' gain in 2020 was mostly due to the decline in the real rate from near zero to -1%, plus a modest coupon return.

The Fed maintained its zero-interest rate policy (ZIRP) throughout 2021. Inflation began to surge in 2021 and TIP gained about 6%. At its peak, annualized inflation reached 9%. After erroneously declaring "inflation is transitory," the Fed finally acted, raising the Fed Funds rate to 4%. As a result, longer-duration bonds, including TIPS, were hammered. Price declines wiped out the gains from higher inflation and TIP declined 12% in 2022.

Note that although nominal rates went up by four percentage points, the real rate moved up 2.6% percentage points. This smaller increase, along with the positive inflation adjustments to TIPS principal allowed them to outperform nominal Treasuries. For example, in 2022 the Vanguard Long-Term Treasury Index Fund ETF Shares (VGLT) declined 29% and the 10-year Treasury declined 15%.

This example demonstrates that TIPS performance in a surging inflation period depends largely on real rates. And the latter depends on market and Fed reactions.

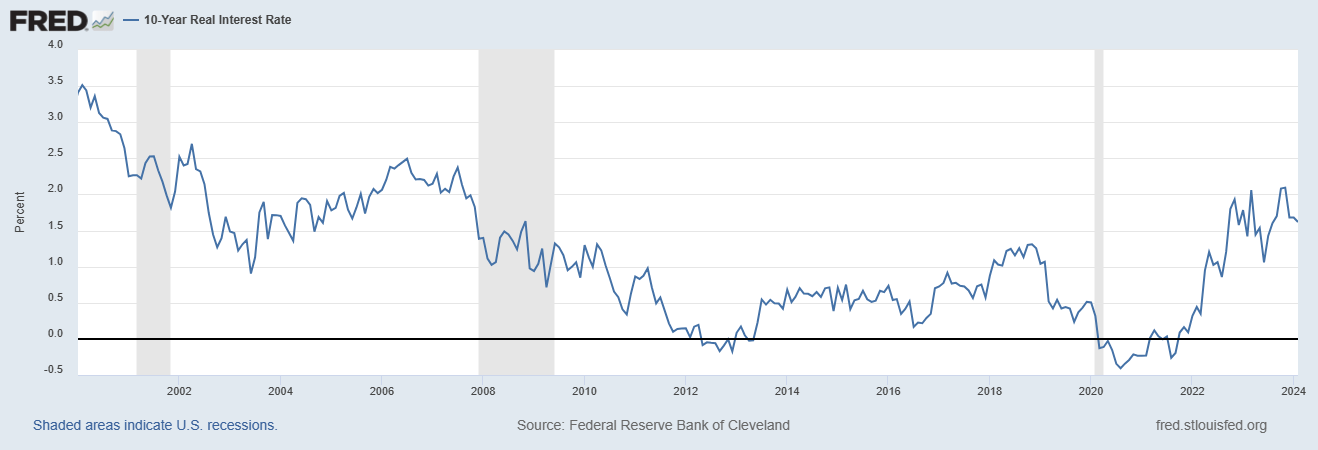

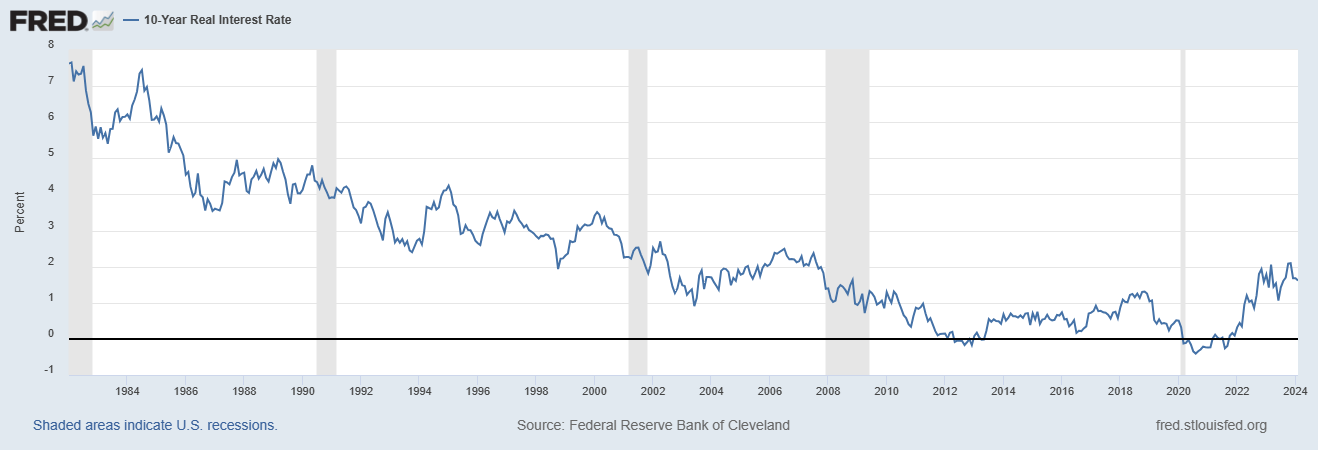

Let's consider what might happen if inflation surged again. This might occur after accommodative Fed policy in response to a recession. At some point, the Fed would be compelled to raise rates. Our example above and the Nuveen data show that what matters most is real rates. The chart below shows current real rates are near 14-year highs, but not as high as they got in response to the 1970s inflation surge.

FRED

For a full discussion, I refer you to Revisiting TIPS Potential in the Decade Ahead. There I explained why the Fed would be hard-pressed to come anywhere close to Paul Volcker's feat of raising the Funds rate to 22% with a real rate of 8%. This is due to the crushing effects of interest service on the gargantuan government debt and economic devastation. Could we really see inflation of 10% and a Fed Funds rate of 15% or more? It seems highly unlikely.

Nonetheless, let's play what if. Suppose the Funds rate reached 16% with 10% inflation. Using the duration calculation principle, if we applied the TIP ETF's duration of 6.75 to a real rate increase of 4 percentage points, from about 2% now, the price decline could be on the order of 27% (4% times 6.75). This would deal a major blow to TIPS ETF holders, especially those who needed to sell to raise cash. Thankfully, the decline would be partially offset by inflation adjustments to the TIPS principal. An annualized 10% inflation adjustment could reduce the total return to the 15-20% range.

Although TIPS ETFs would likely experience substantial losses in the above scenario, there is an alternative. I explored this in TIPS Funds Versus a Ladder. Owners of TIPS bonds who hold to maturity would be immune from a price drop unless they had to sell. Individual bonds would continue to earn the real rate at the time of purchase plus the inflation rate. Granted, those investors would incur an opportunity cost by not enjoying the higher market-based real rates.

If inflation and rates did surge, the resulting higher nominal rates would eventually allow patient investors to recoup paper losses. So, the holding period is an important consideration.

Another way to reduce the interest-rate risk of TIPS is to buy shorter duration. Investors could do this via a fund or ETF such as Vanguard Short-Term Inflation-Protected Securities Index Fund ETF Shares (VTIP) or iShares 0-5 Year TIPS Bond ETF (STIP). Both presently have a real yield of about 2%. According to Nuveen, the TIPS 1-10-year index has just 69% of the duration of the full-duration index with slightly greater return potential and 22% lower volatility. Short-term TIPS also have a higher inflation correlation.

Now let's consider how TIPS might perform during a deflationary depression. Again, we can look to history as our guide. The economy experienced the most severe, prolonged economic decline since the 1930s Great Depression during the Great Recession of 2007-2009. There were also some similarities between this period and the pandemic recession given there was deflation. However, the Great Recession lasted much longer and didn't lead to high inflation afterward.

Author, BlackRock, FRED, Minneapolis Federal Reserve

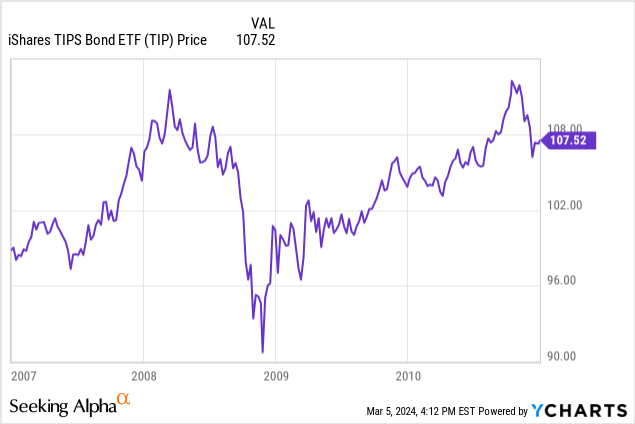

A credit crisis emerged in August 2007 when two Bear Stearns hedge funds failed. TIPS performed well throughout 2007. However, in the summer of 2008, Lehman Brothers announced a second quarter loss of $2.8B. This was followed by bankruptcy and a stock plunge in September. Equity markets worldwide plummeted, as did TIPS.

Ycharts via SeekingAlpha

How can we explain this when TIPS are supposedly a virtually risk-free asset? I dug up an old Advisor Perspectives article that may have unlocked the answer:

We view the experience with TIPS yields after the Lehman bankruptcy as the sign of a highly abnormal market situation, where liquidity problems suddenly created severe financial anomalies. This may seem to imply that we can take the recent episode as unrepresentative and ignore the observations from these dates. And yet, investors in TIPS who would like to regard them as the safest long-term investments must consider the extraordinary short-term volatility that such events have given their yields."

More specifically, Lehman was one of the largest TIPS holders and caused a market dislocation due to forced selling. The crisis triggered a cascade of other sellers in the relatively illiquid TIPS market. As a result, the TIP ETF suffered a peak-to-trough decline of 17%. However, after recovering late in the year, the TIP ETF ended down only 0.5% for the full year.

In contrast to our first scenario, although the Fed aggressively lowered the Funds rate from 4% to zero in 2008, TIPS real rates increased slightly. Therefore, TIPS didn't benefit from monetary policy easing. At one point CPI ran at -2.5% on an annualized basis and 10-year inflation expectations declined to nearly zero, further pressuring TIPS.

In 2009, amid the beginnings of economic recovery, even though there was deflation TIP gained 9%. The economic recovery continued in 2010 with a return to modest inflation, leading to a TIP gain of 6%.

The Great Recession demonstrates the vagaries of the financial markets. One wouldn't expect a virtually risk-free asset to decline so much and so fast. And during a full year of deflation in 2009, TIPS somehow gained 9%. Perhaps the Lehman Brothers dislocation was a one-off event. Regardless, this piece of history shows us that TIPS can have a sudden, dramatic double-digit decline in the event of a market panic.

FRED

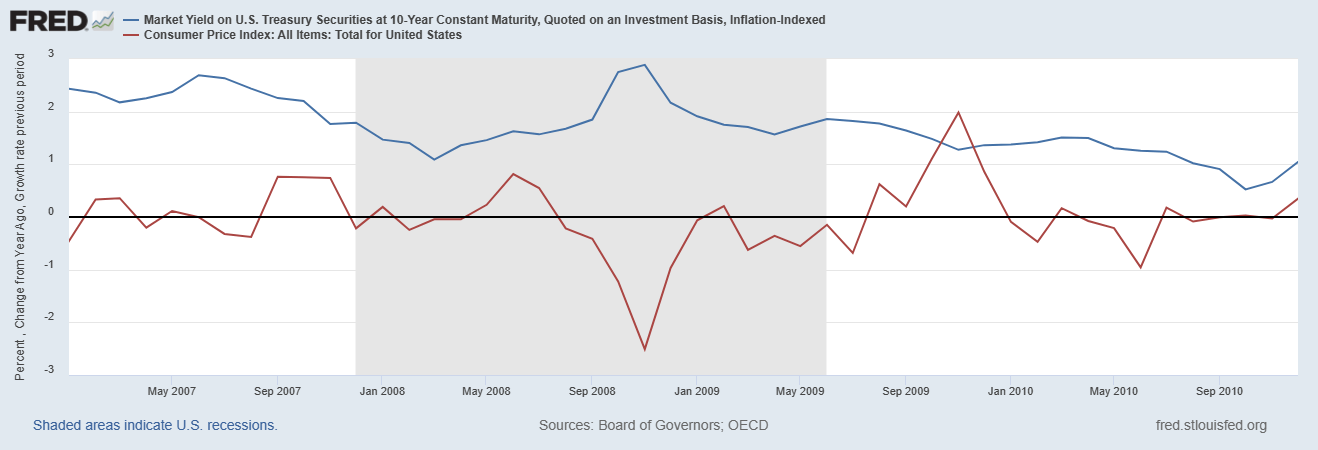

In summary, the chart above shows real rates trended gently downward over the period, helping TIPS. A surprising fact is that long-term TIPS have a correlation with inflation of -10% over the ten years ending 2022, according to a paper by State Street Global Advisors. That's because duration effects have dominated. As a result, buy and hold TIPS investors fared well during this deflationary depression period. TIPS had positive returns each year from 2007-2010, except for a slight decline in 2008. The TIP ETF recovered to its pre-recession price level by 2010.

Now let's consider the reader's question. This happened in Europe and Japan not too many years ago, so there is a precedent that it could happen in the U.S.

Let's consider an example where nominal rates go to -2% and inflation runs at 0% due to a weak economy. This produces a real rate of -2%. Once again, the duration effect can give us an idea of potential price change. A four-percentage point drop (2% real rate moving to -2%) coupled with the TIP ETF's duration of 6.75 suggests a price increase of approximately 27%. However, zero inflation would take away the inflation adjustment benefit.

There are two means of government default: failure to make scheduled payments and devaluing the currency.

While theoretically possible, it's unlikely the U.S. government would ever fail to make its interest payments. Unless the currency loses its reserve status and international investors completely lose confidence, the Fed can be the buyer of last resort. However, there is still a possibility of a currency collapse. As Ray Dalio stated in his Changing World Order Series:

Of the roughly 750 currencies that have existed since 1700, only about 20% remain, and of those that remain all have been devalued."

The watershed book, This Time is Different, Eight Centuries of Financial Folly, by Rogoff and Reinhart is instructive. Their research on more than 66 countries over eight centuries demonstrates when debt reaches such levels where it cannot be paid off in today's real dollars, most governments have inflated their way out of it.

Based on the world dominance of the dollar and the lack of a viable alternative, my bet would be on devaluation (stealth default) rather than outright default. In fact, it is already happening. Just look at the value of the dollar relative to gold. Given that most major countries are devaluing their currencies, the dollar has held its own on a relative basis. Rising inflation and a declining dollar erode the real value of nominal bonds and TIPS. However, TIPS may fare better due to inflation adjustments.

Nonetheless, I wouldn't view TIPS as a great portfolio hedge against a currency collapse. Rather my preferred vehicle is real assets. I discussed this in The Case for $5,000 Gold and Natural Resources Equities: Preparing for Reflation and Dollar Decline.

Investing is humbling. Although we can apply financial logic and study history to gauge what might happen to TIPS in unusual circumstances, the markets have a way of surprising even the best and brightest investors. Ray Dalio tells the story of how he was clerking on the New York Stock Exchange in 1971 after Nixon removed the dollar from the gold standard. He expected pandemonium and a market selloff. But shockingly, the market rallied 4% the next day.

My 40+ years of hard investing lessons and study of history have led me to employ an all-weather portfolio. In my SA series, I've reviewed how different asset classes have performed under different scenarios, and how asset class diversification creates a smoother ride for patient, long-term investors.

In my previous Revisiting TIPS Returns in the Decade Ahead I showed why TIPS could return 4-7% per year. They are a useful component of an investment portfolio. TIPS have excellent diversification benefits, and relative safety and presently earn real yields near 14-year highs.

However, there is a downside risk associated with an extreme financial environment. Based on this analysis, the maximum annual drawdown for TIPS could be in the 15% range. Such risks can be mitigated by buying and holding individual TIPS bonds to maturity or by shortening maturities. History shows that even the smartest investors are susceptible to unforeseen events. As such, a useful approach is to temper the weight of any given asset class and employ an all-weather portfolio.

As I've described in TIPS Funds Versus a Ladder, I prefer to own individual bonds, rather than an ETF or conventional mutual fund.