Marco VDM/E+ via Getty Images

Marco VDM/E+ via Getty Images

The purpose of this article is to evaluate the iShares U.S. Utilities ETF (NYSEARCA:IDU) as an investment option at its current market price. This is a fund "to track the investment results of an index composed of U.S. equities in the utilities sector" and offers exposure to U.S. companies that supply electricity, gas, and water, as well as waste management services.

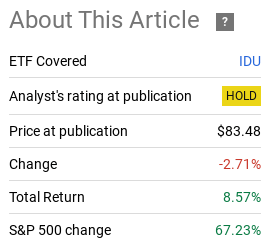

I cover the Utilities sector regularly, but it has been a while since I looked at IDU in isolation. In fact, the last time I did was back in 2020 when I put a "hold" rating on the fund. In hindsight, this relative caution was the correct assessment based on its performance since that time:

Fund Performance (Seeking Alpha)

With 2024 off with a bang, I figured it was time to take another look at more defensive options - including the Utilities sector. While I normally invest in - and write about - the Vanguard Utilities ETF (VPU) and the BlackRock Utilities, Infrastructure, and Power Opportunities Trust (BUI) - IDU is back on my radar for a couple of reasons. I actually see the fund as a "buy" now, to supplement my other Utility-focused holdings, and I will explain why in detail below.

To begin this article, I want to take some time to look at the macro-equity environment and discuss why I see merit to building on to defensive positions. This can mean Utilities, but any number of other equity hedges could also be relevant here. These include Real Estate, Consumer Staples, quality bonds, cash, among other sectors.

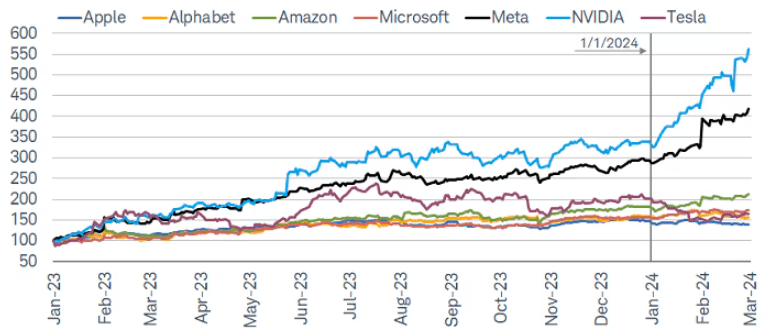

The logic here is this market continues to push to new highs which, while a positive, has me a bit concerned because of how concentrated the gains are. As my followers know, I am not a "bear" on Big Tech or the Magnificent 7. I have been expressing caution for a while now and those themes keep moving higher nevertheless. Yet, I am not upset about this, because I have plenty of exposure to the S&P 500 and NASDAQ 100. But this doesn't mean I want my entire portfolio exposed to just a handful of names. This is not good portfolio management or proper diversification, no matter how tempting the current "alpha" is that the Mag 7 is providing.

Beyond that, we are starting to see some push-back to this performance. Even the Mag 7 is not immune to some market pressure, with stocks like Apple (AAPL) in particular seeing some negative sentiment over the past few weeks. So now, in the more immediate term, we are seeing even fewer tickers push the broader indices higher - which is all the more concerning to me:

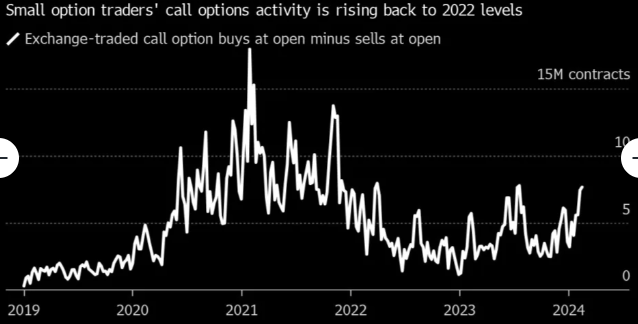

Mag 7 Becomes Mag 2? (Bloomberg)

What I view from this is that some of the high-flying stocks are starting to see more modest gains and that means we will need to see more market breadth in order to see new market highs. This is important for the overall health of the market, and also a reminder to be diversified and prepared for such an occurrence. I see a market whose valuations are rising on the backdrop of a few shining stars and that cannot continue forever. Yet, despite my sense of caution, equity investors are piling on hopes for higher and higher levels in the short-term based on options activity:

Volume of Option "calls" Rising (Yahoo Finance)

The conclusion I draw here is that investors need to be careful at these levels. Rising bullish sentiment and rising share prices can be great for momentum buyers, but I use times like this to prepare for when that momentum ultimately runs out. The lack of market breadth combined with rising optimism among retail investors is an environment where I lean towards building on to my defensive holdings, rather than chasing more gains in my top performers.

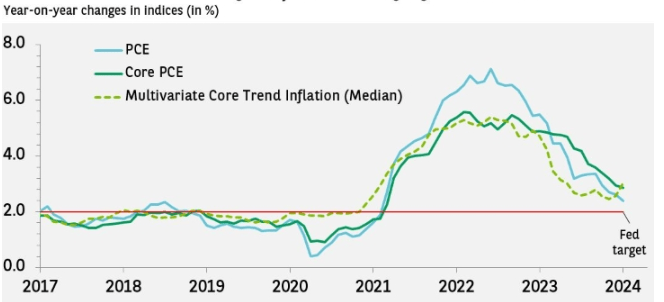

Aside from the overarching theme of equity markets getting a bit frothy, the positive news for utility stocks has been the consistent decline for inflation. While still above the 2% Fed target, inflation's decline is notable and bodes well for income-producing sectors like Utilities:

Inflation Metrics (US) (Fed of NY)

The Utilities sector has a long standing relationship to move in an inverse direction with inflation and interest rates. So a decline in this metric is essential - in my opinion - for maintaining a bullish outlook on this idea.

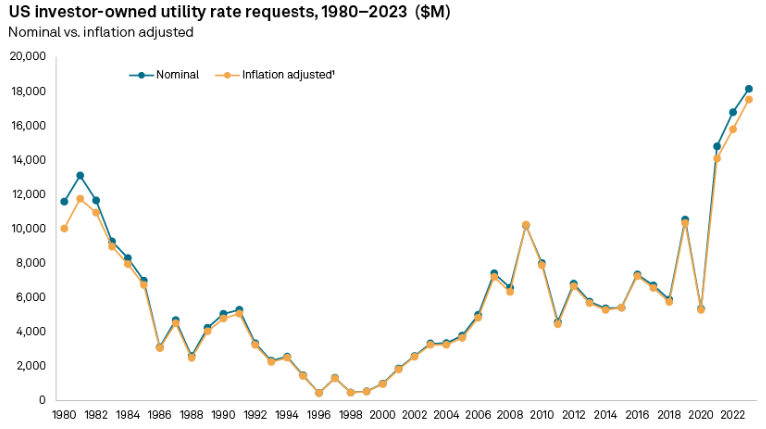

Another reason why I view Utilities as a reasonable bet in 2024 is the underlying companies have been trying to keep up with inflation via boosting revenues through rate increases. While a rate request is only that - a request - and not a guarantee of an eventual pass-through to end users, I like the fact that utility companies have been modest in their requests. While they seem high on the surface, on an inflation-adjusted basis the rate increases are in-line with what one would actually expect:

Utility Rate Increases (US) (S&P Global)

While I know (or greatly suspect) all requests won't ultimately be approved, this is still a tailwind for the sector if most do. This will help shore up revenues during a difficult macro-climate given how elevated borrowing costs are. Further, it lends support to the idea that Utilities can actually be somewhat of an inflation hedge since they can pass on some of their higher costs to their customers. In short, I think this negates some of the bearish sentiment that has been clouding the sector of late.

Let us now look into IDU individually. Why is this a smart choice for readers to consider when looking at the Utilities sector? After all, there are a host of ways to get exposure to this arena, so IDU needs to have a couple of clear positive attributes to get the discussion off the ground.

Fortunately, there are multiple reasons I like this fund. One is the passive, diversified nature of it. This is critical to any sector ETF I evaluate. There are some (especially in areas like Energy, Consumer Discretionary, and Communications Services) that are dominated by a couple of names. For example, top-heavy Energy funds hold a disproportionate amount of Exxon Mobil (XOM) and Chevron (CVX). Similarly, some Consumer Discretionary Funds are greatly exposed to Amazon (AMZN) and/or Alibaba (BABA). There is nothing "wrong" with owning these companies - I am not suggesting that at all. But I don't see the point in buying a sector ETF if you are just going to have half the fund in a couple of names. Just buy those names directly and save yourself the management fee.

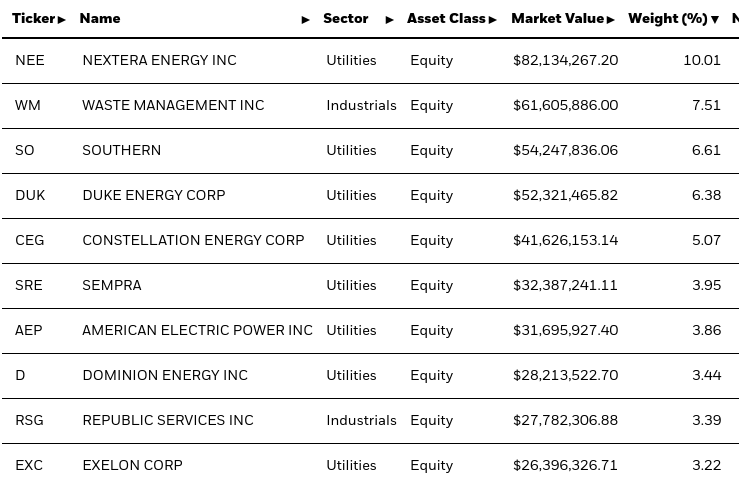

But IDU is not like that. The top holding is a bit heavy at 10%, but there is good diversity and balance among the rest of the primary tickers:

IDU's Top Holdings (iShares)

A second point to consider also concerns the top holdings. While I stated at the onset why I like "Utilities", IDU actually offers more than just Utilities (despite the name). I see this as an added bonus because waste management (trash and recycling) services is a relatively boring area that I have been bullish on for a while. This is especially true when I want to get defensive. In fact, I used to own Waste Management (WM) directly, but have now used IDU as a way to have some indirect exposure to that name and simplify my portfolio holdings. With WM and Republic Services (RSG) combining for over 10% of total fund assets, this sector ETF actually gives investors exposure to more than one pure sector.

This is important to understand either way. For me, I view this positively, and it is important for why I added IDU when I already own VPU. The Vanguard Utilities ETF does not have this "trash" sector allocation the way IDU does. So I can buy two "Utilities" funds that actually complement each other, rather than offering duplicative exposure.

However, this may not be what some readers want. If that is the case, understanding what is actually held by IDU is perhaps even more important. If you want a pure Utilities sector ETF, then IDU is not the best choice out there. This is a great lesson for why diving into what the fund actually holds - rather than just relying on the title of the fund - is essential.

A third positive for IDU is how the expense ratio has declined (albeit slightly) over time. When I wrote about this fund in 2020, I noted the expense ratio was a bit high at .43%. This is especially true compared to VPU, which comes in at just .10%. Today, IDU charges a lower amount at .40%:

IDU's Stats (iShares)

Granted, this is still a bit too high for my liking but I like the trend that it is moving in the right (lower) direction. Further, this is why the fact that IDU differentiates itself a bit in terms of holdings allocation compared to VPU is so important. If the funds were exact replicas then VPU is the obvious choice because it would be cheaper to own the same exposure. But IDU, while charging a bit more, has some nuances that VPU lacks. This, combined with the fact the IDU's expense has indeed declined over the years, is key to why I see this fund as a "buy" at the moment.

The premise of this review is that I believe equity valuations are a bit extended and that could lead to some volatility in the weeks and months ahead. There continue to be major risks that I don't see reflected in stock prices broadly. These include an elevated interest rate environment, a shaky commercial real estate sector that is facing markdowns on valuations, and geopolitical risks from an upcoming US presidential election, war in Gaza and Eastern Europe, and heightened tensions with China. All of these attributes indicate to me that getting defensive with Utilities is a wise move.

Expanding on that, I think IDU can supplement my existing exposure to the sector. While it still trades mostly in-line with other ETFs like VPU, there is some divergence given IDU holds significant exposure to the waste management sector. Over time, this has helped with some slight out-performance:

5-Year Returns (IDU and VPU) (Google Finance)

Ultimately, I still like VPU, but I see enough catalysts to speculate IDU will move higher from here. I like the fund's make-up, lower expense ratio over time, and defensive tilt. Therefore, I am upgrading this ETF to "buy" and suggest to my followers they give the idea some thought at this time.