Abandoned office building - surplus to requirements.

Wirestock/iStock Editorial via Getty Images

Abandoned office building - surplus to requirements. Wirestock/iStock Editorial via Getty Images

The overall office vacancy rate at the beginning of 2024 was 18.6%, a 30 year high, reflecting both reduced use and increased supply.

Barry Sternlicht, CEO of Starwood Capital Group, is widely reported to estimate that what was a $3 trillion office property market is now worth only $1.8 trillion, incurring $1.2 trillion in losses. Commercial real estate in general and the office market in particular can expect years of bad headlines as these losses are realized by landlords and lenders.

Share prices for traditional office REITs, particularly the large and popular names with investments focused on Class A properties in the central business districts of a few metro areas, are trading at 40-60% below pre-COVID levels.

This may be a "blood in the streets" opportunity, but the blood may get deeper yet, reaching 80%+ declines. An entry point coincident with maximum pessimism may occur within the next 12-18 months.

In this environment, an investor might require an 80% price decline from pre-COVID levels with the prospect of a 400% capital gain when/if prices return to pre-COVID levels, and at least a modest dividend.

This article was motivated by reading perhaps the third story in a week recounting the "disaster" in commercial office real estate "CRE" and lending. The fact that these stories are showing up in general news feeds suggested there might be an opportunity here.

There is a famous, if perhaps apocryphal quote, attributed to Nathan Rothchild, supposedly made when the outcome of the 1815 Battle of Waterloo was in doubt:

Buy when there's blood in the streets, even if the blood is your own.

However dubious the origin, it succinctly captures the idea of investing at the point of maximum pessimism.

I can personally attest to the power of this insight. I bought (in retrospect, far too little) First Industrial Realty Trust, Inc. (FR) in February 2009 at $3.85 per share. Things looked really, really bleak for industrial REITs at the time; FR was down over 90%. Today FR trades around $54, and my yield on cost is 38%. But it took over a decade for the share price to fully recover.

I've previously avoided the traditional office space REITs. While I don't expect to duplicate the FR results - the blood isn't nearly deep enough yet - perhaps there is enough to warrant some investigation.

Office REITs

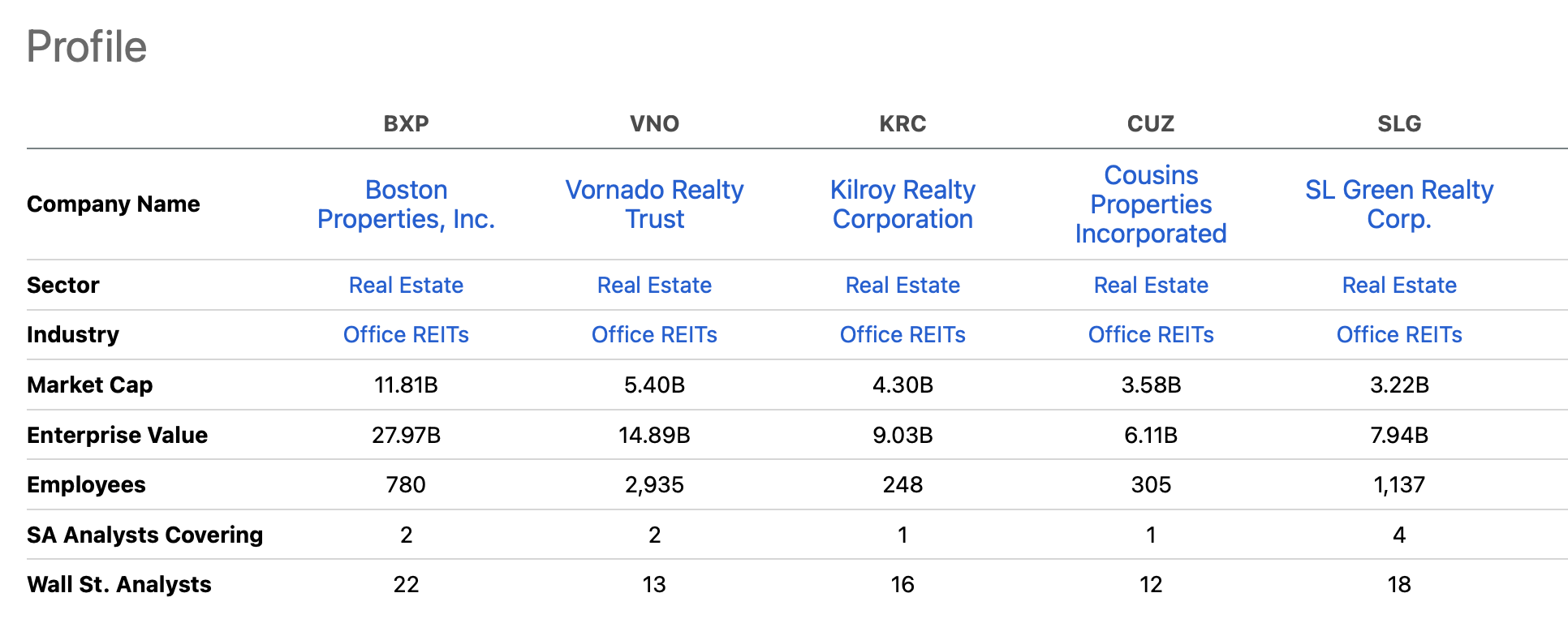

Seeking Alpha identifies 23 office REITs. The largest by market cap ($21 billion), Alexandria Real Estate Equities Inc. (ARE) is invested in biotech research properties, and is not really a traditional office REIT. Thirteen are small caps (less than $2 billion market cap), including several with an atypical focus such as government offices and post offices.

Excluding ARE, the five largest traditional office REITs by market cap are Boston Properties, Inc. (BXP), Vornado Realty Trust (VNO), Kilroy Realty Corp. (KRC), Cousins Properties Incorporated (CUZ), and SL Green Realty Corp. (SLG).

These have been the most familiar go-to names for investors with a desire to invest in office properties, and to keep this analysis manageable, we will limit our analysis to them. Seeking Alpha "SA" provides a useful comparison tool.

Comparison of Five Office REITs (Seeking Alpha 17 Feb 2024)

They fall between $12 and $3 billion in market cap. All are heavily followed by Wall Street analysts.

To give a sense of scale, as of 31 Jan 2024, Office REITs as a group constituted 4.7% of the Vanguard Real Estate Index ETF (VNQ), and BXP was 0.65%.

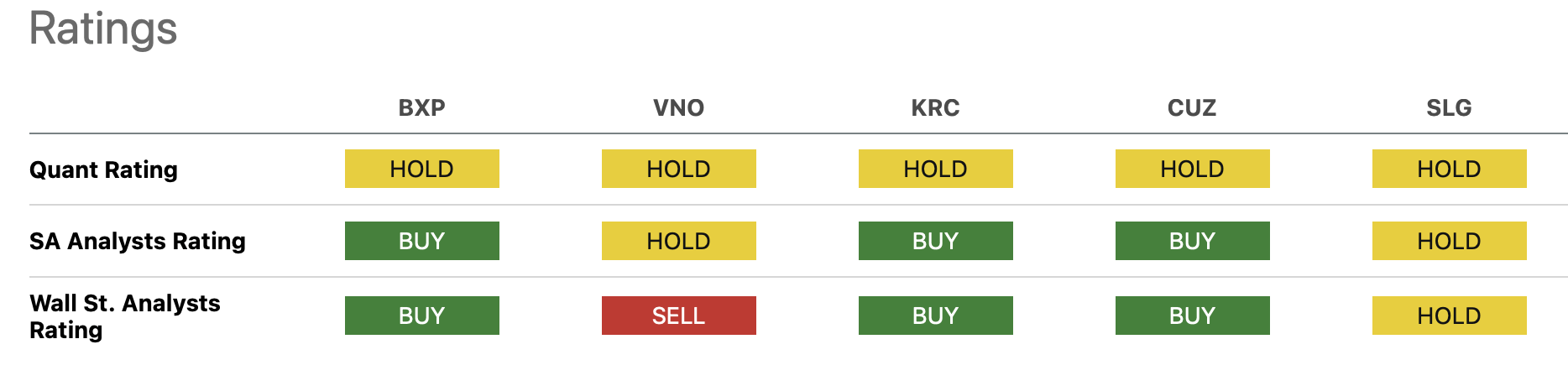

Enthusiasm for these firms is mixed.

Office REIT Ratings (Seeking Alpha)

Unless otherwise noted, most of the information below comes from the Q4 2023 supplementals and Q4 2023 earnings calls of the five firms.

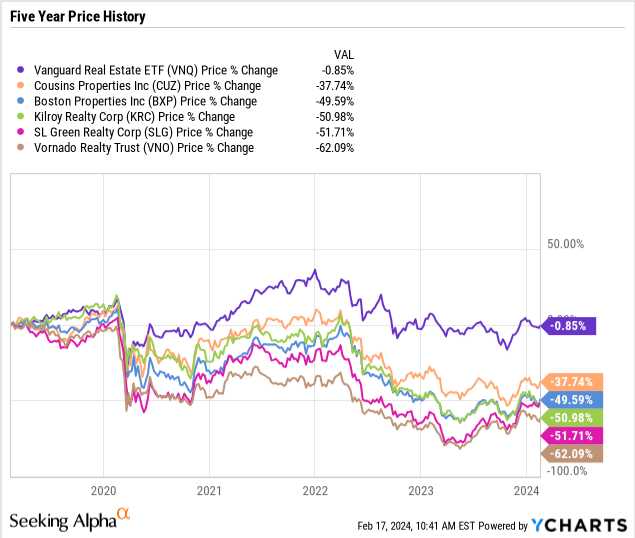

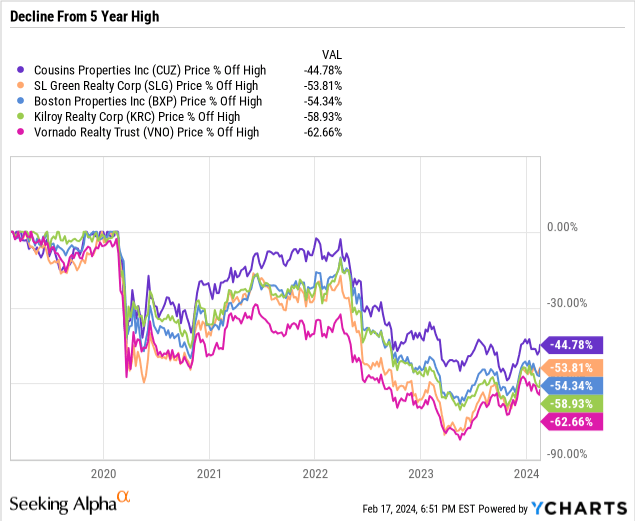

The market has not been kind to these REITs in recent years. The chart below shows the decline in prices for these five, plus the benchmark VNQ. The five-year period includes the 2020 COVID event and response and the 2022-2023 rise in interest rates.

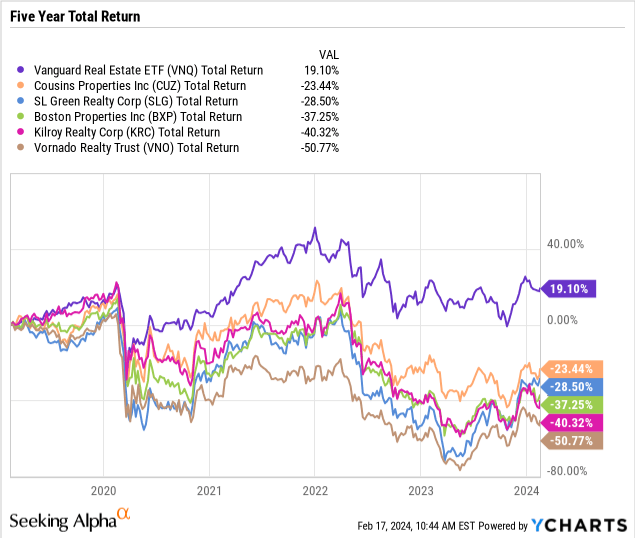

The Total Return story below is similar, mitigated somewhat by dividends.

Bear in mind that results in real dollars are significantly worse; the All Urban Consumers CPI has increased about 23% over this period.

The effect of increased interest rates, beginning in early 2022, is evident in both the charts above.

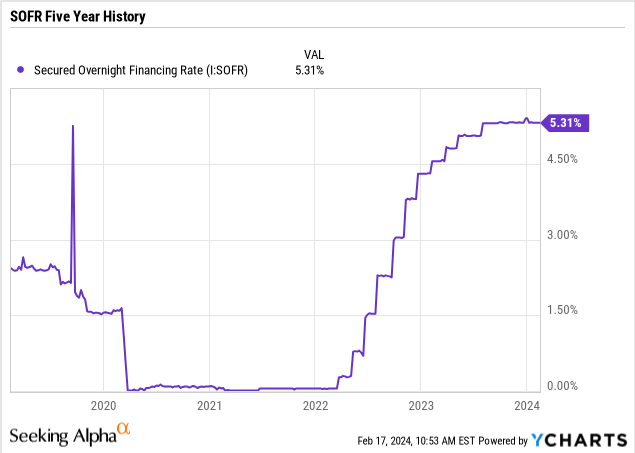

The Secured Overnight Financing Rate (SOFR), which serves as the reference for most variable rate real estate financing, dropped with the onset of COVID but subsequently rose to levels considerably above the pre-COVID level.

From the VNO earnings call:

... our results were negatively affected by the dramatic increase in interest rates. This will carry through next year but I expect will reverse as interest rates recede.

It's useful to discuss the nature of the traditional office real estate business and some of the issues that are impacting that business.

A Handful of Markets

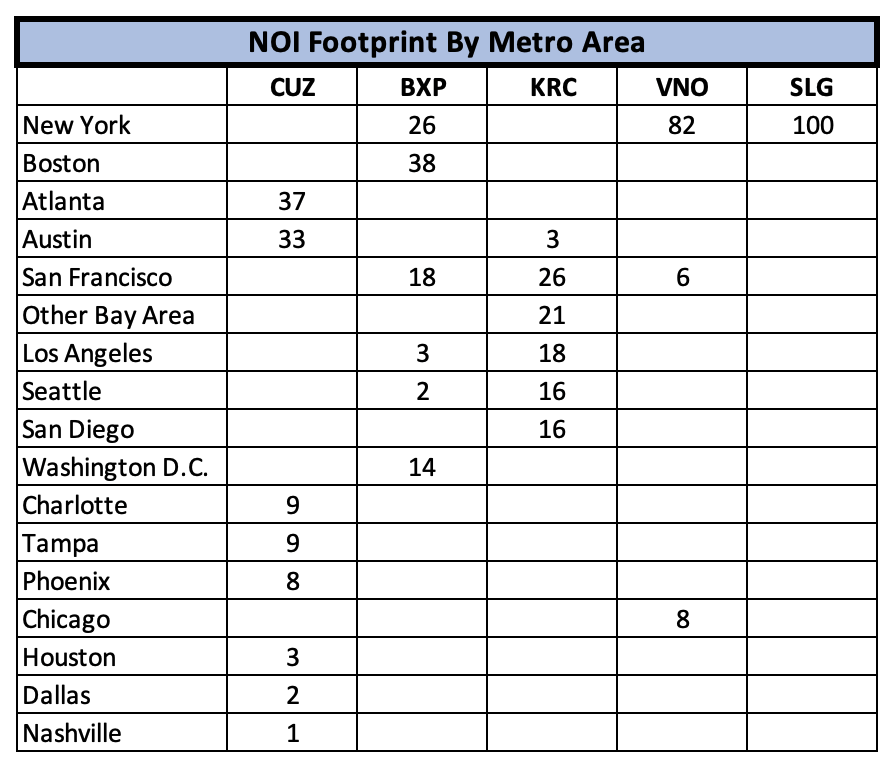

All five of these REITs are geographically concentrated in a handful of cities, largely in their central business district "CBD".

The table below gives a sense of the footprint of each REIT. (Note that these are fractions of net operations income (NOI) numbers for each company, and are not directly comparable in dollars across companies.)

Geographic Concentration (Company data, table by author)

SLG is essentially 100% New York City, and VNO is 80%+. KRC is 80% California, with 50%+ San Francisco metro. BXP is 80%+ Boston, New York, and San Francisco. CUZ is 70% Atlanta and Austin.

This provides a striking contrast to most other REIT sectors which highlight their geographic diversification across the states or top 50 metro areas.

Very Expensive Properties

Their assets are further concentrated in a relatively small number of very expensive properties. Two examples:

KRC's 2023 results press release noted a Q4 addition to their stabilized portfolio of "Indeed Tower, a $690 million, 759,000 square foot office building in the Austin CBD."

SLG announced the January 2024 sale of a retail condo at 717 Fifth Avenue for $963 million.

These Office REITs Are Not Uniformly Traditional Office

Several of these REITs have a material fraction of their assets in properties that are not traditional offices, with retail and life science providing the bulk of the diversification.

New York provided 85% of VNO NOI in 2023; 74% of NY NOI is office, 19% retail, and 2% residential. BXP is about 90% office, 7% retail, 2% residential, and 1% hotel. KRC is 65% office, 25% life science, and 10% mixed use.

The Enabling Impact of Technology

Improvements in telecommunication bandwidth, processing power, video camera and display capability, and software to support distributed workflows combined to increase the ability to work effectively outside the office.

Technical capability reached a tipping point a few years ago, and was confirmed by widespread user experience during and after COVID. This altered office worker expectations and preferences.

This plays out both in reduced office space requirements for many companies, and in the ability to locate many back office functions in lower cost, potentially remote, facilities.

While the REITs are quick to point to increased demand for space from AI developers and providers, the impact on tenants who are AI consumers may prove equally or more significant. This January 2024 paper Better Call GPT, Comparing Large Language Models Against Lawyers suggests the impact could be material.

LLMs (Large Language Models) can outperform humans in accuracy, speed, and cost-efficiency during contract review. Our empirical analysis benchmarks LLMs against a ground truth set by Senior Lawyers, uncovering that advanced models match or exceed human accuracy in determining legal issues. In speed, LLMs complete reviews in mere seconds, eclipsing the hours required by their human counterparts. Cost-wise, LLMs operate at a fraction of the price, offering a staggering 99.97 percent reduction in cost over traditional methods.

Fewer Days in the Office May Impact Vacancy

The technical ability for many office workers to work remotely may have permanently reduced office attendance and space requirements. Many of the firms pushing for a return to office are expecting only three of four days in the office. CNN reports January 2024 Conference Board survey results that only 4% of CEOs are prioritizing a full return to the office, and that a hybrid 3-days-a-week schedule is common.

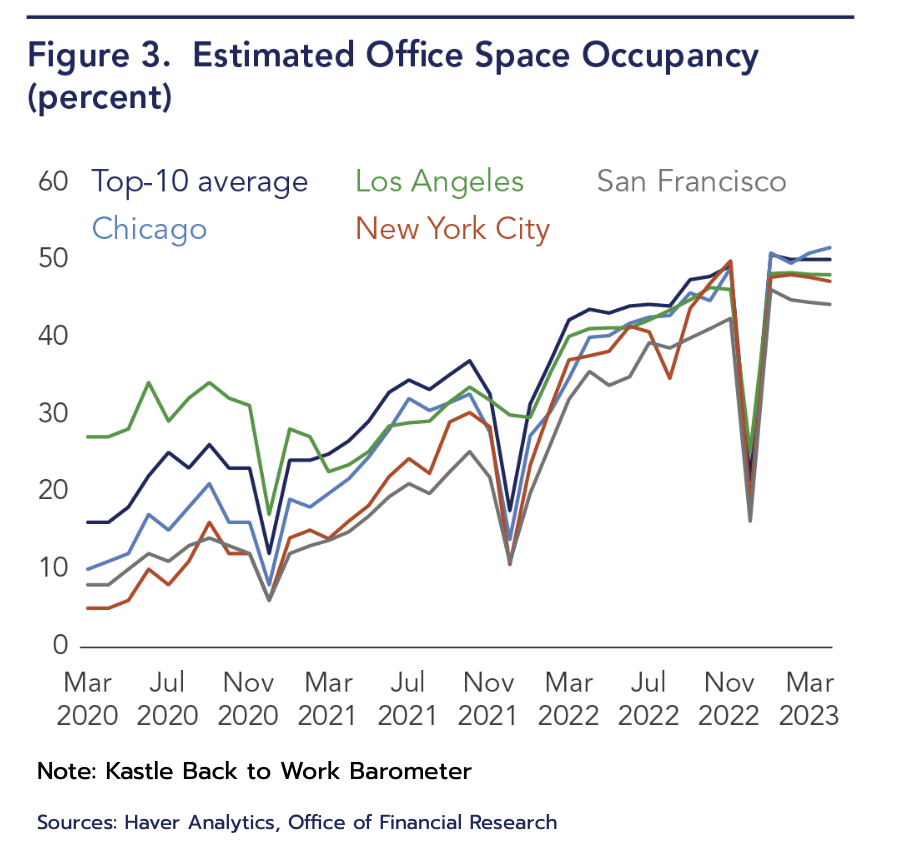

The U.S. Treasury's Office of Financial Research posted a blog comment on Office Sector Metrics in mid-2023. One of the key points they make concerns office occupancy.

Although the current office vacancy rate is 16.4%, the average occupancy rate measured by the Kastle Back to Work Barometer is 49.8% (weekly average). This implies a structural vacancy rate of 50.2%. Prior to the COVID-19 pandemic, office occupancy averaged close to 100%.

As the figure below shows, key card access data demonstrates that office occupancy in large metros has picked up from the abysmal levels during COVID, but is still far below capacity.

Estimated Office Occupancy (US Treasury)

The impact on vacancy is uneven. An April 2023 CBRE analysis of the hardest hit buildings (HHB) found that 10% of buildings accounted for 80% of 2020-2022 occupancy loss. HHBs were more likely to be downtown, particularly in the Pacific and Northwest, and in areas with higher crime rates and fewer neighborhood amenities. HHBs were not older than the general office inventory, with the majority built from 1980-2009.

The January 2024 National Office Report by Commercial Edge provides a great deal of detailed information on regional and metro markets - vacancy rates, costs per square foot, construction, etc. to support additional due diligence.

Mortgage Debt Outstanding is Very Large

The mortgage debt outstanding on CRE is very large, and a lot of it is maturing this year and next.

The Mortgage Bankers Association released an analysis on 12 February 2024 indicating that "twenty percent ($929 billion) of the $4.7 trillion of outstanding commercial mortgages held by lenders and investors will mature in 2024, a 28 percent increase from the $729 billion that matured in 2023. Among loans backed by office properties, 25 percent will come due in 2024."

A December 2023 National Bureau of Economic Research "NBER" paper notes that "about ... 44% of office loans appear to be in a "negative equity" where their current property values are less than the outstanding loan balances. Additionally, ... the majority of office loans may encounter substantial cash flow problems and refinancing challenges.

The NBER paper concludes that "CRE distress can [put] ... over 300 mainly smaller regional banks ... at risk of solvency runs".

One can see why the banks might be very nervous about renewing or adding loans for office property, as well as other CRE. The problems may be severe enough that the collateral damage will impact even normally credit-worthy firms.

From the VNO call:

And most office loans [in the general market] will have to be restructured or extended as they aren't refinanceable at their current levels. More broadly, lenders have no appetite for construction financing across most property types.

BXP and KRC were noted by JP Morgan on 20 January as particularly at risk from a "higher for longer" interest rate environment.

The Urban Doom Loop

San Francisco is often cited as an example of the "urban doom loop" - the amplifying feedback loop between declining office occupancy and the decline in civil order and amenities.

A search for "companies leaving San Francisco" will yield dozens of articles detailing the impact.

This June 2023 local ABC News analysis of downtown recoveries ranked San Francisco last among 63 cities, based on cell phone activity, compared to a 2019 baseline.

CNN reported in August 2023 on the issues facing downtown San Francisco, including a comment from a Westfield Mall spokesman:

A growing number of retailers and businesses are leaving the area due to the unsafe conditions for customers, retailers and employees, coupled with the fact that these significant issues are preventing an economic recovery of the area.

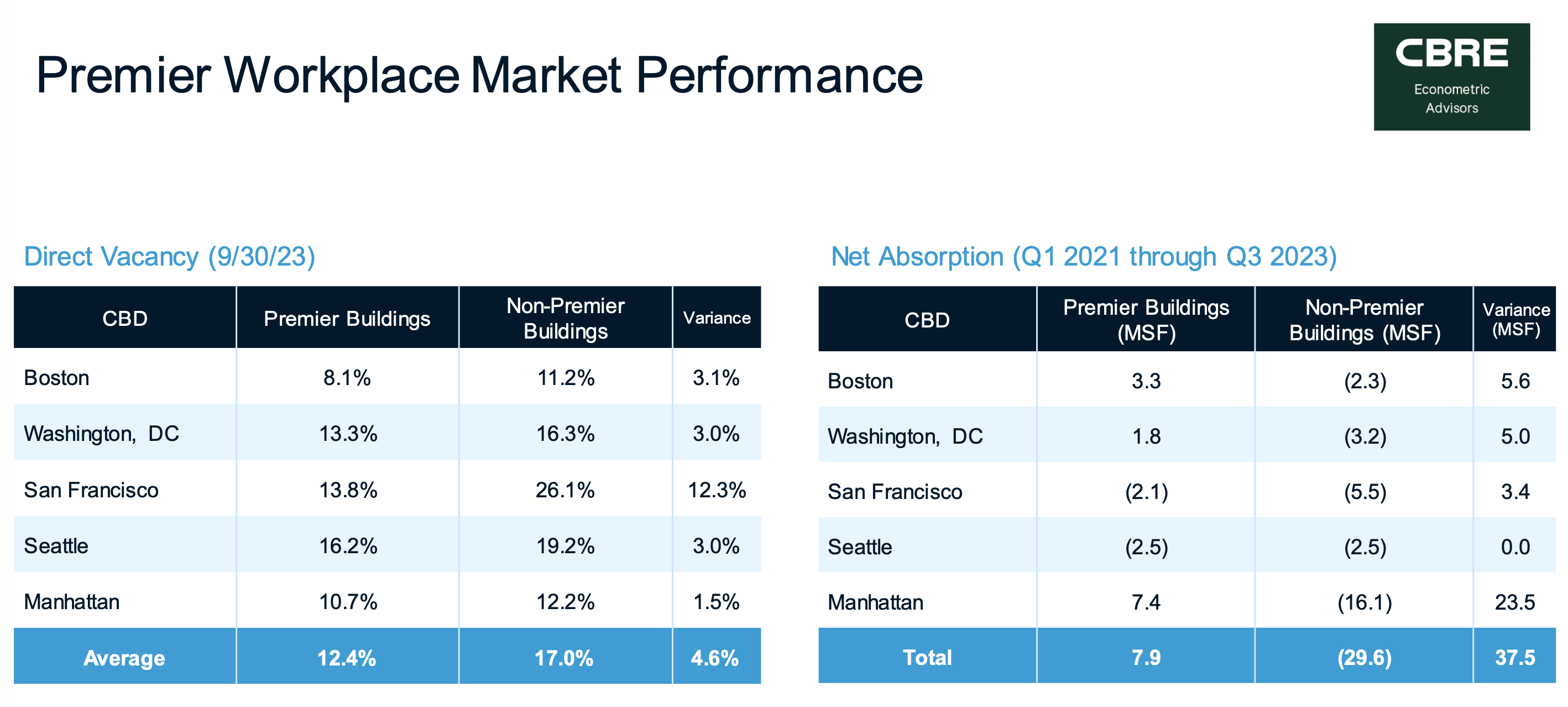

BXP's Q3 Investor Presentation notes the lower vacancy rates and higher absorption for premier vs. lower tier other properties; San Francisco's lower tier is particularly weak.

Relative Performance of Premier Class Properties (BXP Q3 2023 Investor Presentation)

It's not just office, there are issues with multi-family as well. The Mosser Company (with about 75% of its 3,000 unit portfolio in San Francisco) defaulted in August 2023 on a 2018 loan for $88 million, covering 12 properties appraised at $154 million, and with 94% occupancy, at the time of the loan. In January 2024, occupancy was 82%, and the lender is trying to sell the properties. Mosser is not unique; The San Francisco Chronicle also notes that last year multi-family operator Veritas defaulted on $1 billion in loans tied to dozens of its buildings.

Regardless of what weight an investor assigns to this effect, CBRE Group, Inc. (CBRE) reported that "the San Francisco office market closed Q4 2023 with an overall vacancy rate of 35.6%, and net absorption of negative 1.25 million sq. ft."

There Are Options to New York City and CBD Office Towers

Although there is considerable institutional inertia, there are in fact options to both New York City and CBD office towers. As one example, Charles Schwab moved its headquarters from the San Francisco CBD to a custom built campus in suburban Dallas in 2019. Initially 2,500 people, the campus is sized to support 6,000.

Schwab is not alone. This August 2023 NY Post article reports that "158 Wall Street firms have moved their headquarters out of New York since the end of 2019, taking nearly $1 trillion in assets under management with them". A similar migration of assets occurred from California. Motivations include lower taxes and a 40% lower cost of living for employees.

Management Outlook Appears Generally Optimistic

Despite the issues outlined above, management is generally optimistic. I reviewed the Q4 2023 earnings calls of all five companies. My impressions here are admittedly subjective, and reflect my preference for direct and detailed comments and answers.

The CUZ call was excellent, directly responsive to questions, and with a lot of detail.

BXP was very professional; calm, transparent, and grounded in a lot of data.

I found the KRC call enthusiastic but vague.

The SLG call was positive, but often seemed to be a non-specific "we are working on it". The call was dominated by SLG's reported "acquisition of interests in the JV that owns the leasehold interest at 2 Herald Square for no consideration, increasing SLG's interest to 95%", i.e. the JV partner basically appeared to give it to them for nothing. Multiple analysts asked for clarification on this deal and its implications, and I don't think they got it.

I was not impressed with the VNO call; it was a missed opportunity to crisply make their case, and left me with the impression that they feel the assets are so good they speak for themselves. They were the only one of the five REITs that did not offer 2024 guidance.

A few specific comments from the earnings calls:

From CUZ:

First, the return to work in lifestyle office properties is accelerating. As a result, our parking garages are filling up and demand for our space is increasing despite higher professional layoffs.

Second, there is little to no customer or capital demand for old and tall CBD towers or suburban commodity properties. Many of these buildings will stagnate until they are repurposed or torn down. The process has already begun.

In the short term, the narrative for the office sector is likely to get worse before it gets better. Media will focus on high vacancy rates and accelerating loan defaults, and this reporting will not be wrong. However, it will be an overgeneralization that conflates commodity office with lifestyle office.

BXP's noted that:

The bifurcation of client demand between the East Coast and the West Coast continues to be very wide. San Francisco, West L.A. and Seattle are dependent on technology employers. Traditional technology demand growth continues to be weak and more times than not renewing technology clients are reducing their lease premises.

Regarding the limited amount of new development, BXP said:

Current market rents and concessions associated with available existing space don't support new office development.

Everyone has a view on the timing and depth of Fed Red rate cuts, but if SOFR goes to 4%, construction financing, if you can arrange it, is still going to be very expensive and a significant drag on new construction starts.

The VNO call made a similar point:

And in the end, the supply-demand equation will come into balance and bring on a landlords market by a total cut-off of new supply. You can't build anything in these frozen capital markets. And in New York, the evaporation or [ir]relevance of, say, 100 million square feet of old, obsolete, unrentable space.

VNO also said:

"We expect 2024 will represent the trough in our earnings."

"We will not make acquisitions of conventional office at full pricing. We will only be a buyer at ... distressed prices for office building. And we will only buy the finest of building."

"At this time, it's a financial policy of our Board to pay out the minimum dividend because from a capital allocation point of view, that's the right decision."

VNO was paying a $2.64 dividend pre-COVID. In 2023, they paid $0.375 in January and $0.30 in December. VNO plans to pay one dividend in 2024, with the amount to be determined.

One might expect that the senior management of New York City centric real estate would attract people with an enthusiasm for New York City. However I find it hard to assess how much of this enthusiasm is dispassionate business judgement vs. talking their book.

FFO Projections Going Forward

One way to quantify how optimistic they might be is to look at FFO projections.

CUZ: 2023 FFO/share $2.62, down from $2.72 in 2022. Projected $2.57-$2.67 for 2024 (flat Y/Y, down 4% from 2022).

BXP: 2023 FFO/share $7.28, down from $7.53 in 2022. Projected $7.10 FFO/share for 2024, (2.5% decline Y/Y, down 9% from 2022).

KRC: 2023 FFO/share $4.62, down from $4.68 in 2022. Projected $4.18 FFO/share for 2024 (9% decline Y/Y, down 11% from 2022).

SLG: 2023 FFO $4.94, down from $6.64 in 2022. Projected FFO $6.05 for 2024, (22% increase Y/Y, down 9% from 2022).

VNO: 2023 AFFO/share $2.61, down from $3.15 in 2022. No guidance for 2024.

I will assert that traditional valuation metrics are more useful in a relatively stable environment. Almost by definition, these metrics are less useful for our "blood in the streets" thesis.

So the approach I've adopted here is to assume that the pre-COVID prices were reasonable (what I'll refer to below as the Base Price), and look at prices relative to those Base Prices.

The chart below shows the declines from the pre-COVID highs, which range from 45%-63%, as of 17 February 2024.

Short Interest

The variance in short interest among these five stocks is fairly high, and I would argue to give that variance some weight- it reflects the assessments of investors willing to put money on the table. SLG and VNO appear particularly unloved, which is consistent with the Ratings summary near the top of this article. I should note that I pulled the data below from Seeking Alpha about 10 days ago, and that short interest data is not currently available for these stocks.

Short Interest for Office REITs (Seeking Alpha)

Normally, I would find it hard to be very enthusiastic about investing in these REITs.

Generally, investors should expect a steady drumbeat of bad news for office real estate in 2024 and 2025 - assets sold at very large discounts, and real estate loans marked to market with significant adverse impact on lenders. There is a large overhang of vacant space and problematic loans.

Second tier properties and landlords, and their lenders, will be under particular stress for years.

The CEO of CUZ, in response to a question in the Q4 Earnings Call, commented on the fate of office properties less prime than theirs:

I'd say if I had to characterize it today, you're seeing more suburban office, commodity office product, being purchased at a very low basis and that product ultimately being torn down to be replaced with multifamily residential and mixed-use type properties. And I'd say the larger, older towers.

The Class A or better office market where these five RETIs focus has at least one more challenging year. That may be too optimistic.

Quantifying The Investment Thesis

But our basic thesis is that we want to buy at the point of maximum pessimism, in the expectation that this degree of pessimism is unwarranted.

I define this as an 80% decline. I would argue that's not unreasonable, in fact, VNO and SLG touched that point in March 2023, when I wasn't paying attention. If the stock prices regain their pre-COVID Base Price, that would yield a 400% capital gain, sometimes described as a 5-bagger. This price recovery may take years; it was 10 years with the FR example I gave.

In any case, buying at that price point should provide some margin of safety. As an additional margin of safety, I'd like at least some dividends, although I would expect at least some dividend cuts (VNO and SLG have already cut their dividend).

To be explicit, the assumptions for this article's investment thesis are:

A less dramatic alternative criteria might be considered:

Based on performance to date, and shorting levels, the market appears to put CUZ in a different class than the other four stocks. The alternative criteria might apply there. Note that CUZ touched that point in 2023.

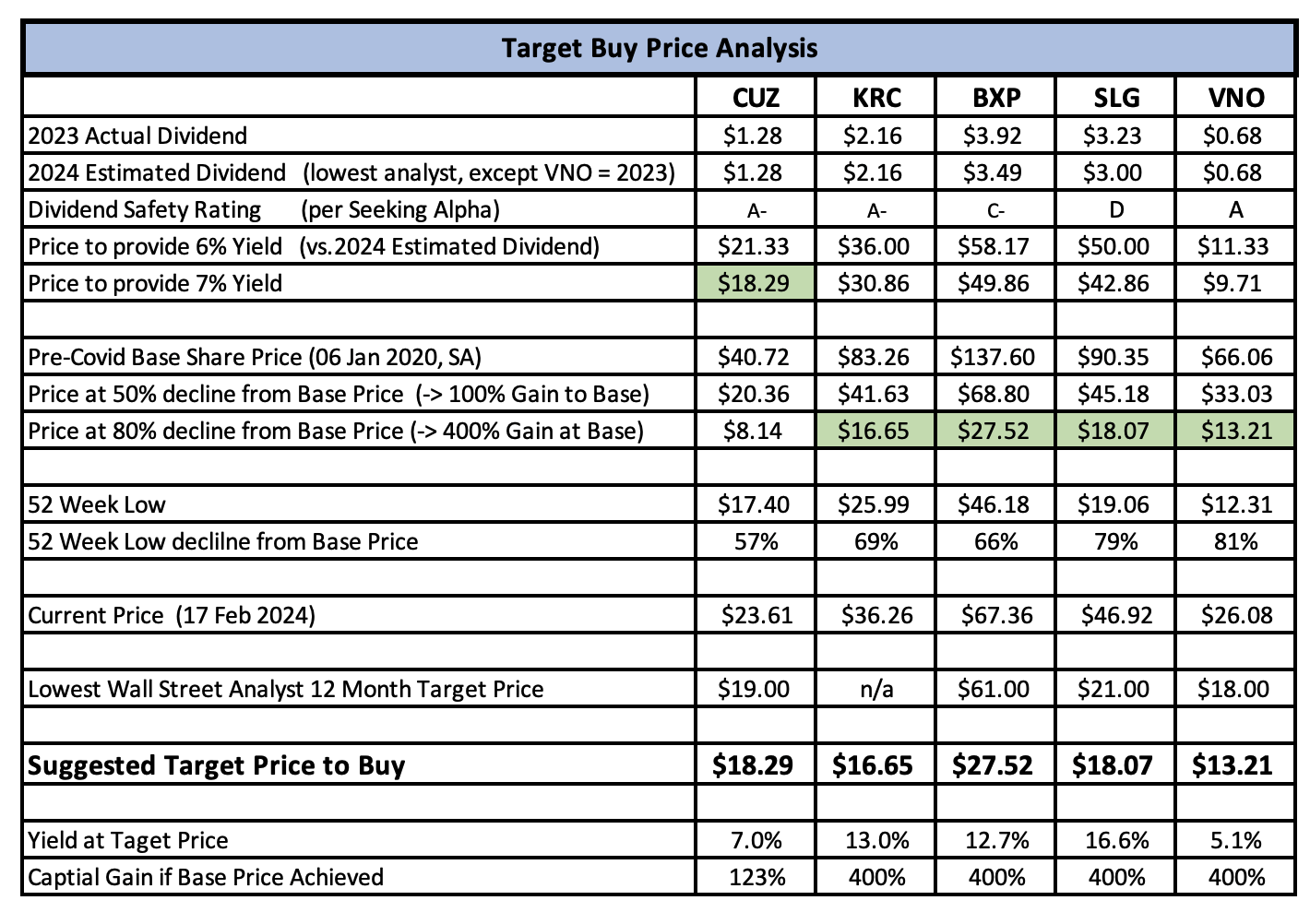

The table below runs some numbers for this, showing the buy price required to generate a 7% dividend from the estimated 2024 dividend, and the buy price required to generate a 100% and 400% capital gain if the stock returns to pre-COVID Base Price levels (I used the 06 January 2020 price for this, which SA conveniently provides.).

For the 2024 dividend, I've used the lowest analyst estimate, again from SA, except for VNO, where I used the 2023 value. I included the SA dividend safety rating. In addition, I've included the 52 week low for each stock.

The green shaded cells indicate the key buy criteria.

Target Price Analysis (Seeking Alpha data, table by author)

The buy prices are roughly half the current prices, which is the kind of behavior one sees with 80% declines. Patience is a virtue here.

There are two obvious risks to this thesis that should be noted.

First, the 80% decline may not occur. Both SLG and VNO are currently up significantly from their March 2023 lows.

The Federal Reserve is very widely expected to reduce interest rates this year, which will be a boost to REITs. Opinions vary considerably on the timing and extent of interest rate cuts. In January, Bankrate.com expected only two 25 basis point cuts, but thought markets were expecting six.

Second, prices for traditional office REITs may not recover to or near pre-COVID levels. My thesis suggests it may take up to 10 years, but even that might be too optimistic. And there is a long list of potential problems beyond those already discussed.

There could be a large and long term general market decline (the S&P is now at record highs). The REITs or the office market might be weaker than is currently apparent, and force mergers, stock dilution, etc. that will destroy value. Tax or regulatory changes that are particularly adverse for office REITs or CBDs could occur. Landlords may not be able to convince people that even great amenities - snacks, gyms, and rooftop cafes are often mentioned - justify a commute.

I'm not too concerned about the first risk. I think there is going to be a LOT of bad news for office REITs over the next year; this systematic attack on sentiment is really at the heart of the thesis. And if the buy point is never reached, there will be no capital invested and at risk with this thesis. There will be opportunities elsewhere.

The second risk is real, but I think buying at 80% off and setting an expectation for a 10-year recovery period reasonably mitigates that risk. Even if prices only recover to half of pre-COVID levels, it's still probably not a bad deal.

The large traditional office REITS, focused on the top tier of properties in a literal handful of markets, have seen share prices decline ~ 40-60% from pre-COVID levels.

Headwinds including fewer days in the office for many workers, the need to refinance a large amount of debt at higher rates, and a less attractive environment in some cities.

A steady drumbeat of negative news is likely over the next year or two. The point of maximum pessimism - and lowest prices - probably lies ahead.

There may be an opportunity for a prepared investor to achieve significant alpha if prices reach "blood in the streets" 80% declines, indeed two of these stocks touched that point last year.

CUZ and BXP would probably be my preferred long-term holdings, but the SLG and VNO footprints probably provide the best fit to the "blood in the streets" thesis.

I would rate all of these REITs as hold currently.

Personally, I now own only ARE of the large cap office stocks. After doing the research for this article, I put all five of these REITs on my watch list.