Brilt/iStock via Getty Images

Brilt/iStock via Getty Images

Verisign (NASDAQ:VRSN) released its Q4 and FY 2023 results just last month. I figured it was a good time to assess a good company for an opportunity.

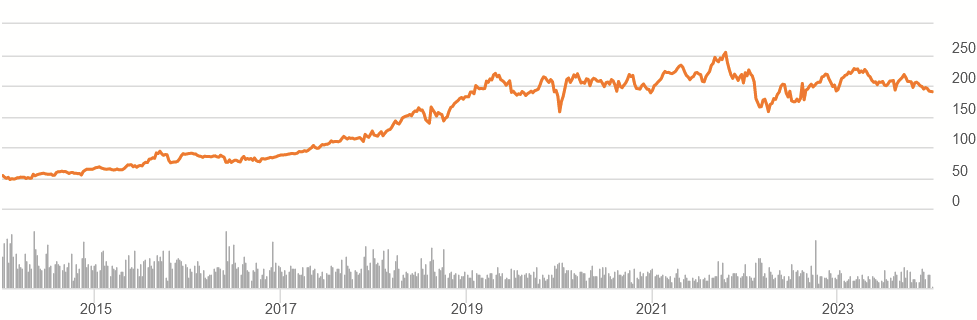

Seeking Alpha

After spending the first half of the decade steadily rising, VRSN has had a fairly indecisive run for the last five years, while continuing to grow in that time. I've decided to take in the 2023 results, look at its prospects going forward, and see if the current price is attractive.

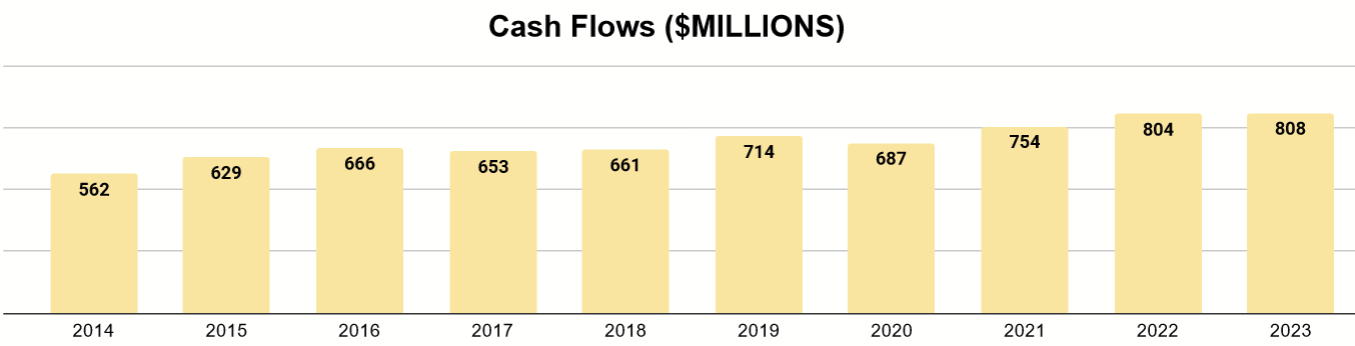

The company has had a very profitable history over the last decade. Let's take a look at the cash flow situation.

Author's display of 10K data

We can see that it's been consistently positive and steadily increased at a CAGR of about 4% during this time. This owes to the wide margins it enjoys on its domain name registration service, its primary source of revenue. Similarly, capex is small, never exceeding 10% of operating cash flows the past decade.

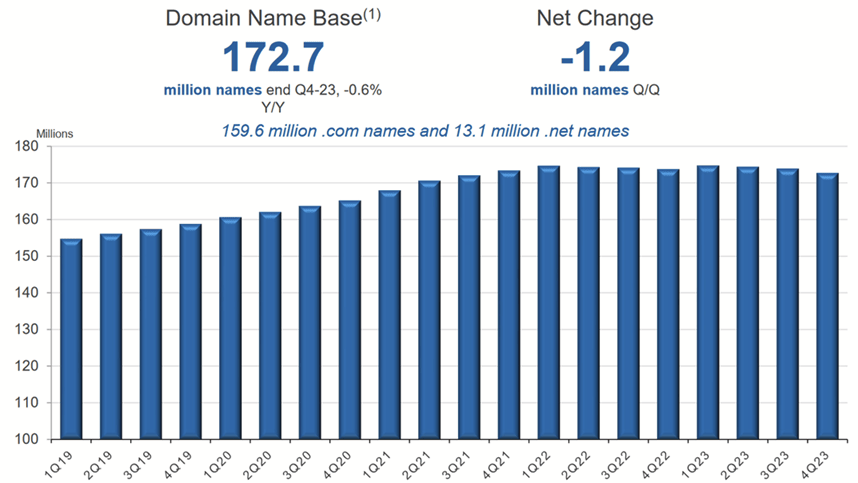

This has been associated with the growth of their base of domain names, which starting slowing down in 2022.

Q4 2023 Company Presentation

On top of this trend with the base of domain names (which affects long-term renewals), growth of FCF has been affected by regulations on pricing. Their 2023 Form 10K (pg. 6) notes:

Amendment 3 to the .com Registry Agreement permits an increase to the Maximum Price (as defined in the .com Registry Agreement) of .com domain name registrations by up to 7% over the previous year in each of the final four years of each six-year period. The first such six-year period began on October 26, 2018.

While there are conditions in which they are allowed to price more flexibly, this creates a limit on their ability to raise prices.

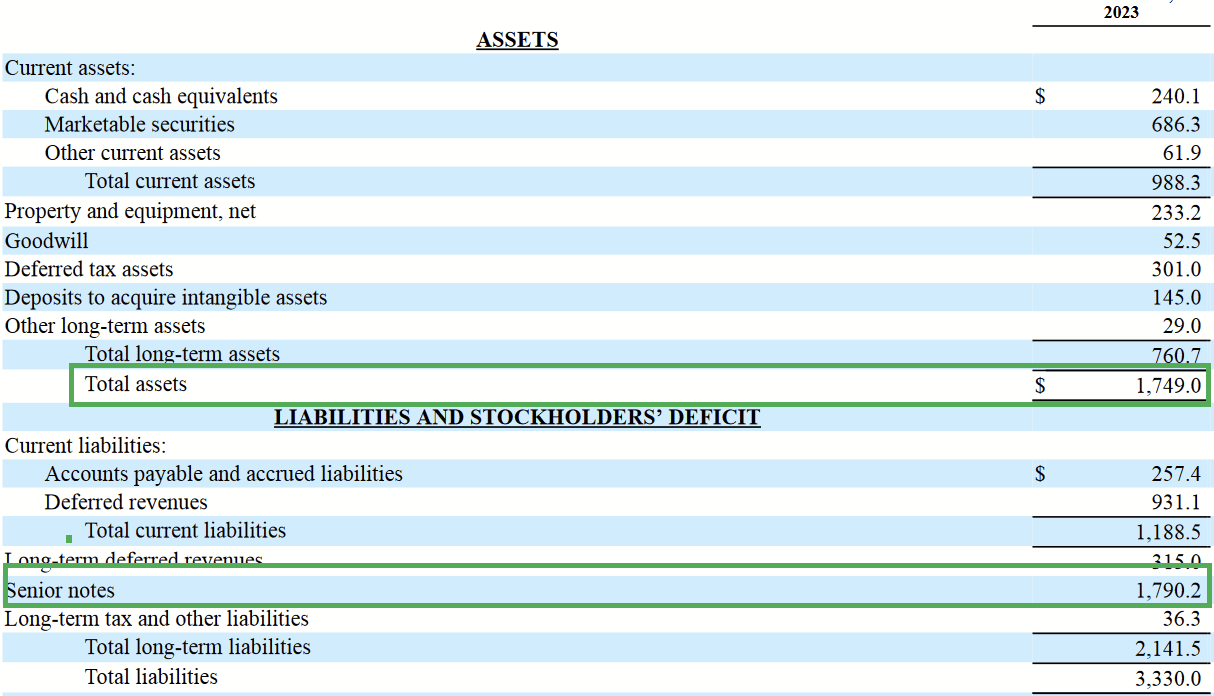

Balance Sheet (2023 Form 10K)

A quick look at the balance sheet might concern folks, as the long-term debt exceeds the value of their assets. Yet, I think a closer look at those senior notes alleviates those concerns.

2023 Form 10K

The maturities are staggered and well within what's covered by FCF, along with their $932M in liquid assets. We may even note the attractively low interest rate of 2.7% for the 2031 maturity which also accounts for the largest portion of the debt.

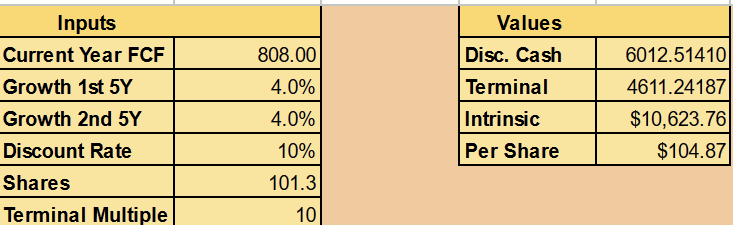

There is enough information for us to form a valuation using a Discounted Cash Flow model. I'll use the following assumptions in my calculation:

As the first two points imply, I'm assuming that 2023's FCF and the prevailing CAGR of FCF are reliable indicators of how well the company can do going forward. I see no major disruptions to those assumptions. A terminal multiple of 10 seems reasonable, simply because I don't think a high-margin company like this would usually be valued that low.

Author's calculation

This assumes an intrinsic value for the company of about $10.6 billion and $105 per share. That's much lower than the current price around $186, so let's discuss the possible concerns and why my growth assumptions aren't more optimistic.

In their Q4 2023 earnings call, management explained:

While there are many factors that drive demand for domain names, declining demand from China remains the primary source of drag on the overall domain name base growth.

Our domains under management from China-based registrars declined by 2.2 million names in 2023. China-based registrar demand has been weak as a result of several factors, including challenging economic conditions, a more stringent regulatory environment and the impact of a weaker local currency combined with retail pricing adjustments.

As American companies grow and saturate the U.S. market, one of their next areas for attractive growth is China. Yet, regulated as the domain name service is here in the U.S., greater barriers exist there. Moreover, the Chinese government may always increase these barriers as part of its domestic efforts to control Internet use more tightly.

I believe these issues are going to make it difficult for growth to continue in the Chinese market.

Revenue by Geography (2023 Form 10K)

Verisign will be more likely to enjoy growth in its U.S. and EMEA markets. On that note...

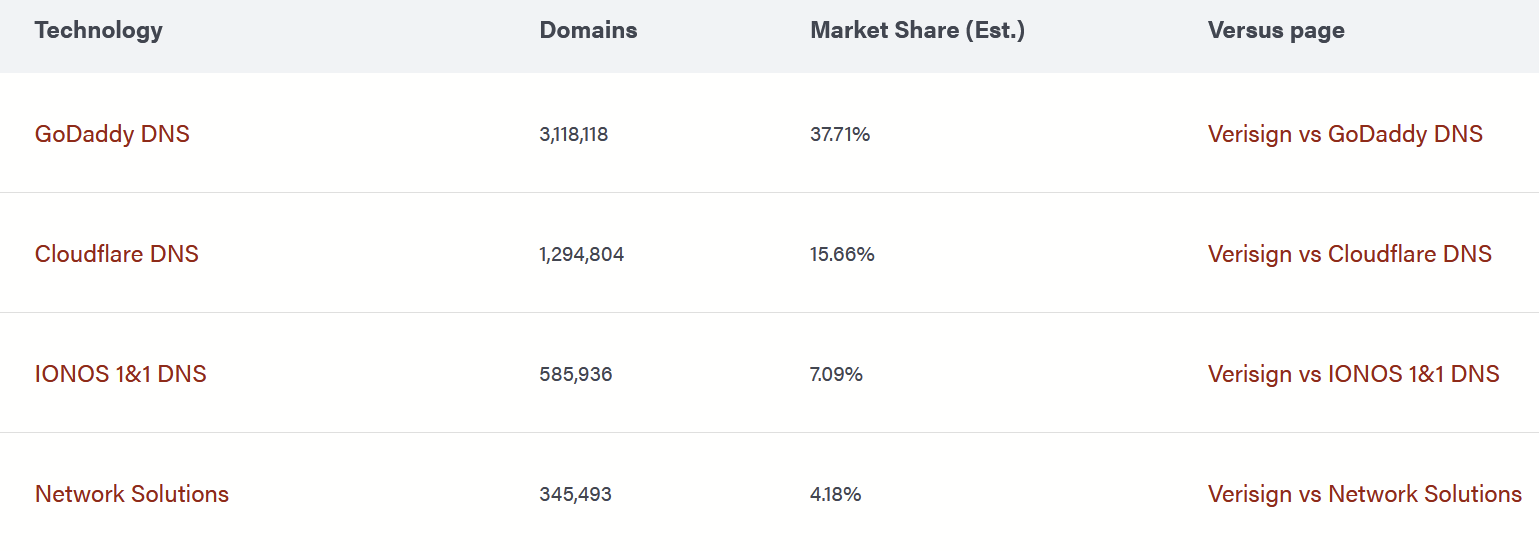

The company faces strong competition even in those markets. Verisign has a tiny market share compared to other players in the domain name space.

6sense.com

CEO Jim Bedzos even had praise for the work of GoDaddy (GDDY) in Q4 earnings:

First of all, I don’t want to speak for either ENS of course or GoDaddy. But what they did is, is make it easier to link a domain name to a block chain address. So it’s a very positive development for the DNS and it reinforces the utility of a domain name and the already strong value proposition of a domain name.

This was in the context of showing more optimism about the value of domain names in the industry overall, but they aren't mentioning Verisign in their earnings calls, while Verisign is tipping its hat to GoDaddy. Where pricing is limited, competitive edge to draw domain registrations is key to FCF growth, and it seems like signs are pointing to GoDaddy to me.

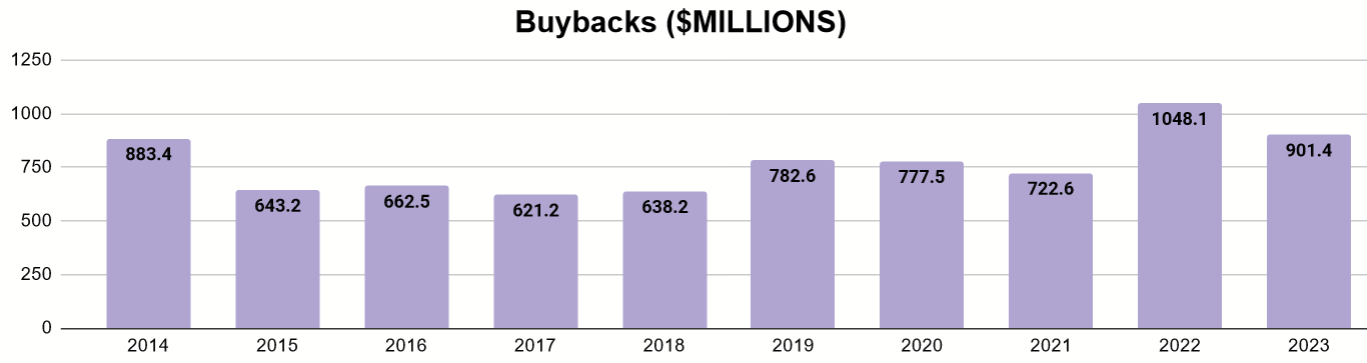

Over the past decade, company has not paid dividends. Buybacks have been the primary way by which value has been returned to shareholders.

Author's display of 10K data

The amount has stepped up over the last couple of years, in excess of FCF. While most of the interest on their debt is low, I personally feel, especially after rates started climbing, that it might have been prudent to pay off the 2025 maturity which has the highest yield of 5.25%.

Author's calculation

I don't often do this, but if you simply adjust the discount rate to 2% (pricing VRSN for an average annual return of 2%), you get roughly the current stock price, and some of these buybacks happened when shares traded closer to $200.

Eliminating that debt would make for a better long-term return to shareholders. Even sitting on the cash, with Treasury Bills paying near 5%, would be better than a buyback. It suggests to me that management is not thinking carefully about the return on capital for its shares, and buying back at a premium has the effect of being value-depletive over time.

Operationally, Verisign is a solid business with strong financials and a service that will be needed for a very long time. Yet, with obstacles to growth in China, a very competitive environment, and limits on pricing ability, the current valuation on the market assumes levels of growth that seem difficult to justify.

A sufficient price decline gives shareholders a fair price to buy into a wonderful company. It would also enhance the benefit of the buybacks. For these reasons, I would prefer to wait for a better price before I consider it a Buy.