Win McNamee

Win McNamee

The current Federal Reserve has two operating tools it is using to manage the inflation situation.

The first tool is quantitative tightening, or, reducing the size of the Federal Reserve securities portfolio.

It is still continuing a path that it has been on for two years.

The second tool is market guidance, or, presenting the interpretation of where the Fed's policy rate of interest should be and what changes might be in store for the future.

The Fed continues to hold its policy rate of interest steady but it suggests that there may be three reductions in the policy rate of interest in 2024.

"The stock market rose to new highs Wednesday when a narrow majority of Federal Reserve officials reaffirmed projections to cut interest rates three times this year despite firer-than-anticipated inflation in recent months,"

writes Nick Timiraos on the top of the front page of the Wall Street Journal, Thursday morning, March 21, 2024.

Inflation, using the Fed's preferred gauge, "has fallen to 2.8 percent recently, down from 4.8 percent one year ago."

So, we are in the middle of a debate. And, debates revolve around many uncertain things. These debates revolve around what is happening now and what is going to happen in the future.

Much of what is debated revolves around guesses.

We are in the world of "market guidance," the second of the current Fed's operating tools.

Investors in the stock markets like the conclusions presented by the Federal Reserve.

The S&P 500 Index (SP500) and the NASDAQ Composite Index (COMP:IND) hit new historical highs at the close of the day.

So, looking at the Fed's two "tools," we see that the central bank has just finished its second year of quantitative tightening, but the stock market is hitting new historical highs.

What is going on here?

The Fed has been engaged in quantitative tightening for two years and has reduced the size of the Fed's securities portfolio by more than $1.4 trillion.

But, one has to ask, as I have been trying to do, about all the securities that the Fed bought during the Covid-19 pandemic and the following economic recession.

The Fed increased its securities portfolio by $4-$5 trillion during that period of time.

And, in its quantitative tightening, the Fed has only reduced its securities portfolio by $1.4 trillion.

Is this all that is needed?

I have been writing a lot about all the "money" that is still in the economy, my latest effort was my recent post titled "The Wall of Cash."

There is lots and lots and lots of money running around in the U.S. financial system.

Notice, I said the U.S. financial system.

I did not say the U.S. real sector of the economy, the sector that produces real goods and services.

A very large part of the Fed's injection of money into the economy went into the financial sector and not the "real" sector and, as a consequence, the financial sector prospered and the "real" sector did not do as well, one reason inflation has not been a bigger problem than it has been.

The major evidence of this?

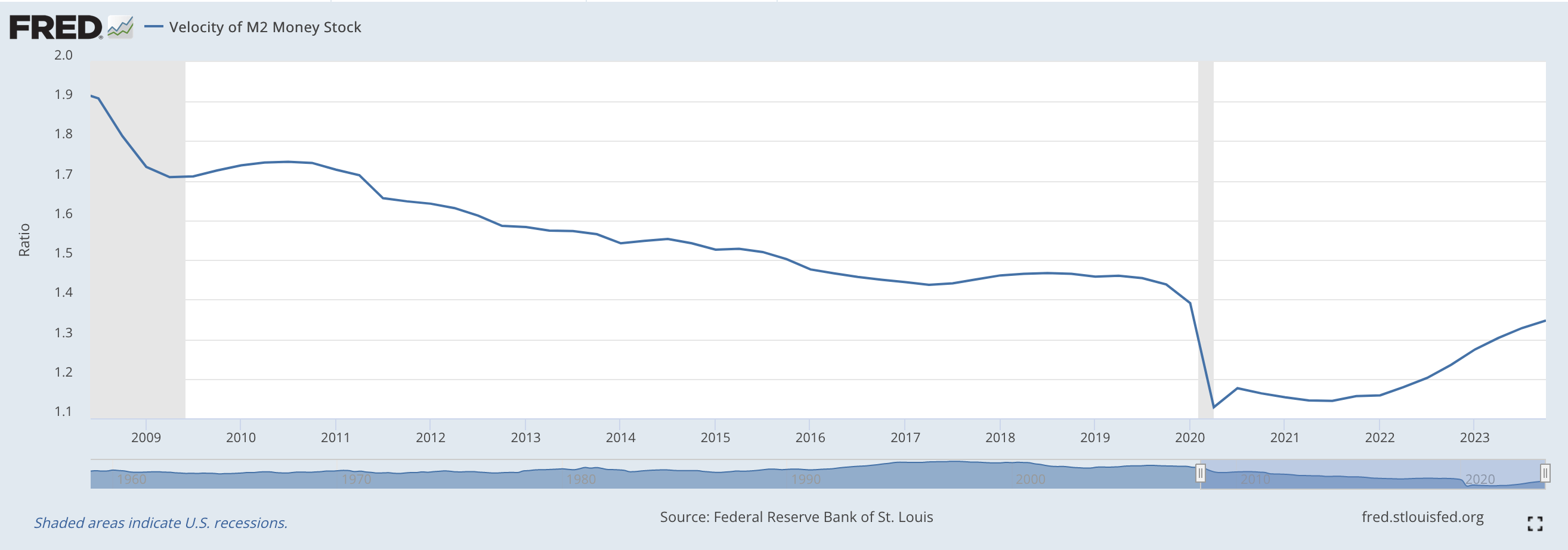

The income velocity of the money stock declined and has not returned to previous levels.

Take a look.

Velocity of M2 Money Stock (Federal Reserve)

So, lots and lots of money has been generated since the Great Recession, but, less and less of the increasing money stock has gone into the purchase of real goods and services while more and more money has gone into the financial sector.

And, especially notice what has happened to the velocity measure since the beginning of the Covid-19 pandemic.

Why is there so much money "hanging around"?

Well, people are not spending it. The money is going into financial assets, into the stock market, and, into money funds.

Yes, the velocity of circulation has risen in recent times as economic affairs have become a little more settled, but, there is still lots and lots of money out there in financial assets, monies that could at some time or another flow into the purchase of goods and services.

This is something the Federal Reserve has to be concerned about.

But, this is why the Fed can be "tightening" and the stock market can be rising...at the same time.

The other problem connected with this picture is the fact that the money flowing into financial assets is generally associated with wealthier people. That is, it is usually wealthier people that are able to take advantage of the plenitude of money floating around and increase their wealth and income.

The less-well-off are not the ones that have been able to take advantage of strong and active financial markets.

And, as we see in the economy, these people are having a harder time making ends meet, buying and holding onto homes, and finding jobs.

This division might become even a larger factor going forward if the Fed has to do more to hold down the wealth that is accumulating so much of the rewards these days.

So, the concern about unemployment and avoiding a recession. Mr. Timiraos writes about these factors in his piece in the Wall Street Journal.

Mr. Powell and the other Fed officials are attempting to walk between all these issues. That is why they are struggling with the market guidance part of their current efforts.

Yes, watch what the Fed is saying...and doing...about its policy rate of interest but still...watch what the Fed is doing with its securities portfolio.

There is a lot going on right now. There is a lot of uncertainty around right now.

These are not easy times.