Anastasia Turshina/iStock via Getty Images

Anastasia Turshina/iStock via Getty Images

Victoria's Secret (NYSE:VSCO), a renowned fashion retailer established in 1977, epitomizes glamour and sophistication in the lingerie industry. With its iconic fashion shows and globally recognized brand, Victoria's Secret has become synonymous with luxury and feminine allure. Offering a wide array of lingerie, sleepwear, and beauty products, the company caters to women seeking elegance and confidence. Despite recent shifts in consumer preferences and societal trends, Victoria's Secret continues to innovate, embracing inclusivity and diversity in its marketing campaigns. Through its distinct blend of style and sensuality, Victoria's Secret remains a leading force in empowering women to embrace their individuality with grace and poise.

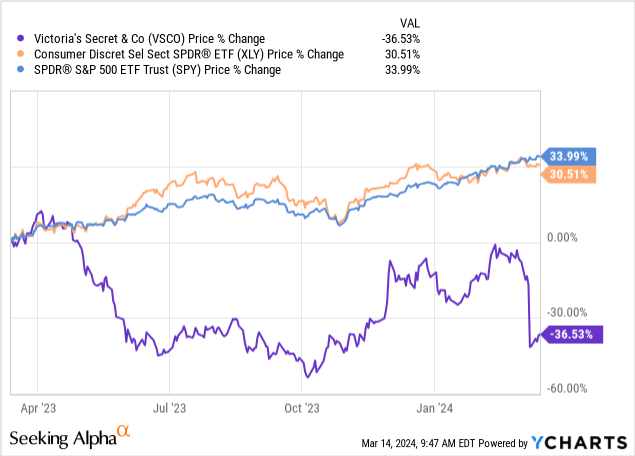

In recent weeks, the performance of VSCO's stock has been lackluster. The company has witnessed a notable decline of over 37% in market value over the past month, significantly underperforming both the broader market and the consumer discretionary sector.

In September 2023, we published an article on Seeking Alpha expressing our bearish perspective on VSCO. Our analysis centered on the company's deteriorating financial performance, including declining net sales and operating income, coupled with weak fundamentals. Additionally, macroeconomic challenges such as subdued consumer sentiment and heightened inflation levels have further impacted the company's prospects in recent years.

Today, we revisit VSCO to provide an updated assessment. Our analysis will focus on the latest earnings results, alongside fundamental metrics and valuation considerations

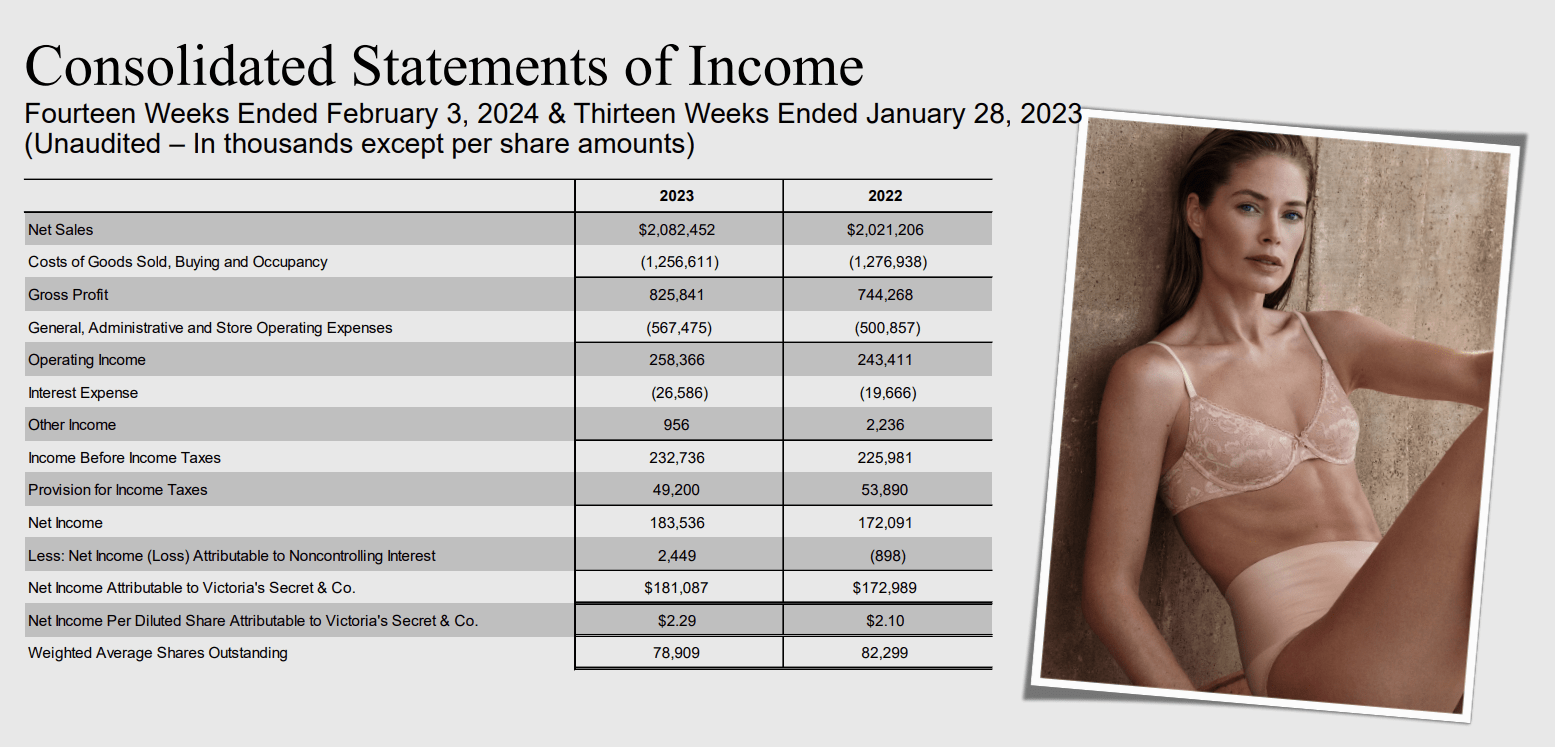

VSCO has delivered relatively lackluster Q4 results in early March. In the 14-week fourth quarter of 2023, net sales fell into the firm’s guidance range and amounted to $2.082 billion, marking a 3% increase from the $2.021 billion recorded in the 13-week fourth quarter of 2022. However, total comparable sales experienced a 6% decline compared to the previous year. Moreover, we also find it quite worrying that the intimates market sales in North America as a whole fell mid-single digits in the fourth quarter compared to the same period in the prior year, marking the fourth consecutive quarterly decrease YoY. On the costs side, there have been also negative developments, especially when looking at the SG&A expenses, which grew to 26.4% of sales, compared to 23.7% in the prior year. This expense growth has been driven also by the additional week in Q4 2023, the inclusion of Adore Me in the results, as well as the technology investments that are dedicated to boost digital presence.

When looking at the full year results, there are even less things to be happy about. Total comparable sales for 2023 have declined by 9%, while adjusted net income per diluted share for the 53-week fiscal year 2023 was $2.27, in contrast to adjusted net income per diluted share of $4.95 for the 52-week fiscal year 2022. The firm’s free cash flow has also declined markedly, driven by growth in CAPEX and decrease in cash flow from operations.

On the positive side, we have to mention that VSCO has managed to keep its market share of roughly 20% and remains the market leader in the intimates category. Also important to note that the firm’s international sales have increased by as much as 24%, mainly driven by the demand in China. The firm has also managed to improve its profitability, at least in terms of the gross profit margin, as a result of the modernized supply chain model, lower freight costs, favorable merchandise mix and disciplined inventory management.

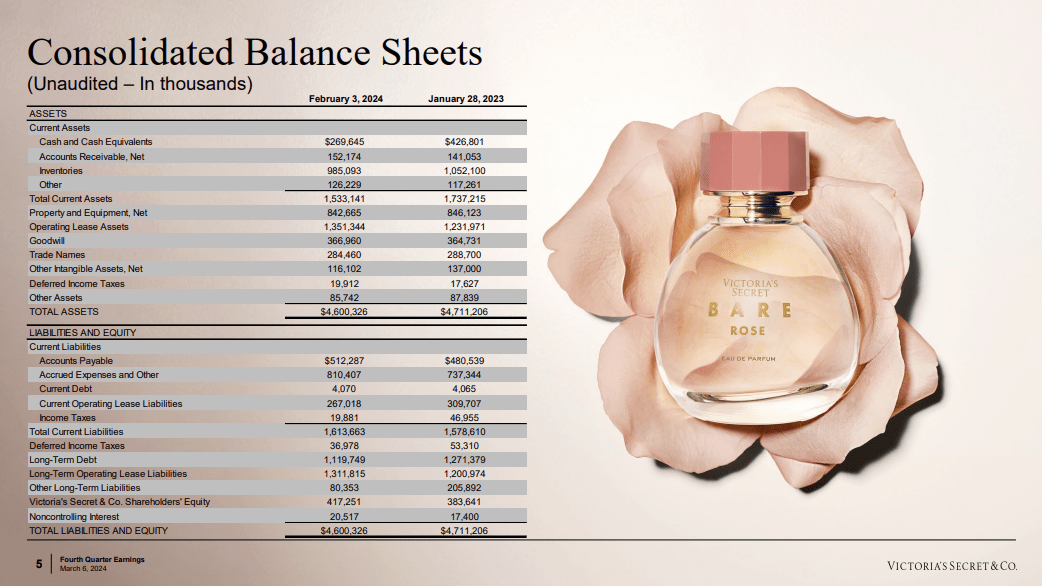

Income statement (VSCO) Free cash flow (VSCO) Balance sheet (VSCO)

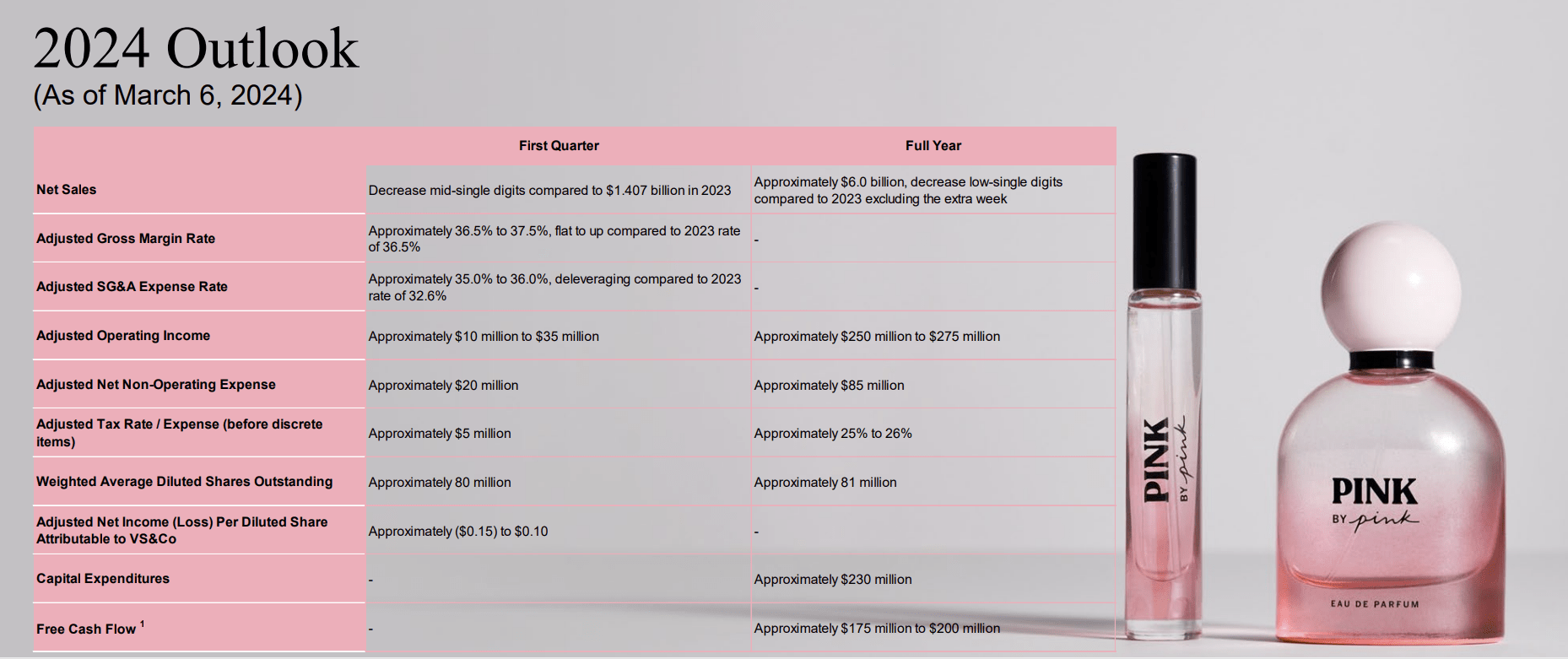

Looking forward, we cannot be too optimistic about the 2024 outlook provided by the management in terms of sales. Sales are forecasted to remain weak and decrease mid-single digits in the coming quarter and low-single digits in the coming year.

Outlook (VSCO)

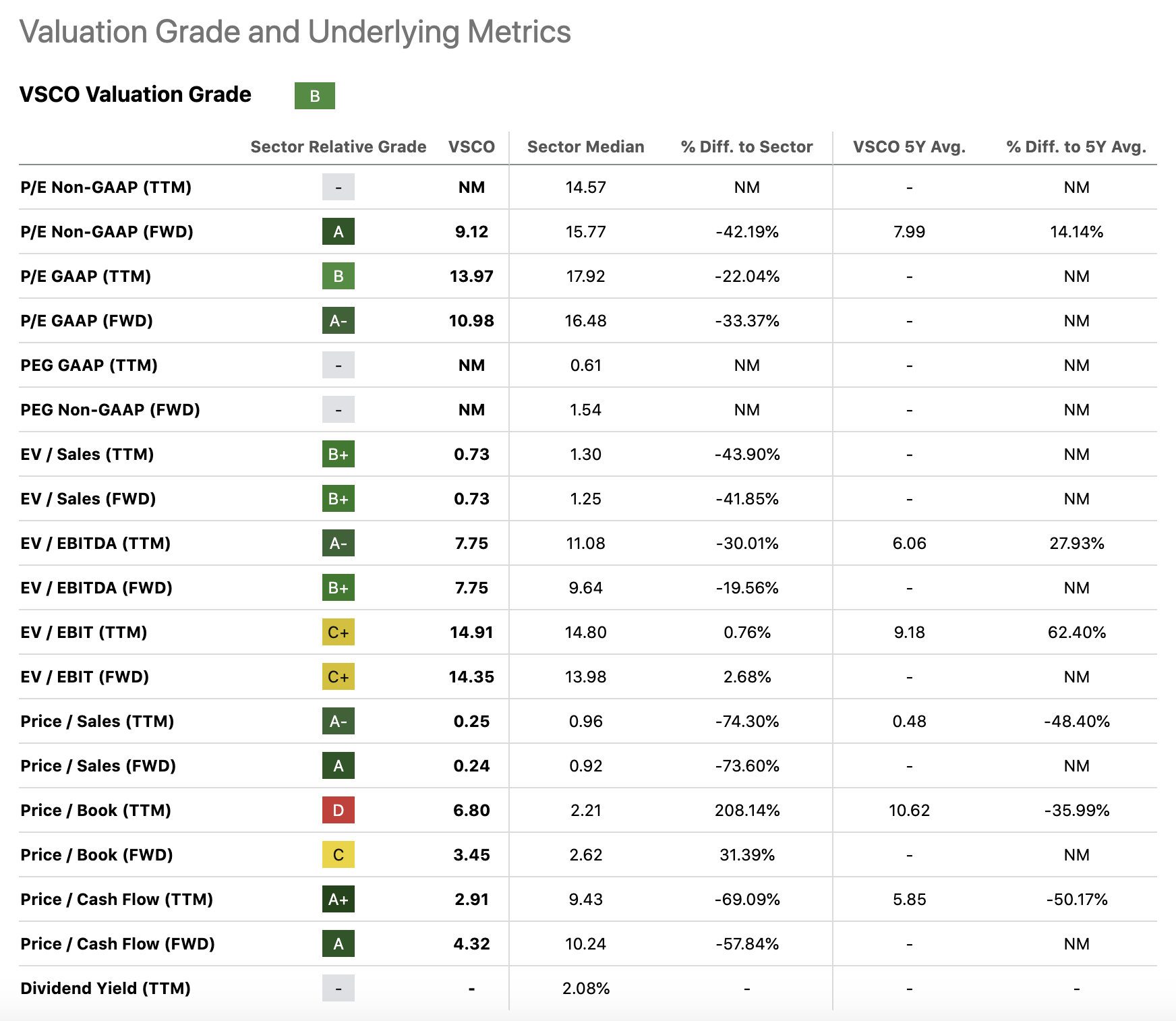

To evaluate the attractiveness of VSCO's stock from a valuation standpoint, we will analyze a series of conventional price multiples. Our objective is to assess whether VSCO's stock presents an appealing investment opportunity relative to its industry peers and competitors, as well as in comparison to its historical valuation. The subsequent table juxtaposes VSCO's valuation metrics with the median metrics of the consumer discretionary sector and its own five-year averages (where exists).

Valuation (Seeking Alpha)

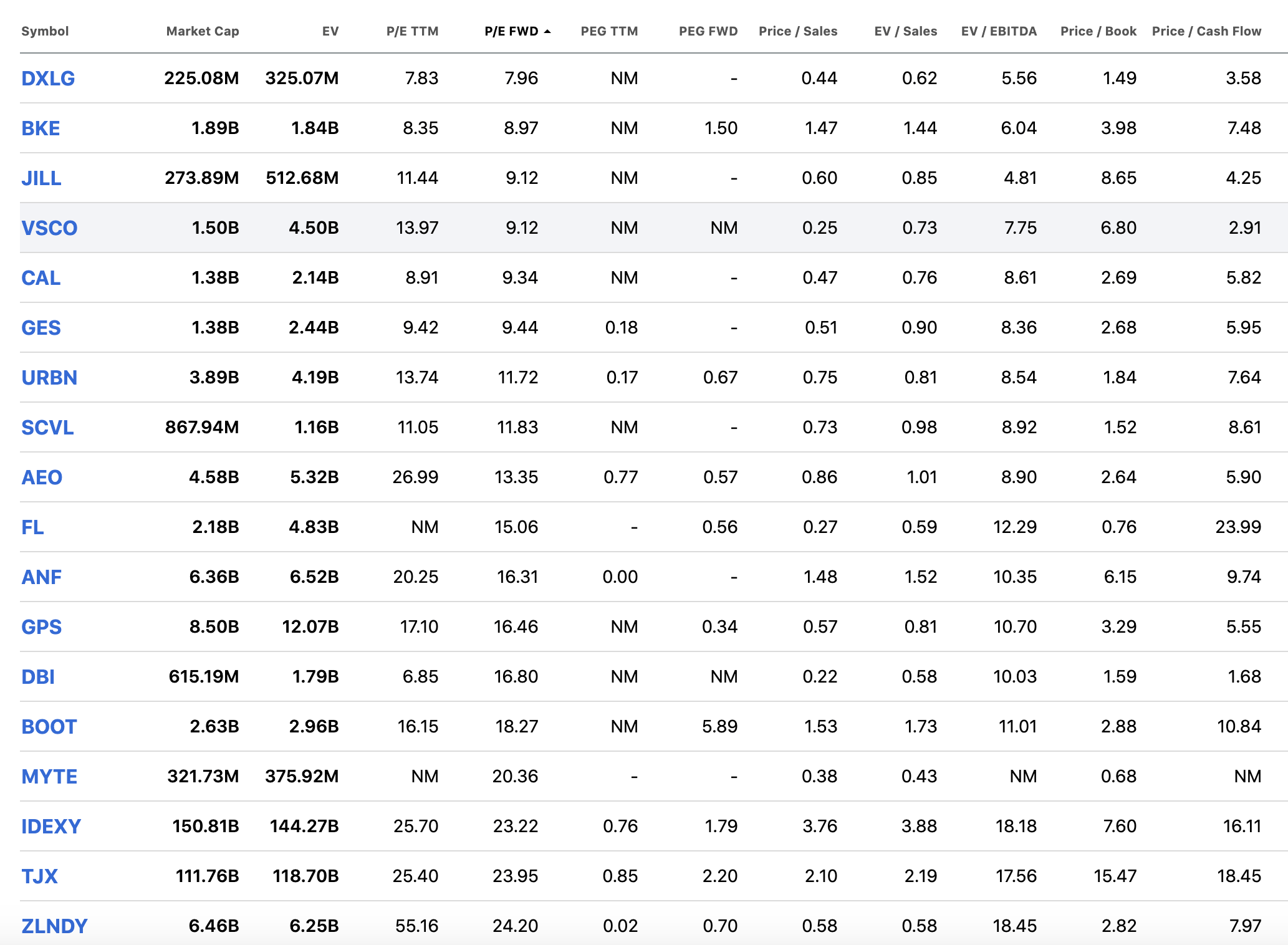

As the consumer discretionary sector may be too broad for meaningful comparisons, we are shrinking the peer group to the apparel retail industry.

Comparison (Seeking Alpha)

Within the industry, VSCO has one of the lowest valuation metrics. Even in our previous writing, we have pointed out that the company appears attractive from a valuation perspective, but we have highlighted that it is largely driven by the weak fundamentals and poor financial performance. At that time, we believed that VSCO’s stock is likely a value trap and a discount to the rest of the industry is justified.

When looking at the guidance for the coming quarter and full year 2024, there is also little to get excited about. Net sales are expected to decline and SG&A expenses are expected to rise, putting downward pressure on the profitability. We do not see significant tailwinds that could provide a material upside from the current price levels.

All in all, we believe that it is still not worth owning VSCO's stock. We would like to see the demand for the firm's products growing and its sales increasing on a global level. For now, we maintain our bearish view.