Solskin/DigitalVision via Getty Images

Solskin/DigitalVision via Getty Images

Vertex Pharmaceuticals (NASDAQ:VRTX) is a promising biotechnology with solid financial results in 2023, a dominant Cystic fibrosis ("CF") franchise, and is on track to diversify its drug portfolio by launching five new products by 2028, which include its newest CF drug, a non-opioid pain management drug, and a therapy addressing Sickle Cell Disease and Beta-Thalassemia. Several of these solutions have the potential to produce blockbuster status. Investors were excited by the potential in 2023 as the stock was up 41% last year, handily smashing the 7.60% total returns of SPDR S&P Biotech ETF (XBI) and the returns of the S&P 500 of 24.2%.

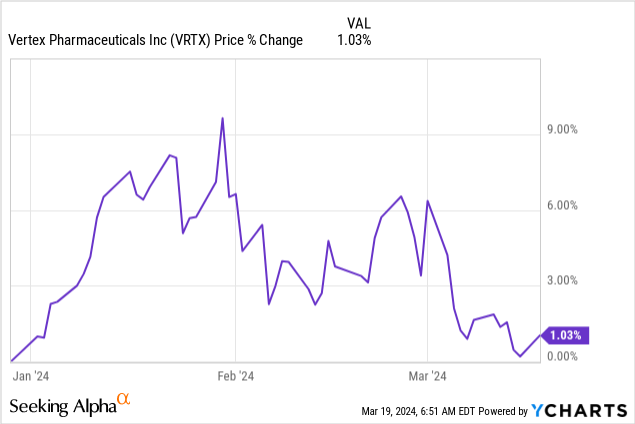

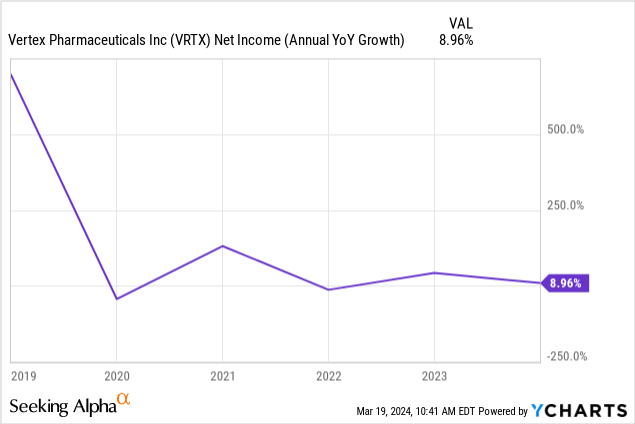

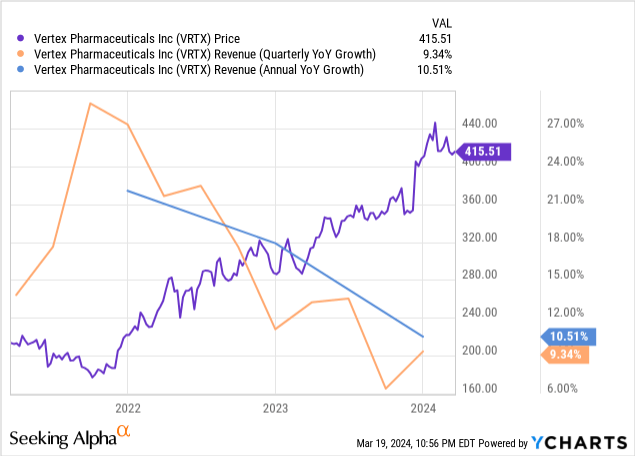

Although the company holds tremendous promise, as seen on the chart below, the stock has stalled so far in 2024. For several reasons, investors seem reluctant to push the stock price much higher in the near term. First, the company has forecast a revenue range in 2024 of $10.55 billion to $10.75 billion, which would be around 8% year-over-year growth at mid-point, down from the 11% year-over-year growth it produced in 2023 -- unappealing for some growth investors.

The appeal of Vertex for those investors who are bullish on the stock is in the long-term potential of its drug pipeline. This article will review the company's valuation, briefly review its fourth quarter 2023 earnings report released in early February, discuss its CF franchise and a few risks, and explain why some of the highest-potential drugs in the company's pipeline may justify buying for long-term growth investors.

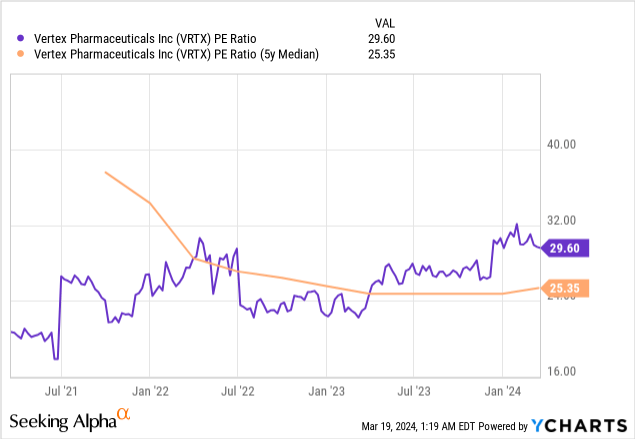

First, let's go over the company's current valuation. Based on many traditional valuation ratios, I consider the stock overvalued based on its current growth rates. Seeking Alpha's quant rates the stock's valuation a D. Vertex's price-to-earnings (P/E) ratio sits well above its five-year median. If Vertex traded at its five-year median P/E today, the stock price would be $352.67, which is 14% below its closing price on March 18 of $411.38.

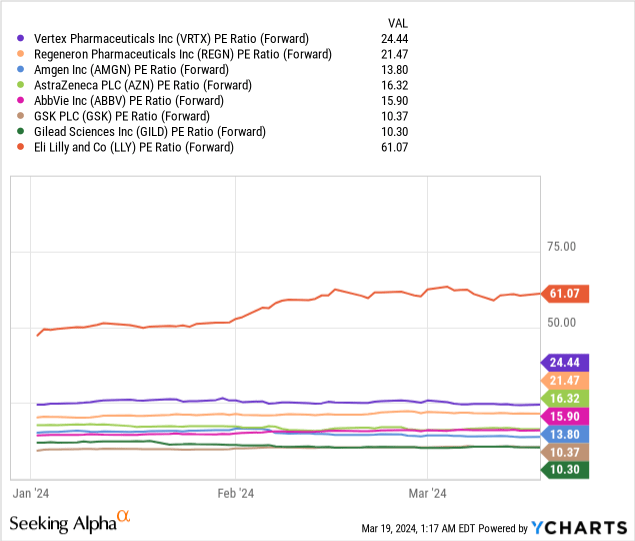

The stock has a forward P/E of 24.44, higher than many of its biotech and pharmaceutical industry peers.

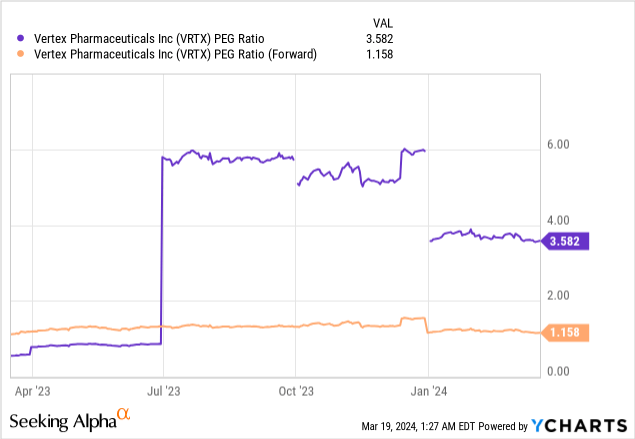

Let's look at its Price/Earnings-to-growth ("PEG") ratio. Based on its PEG ratio on a trailing 12-month basis, the stock looks overvalued at 3.582. However, its forward PEG ratio is 1.158, which means that according to the earnings-per-share ("EPS") growth analysts expect the company to produce this year, the market may fairly value stock at the current price.

The following reverse DCF shows the implied free cash flow ("FCF") growth rates over the next ten years for Vertex's closing price of $ 411.38 on March 18, 2024.

| The first quarter of FY 2025 reported Free Cash Flow TTM (Trailing 12 months in millions) | $3,337 |

| Terminal growth rate | 3% |

| Discount Rate | 11% |

| Years 1 - 10 growth rate | 15.6% |

| Stock Price (March 12, 2024, closing price) | $411.38 |

| Terminal FCF value | $14.643 billion |

| Discounted Terminal Value | $64.465 billion |

| FCF margin | 33.22% |

Analysts forecast Vertex to grow revenue at a Compound Annual Growth Rate ("CAGR") of 8.22% over the next ten years. The company only grew its 2023 net income at 9%, and its 2023 annual FCF dropped 14.99%from 2022. Those statistics don't augur well for the company to generate a yearly FCF growth rate of 15.6% over the next ten years.

Let's say it did grow FCF by 10% over the next ten years; the estimated intrinsic value would only be $269.93. If Vertex cannot find additional revenue growth drivers, the market has overvalued the stock at current prices, in my opinion. One potential reason investors seem unwilling to push the current price up this year is that they are waiting to see how much the current drugs in the pipeline will produce additional growth.

Suppose Vertex's pipeline produces one or two blockbuster drugs, and its FCF growth rate starts increasing at a 20% annual rate; the stock's intrinsic value would be $564.91, up 37% from the current stock price. How an investor decides to value Vertex depends on their expectations for its drug pipeline's success.

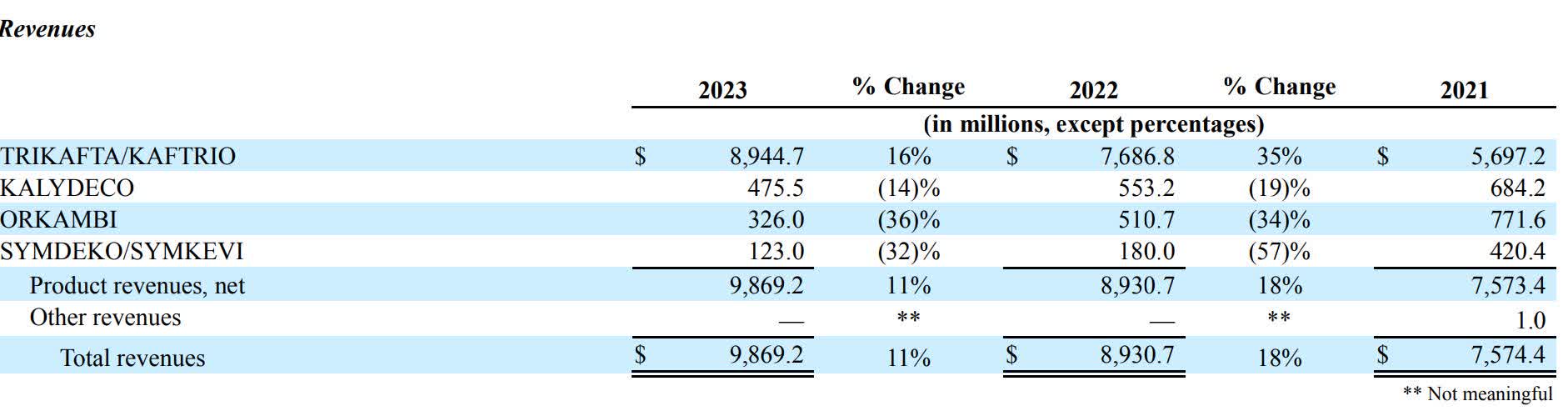

Vertex has several products approved by the Federal Drug Administration ("FDA") and a few other regulators worldwide. However, the only medications on the market generating revenue are products within its CF franchise. CF is a disease that affects the lungs. The company has developed several drugs that target different indications in CF. Vertex's drugs currently treat most people with CF in the locations where regulators have approved it. The company stated in the 2023 10-K, "Collectively, our four marketed CF medicines are being used to treat nearly three quarters of the approximately 92,000 people with CF in North America, Europe and Australia." The image from its 2023 10-K below shows the four products that generated revenue for Vertex in 2023.

Vertex 10-K

Vertex was one of the first companies to develop effective drugs for CF, making it a first mover in the space. In 2023, KALYDECO was Vertex's second-largest revenue-generating product, accounting for approximately 5% of revenue. It was also the first therapy to effectively address one of the root causes of CF when the FDA approved KALYDECO in 2012 for patients aged six and above. The FDA has since expanded the indication to infants older than one month. The drug is effective for people with CF who have a mutation in one specific gene.

The next CF drug the FDA approved from Vertex was ORKAMBI in 2015 to treat CF patients aged 12 or older with two copies of a specific mutation. Later, the FDA reduced the age to two years old. SYMDEKO/SYMKEVI is an oral combination of two medications, tezacaftor, and ivacaftor, that FDA regulators approved in 2018 for CF patients aged 12 years and older who have a specific mutation. The FDA later expanded the indication to patients older than six with one of 154 different mutations.

The company's largest revenue generator at 91% of total 2023 revenue is TRIKAFTA, which the FDA first approved in 2019 for patients 12 and older with a common CF mutation. After the FDA approved it, TRIKAFTA became one of the most effective drugs in the world to treat CF and its prime moneymaker. According to several studies, when a CF patient starts TRIKAFTA at an early age, their lifespan can increase by four or five decades. Since CF is a chronic disease and the patient must take the drug regularly to receive its benefits, TRIKAFTA and its other franchise drugs can perform similarly to a subscription business, which is much more valuable to the company than a one-and-done cure. Another factor in Vertex's favor is that patent protection for most drugs usually lasts for 20 years in the U.S., so the company probably won't have to deal with generic competition for TRIKAFTA until the late 2030s. This revenue source should be solid for Vertex for a long time.

Consequently, its CF franchise has become a valuable funding source for the Research and Development of other drugs in Vertex's pipeline, including its newest CF drug, Vanzacaftor (Vanza) Triple, which management believes is even more effective than TRIKAFTA. Currently, Vanza Triple is in phase III trials with the company hoping to put it on the fast track for approval. During the company's latest earnings call, Chief Executive Officer Reshma Kewalramani said the following:

In summary, we set a goal to establish a new and higher bar in the treatment of CF with CFTR modulators, and with these Phase 3 Vanza Triple results, we have the first evidence that we have done so, and with these results, we now know that the Vanza Triple has indeed surpassed the very high bar set by TRIKAFTA in people with CF, ages six and older. And by treating patients early with the Vanza Triple, we have the potential to possibly prevent systemic manifestations of CF in more people.

Source: Vertex Fourth Quarter 2023 Earnings Call.

Vertex is trying to get the EMA (European Medicines Agency) and FDA to approve Vanza Triple by mid-2024. Suppose the FDA ultimately approves Vanza Triple, and the drug proves more effective than TRIKAFTA; Vertex will have set a higher bar for potential competitors' CF treatment plans and reset the clock for the patent expiration of its current lead drug.

Vertex Fourth Quarter 2023 Investor Presentation.

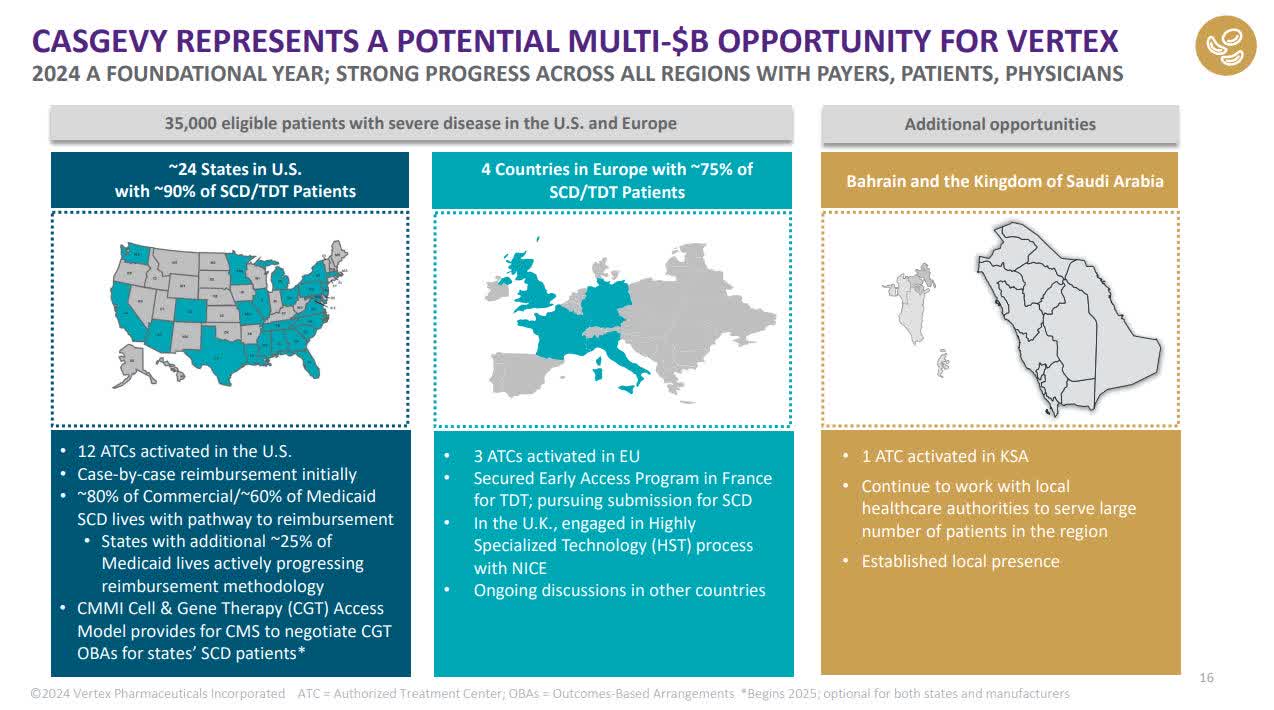

Vertex has one more FDA-approved drug that I have yet to discuss, CASGEVY, which is Vertex's first drug outside of its CF franchise. CASGEVY has already gained approval in the U.S., England, Saudi Arabia and Bahrain. Vertex partnered with CRISPR Therapeutics (CRSP) to develop the therapy to treat sickle cell anemia ("SCD") and transfusion-dependent beta-thalassemia ("TDT"), which are both blood disorders that impair the ability of red blood cells or hemoglobin to carry oxygen. The treatment consists of removing blood stem cells from a person's body, which then goes to a manufacturing site where gene editing technology changes the stem cells to make them produce hemoglobin that can carry oxygen.

Vertex Fourth Quarter 2023 Investor Presentation.

CRISPR Therapeutics contributes the CRISPR/Cas9 gene-editing technology to the partnership. Vertex describes its contribution to the partnership in a press release on its website (Emphasis added):

Vertex leads global development, manufacturing and commercialization of CASGEVY with support from CRISPR Therapeutics. In conjunction with the FDA approval of CASGEVY, Vertex will make a $200 million milestone payment to CRISPR, which will be capitalized and amortized to cost of sales. Additionally, Vertex will record 100 percent of CASGEVY revenues; costs of sales; and selling, general and administrative expenses and will record CRISPR's 40 percent share in the net profits or losses from CASGEVY within its cost of sales. Lastly, Vertex will record 60 percent of research and development expenses, net of CRISPR's 40 percent share.

Source: Vertex Press Release

According to Seeking Alpha analyst Edmund Ingham, "Vertex insists CASGEVY has 'multibillion-dollar market potential.'" The FDA approved CASGEVY in December 2023 to treat blood disorders SCD and TDT in patients 12 and older. So, the company is only beginning to commercialize this therapy. If this therapy produces multibillion in revenue, it will go a long way toward rejuvenating Vertex's top line and FCF.

Vertex Fourth Quarter 2023 Investor Presentation.

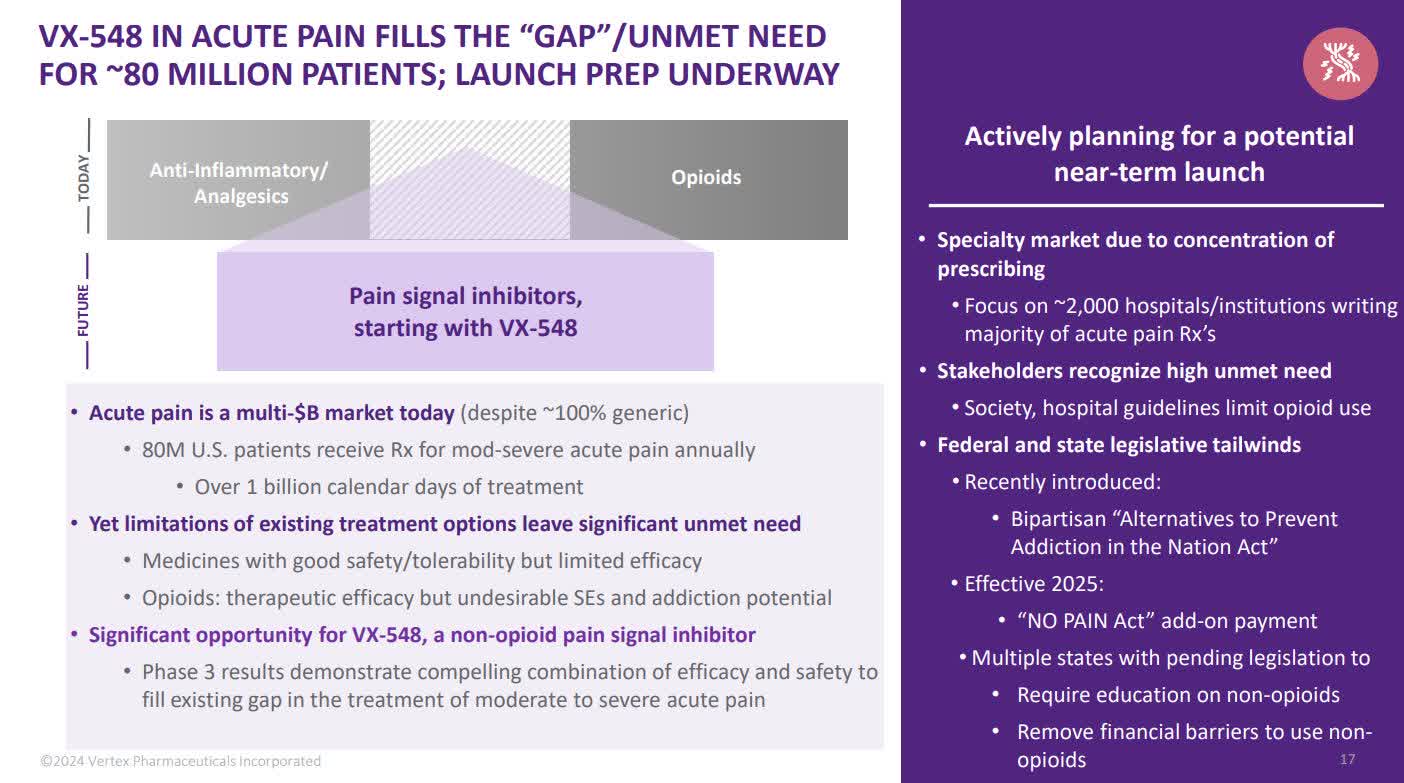

The next Vertex near-term monetization opportunity investors should consider is VX-548, an oral non-opioid pain medication. Management sees VX-548 as fitting the need for a pain medication between non-steroidal anti-inflammatory drugs (NSAIDs) and opioids. Aspirin and ibuprofen are a few examples of NSAIDs. A few examples of opioids are morphine, OxyContin, Vicodin, and Fentanyl, all highly addictive drugs. Management believes that VX-548 can potentially reduce pain as effectively as some opioids without being addictive. If that turns out to be accurate, this pain management medication has blockbuster potential. Currently, VX-548 is in Phase III testing.

Vertex Fourth Quarter 2023 Investor Presentation.

There appears to be significant demand for VX-548. At a recent investing conference, Vertex Chief Financial Officer Charlie Wagner said:

We've done market research. We've talked to 600 or so physicians, including orthopedic surgeons, plastic surgeons, anesthesiologists, pain experts, et cetera. Among those 600 physicians, the overwhelming majority are interested or very interested in prescribing a medicine like VX-548 because they really don't have any great alternatives today. Beyond the physicians, we've begun compliant pre-approval information exchanges with decision-makers on formularies at the institutional level in hospitals and IDNs [Integrated Delivery Network] with PBMs [Pharmacy benefit managers], with payers [Insurance companies]. And of course, we have ongoing conversations with state and federal legislators as well. And across the board, the reaction has been very positive.

Source: Leerink Partners Global Biopharma Conference

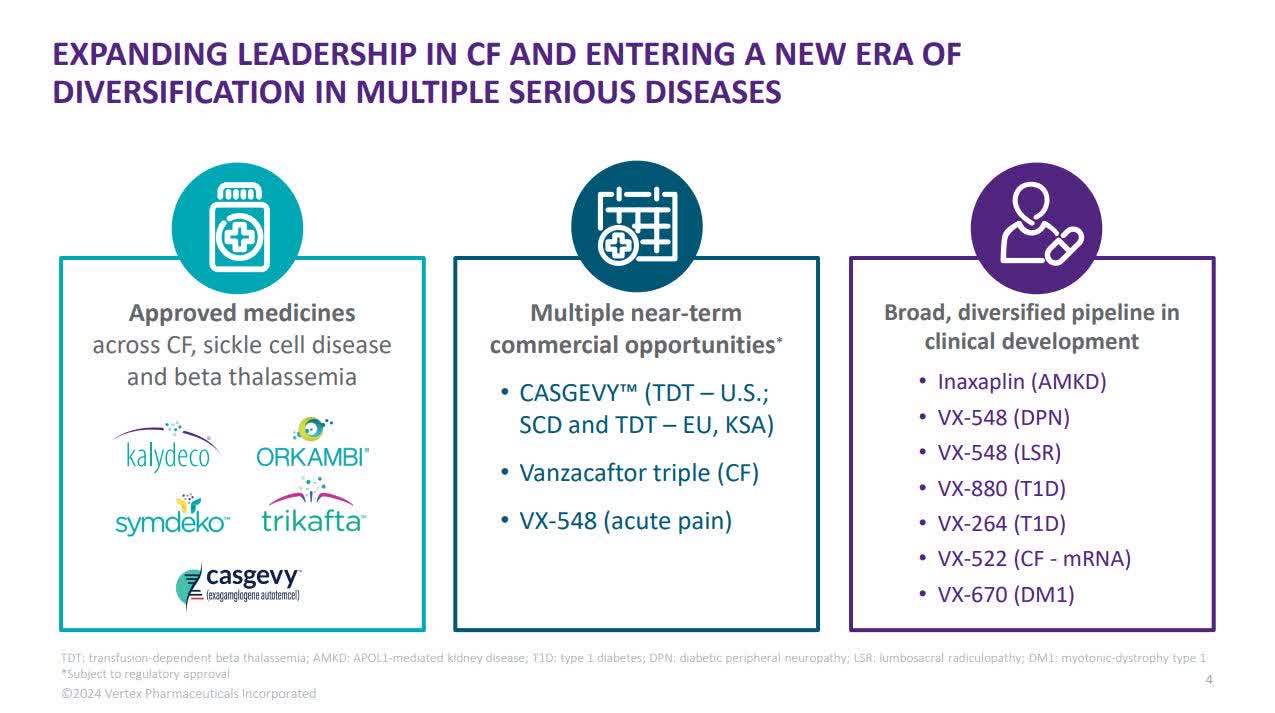

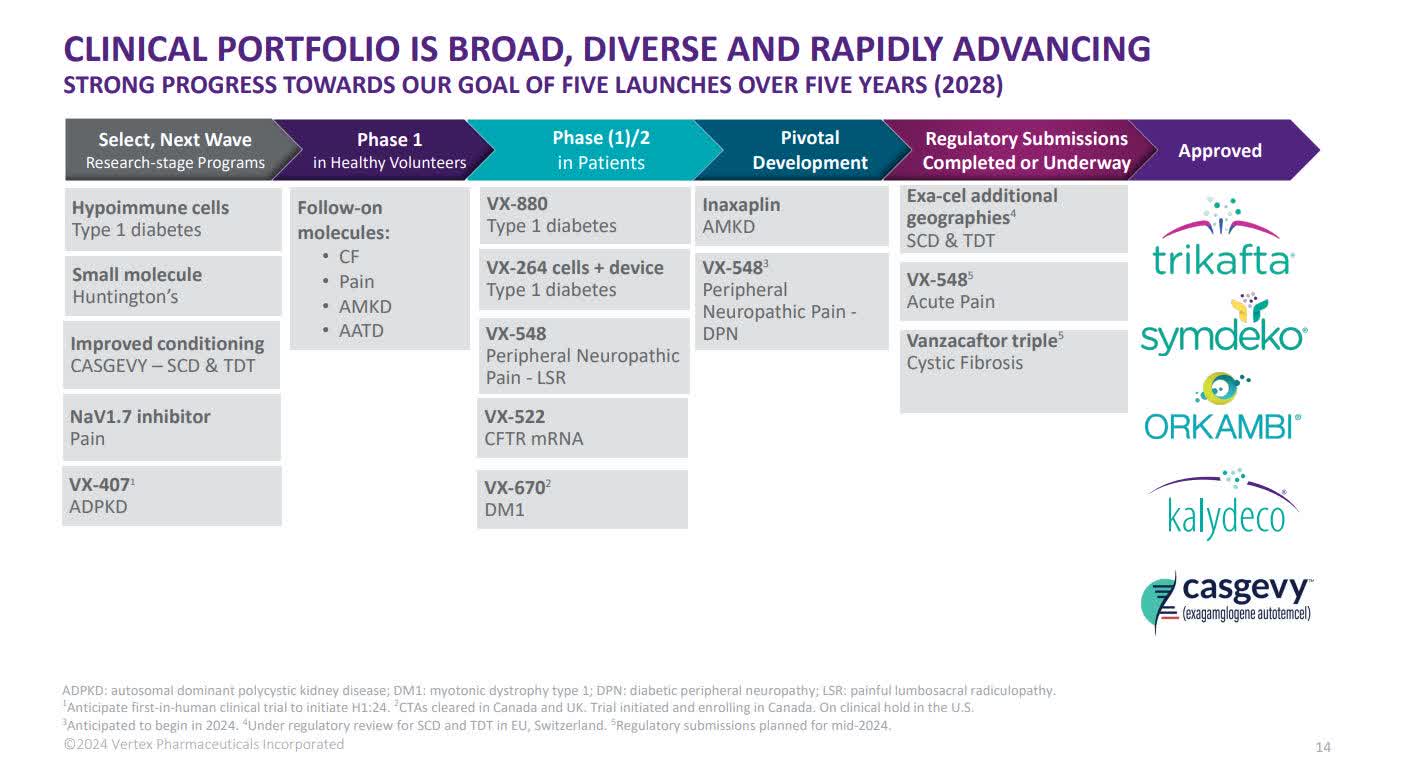

The chart below shows that the company has a goal of five drug launches by 2028. Three of those drugs, CASGEVY, VX-548, and Vanza Triple, are in the process of receiving approvals in the U.S., or in the case of CASGEVY, which has already received approval in the U.S., is seeking additional approvals in the E.U. and Switzerland.

Vertex Fourth Quarter 2023 Investor Presentation.

Two other drugs, part of the five that the company hopes to get approved by 2028, are listed under Pivotal Development. One is a phase II trial testing VX-548 as a pain medication for diabetic peripheral neuropathy (DPN) . The other drug is Inaxaplin (VX-147) in Phase 2/3 trials. The phase III portion should have started sometime in the first quarter of 2024. Vertex designed VX-147 to treat APOL1-Mediated Kidney Disease (AMKD).

I won't go through the rest of the pipeline since the rest are either in the developmental stage or in Phase I or II trials and will likely take five to ten years to get approved if they get approved. However, it's interesting to note that in future drugs under development, Vertex focuses on following up its first drugs with additional indications in areas like pain management, AMKD, CF, SCD, and TDT, as well as diving into health problems like diabetes. Vertex likes to focus on providing solutions to medical issues where there are few viable solutions.

The company's decision to invest heavily in other areas outside its CF franchise well before the patents expire for its leading drug TRIKAFTA is sound. The multibillion-dollar potential opportunity of this pipeline keeps some investors bullish on the stock. If everything goes well, investors should see a positive impact from Vanza Triple, CASGEVY, and VX-548 on revenue growth and FCF growth over the next one to three years.

Although the company beat analysts' revenue estimates by $3.12 million, topline growth was nothing to get excited about. Vertex produced quarterly revenue of $2.52 billion, up 9.34% over the previous year's comparable quarter. The company's 2023 annual revenue was $9.87 billion, up 10.51% over 2022. The chart below shows that revenue growth rates have steadily declined since January 2022. In my opinion, investors will likely not become excited enough to push the stock much higher unless they see revenue trending upwards or good news comes in concerning CASVEGY adoption or VX-548 or Vanza Triple FDA approval.

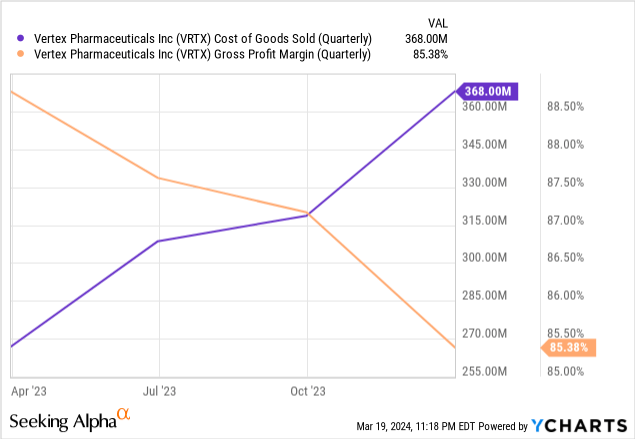

One thing to be aware of is that once the FDA approved CASVEGY and it became a commercial product, it triggered a $200 million milestone payment to CRISPR Therapeutics, which shows up as Cost of Goods Sold ("COGS"). The commercialization of CASGEVY also changed how Vertex treats certain costs. During the fourth quarter, Charlie Wagner said, "We took some of the manufacturing costs that previously had been recorded in R&D and moved them up to cost of goods sold." Manufacturing costs will remain in the COGS moving forward. You can see the impact of these moves on the following chart, which shows COGS going up and gross margins going down.

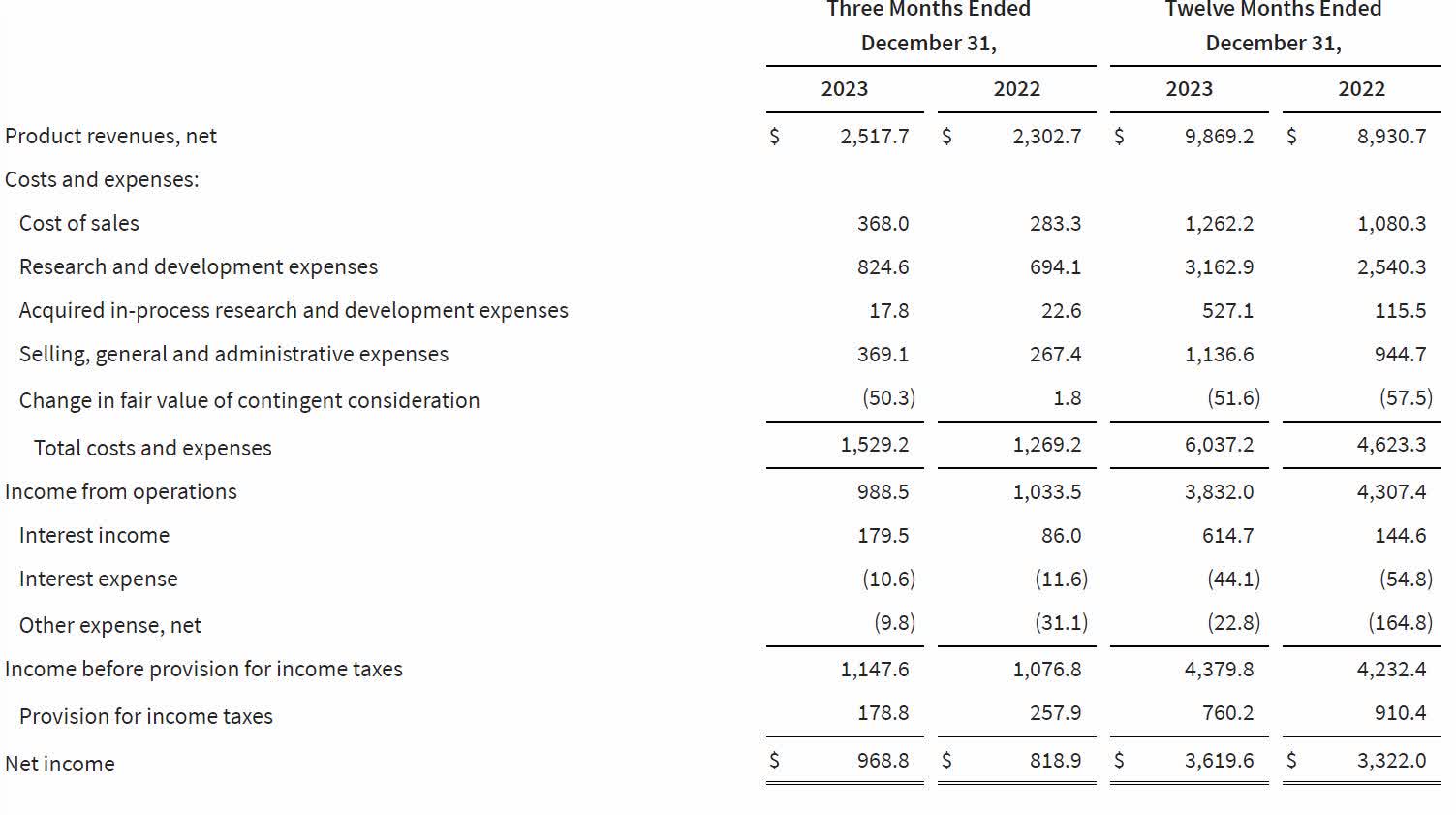

Operating expenses were up due to increased investments in the pipeline. CFO Wagner said about the increased operating expenses during the earnings call, "In the fourth quarter and throughout 2023, the most significant areas of increased investment versus prior year included the pivotal studies for VX-548 in acute pain and the vanzacaftor triple in CF, the Phase 1/2 study for Type 1 diabetes as well as the build-out of capabilities for both our expanding pipeline and our anticipated near-term commercial launches." I view these as necessary expenses for long-term revenue growth, although they reduced operating margins in the near term. The following chart shows Vertex's income statement for the fourth quarter and full year 2023.

Vertex Fourth Quarter 2023 Earnings Release.

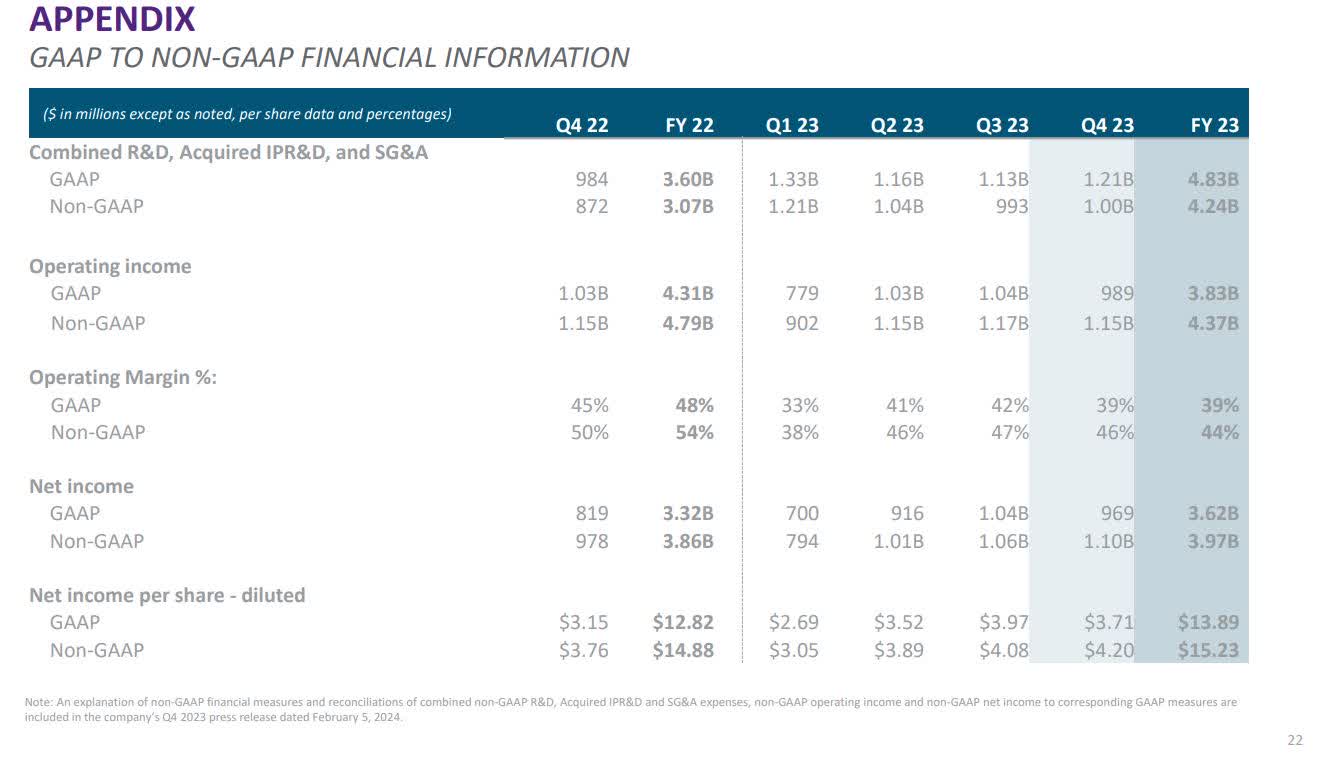

The company also reports non-GAAP numbers as it has many one-time expenses associated with its business that obscure its core profitability. One of those costs is a term you might not have heard of before. IPR&D stands for In-process research and development. Whenever Vertex acquires another company or its ongoing projects, it also takes on the associated costs. IPR&D can sometimes have intangible asset amortization expenses related to them and have a lot of different accounting rules, depending on whether the project gets completed or not. You might also see another related term when reviewing Vertex's results called AIPR&D, which stands for Acquired In-process research and development, which has a different set of accounting rules. Vertex's fourth quarter 2023 earnings report states (Emphasis added):

In particular, non-GAAP financial results and guidance exclude from Vertex's pre-tax income (i) stock-based compensation expense, (ii) intangible asset amortization expense, ("III") gains or losses related to the fair value of the company's strategic investments, (iv) increases or decreases in the fair value of contingent consideration, ("V") acquisition-related costs, (vi) an intangible asset impairment charge and ("VII") other adjustments. The company's non-GAAP financial results also exclude from its provision for income taxes the estimated tax impact related to its non-GAAP adjustments to pre-tax income described above and certain discrete items.

Source: Fourth Quarter 2023 Earnings Release

Although investors should analyze GAAP measurements alongside non-GAAP measurements because the above costs can be inconsistent from quarter to quarter, non-GAAP metrics may be the best for making quarter-to-quarter and year-to-year comparisons, especially when comparing metrics on the operating line, net income line, and EPS. The following image shows the GAAP and non-GAAP reconciliation.

Vertex Fourth Quarter 2023 Earnings Presentation.

The company reported a fourth-quarter 2023 GAAP diluted EPS of $3.71. Fourth quarter 2023 non-GAAP diluted EPS was $4.20, above analysts' consensus estimates by $0.11.

This company is in excellent financial condition, with $11.22 in cash and short-term investments against zero long-term debt. The company has a quick ratio of 3.78, indicating it can pay its short-term financial obligations.

Despite the pipeline having high upside potential, each of the three therapies that Vertex hopes to monetize in the near future could have issues. For instance, Baird analyst Brian Skorney was unimpressed with some results from phase III data for VX-548. Skorney commented that he didn't believe VX-548 was much better than "generically available pain meds." Evercore downgraded Vertex on February 6, 2024, citing "potential headwinds" in the near term for VX-548.

Although CASVEGY may provide a cure for SCD and TDT, the therapy may have a challenge to be a huge multi-billion-dollar needle mover, as the process of receiving this treatment can be long and complex. Patients don't pop into an office, receive a blood transfusion, and complete the treatment in an hour. Instead, CASVEGY treatment can take up to a year. If a patient is lucky, the process may only take months. The method also involves being hospitalized for a period and can potentially have severe side effects. This treatment has a small market, and only people who have the most severe forms of the disease will likely go for this treatment. CASVEGY is also expensive, around $2.2 million. One analyst believes that adoption of this therapy will be slow, and people may want to lower their expectations for CASGEVY. Last but not least, Vertex only recognizes revenue from this procedure once the patient has received their transfusion, which, as I said previously, could take up to a year.

The concerns surrounding the Vanza Triple therapy have to do with the cost. This new CF therapy may not provide the same huge leap in effectiveness over TRIKAFTA that TRIKAFTA had over Vertex's previous CF drugs. The issue is that insurance companies may not want to switch people currently using TRIKAFTA to a more expensive Vanza Triple when they feel they may not get enough bang for the buck.

In addition to the risks associated with bringing the three promising therapies above to market, private and government initiatives exist to lower drug prices. Vertex's highly-priced drugs are a likely target in various groups' crosshairs. Over time, the pressure to lower prices could reduce Vertex's returns.

Although Vanza Triple, CASVEGY, and VX-548's potential upside may not fully show up this year, these drugs have a promising long-term future. If you decide to invest, understand that the stock could stall throughout 2024. If Vertex does move higher in 2024, it will likely be news-driven, meaning the market has received positive news concerning VX-548, which has the highest potential up, or Vanza Triple, which Vertex hopes to be a successor to TRIKAFTA. Growth investors looking to diversify their portfolio away from tech stocks should consider an investment in Vertex. I recommend the stock as a buy.