Andriy Onufriyenko/Moment via Getty Images

Andriy Onufriyenko/Moment via Getty Images

I wrote about Varonis Systems (NASDAQ:VRNS) previously with a buy rating, as I was fond of the progress that VRNS is making in its transition to a SaaS model that has long-term benefits because of its higher contribution margin and shorter sales cycle. To give a quick background on the transition, I cite from my previous post:

Like many high-growth software companies, VRNS was a business that grew at a very high rate (30+%) in the initial part of the 2010s. However, growth dipped significantly in FY19 to -6% from 25.5% in the previous year due to the pandemic. Growth was further slowed down as the business went through the transition into a SaaS (software-as-a-service) model in recent quarters (LTM growth now at 6.6% vs. 21.4% in FY22 and 33.3% in FY21). On the other hand, regarding profitability, the business has never been profitable over the past decade. Positively, the business has always been in a net cash position. As such, liquidity was never a problem for the business, despite the cash burn

In this post, I reiterate my buy rating for VRNS as management continues to execute strongly on the SaaS transition and has clinched an important partnership deal with Microsoft that allows it to better ride on the increased utilization of AI.

VRNS outperformed in 4Q23 on almost all fronts. ARR (annual recurring revenue) grew 16.7% to $517.5 million, with net new ARR (NNARR) growing 47% annually and 24% sequentially to $25.5 million. Revenue performance followed in the same direction, increasing by 8% to $154.1 million, beating the high end of management's own guidance ($150 to $154 million range) and consensus expectation for $152 million. Within it, subscription revenue grew 11% to $129.2 million, while maintenance and services were down 4% to $24.9 million. Non-GAAP EBIT saw $27.2 million, which was also above management's guided range of $25 to $27 million, which translates to an EBIT margin of 17.7%. Lastly, non-GAAP EPS of $0.27 also came in higher than management expectations.

I am very satisfied with VRNS's progress in its SaaS transition, which was evident in the 4Q23 results as SaaS now accounts for 66% of new business ARR, up by 700bps vs 3Q23. Note that this is way above management guidance of 60%. On a total ARR mix basis, SaaS is now ~23% of total ARR, up by 800bps sequentially, and management noted that they continue to see solid traction from both new and existing customers. We can also see the strong impact of this shift in the difference between revenue growth and ARR growth, but it is for the longer-term good as SaaS has better pricing compared to on-premise products. It is also becoming increasingly clear that the transition will drive a long-term expansion of margin, as 4Q23 saw ARR contribution margin step up by 230bps to 13.4% vs. 3Q23, reflecting a more favorable margin contribution from SaaS. To give a good precedent on how long this margin expansion can last, I use Adobe (ADBE) as an example. ADBE first launched its SaaS model in 2012, which caused its EBITDA margin to fall by 800bps over the next 3 years. However, the EBITDA margin went ahead and expanded for the next 7 years until COVID-19 happened.

While the faster the SaaS transition, the bigger the near-term headwind to revenue growth, there is a silver lining here that helps to cushion this impact by improving unit economics - conversion of existing customers. In 4Q23, VRNS realized ~$15 million of conversion from existing customers, and I view such conversion very positively as it drives better attach rates, a 25-30% pricing uplift, and higher margins. We should start to see more apparent impacts from this uplift moving ahead as VRNS progresses towards Phase 2 of the transition (starting in 2H24), where management will focus on the conversion of the installed base.

So, Jason, I'd start by saying that that 25% to 30% uplift is actually a significant incentive for our customers to convert, because the total cost of ownership saves them money. So, yes, they pay more on our price list. Company 4Q23 earnings

In addition to conversions, I expect that the recently released Managed Data Detection and Response [MDDR] system, which aims to halt threats at the data level, will bolster performance. Based on management comments, MDDR is ASP, and margin accretive (similar margin as the SaaS model) should boost renewal rates. Another positive aspect of the transition to the SaaS model is well highlighted here, in that it provides VRNS with more opportunities to cross-sell or up-sell new products because of the increase in touchpoints and frequency.

Lastly, I see the partnership with Microsoft (MSFT), which secures MSFT's M365 Copilot, as a major growth driver over the long term (with increased AI utilization as the main secular growth driver)because of the strong distribution power of M365. By leveraging M365, VRNS can gain access control business for Copilot with its current product line. In addition to acquiring more logos, Copilot motivates its current customers to upgrade to SaaS and make use of the automation engine, which opens up more opportunities for upselling.

With SaaS, we have been able to innovate much faster, we have gone wider with more coverage of enterprise data stores, and we have gone deeper, adding more automation, so that our customers can achieve their business outcomes with very little effort, but this is just the beginning.

First, it's just a tremendous amount of automation, and with ease, we can cover many more data repositories. But also with the MDDR, the automation, the threat detection response, the classification, the data protection, we can do so much more for customers. Company 4Q23 earnings

The visible catalyst ahead is the demand generated by increased utilization of AI. The truth is that data access controls are more important with AI tools like MSFT Copilot. The use of access controls allows AI tools to determine who has access to what data. Protecting passwords and HR records from AI tools requires precise and real-time access controls. Because of this intricacy, VRNS's value proposition is enhanced, as it provides the ability to automatically see and implement access controls. In addition, VRNS has classification capabilities that let users automate data labeling. These capabilities are fast, accurate, and necessary for AI tool guardrails. Although it's early days, management has noticed that GenAI has been a common topic in customer conversations recently. I think this bodes well for data security and governance, as customers are focused on protecting sensitive information from LLM data leaks.

May Investing Ideas

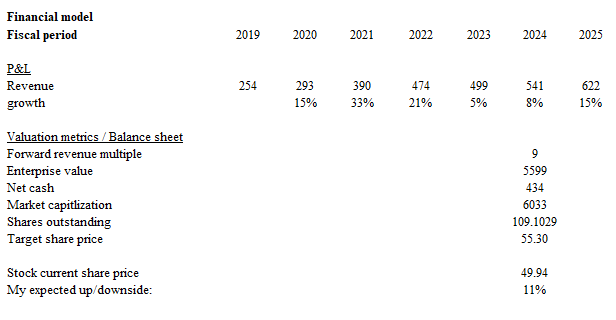

Based on my research and analysis, my expected target price for VRNS has increased from ~$50 to $55.30.

The subscription net retention rate dropped to 107% in the most recent quarter, which, if it continues to decline at a higher rate, may indicate that customers are not particularly enthusiastic about VRNS products. From what I understand, management has acknowledged that the significant decline in NDRR was most likely caused by the friction in the pipeline caused by the introduction of SaaS. Nonetheless, this is an area to monitor.

I am giving a buy rating for VRNS. 4Q23 results exceeded expectations, showcasing robust growth in ARR. The progress in the SaaS transition is moving along very well too, with SaaS now accounting for 66% of new business ARR. Conversion of existing customers, the release of the MDDR system, and the Microsoft partnership all support a positive outlook. Lastly, I see the increased utilization of AI as a visible catalyst for VRNS, as it highlights the value proposition of VRNS offerings.