JHVEPhoto

JHVEPhoto

Veritiv Corporation (NYSE:VRTV) was formed in 2014 as a RMT, and is primarily a packaging company. Their revenue breaks down into packaging, facility solutions, and print solutions:

VRTV 10-K

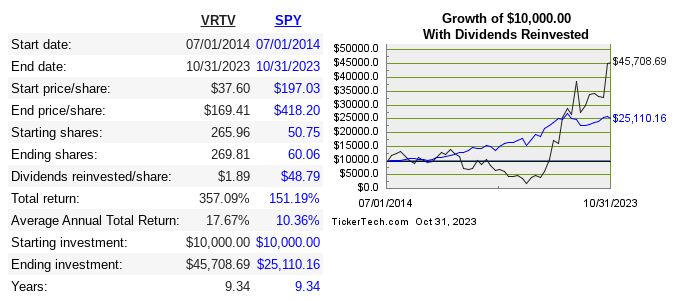

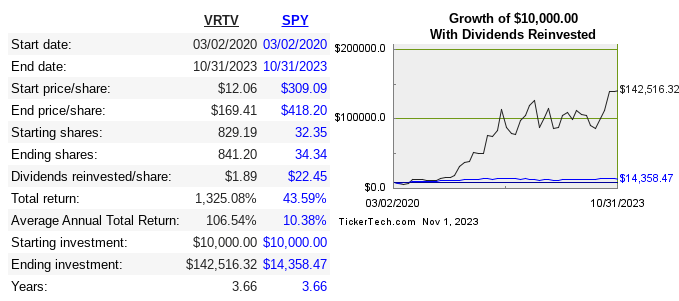

Below is their returns since IPO and period of best returns:

dividendchannel dividendchannel

The big news is of course that VRTV is set to be acquired by private equity firm CD&R is the fact that and that there isn’t any meaningful spread between the current share price and the acquisition price, but more on that later. Let's look at the fundamentals of VRTV to see the quality of the business.

Below are the return metrics:

Company | Revenue 10-Year CAGR | Median 10-Year ROE | Median 10-Year ROIC | EPS 10-Year CAGR | FCF 10-Year CAGR |

VRTV | 1.7% | 2% | 0.7% | 46% | 18.4% |

-0.3% | 19.6% | 6.1% | 8.6% | -2.3% | |

11.5% | 27.5% | 13.3% | 21% | 9.3% | |

6.2% | 13.4% | 7.7% | 14.9% | 7% | |

8.7% | 7.5% | 4.3% | 7.7% | 5.7% |

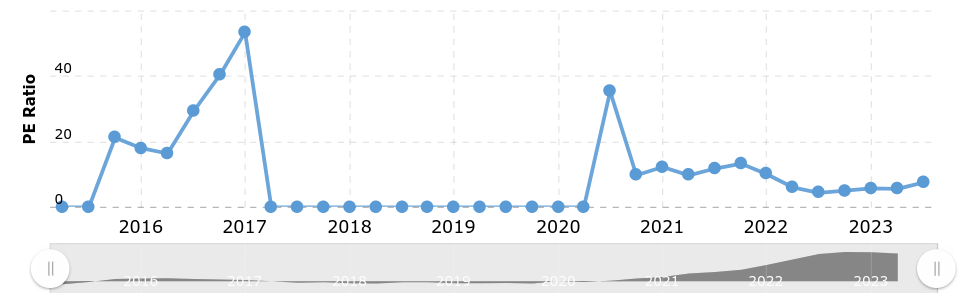

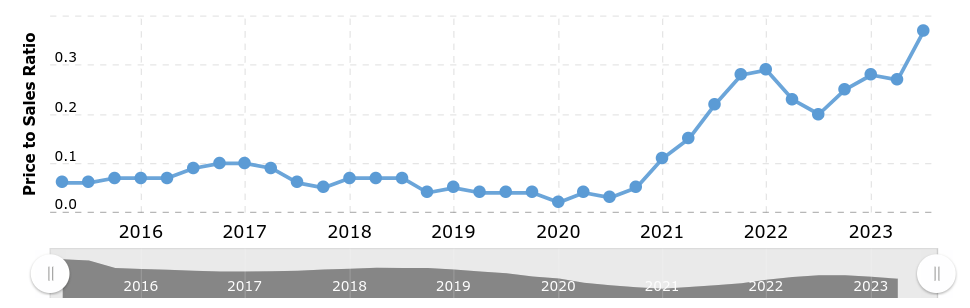

The global packaging industry is projected to grow at 4% compounded rate till 2031. In 2022, VRTV achieved record highs in gross profit, operating profit, net income, ROE, and ROIC. We also see how capital intensive the industry is when we compare the 10-year CAGR of revenue at 1.7% versus the CAGR of assets at 7.2%.

They paid a dividend for the first time ever last year, and it was a payout of $8 million compared to $338 million in net income.

Below we see how the cash was allocated in USD millions:

Year | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 |

EBIT | 36 | 73 | 125 | 113 | 71 | 69 | 67 | 100 | 222 | 414 |

FCF | -19 | -12 | 69 | 99 | 4 | -30 | 247 | 266 | 134 | 231 |

Acquisitions | 145 | |||||||||

Debt Repayment | 3,765 | 2,606 | 4,762 | 4,649 | 4,751 | 5,783 | 7,016 | 5,732 | 5,8,28 | 6,404 |

SBC | 0 | 4 | 4 | 8 | 16 | 18 | 15 | 18 | 7 | 10 |

The record profits and returns on capital are impressive, but they don’t necessarily mean that VRTV has leveled up quality-wise. If that were the case, then I would be very interested in the stock going forward but this is just part of the cyclicality.

The risk is inherent to the industry. For me there is almost no price cheap enough to warrant a long term investment in virtually any company in the sector. The returns on capital are enough to scare me off, but the cyclicality and debt load of FRTV add even more evidence to the bear case.

Obviously the acquiring company doesn’t agree with me at all. So for investors, the main risk would be using a shorting strategy in case the deal surprisingly doesn’t go through. This was not a hostile event, and the largest shareholders were in approval of the deal.

Let's try to determine if CD&R got a good deal from this price. Below is the historical multiple and comp versus peers:

Company | EV/Sales | EV/EBITDA | EV/FCF | P/B | Div Yield |

VRTV | 0.4 | 5.4 | 7.1 | 2.6 | 1.4% |

IP | 0.8 | 6.5 | 18 | 1.4 | 5.5% |

PKG | 1.7 | 8.8 | 23.5 | 3.5 | 3.3% |

DITHF | 0.6 | 4.2 | 14.6 | 0.9 | 6.7% |

WRK | 0.8 | 6.1 | 24.9 | 0.9 | 3.1% |

macrotrends macrotrends macrotrends

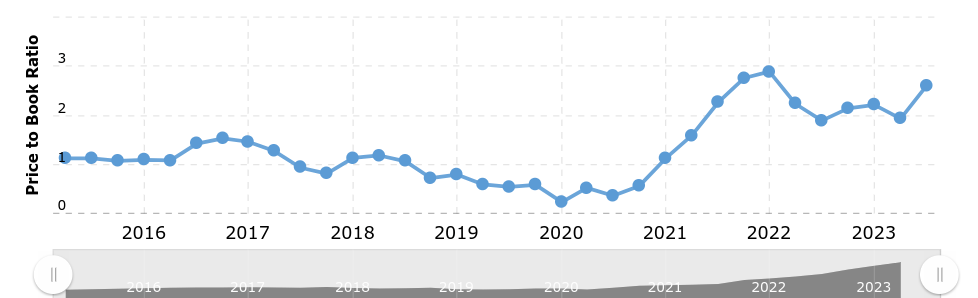

As we can see, the stock has been rerated from pre-pandemic levels, yet trades in line with its peers currently. This is why it’s important to not look at the multiple in isolation. It shows the potential dangers of screening for cheapness.

Since I see the current earnings reverting back to the mean eventually, I think CD&R has grossly overpaid on this one. It will be interesting to see how much value add will come about from the acquirer’s efforts as operators. Of course, these kinds of details are often within a black box at the PE firm potentially selling the shined up version of the business to someone else.

Shareholders can at least perhaps take some further satisfaction that the fact that VRTV was acquired by a firm known for partnering with the founders/leaders of the acquired businesses. It won’t be stripped down and liquidated ASAP in my view.

VRTV has just achieved record high profits and returns on capital, and is clearly in a healthy place at the moment. The stock has been a volatile one, with a beta of 2.1, so that era will soon be over once they are private. The biggest winners are shareholders who held before the buyout news, but that leaves nothing for anyone else as the spread is tight, and I believe the close of the deal is rather straightforward and predictable.