JHVEPhoto

JHVEPhoto

Verisk Analytics (NASDAQ:VRSK) unveiled their Q4 results on February 21st, demonstrating consistent organic growth. I presented my 'Hold' thesis in my previous coverage, emphasizing their rich stock valuation and steady business growth. I reiterate my 'Hold' rating with a fair value of $210 per share.

Premium Rate Increase, AI, Data Analytics Drive Growth

In Q4 FY23, Verisk Analytics achieved 6% organic revenue growth and 6.5% organic EBITDA growth with 74bps margin expansion year-over-year, as shown in the table below. It is worth noting that Verisk Analytics had generated some hurricane related revenues in FY22, which poses 90bps growth headwinds in this quarter. Excluding the Hurricane Ian’s impact, their organic revenue would grow by 6.9%, reflecting a robust growth.

Verisk Analytics Quarterly Results

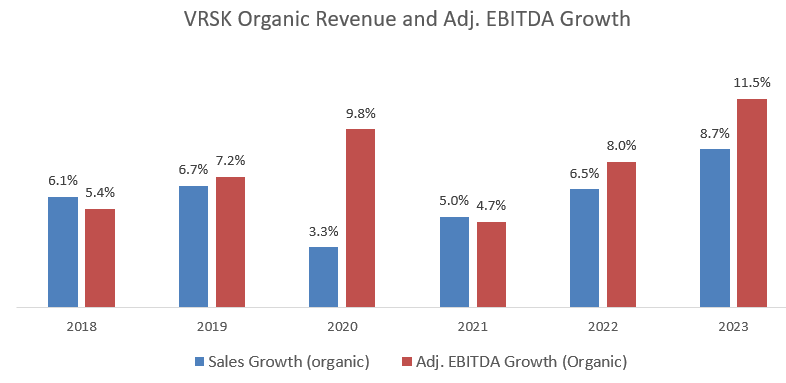

Notably, their adjusted FCF was up 15.8% year-over-year, and repurchased $250 million of own shares in the quarter. In addition, their Board approved another $1 billion share repurchase authorization. They ended with $303 million in cash and $2.86 billion in debts, with a net debt leverage of 1.8x. Their balance sheet continues to be robust. For the full year, they generated 8.7% organic revenue growth and 11.5% adjusted EBITDA growth, as illustrated in the chart below. I admire their consistent revenue and profit growth, as I pointed out in my previous coverage.

Verisk Analytics 10Ks

Their growth drivers could be summarized as follows:

Firstly, due to the inflation, insurance carriers persist in elevating their underwriting premium rates. Their management indicated that the net written premium growth increased by 10.8% for the first nine months of 2023. Verisk Analytics's underwriting business would benefit from the premium rate increase, as the segment’s revenue is linked to the underwriting premium to some extents. Consequently, their underwriting business grew by 7.3% in Q4 FY23.

Secondly, Verisk Analytics is providing data analytics tools and data to insurance carriers. Over the past few years, insurance carriers have been investing heavily in data analytics and upgrading their legacy IT systems in order to compete against Fintech companies. The success of Verisk Analytics today could be attributed to the data analytics and IT system upgrades in the insurance industry.

Lastly, AI is poised to reshape the entire insurance industry. According to McKinsey, AI technologies will have a seismic impact on all aspects of the insurance industry, from distribution to underwriting, pricing, and claims, and external datasets are the key elements to unlock the value of insurance AI technology. Verisk Analytics’s distinctive datasets would be quite unique in the rising AI era.

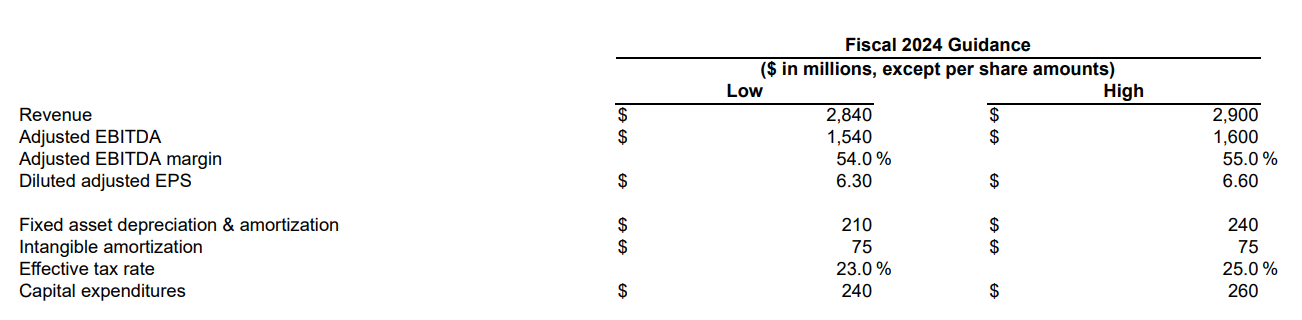

As shown in the table below, Verisk Analytics is guiding for approximately 8% revenue growth and 10% adjusted EBITDA growth for FY24.

Verisk Analytics Investor Presentation

There are several factors to consider for their FY24 growth:

On February 13th, 2024, Marsh, the world’s leading insurance broker owned by Marsh & McLennan (MMC), announced the rollout of its digital trading initiative for risks placed in the London insurance market. Marsh is planning to roll out the digital trading platform globally over the coming years, with the system leveraging Verisk Analytics’s Whitespace platform. In 2021, Verisk Analytics acquired Whitespace, a leading platform provides highly effective digital placing platform, and I view the tuck-in acquisition is quite successful. During the earnings call, Verisk Analytics’s management revealed that Marsh’s digital trading initiative traded over $400 million in insurance premiums, and Marsh anticipates 90% of their client premiums will flow through Whitespace platform by the end of 2024. Given that Marsh is one of the biggest insurance brokers globally; therefore, the adoption of Whitespace is poised to generate significant value for Verisk Analytics in the near future.

During the earnings call, Verisk Analytics disclosed that the company has been working with external consultants to refine their go-to-market strategy since 2023, and the new strategy will be rolled out throughout the upcoming fiscal year. The company plans to adopt new contract pricing and packing strategy, which could potentially improve the sales productivities in the near future.

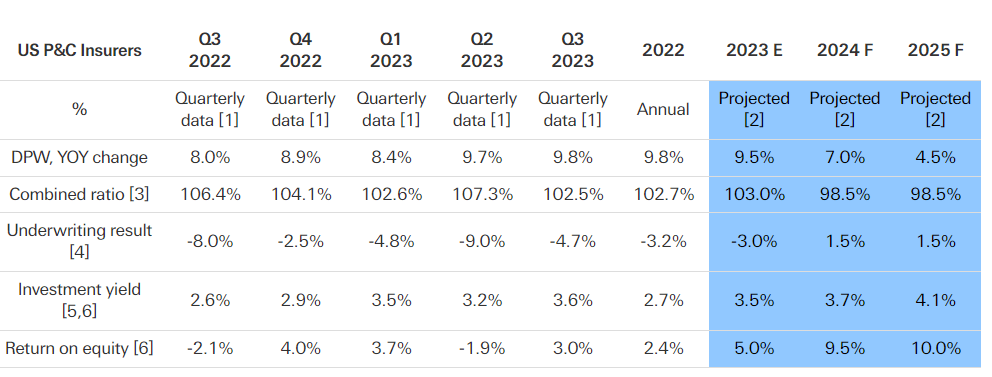

As previously discussed, the insurance premium rate would affect Verisk Analytics’s underwriting business. Swiss Re forecasts U.S. P&C insurance premium to grow by 7% in 2024, as illustrated in the table below. As disclosed during the earnings call, approximately 20%-25% of Verisk Analytics’s revenues are directly linked to the prior two-year premium growth.

Swiss Re Forecast

Putting all the pieces together, 8% revenue growth would be quite realistic and achievable in FY24, and the growth rate is consistent with their historical average level.

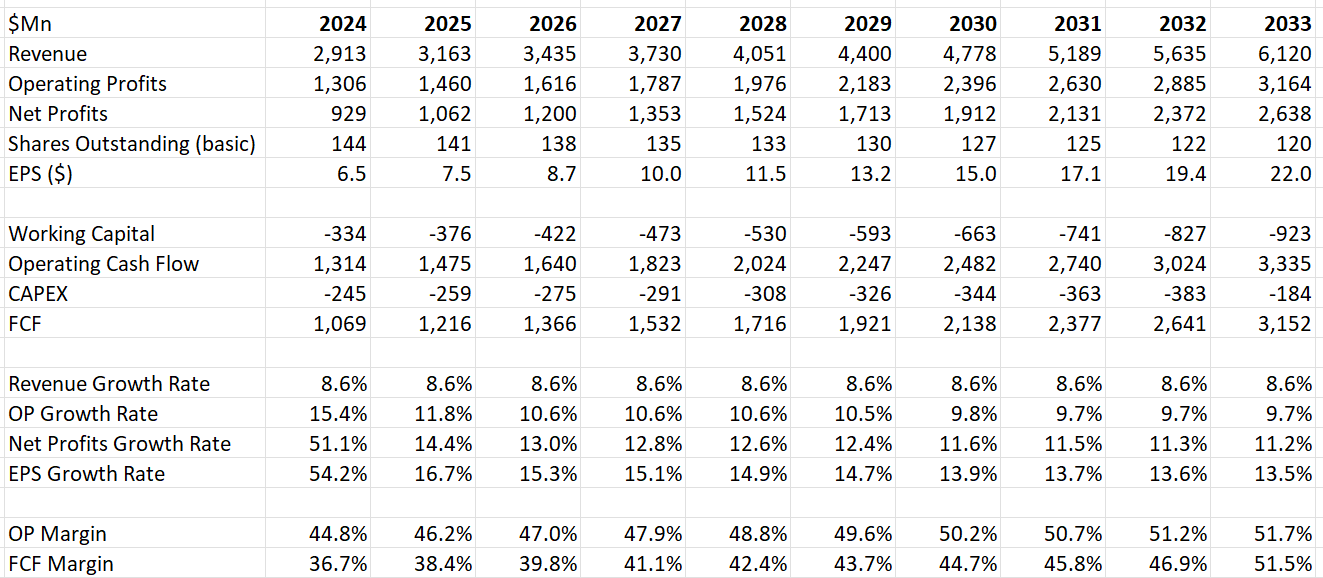

The model’s assumptions for FY24 align with the company’s guidance, anticipating 8% organic revenue growth and 60bps acquisition growth. The capital expenditure is assumed to be $245 million, aligning with the guidance. For the normalized growth, the model projects 8% organic revenue growth and 60bps acquisition growth. Both assumptions are consistent with their historical average. In addition, I forecast the industry adoption of AI technology could potentially accelerate Verisk Analytics’s data analytics business growth. To be conservative, I have not incorporated any AI related growth in the model.

I forecast their operating expenses will grow by 6.8% annually, leading to operating leverage. The operating margin is forecasted to reach 51.7% by FY33 as per my calculations.

I keep the remaining assumptions intact in the model, and the new fair value is estimated to be $210 per share. The current stock price is trading at around 32x forward FCF.

Verisk Analytics DCF - Author's Calculation

Auto Business: In Q4 FY23, Verisk Analytics delivered strong growth in the auto solution business in FY23, attributed to a large deal they signed in 2023. From the next quarter, Verisk Analytics would encounter challenging comparables for its auto solution segment. Consequently, the auto business revenue is expected to decelerate in FY24.

Transactional Revenue: Transactional business accounts for 20% of group revenue and is inherently volatile in nature. In Q4 FY23, the business grew by only 0.8% year-over-year. As the business benefited from Hurricane Ian in FY22, the strong comparable caused the subdued growth in FY23. It would be challenging to predict the transactional revenue growth in FY24.

I am impressed by Verisk Analytics’s ability to achieve high-single-digit organic revenue growth, and their strength in insurance data analytics. However, the stock price is overvalued; therefore I maintain a 'Hold' rating with the fair value of $210 per share.