digihelion

digihelion

Vista Outdoor (NYSE:VSTO) manufactures shooting sports products. VSTO recently announced its Q3 FY24 results, and I will analyze it in this report. Its valuation looks good, but the expectations for the upcoming quarter aren’t good, which can adversely affect its share price. In addition, its technical chart provides no buying opportunity. So, I see no buying opportunity in VSTO for now. Hence, I assign a hold rating on VSTO.

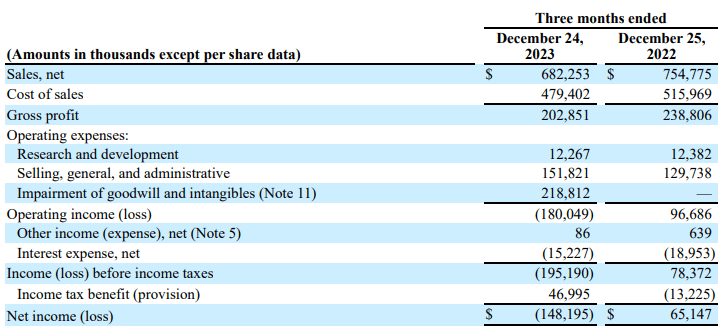

VSTO recently posted its Q3 FY24 results. The sales for Q3 FY24 were $682.2 million, a decline of 9.6% compared to Q3 FY23. Its Kinetic Group and Revelyst segment underperformed, leading to a decline in sales. The sales from The Kinetic Group declined 9% in Q3 FY24 compared to Q3 FY23. The main reason for the decline was lower shipment across all categories. The revenue from the Revelyst segment declined 10% in Q3 FY24 compared to Q3 FY23. The major reason for the decline was increased discounting and unfavorable mix. Its gross profit margin for Q3 FY24 was 29.7%, which was 31.6% in Q3 FY23. The major reasons for the margin decline were higher input cost, lower volume, and lower selling price.

Seeking Alpha

It incurred a goodwill cost of $218.8 million in Q3 FY24. So excluding this charge, the adjusted net income for Q3 FY24 was $48 million, which was $65 million in Q3 FY23. The numbers clearly show weakness. However, I think we might see better margins in the coming quarters because the freight costs are continuing to decline, which will lower its inventory costs. In addition, the management said that the purpose of giving higher discounts in this quarter was to work through its high-priced inventory, and it saw success. So we might see lower discounts in the coming quarters. But despite the higher margin expectations, I think we might continue to see weakness in the upcoming quarter due to low sales expectations. The management is expecting its FY24 sales to be around $2.77 billion, which is 10% lower than FY23 sales. So, the weak sales guidance can adversely affect its share price, and considering normalized channel inventories, we might see weakness in the sales growth.

Trading View

VSTO is trading at $29.5. This stock has been trading sideways completely for the last 20 months. It has been consolidating between $23 and $32 since June 2022. However, it broke out of the $32 level in September 2023, but it turned out to be a false breakout. The stock price immediately reversed after giving the breakout. In my opinion, this stock is in a no-trading zone because it might continue to consolidate between the $23-$32 level in the coming times, and the consolidation can be a bit long. So, investing in it at its current level might get your money stuck, and no one knows how long the consolidation will last. So I would advise you to avoid it. We will only see a fresh upward momentum in the stock once it breaks the $32 level.

The valuation of VSTO looks cheap. VSTO has a P/E [FWD] ratio of 12.94x, which is lower than the sector median of 16.30x. However, the valuation is not the problem here. The problem here is expected weakness in the upcoming quarter. The management expects its sales to be down, which creates a negative sentiment, and despite the low valuation, we might see its share price under pressure. In addition, its stock price is in a no-trading zone. Hence, I think one should avoid it. So, I assign a hold rating on VSTO.

The outdoor sporting and recreation market in the United States is served by a somewhat concentrated retail and distribution sector. In the fiscal year 2023, sales to their top 10 clients made up roughly 33% of their total net sales. In the future, the retail and distribution sectors in the United States may see even more consolidation, which would concentrate their consumer base even more. They typically don't have long-term sales agreements with their consumers, as is customary in the markets in which they compete. They are, therefore, reliant on specific purchasing orders. Consequently, these retail clients can modify the conditions of their business relationships, postpone purchases, cancel orders, alter purchase quantities from predicted volumes, or stop buying their items completely before acceptance. Additionally, they sell their consumers things on credit, which puts them at risk financially if those customers experience credit issues, insolvency, or other financial setbacks.

VSTO’s quarterly results were weak, and the guidance is also weak, which I think can affect its share price. We might see better margins, but the sales growth expectations aren’t positive. In addition, its technical chart suggests that it is currently in a no-trading zone. Hence, I see no buying opportunity in it for now. So, I assign a hold rating on VSTO.