da-kuk

da-kuk

We believe that an investment in eGain Corporation (NASDAQ:EGAN) represents an inexpensive way to gain exposure to long-term generative AI tailwinds. Shares sold off sharply after the company reported its F2Q24 earnings on February 8 due to the non-renewal of two customers that represented $8M in ARR (8% of annualized revenue). Despite the loss of these two customers, management seemed enthusiastic about the prospects of the business and expects to see continued positive momentum in new business activity given the level of interest in its AssistGPT generative AI product. Given the quantity of potential customers currently undergoing Knowledge Hub trials, we believe significant new logo wins are forthcoming. We urge investors to keep an eye out for new logo wins, which we believe will validate our thesis.

eGain is a provider of knowledge SaaS products for contact centers that assists with automating customer engagement for its customers' contact center agents. The company's software improves the customer-to-contact center agent experience through automation and analytics by:

The result is a reduction in the knowledge and guidance gap between what contact center agents should do versus what they actually do without eGain's products. This improves efficiency and reduces operating costs for eGain's customers.

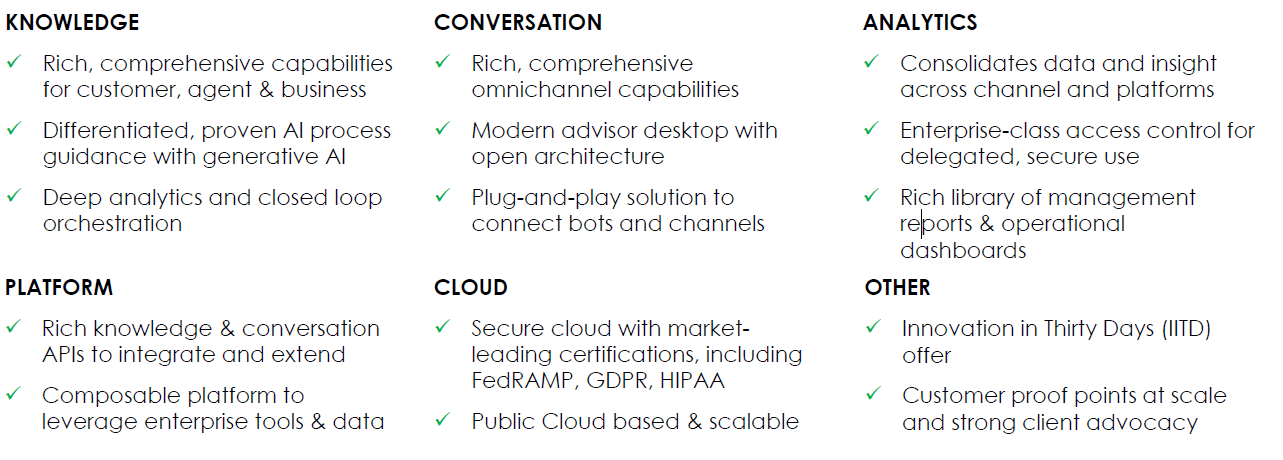

eGain's three product offerings include:

Figure 1: eGain Hubs

eGain Hubs (Company Reports)

Source: Company Reports

The company predominantly sells to large enterprises within the financial services, telecommunications, retail, government, healthcare, and utility industries.

Figure 2: Customers

eGain Customers (Company Reports)

Source: Company Reports

In our opinion, eGain has a highly scalable business model that should benefit significantly from increased existing and new customer adoption of its AssistGPT product included in its Knowledge Hub. The company boasts gross margins of over 70% and noted it does not need to hire additional sales employees to significantly grow this business. We believe the company has strong secular tailwinds for top line growth which should translate into meaningful margin expansion going forward.

Let us start by saying that eGain did not simply see the hype around AI and decide to launch an AI product hoping for multiple expansions and a subsequent capital raise like many other companies (particularly small cap) have done. On the contrary:

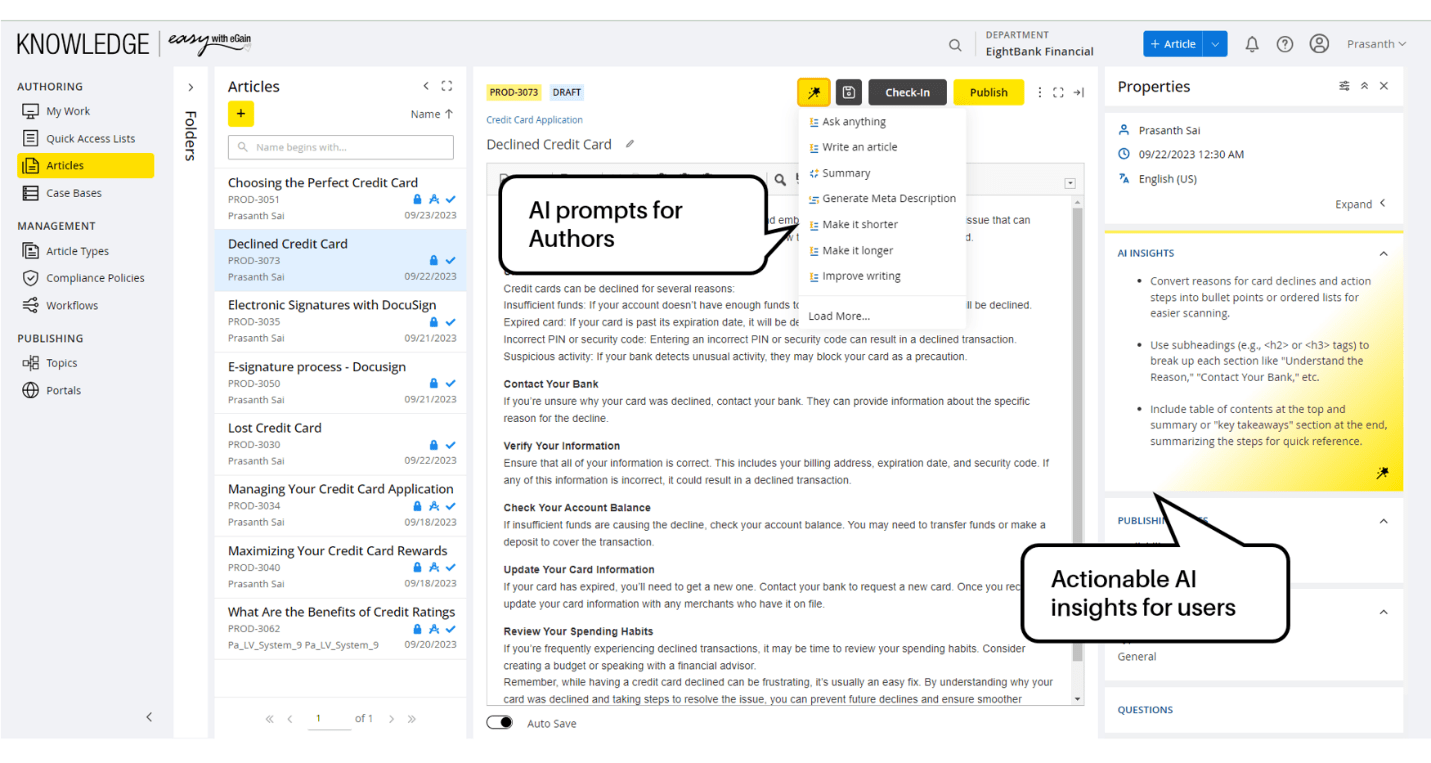

eGain's AssistGPT is powered by generative AI and helps customers find answers by further automating knowledge creation, omnichannel delivery methods, and optimization. Examples of its automation include:

Figure 3: eGain Knowledge Hub AI Example

eGain AssistGPT Example (Company Reports)

Source: Company Website

eGain's Knowledge Hub and generative AI products make contact center operations more efficient, saving companies time and money.

According to Gartner, generative AI helps turn byproducts of normal interactions into structured knowledge assets, which "radically reduces the effort required to capture institutional and subject matter knowledge in external, persistent forms." The company's Instant Answers feature, included in AssistGPT, gives answers needed to contact center agents quickly, rather than the agent reading an entire document of very detailed content to find their answer. This feature allows companies to essentially create virtual assistants for each of their agents. The results of these two products speak for themselves and should be extremely attractive to existing and potential new customers:

The company noted on its last earnings call that it is seeing positive momentum in new business activity given these new offerings and that the number of potential customers doing a 30-day free trial program is more than they have had in the last several years.

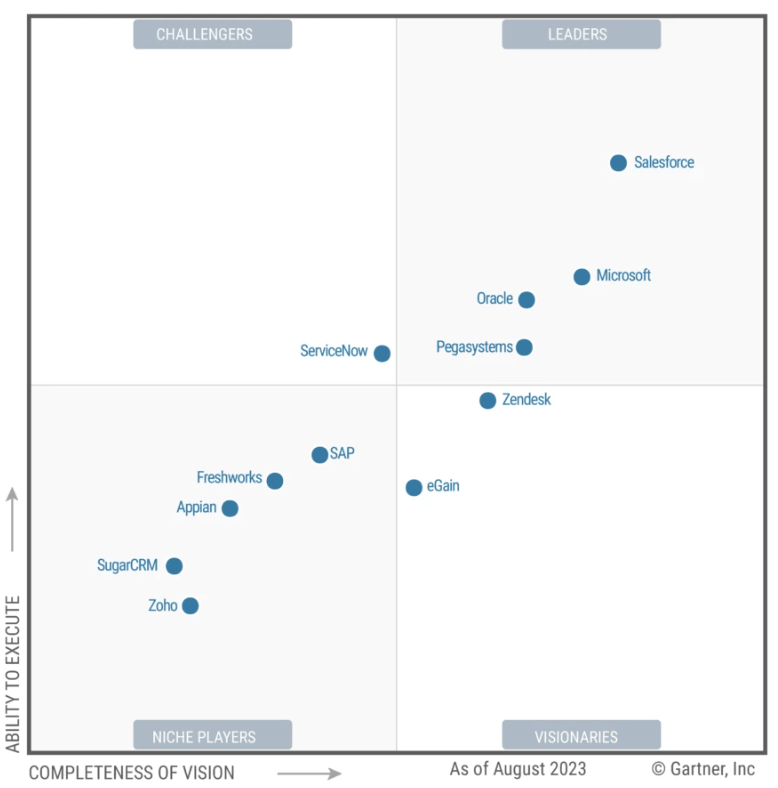

eGain was also listed as a "Visionary" in Gartner's 2023 Magic Quadrant for the CRM Customer Engagement Center. Gartner defines a "Visionary" as a company that is ahead of many of its competitors in terms of delivering innovative products with a strong potential to influence the direction of the market. Not only does this speak to the strength of eGain's Knowledge Management products, but it also serves as a free marketing tool that, we think, will result in increases in new potential customers.

Figure 4: eGain Named Visionary on Gartner's Magic Quadrant for the CRM Customer Engagement Center

Magic Quadrant (Gartner)

Source: Gartner, Inc

We see a very bright future for eGain if the company is able to even come close to the results that these past visionaries have had. Results for prior newly added "Visionaries" over the past ten years are impressive. Visionaries include:

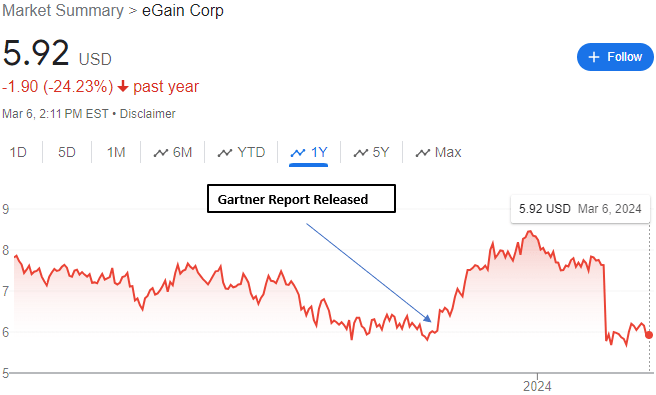

Clearly, the market saw this as a positive when the news was released in November 2023, and we believe the current drop in share price represents a great buying opportunity.

Figure 5: Stock Chart

Stock Chart (Google)

Source: Google

Currently, shares are down over 20% since eGain released its F2Q24 results. We feel that the company was unfairly punished and believe investors are misunderstanding the true growth prospects of the company, presenting an opportunity for savvy investors to acquire shares.

Despite its Knowledge Hub SaaS ARR increasing 6% Y/Y in the quarter, two customers that represent 8% of ARR have chosen to not renew their subscription with eGain. However, these customers are Conversation Hub and Analytics Hub clients and do not have access to the company's growth engine, AssistGPT, which is an integral part of the company's Knowledge Hub and the company's growth engine going forward.

As the company executes on its growth initiatives that have been reignited by AssistGPT, the contribution from Knowledge Hub SaaS ARR should have a more meaningful impact on overall revenue, as Knowledge Hub revenue now represents roughly 50% of total revenue, up from roughly 46% last year. We feel that investors are missing the forest for the trees.

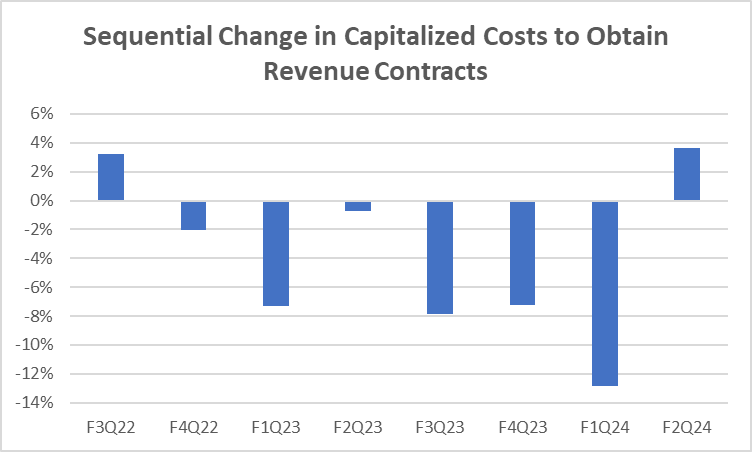

Since the company launched AssistGPT, we're currently seeing early indications that new customers have taken interest. The company's "costs capitalized to obtain revenue contracts" primarily relate to commissions paid to sales employees on new logo wins. Costs capitalized to obtain revenue contracts in F2Q24 showed sequential growth in the quarter, reversing a multi-quarter trend going back to F3Q22.

Figure 6: Sequential Change in Capitalized Costs to Obtain Revenue Contracts

Capitalized Costs (Company Reports)

Source: Company Reports

We look for continued improvement in this figure to assess the company's success in winning new clients. Given that AssistGPT was launched in September 2023, we believe this figure should continue to increase sequentially because the sales cycle to win new logos typically takes six months. We expect new orders to generate $200-$300K of ARR with opportunities to upsell products to new customers, increasing the ARR significantly. We also see low-hanging fruit for eGain to cross-sell AssistGPT products to its existing customer base. The product will generate an incremental fee for eGain based on the customers' usage of the generative capability on its platform.

According to Gartner, knowledge management tools have only penetrated 5-20% of the market. With AssistGPT reducing human effort by 80%, we believe that there will be a reacceleration of growth in knowledge management given these technological breakthroughs that will ultimately save money for eGain's customers.

While management has guided toward a decline in revenue for FY24 due to the loss of customers in its Conversation and Analytics Hubs, we believe the company is poised to benefit from the secular tailwind of increased spending on AI products and look to see further growth in the company's Knowledge Hub.

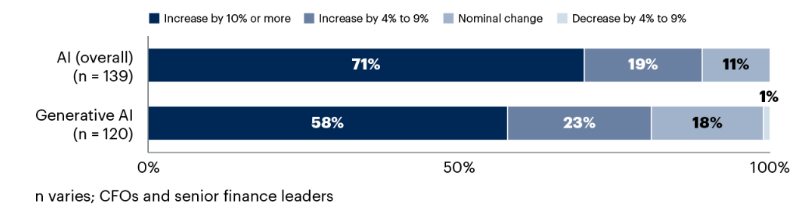

According to a Gartner survey of more than 300 CFOs and senior finance leaders, 90% of CFOs are projected higher AI budgets in 2024, with 71% of CFOs planning to boost spending on AI by 10% or more versus last year.

Figure 7: Gartner CFO Survey

Survey (Gartner)

Source: Gartner

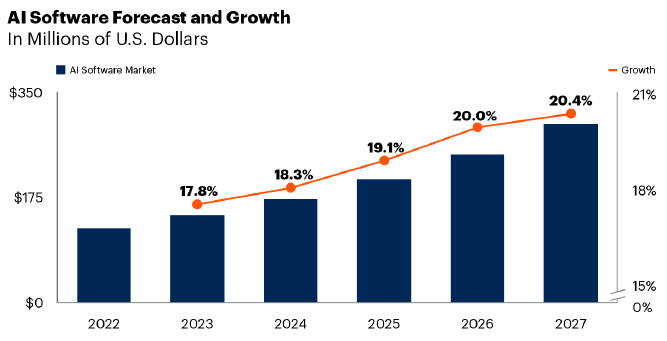

Gartner forecasts that the spending on generative AI software will increase by 19.1% per year from 2022 - 2027.

Figure 8: AI Software Growth

AI Growth (Gartner)

Source: Gartner

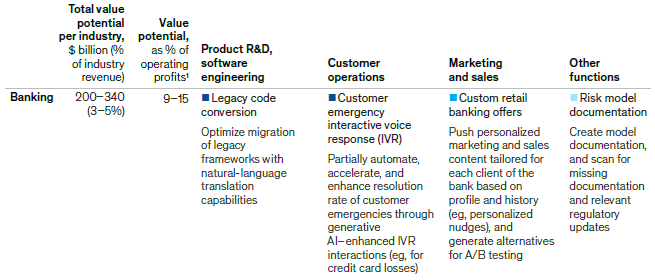

McKinsey estimates that generative AI could reduce the volume of human-service contacts by up to 50% in the banking industry (one of eGain's largest client industries), saving the industry billions of dollars. We note that eGain's products specifically assist with compliance issues in heavily regulated industries, such as the financial services and healthcare industries, making the company well-positioned to win new customers in the near future.

Figure 9: Banking Industry to Benefit from Generative AI

Industries benefiting from AI (McKinsey)

Source: McKinsey

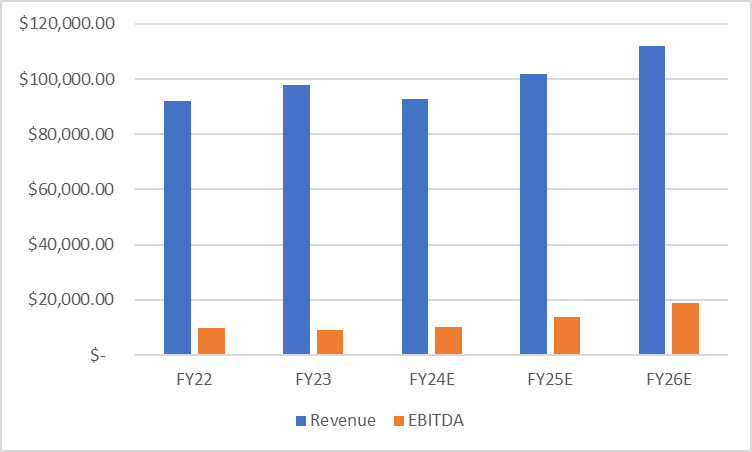

Our base case is that eGain will increase its revenues by 10% per year from FY24 to FY26. While we anticipate accelerating growth for its knowledge products, its conversation and analytics products may be a drag on overall growth. We see EBITDA growth of 36.5% per year from FY24 to FY26 due to the operating leverage inherent in its business models and the cost-cutting measures eGain has taken in the past year (over $15M in annualized OpEx savings).

Figure 10: Base Case Revenue & EBITDA Projections (Thousands)

Estimates Base Case (Company Reports, Philaretos Estimates)

Source: Company Reports, Philaretos Estimates

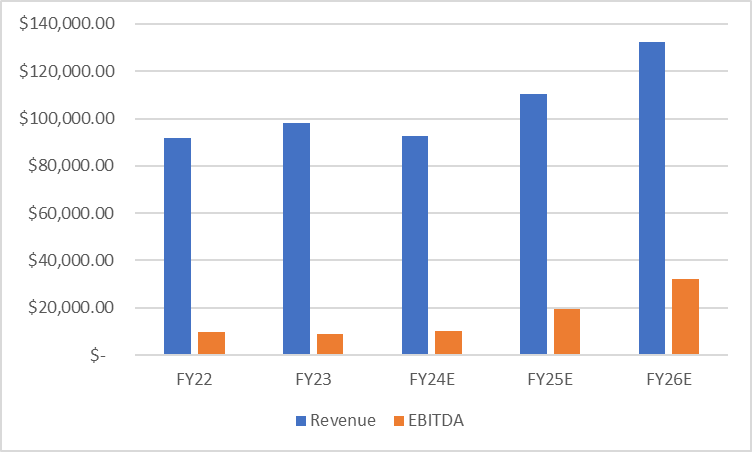

Our bull case is that eGain will increase its revenues by 19.5% per year from FY24 to FY26, in line with industry spending on AI. We expect EBITDA to nearly triple from 2024 to 2026 due to the operating leverage inherent in its business models and the cost-cutting measures eGain has taken in the past year (over $15M in annualized OpEx savings).

Figure 11: Bull Case Revenue & EBITDA Projections (Thousands)

Bull Case Estimates (Company Reports, Philaretos Estimates)

Source: Company Reports, Philaretos Estimates

With $2.78 per share in net cash (47% of current share price) and strong tailwinds for growth going forward, we believe eGain shares are cheap on an absolute and relative basis.

Figure 12: Base Case Valuation

Base Case (Company Reports, S&P Capital IQ)

Source: Company Reports, S&P Capital IQ, Philaretos Estimates

Based on a relative valuation analysis of FY25 gross profit, we value shares of eGain at $14.90 per share as our base case, which represents a 153% return from current levels in two years. Additionally, we anticipate cash to continue to accumulate on the balance sheet and see the company ending FY25 with $3.31 in net cash per share.

Figure 13: Bull Case Valuation

Bull Case Valuation (Company Reports, S&P Capital IQ, Philaretos Estimates)

Source: Company Reports, S&P Capital IQ, Philaretos Estimates

Based on a relative valuation analysis of FY25 gross profit, we value shares of eGain at $16.30 per share as our bull case, which represents a 177% return from current levels in two years. Additionally, we anticipate cash to continue to accumulate on the balance sheet and see the company ending FY25 with $3.44 in net cash per share. We also note that a 5.1x multiple on gross profit in FY26 produces a fair value of nearly $20.

With nearly half of its market cap in cash and a fair value between $14.90-$16.30 per share, we believe eGain has a large margin of safety and should be accumulated aggressively at current levels due to short-term weakness in the company's share price.

Catalysts for a re-rating include:

In our opinion, eGain shares are materially mispriced. The company has industry growth tailwinds spurred by increased budgets from potential customers looking to spend more on AI. It has the opportunity to cross-sell its AssistGPT and Knowledge Management products to existing customers and is seeing momentum in its sales pipeline as made evident by the large quantity of trial periods it has given prospective customers. New and existing customer wins will likely lead to a reacceleration in revenue growth and margin expansion going forward. eGain is cheap relative to its peers and on an absolute basis, we believe shares should be bought aggressively at current levels.