amgun

amgun

Orange S.A. (NYSE:ORAN) reported financial results for the full year 2023 (FY-2023) last week with revenues of 44,122 million euros representing a YoY increase of 1.8% driven mostly by its African and Middle East operations. Consolidated net income increased even more by double-digit figures or 10.5% made possible by higher-priced subscriber plans and cost reductions championed by the new CEO, Christel Heydemann, appointed in April 2022.

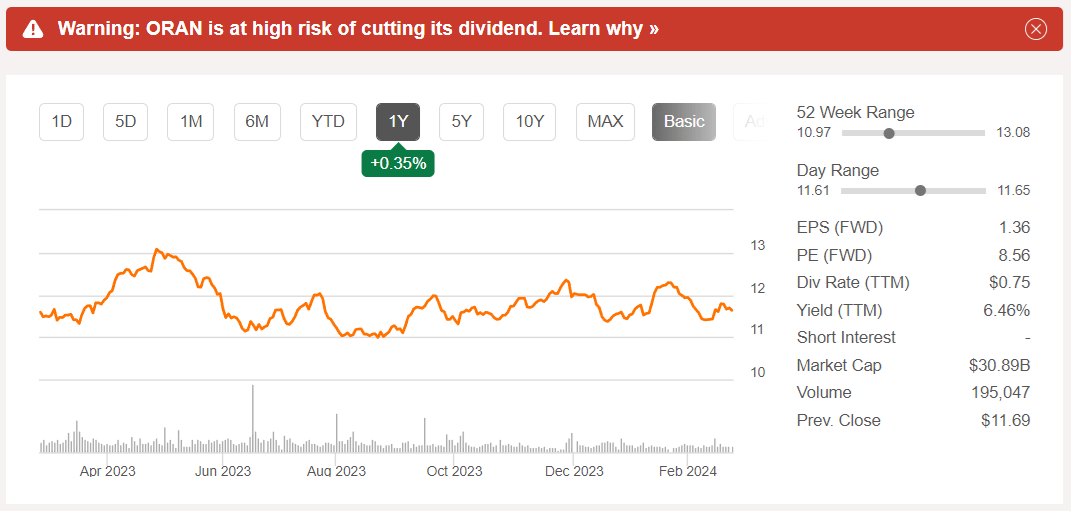

However, given the risk of its juicy dividend yield of 6.46% being cut as pictured below, this thesis focuses on capital spending reduction and cash flow generation efforts to chart an investment case.

(Seeking Alpha)

In this respect, the European Commission approving the merger of its Spanish operations with MasMovil is a positive in a market where it not only faces tough competition but at the same time has to invest a lot of money in expanding fiber and 5G infrastructures. Another positive is the way regulators have packaged the deal, which bears some similarities with the T-Mobile (TMUS)-Sprint merger four years back.

I start by showing how the European telecommunication industry is ripe for consolidation, following the lessons learned on the other side of the Atlantic Ocean.

Competition remains fierce, especially for the larger integrated service providers like Orange, which initially enjoyed a monopoly status in a market dominated by copper-based fixed telephony and ADSL internet. These incumbents gradually evolved to become MNOs or mobile network providers with 2G/3G/4G mobile. Still, things became more difficult with the advent of 5G, given the huge amount of investment required to upgrade cellular wireless infrastructures. Then, the secular digital transformation trend got a boost from COVID-19 accelerated the migration from copper to fiber optics, again requiring money to be poured into civil engineering works.

The transition from old to new has not been easy, as exemplified by Orange's wholesale fees decreasing by 8.5% YoY in 2023 following the planned extinction of the copper network, thereby impacting operating revenue in France, its main market, which accounted for 40% of revenues last year.

At the same time, mobile virtual network operators (MVNOs) have emerged which have generally proved to be more agile with their ability to offer cheaper plans than established providers like in Spain where the competition in large part was due to Digi Communications. The MVNO has a wholesale agreement with Telefonica (TEF), for using the Spanish incumbent's physical network, and, after providing aggressive discounts, it has grown rapidly to now be positioned as the nation's fifth-largest mobile service provider. In this connection, Orange is second behind Telefonica, and Vodafone (VOD) is in third position in front of MasMovil which is privately held.

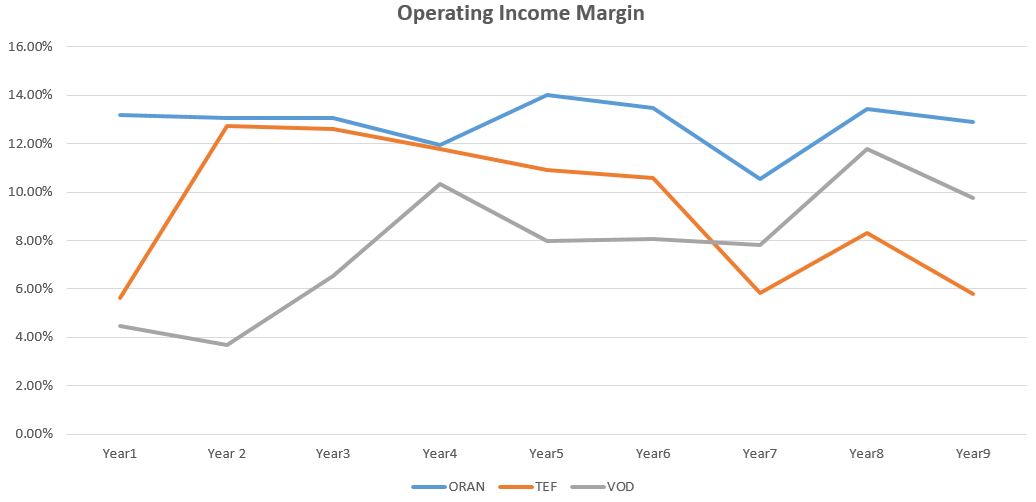

All this competition puts pressure on operating margins as shown in the chart below, which for Orange (in blue) has largely remained flat during the last nine years.

Charts built using data from (Seeking Alpha)

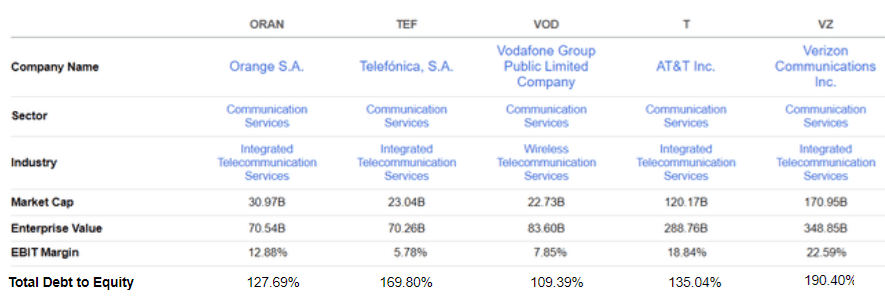

As for Telefonica, its margins have suffered a downtrend while Vodafone is the only one to see a net margin progression, but, at less than 10%, remains well below American peers AT&T (T) and Verizon (VZ) as tabled below. As per Digi's income statement covering the first nine months of 2023, its EBIT margin was 7.8%.

Comparison of key metrics (Seeking Alpha)

Thinking aloud, the U.S. telecom market has been through different stages of consolidation, with a high-profile one being the merger of Sprint and T-Mobile in 2020, which led to the latter becoming America's largest mobile wireless operator. This also gave birth to DISH Network (NASDAQ:DISH) which evolved from a satellite TV provider to become America's fourth nationwide wireless carrier after it agreed to buy some of the divested assets, thereby satisfying antitrust concerns.

Translating in the European context, the €18.6 billion Orange-MasMovil combination in Spain will reduce the number of wireless providers from four to three, thereby reducing the choice available to retail customers for mobile and fixed internet services. At the same time, it also opens the door for the expansion of Digi as the merger is conditional to spectrum frequencies being divested to the Romania-based company, allowing it to expand further into the Spanish territory, but this time by building its physical network.

However, to be realistic, spectrum licenses cost a lot of money and DISH has sought an extension to purchase T-Mobile's 800MHz holdings valued at $3.6 billion. Therefore, it will ultimately depend on Digi, which by the way already operates a physical network in Romania, but, still, building from the ground up (instead of hitching a ride on Telefonica's infrastructure as is the case currently) will take time.

Therefore, in the medium term, Orange and MasMovil should be the two winners as the 50-50 joint venture called LORCA JVCO will become the most significant player in the Spanish market, ahead of Telefonica. Talking capital allocation, the JV enables more synergistic investment in infrastructure both for FTTH and 5G, with above 450 million euros of synergies expected to be reached by the fourth year after closing. Now, spending less capex, for example to densify 5G network coverage or mutualize fiber works, can increase free cash flow.

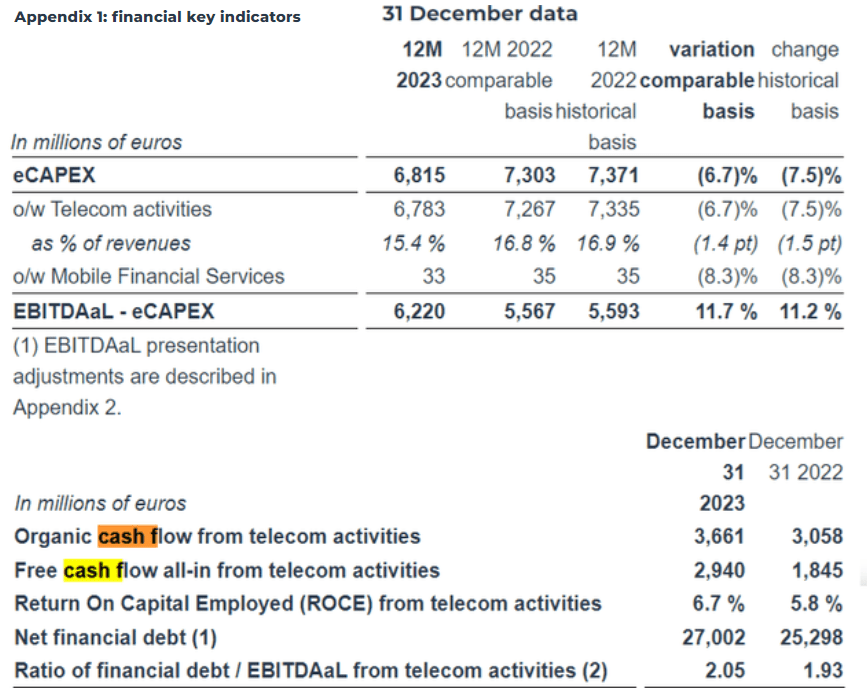

To further justify that the company is progressing on the free cash flow front, progress has also been made in terms of capex as a percentage of revenues, decreasing from 16.8% to 15.4%. Now combined with higher organic cash flow from telecom activities of €3,661 million (+19.7% YoY) FCF reached 2.9 billion euros at the end of last year, or an increase of 1.1 billion euros as tabled below. Moreover, these results have also been helped by €300 million of cost savings as part of the operational efficiency program elaborated when the new CEO took office, which includes a total of €600 million to be achieved by 2025.

GlobeNewswire

This means more cash available to make distributions to shareholders, in turn, reduces the probability of a dividend cut during the shareholders' meeting on 22 May 2024 when a decision on whether to pay 0.72 euros per share for FY-2023 will be made.

Moreover, in addition to spending on its passive tower infrastructure for hosting radio antennas for 5G, the existing ones are being monetized through TOTEM, Orange's European towerCo, and was one of the reasons for my bullish position when I covered the stock in April 2022. Hence, €686 million of TOTEM-related revenues were reached last year, with 16.6% coming from third-party customers (or not from Orange's internal usage). Now, considering that for United States Cellular Corporation (USM), 87% of tower revenues come from third-party rentals, Orange has a lot of potential to generate sales from other MNOs.

Consequently, given its progress with TOTEM, cost-saving efforts, fiber investments in France reaching a peak (maturity), and the eventuality of mutualizing capital spending in Spain through LORCA JVCO, Orange deserves better.

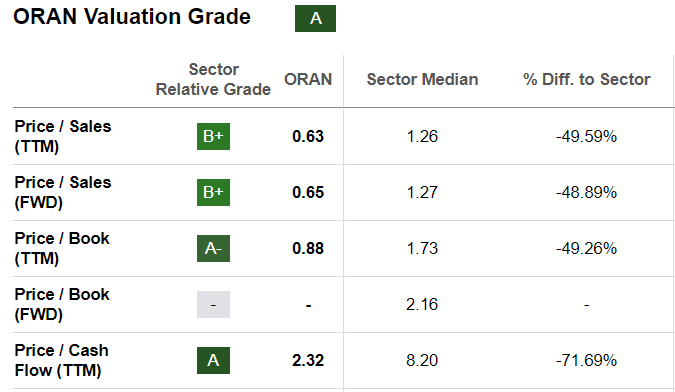

Now, this is already an undervalued stock, and its trailing price-to-FCF multiple of 2.32x is undervalued relative to the Communication Services sector by over 70% as illustrated below. Thus, applying a 20% upside on the current share price of $11.7, I have a target of $14. I consider this to be a fair price as the stock has already gained around 31% from October 2022, after the group initially signed the agreement with MasMovil. On top, the new strategic plan announced in February 2023 also helped to drive the upside.

Valuation Metrics (seekingalpha.com)

This said, till the management executes the merger, do not expect the company to continue growing at the same pace this year as the strategy to hike prices by one to two euros as was the case in 2023 cannot in all likelihood not be replicated this year given the highly competitive European market (including France) where Orange derives more than 65% of its revenues. For this matter, analysts' consensus estimates are for paltry growth in the 2024-2025 period. Along the same lines, with expectations for FY-2024 being downgraded from $48.22 billion to $47.67 billion on February 26, expect volatility in the near term.

However, growth opportunities should become more evident this year after Orange Belgium acquired VOO, a provider of video, voice, high-speed internet, and wireless services (or Quad play) for 1.8 billion euros in June last year. On the other hand, this caused debt to rise to $27 billion, as shown in the financial key indicators above. Now, this figure represents a debt-to-equity ratio of 127.69% which is within the range of other telcos as per the comparison table above. Equally important, despite the acquisition, the net financial debt to EBITDAaL (or EBITDA after leases) from telecom activities was 2.05x at the end of 2023, somewhat aligned with the target of approximately 2x. Moreover, this debt comes with an average maturity of 7.5 years and Orange disposed of 14.3 billion euros of liquidity at the end of 2023.

Now, it may need to contract some additional debt to fund the merger, including the restructuring of Orange Spain before filing for an IPO. However, in return, a €5.85 billion payment will be made to both Orange's and MasMovil's shareholders which will be mostly in favor of the French group on account of the individual levels of indebtedness of the two standalone entities. More importantly, as seen with T-Mobile's double-digit revenue growth and margin expansion in the aftermath of the merger, LORCA JVCO should boast superior financial metrics, implying its public listing in the $35 billion Spanish telecom market can unlock value for Orange. This regulatory approval, which comes about 7 years after a similar merger in the UK which would also have reduced the number of mobile operators from four to three, could indicate that more cross-border mergers are likely as the European telecom industry consolidates, infusing new dynamism in M&A activities.

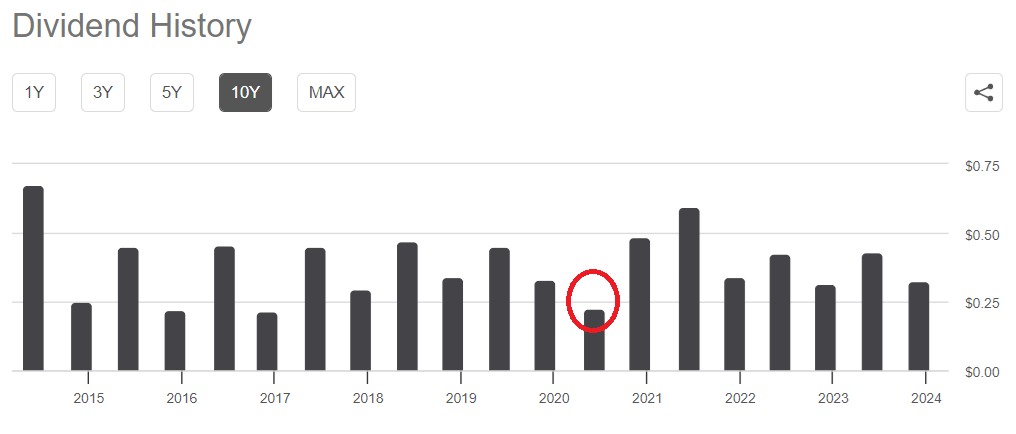

Finally and coming back to dividends, given that the current monetary environment may stay tighter for longer, Orange's semi-annual distributions to shareholders certainly have an appeal over other income alternatives like bonds, which tend to depreciate when the Federal Reserve keeps rates higher for longer. For this matter, Orange boasts a nice dividend history, not necessarily one exhibiting growth but more of a steady one. Moreover, as highlighted in red below, the last time it cut dividends was in June 2021 when it reduced the second payment as the French government called for moderation of dividend policies in light of the damages caused by the pandemic.

seekingalpha.com