Don Juan Moore/Getty Images Entertainment

Don Juan Moore/Getty Images Entertainment

I have not looked in on the softline retail name Vera Bradley (NASDAQ:VRA) since last February (2023), and as it remains a popular brand in my social circle, I like keeping an eye on how the business is doing. Last year, from an investor standpoint, I considered Vera Bradley a hold on working capital challenges with inventory management and the challenge of sustaining margins. While the shares have appreciated in value overall since then, they did take a dive on the release of fiscal year 2024 results a few days ago.

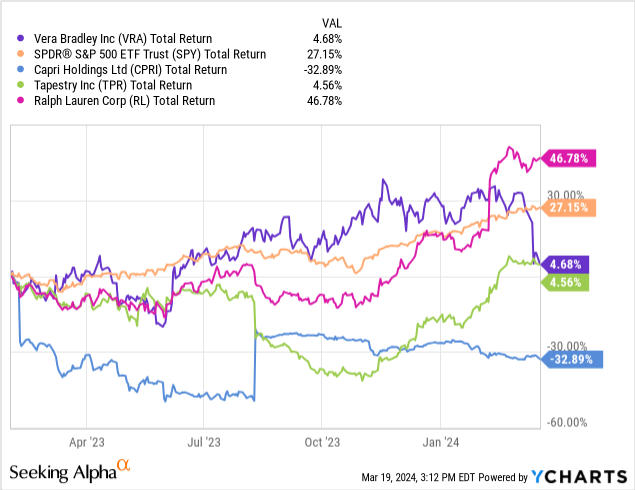

My past view has been that Vera Bradley was not suitable as long-term "buy and hold" sort of investment, as it has historically struggled to create lasting shareholder value. For much of the past year, Vera Bradley shares were outperforming the S&P 500 (SPY) and luxury clothier Ralph Lauren (RL), just losing ground to both recently. On the other hand, Vera Bradley equity has remained well ahead of other peers like Capri Holdings (CPRI) and Tapestry (TPR). On the recent drop, however, I think there is merit for a potential entry point on the shares.

After more than a year since checking in, I am especially looking for positive progress on the inventory status and any clues that margins are headed up in a sustainable way, but I'll walk through the basic flow of their full-year results (fiscal year ended 2/3/2024).

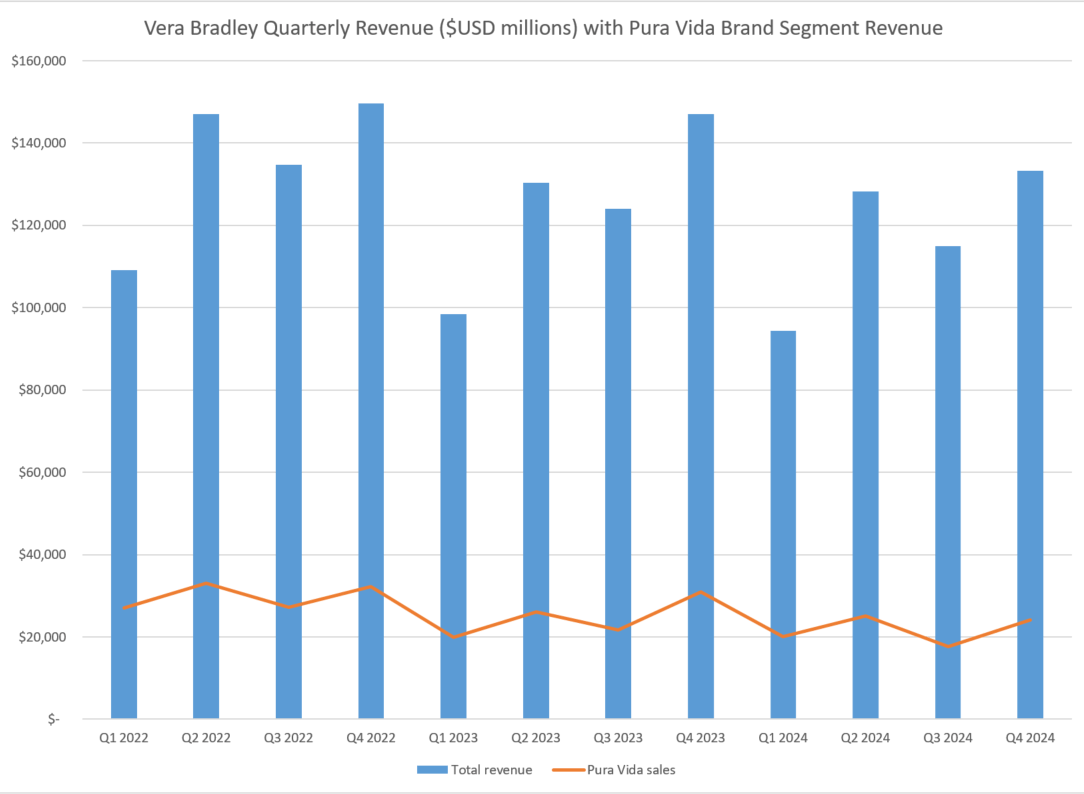

Starting from the top, the sales funnel is not one that ever had a great track record of showing reliable growth year to year, going back multiple years. Bear in mind that Vera Bradley finished buying out the accessories brand Pura Vida in January 2023, which originated as a deal in 2019 with hopes of buying into growth. That effort stalled, whether from unfortunate pandemic timing, changing fashion fads, mismanagement, or some combination of other factors, but whatever the reasons, Pura Vida's revenue growth has not materialized, nor have Vera Bradley's core softline products.

Vera Bradley Revenue Trends, fiscal 2022 - 2024 (Author's spreadsheet; data from Vera Bradley 10-K and 10-Q filings)

The overall revenues, while impacted by obvious seasonality for the sector, have clearly not perked up as a result of adding the Pura Vida brand.

Total sales in Q4 came in at $133.3 million, versus $147.1 million in the year-ago quarter, with Pura Vida accounting for $24.2 million of that total, or 18%. Gross margin of 52% was greatly improved versus the comparable quarter for fiscal 2023, which stood at just 41%, suggesting much better pricing power and inventory management for the period. In spite of the drastic gross margin improvement, EPS for the quarter was a loss of ($0.06). On a fiscal year basis, total revenue of $470.8 million was a drop of 6% over fiscal 2023, with Pura Vida accounting for ~$87.1 million, which puts it at 18.5% of the total, in-line with the 4th quarter. In a similar vein as the Q4 improvement in gross margin, full year GM also saw strong gains, from 48% to 54%, helping drive EPS of $0.25 for the year, versus a full-year loss of ($1.90) for fiscal 2023.

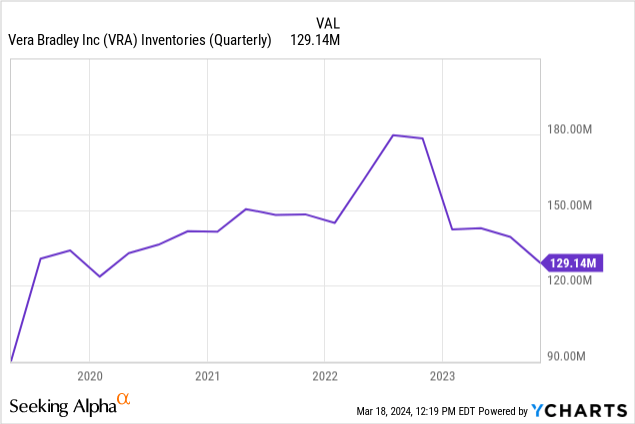

In spite of the drop in sales, the profitability trend is certainly much improved overall, as working capital improvements in inventory combined with stronger pricing power starting flowing through the income statement. Inventory specifically saw a nice drop, declining from $142.3 million at the end of fiscal 2023 to $118.3 million at the close of fiscal 2024, a health 17% drop year over year (the YCharts below is not totally current, reflecting the value at the end of Q3, but the trend is evident, and continued downward for Q4).

Inventories ended the year in-line with the sort of pre-pandemic inventory level, which suggests at long last a sort of return to normalcy, and supports the narrative on the improvements in gross margins in the last year.

Elsewhere on the balance sheet, Vera Bradley has carried no net debt, which remains the case today, with some $77 million in cash and equivalents as of fiscal year end, and no debt. In a the high-rate environment, this is a fairly attractive combination, as it is receiving a nice return on its cash and does not have material interest expense to offset the benefit; it netted $0.9 million in interest income alone for the year. In terms of cash flows, major sources of cash during the year were operating cash flows of $48 million (of which essentially half was from the improvement in inventory management), while the major use of cash for the year was the $10 million for the final 25% stake in Pura Vida. Other investments in CapEx came to just $3.8 million, with an additional $2.2 million in share repurchases, or "approximately 0.4 million shares at an average price of $6.10" according to the earning press release (see link above).

So while last quarter and overall results for fiscal 2024 were material improvements compared the previous year, the shares nevertheless nosedived with the earning release. Clearly this response suggests there was something in the fiscal 2025 guidance that investors did not care for.

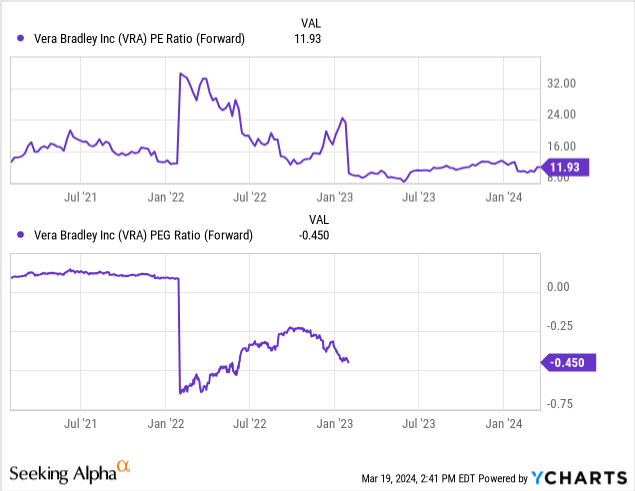

I would not be so bold as to claim I can explain the reaction in full, but I believe there are probably two driving factors. First of all is the expectations around cash flows and earnings. While free cash flow for the past year was strong $44 million (operating cash flow less CapEx), so much of that was driven by the one-time improvement in inventory that it cannot be repeated. Guidance for free cash flow for fiscal 2025 is $10 million, which is still quite a drop off, but due primarily to more extensive CapEx investment in the company's retail footprint, upgrading its physical stores and so forth. So instead of $3 million in CapEx as was the case the year just ended, the guidance for FY 2025 is $12 - $14 million. While there is ~$25 million remaining on the existing share repurchase authorization, it clearly could not be fully funded alone by free cash flow. The initial guidance on diluted EPS for the year is a range of $0.54 to $0.62, assuming 30.1 million shares (no impact from repurchases). Taken at its midpoint of $0.58, the forward P/E at the closing share price of $7.11 on March 12th was 12.25x - not stretched by any measure, but the market was excited by the guidance, as it is not pointing towards any growth in the business for this year. But it compressed further as the guidance came out, and now the P/E is about 11x, below its historical ratio, and reflecting reservations about the limited growth outlook.

Analyst Joe Gomes of Noble Capital Markets put the question to management this way on the earnings call, with Michael Schwindle, the fairly new CFO responding (edited lightly for length):

Joe Gomes: So fiscal 2025 is based on your guidance today, kind of going to be a replay of 2024 from a financial point of view. What do you think, or what do you see could occur that might make 2025 a better outcome from a financial point of view than 2024?

Michael Schwindle: I think the first and the biggest of this would be customer reaction on the other side of New Day. So to the extent that consumer reaction is obviously better than what we had planned, that would obviously be better results as well. I think additionally we are anticipating some continued macroeconomic overhang. We saw sequential declines in traffic patterns across most of the year. . . So we have continued to anticipate that some portion of that's going to continue to hang over into 2025. So if that outlook gets better, then of course the rising tide lifts all boats on that as well.

The second thing I would point to is some degree of uncertainty in how the current corporate strategy initiative will work out. Management spoke of both "Project Restoration" and "Project New Day" in the course of the call. The first, "Restoration," was described as the "comprehensive review of the consumer, brand, product, and channel components for both of our brands" that started a little over a year ago. It was a sort of strategic evaluation, and in essence, it has led to the launch of the second, "New Day," which is the implementation of new strategic efforts based on the findings from "Restoration" and will be rolling out around the middle of this year.

CEO Jacqueline Ardrey's prepared comments went into the specifics at some length, but I have summarized for brevity some salient content of the plans and assumptions.

1) For the Vera Bradley brand

2) For the Pura Vida brand

My point in laying out this summary is not how genius or cutting edge it is, but rather just how routine it is, pretty much the same verbiage you would find from any other traditional retailer whose sales are under pressure. From an investor's perspective, there really is nothing to generate much excitement here - closing underperforming stores and investing in better performing locations is a tried-and-true approach. The strategy is not projected to lead to material financial improvement this year (as seen in the above guidance), and the valuation multiples reflect that sentiment.

With the P/E multiple being under its 5-year average, and in spite of the operational challenges to get growth going again in a fairly low-growth category, I like the valuation here at around $6.00 and change per share. The free cash flow looks to be positive once again, the inventory problem has been worked out, and I do not expect the elevated CapEx investments happening in 2024 to remain at that level consistently, which should leave room for the buybacks to continue. With ~$25 million remaining under the buyback authorization that is in place until the end of this calendar year, assuming even an elevated average buyback price of $8 per share would take out 3.1 million more shares, or 10% of the share count.

As there is no debt and a healthy balance sheet to work from, I think the downside risks are minimal, and I consider Vera Bradley a buy at the moment, with a price target of at least $7 (from the impact of the buyback alone), and any uptick in growth would be a welcome surprise. My ongoing caveat with Vera Bradley is that I consider it more suitable for short-term holding or trading, and is not necessarily suitable as a long-term hold over multiple months or years for value creation.